Sorting the micro from the macro in Emerging Markets

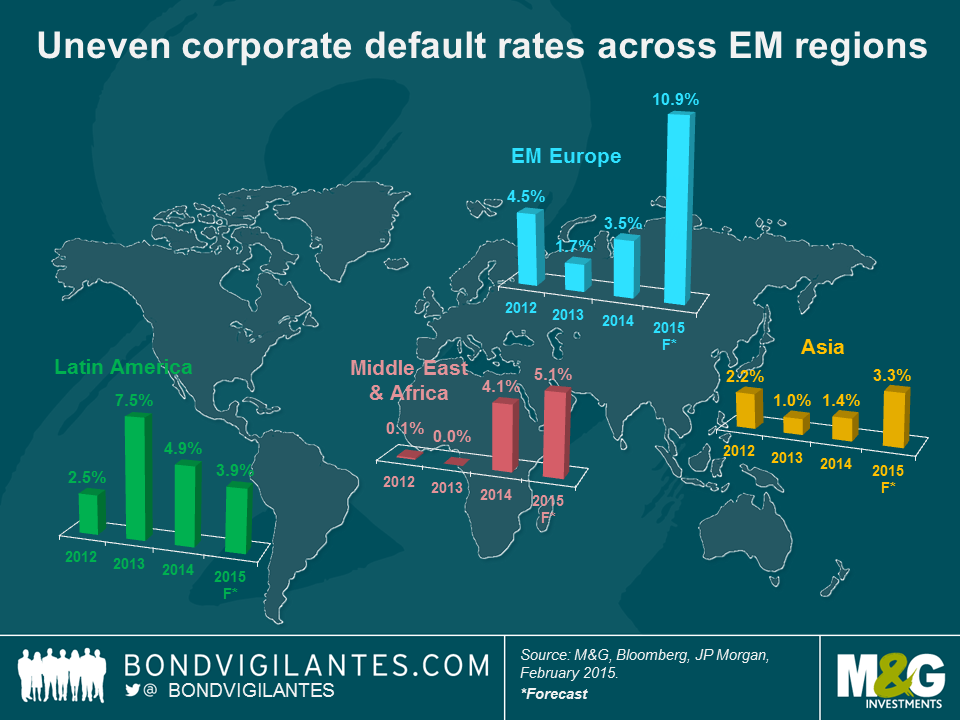

While generating a lot of concerns, one of the benefits of the strong growth of the emerging market (EM) corporate bond universe in the past decade has been the diversification of issuers. The asset class, which at $1.6 trillion is now larger than the US high-yield market, offers a vast number of countries and industries to invest in. Contrary to the EM rhetoric that has been making headlines in 2015, not all emerging countries are experiencing a softening in economic growth: India’s economic outlook is positive and Central America is benefitting from a stronger US economy. Likewise, a number of corporate exporters that have US dollar revenues but domestic costs are actually benefiting from weakness of local currencies against the dollar. In addition, credit quality and default risk is uneven across regions, as per the chart below. There are significant opportunities for the EM corporate bond stock pickers out there.

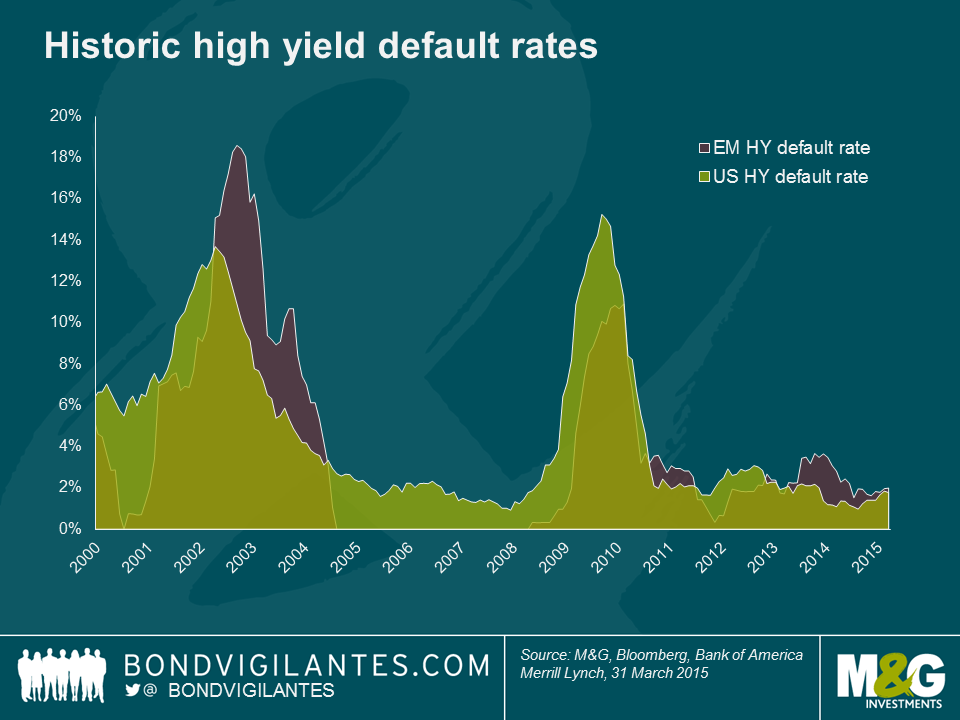

Interestingly, EM corporate defaults have historically been in-line with those of the US high-yield market and follow similar economic cycles. Since the beginning of the year, at least seven EM corporate issuers have defaulted. In the same period, 20 US and 7 European and other developed market issuers defaulted in the bond market.

As is often the case, region and country selection is paramount when investing in the EM world. In addition, assessing the impact of macroeconomic factors on EM corporate creditworthiness is a critical component of the investment process. For example, Argentina, Brazil and Mexico account for over 42% of all EM corporate defaults in value since 2000. These countries have defaulted multiple times on their sovereign debt obligations, proving that when the creditworthiness of the sovereign deteriorates significantly it is very likely that the corporate will encounter difficult times too. In general, an actual (or likely) sovereign default or a sharp deterioration of economic conditions would likely prompt a number of corporate issuers to either (i) opportunistically restructure debt, like the Ukraine-based iron-ore pellet producer Ferrexpo (which in February 2015 launched an exchange offer of its $500m 2016 bonds with new terms), or (ii) literally go bust on the back of an unsustainable economic environment (as has been the case many times for Argentine corporates in the past).

Sometimes, there is a very fine line between sovereign and corporate. Kazakhstan illustrates this point. While Kazakhstan has never defaulted on its sovereign debt, the 2010 restructuring of $16.6bn of government-controlled BTA bank of Kazakhstan – which led to a 70% haircut on creditors – was seen as a sovereign default and seriously tarnished the reputation of the country with investors.

These factors do not mean that EM investors should use a top-down approach only and avoid emerging countries with poor macro dynamics in order to limit corporate default risk in their portfolio. For example, Russian corporates are currently facing a very challenging macroeconomic environment but their solid credit fundamentals and export-driven nature have been acting as a buffer to these poor economic conditions. EM credits can also default due to bottom up factors, unrelated to the health of the local economy. For example, Brazil’s sugar and ethanol producer VGO defaulted this year due to industry and company specific factors – record-low sugar prices resulted in significant cash burn and a weak liquidity position, triggering unsustainable short-term refinancing risk.

In 2015, there is very little doubt that default rates will increase in the emerging market corporate universe and sorting the micro from the macro will be even more important than it was in 2014. Fundamentals have deteriorated and credit rating downgrades outpaced upgrades in 1Q15. Nonetheless, I still think that EM debt is attractive. Macro risks have fallen since the beginning of the year, and the high yields on offer in the marketplace mean there are opportunities for investors to generate decent returns.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox