Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

The euro’s 12-year low against the dollar is a mixed blessing for US companies. On the one hand, the US manufacturing sector is suffering from an uncompetitive currency and lower export revenues. But on the other, rock bottom European interest rates have given US companies an attractive opportunity to issue bonds denominated in euros and lock in cheap financing. For example, in the first quarter of 2015 €27bn worth of “reverse yankee” bonds were issued by US corporates aiming to exploit low interest rates ahead of a potential interest rate hike by the FOMC later this year. Word on the street is that there is a backlog of issuance waiting to come to market should there be a resolution to the situation with Greece and its creditors.

Bond issuers aren’t the only ones that can take advantage of the trend to issue in euros. Given that many European government bonds have ultra-low interest rates by historical standards; bonds issued by US corporates have also become quite attractive for fixed income investors looking for higher yields. Those with a flexible investment strategy may therefore be able to exploit cross-market discrepancies across global corporate bond markets today.

In this edition of the M&G Panoramic Outlook, Wolfgang Bauer – deputy fund manager, gives his views on corporate bond valuations, explores historical changes in spread differentials between USD, EUR and GBP credit and explains how global fixed income investors can exploit attractive yield pick-up opportunities.

Please click here for the M&G Panoramic Outlook web page.

Deflation. Liquidity. Greece. These are the words of 2015 if you are a bond investor. The year started off with a bang, or rather a break, when the Swiss National Bank (SNB) announced the surprise abandonment of the peg with the euro. This was only a mere week before the European Central Bank (ECB) embarked upon an historic quantitative easing programme. Deflation took hold in Europe, government bond yields fell to historic lows, and the US Federal Reserve did nothing.

Fast forward to today, and it seems like we have lived through a full market cycle in only six months. Government bond yields have risen as the European economy has improved; the Greece political situation has also weighed on investors’ minds. In the UK, we had a surprise result in the General Election as investors granted the Conservatives a majority in parliament. And in the US, the undeniable strength of the US labour market may finally be translating into higher wages, leading many to expect the first FOMC rate hike since 2006.

In this edition of the M&G Panoramic Outlook, Jim Leaviss – Head of Retail Fixed Income, gives his views on bond markets and the global economy for the remainder of 2015. Some of the topics covered include credit valuations, bond market liquidity, and global currency markets.

Please click here for the M&G Panoramic Outlook web page.

I have heard it said, semi-seriously, that the biggest risk for the Eurozone isn’t that Greece leaves the single currency and its economy collapses, but that it leaves and thrives. In this scenario Greece starts again, debt free, able to adapt fiscal easing rather than austerity, and with a devalued “new drachma” encouraging an influx of tourists and a manufacturing and agricultural export boom. When the other indebted and austere European nations see the benefits of leaving the euro, they do so, leaving their debts behind and causing the complete breakup of the European Union as we know it (and the second Great Financial Crisis in a decade?). One parallel that’s drawn regularly is that of the 2002 Argentinian devaluation, and subsequent economic recovery. We wrote about the similarities between the two economies a couple of years ago, here.

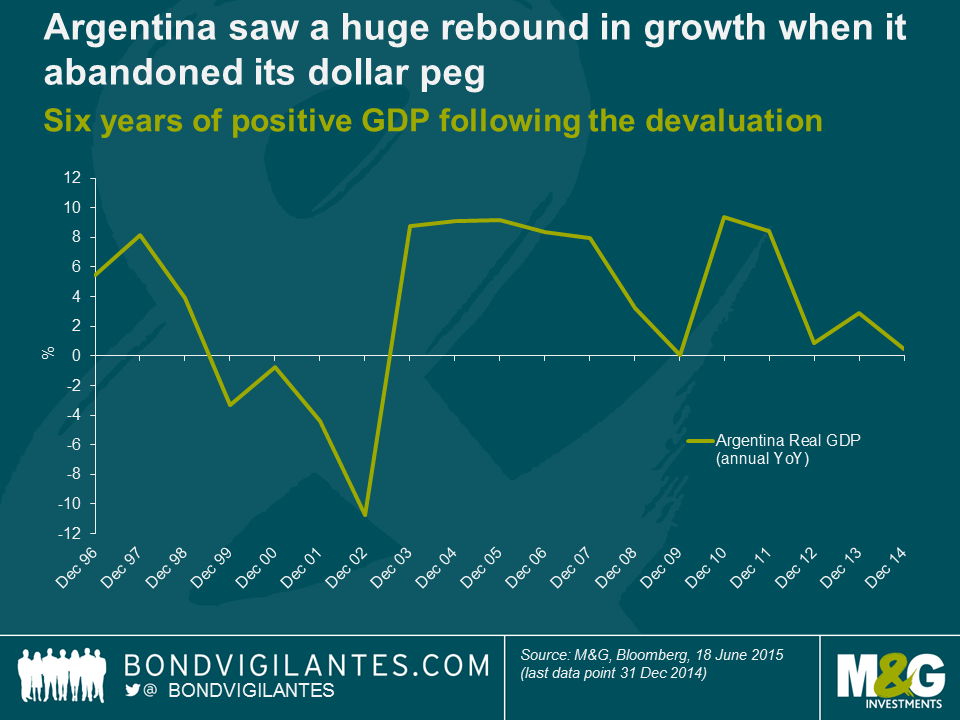

From four years of negative annual rates of GDP growth (at worse over -10% per year), Argentina bounced back to see positive GDP growth of high single digits per year for five years when it left its currency straightjacket. Could we expect Greece to experience the same sort of economic rebound if it left the eurozone that Argentina experienced after abandoning its peso-dollar parity peg in January 2002?

Argentina Real GDP (annual yoy)

There are many economic similarities between the Argentinian and Greek crises; the overvalued currency pegs; unsustainable government debt burdens and IMF involvement; poor tax collection; dubious statistical accuracy and high unemployment. Following the hyperinflation of the 1980s, the Argentinian peso was pegged to the US dollar. Inflation fell dramatically, and this stability and stronger currency led to a boost to domestic living standards and a big rise in imported goods; but there was also capital flight as many realised the peg might not hold forever. The current account deficit soared. In 1999 as the economy slowed from a period of growth, Argentinian unemployment hit 15% and the public debt started to rise alarmingly. External debt hit 50% of GDP, and the IMF told the government that it needed to implement austerity in order to access funds. Market interest rates almost doubled to 16% and Argentina’s credit rating was cut to weak junk (there was subsequently a debt restructuring). Eventually the IMF refused to release new funds as the government hadn’t kept to its budget deficit targets. By the end of 2001 bond yields were 42% above US Treasuries and bank accounts were all but frozen (the “corralito”) to stop bank runs. Amid political chaos and riots (rising inequality had been another feature of the economy) – and the lack of circulating dollars – there emerged alternative IOU currencies issues by municipalities (Claudia Calich here has some “patacons” issued by Buenos Aires, we tweeted pictures on @bondvigilantes if you want to see one). In January 2002 the dollar-peso peg was abandoned, and the peso devalued and floated freely. Dollar bank accounts and investments were forcibly converted into pesos. From 1:1 the exchange rate moved to 4:1. Inflation returned, imported goods became scarce, businesses went bust and the unemployment rate hit 25%, with another 19% under-employed. (Wikipedia has an excellent timeline of Argentinian crisis period for much more detail).

But 2003 saw a turnaround; and it’s this recovery that gives some hope that Greece might follow the same path if it leaves the euro. Tourism was indeed a contributor to economic growth as the weak currency made it a cheap destination. In 1997 tourism and travel had a total contribution of 7.5% of GDP, and by 2006 it had risen to 12.5%. Greece has a much larger tourism industry already, accounting for around 18% of GDP. I’ve heard this high level of the Greek tourism industry described as a handicap – perhaps it already is operating at full capacity (airports and transport, restaurants and hotels) and after default there would be little initial appetite to provide capital to ramp up capacity. But it doesn’t seem fanciful to expect a devaluation to produce growth through tourism in Greece, even though it’s unlikely to be a near doubling as was the case in Argentina.

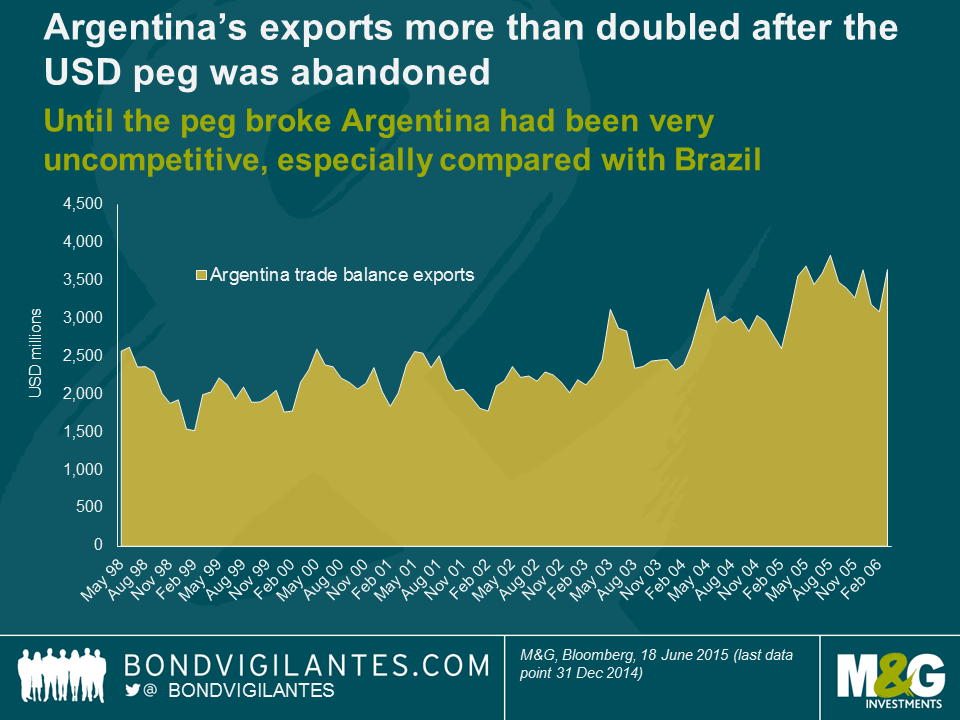

But Argentina’s big win was one of fortunate timing – and Greece won’t have this luck on its side. World growth was very strong in the period post the Fed’s emergency rate cuts after the 9-11 terror attacks. Global GDP growth was 3.1% pa in the period 1992 to 2001, but for the next ten years it averaged 3.9%. China joined the World Trade Organisation (WTO) in 2001 and there was an explosion of global trade – supplier nations to China did especially well – to Argentina’s benefit. Until the ending of the dollar peg Argentina had been extremely uncompetitive, especially once its neighbour Brazil devalued in 1999 (Asian currencies had also devalued – O’Connell points out that only Argentina and Hong Kong had maintained their pegged currencies and suggests that over the 1990s Argentina’s Real Effective Exchange Rate had appreciated by 40%). The rapid rise in global trade, and a return to competitiveness post devaluation helped lead to a 120% rise in Argentina’s exports from 2002 to 2006. Chinese demand for soybeans are often credited for many of the economic gains, although Mark Weisbrot in the Guardian says that’s an exaggeration.

Does Greece have the potential to export its way out of depression? Perhaps, although the poor quality of its land (most is unsuitable for agriculture) makes it much more difficult. Food and meat make up just 12% of its exports, compared to more than a third in Argentina. Greece’s biggest export is refined petroleum, which is a pass-through industry, priced in hard currency in any case, so with no devaluation benefits. Also, its biggest export destination is Germany – possibly problematic post a debt default…

So to conclude, those nations that have thrived post devaluations (Argentina, Canada, Sweden) have been fortunate in that their trading neighbours had been growing strongly at the time. Greece does not have that luxury, nor an economy that can respond quickly to increased export competitiveness. We should also remember that whilst Argentina grew strongly post devaluation and debt restructuring, its current real GDP rate is just 0.5% and hard currency government bond yields are around 8%. The ending of the dollar peg and debt restructuring did not prove to be a permanent economic panacea – but it is also hard to argue that the status quo was sustainable or desirable. Greek policymakers will be thinking the same thing.

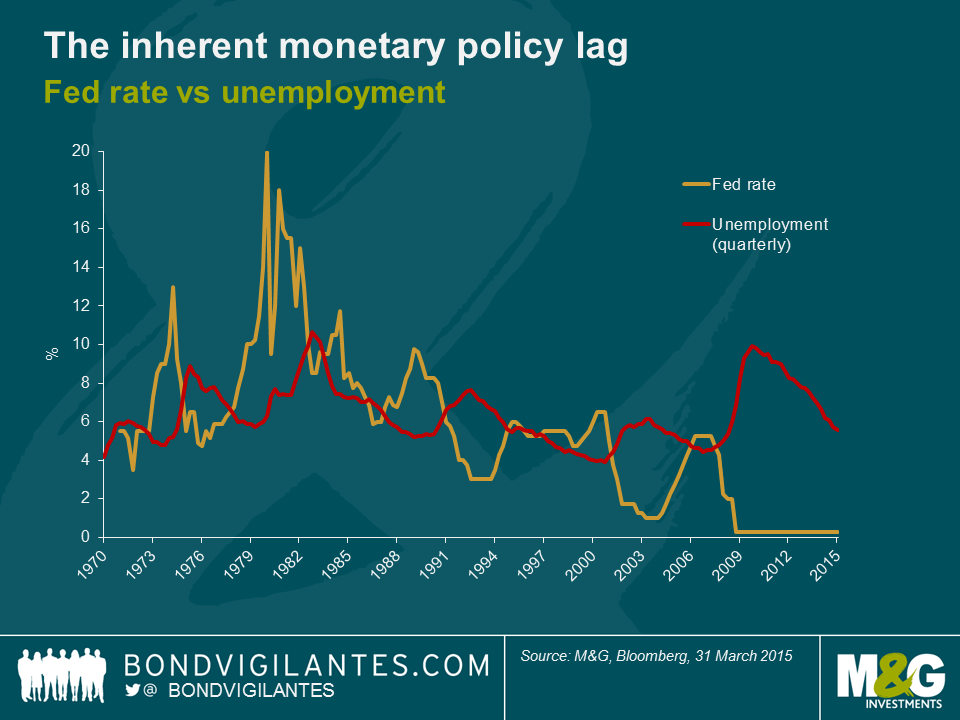

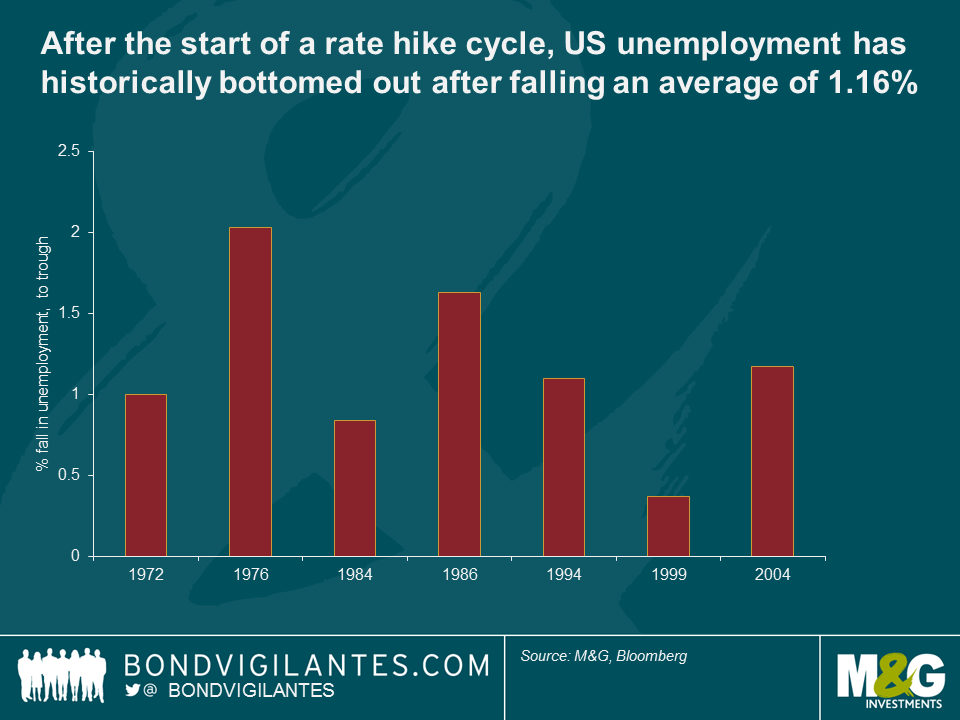

The graph below shows US unemployment alongside the Fed rate over a period of 45 years. From this you can observe the broad relationship between the two, specifically the time delays between Fed rate hikes and the upturn in employment which has historically followed. This time the Fed have delayed the rate hike for a number of reasons, but if history is anything to go by, we can perhaps use this data to make some predictions with regards to the potential timing of the first hike.

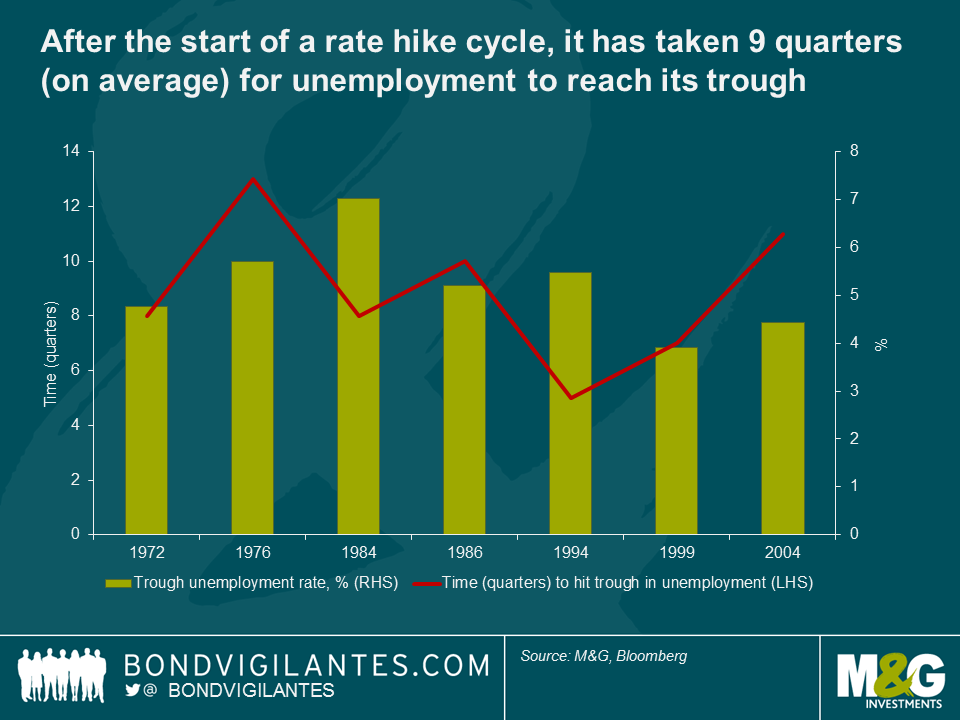

1) After the initial rate hike, the unemployment rate tends to bottom out in 2.25 years

If assessing the timing of an interest rate hike, we need to also consider the time lag inherent in monetary policy. We have therefore looked at each rate hiking period in isolation and determined how long it has taken for the unemployment rate to reach its trough after the first Fed rate hike in its tightening cycle. Although this has varied from 13 quarters in 1976 to 5 quarters in 1994, over the whole period it has taken an average of 2.25 years for unemployment to bottom out after the Fed’s initial rate hike. Therefore, if the Fed was to hike later today, based on previous experience, unemployment may bottom out in September 2017, although it could be between September 2016 and September 2018.

2) Unemployment tends to fall 1.2% after a rate hike cycle

If the Fed hikes rates later today, where will unemployment trend from its end of Q1 reading of 5.6%? Again glancing backwards, when unemployment has bottomed out, it has tended to have fallen by 1.2% on average after the first hike, suggesting that consistent rate hikes commencing in June could result in unemployment eventually falling to 4.4% at the cyclical low.

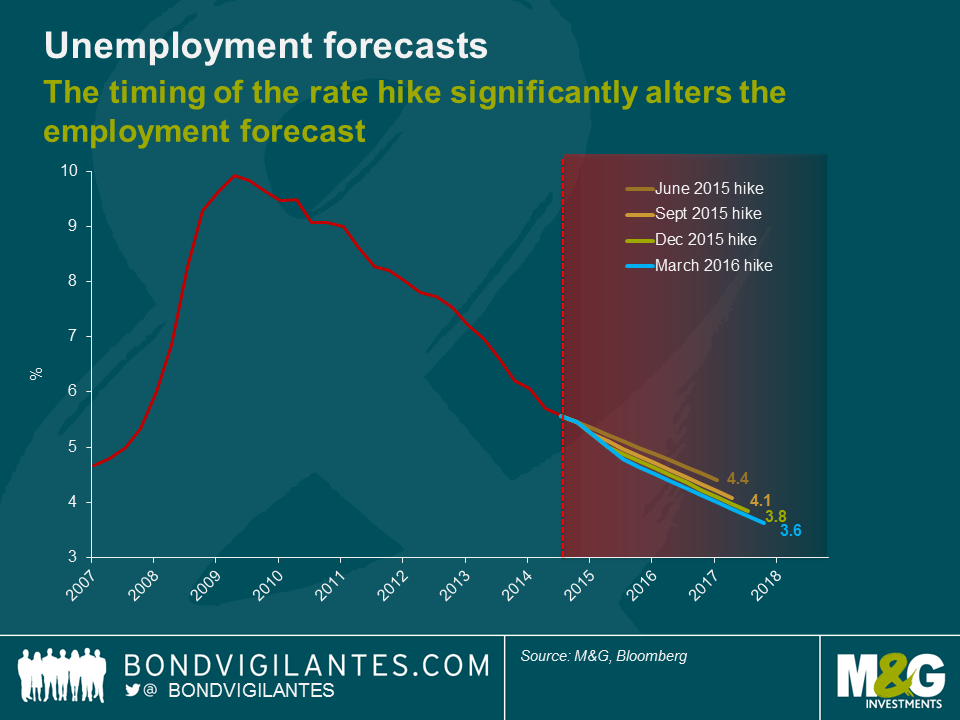

3) Depending on the timing of the rate hike, unemployment could fall to 4.4-3.6%

Building on the observations of the graphs above, we can use these historical averages to predict a range that unemployment could move in, should the Fed hike rates in any of its next four meetings. If the Fed was to delay hiking until March next year, unemployment could fall to 3.6% in June 2018, which would be the lowest US unemployment reading for at least 45 years.

The Fed has delayed its rate hike as wage pressure has been limited so far and the extent of the financial crisis and the lack of flexibility with regard to rate setting at the zero bound necessitated a more than a traditional easing cycle. However, as we have commented before, employment markets are healthy and full employment approaches. As we can see from the above analysis, extrapolating the current trend in employment growth, it is unlikely the Fed will delay its hike until next year and should signal a rate hike very soon given current economic trends and the inherent lag in monetary policy.

A wide range of household decisions – like whether to buy a house, take out a car loan or ask for a pay rise – are affected by expectations about future inflation. Central bankers believe that by closely monitoring inflation expectations they can deepen their understanding about the economic behaviour of consumers. Surveys like the M&G YouGov Inflation Expectations Survey are extremely interesting to central bankers, who will factor them in to their analysis when they determine what to do with interest rates.

The M&G YouGov Inflation Expectations Survey is the only survey of its kind that asks consumers from nine different countries across Europe and Asia about their expectations for the future. Our survey is an alternative source of information for central bankers, economists and investment market participants that draws on research from the Federal Reserve Bank of New York. By asking consumers directly about the “rate of inflation” rather than “prices in general”, the survey leads to a measure of short and long-term expected future inflation outcomes that is more informative and less susceptible to misinterpretation. This is a considerable advantage over alternative inflation expectations surveys.

Some of the key highlights are:

The full report and data from our Q2 2015 survey is available here. In addition, we regularly tweet inflation updates via our dedicated @inflationsurvey Twitter account.

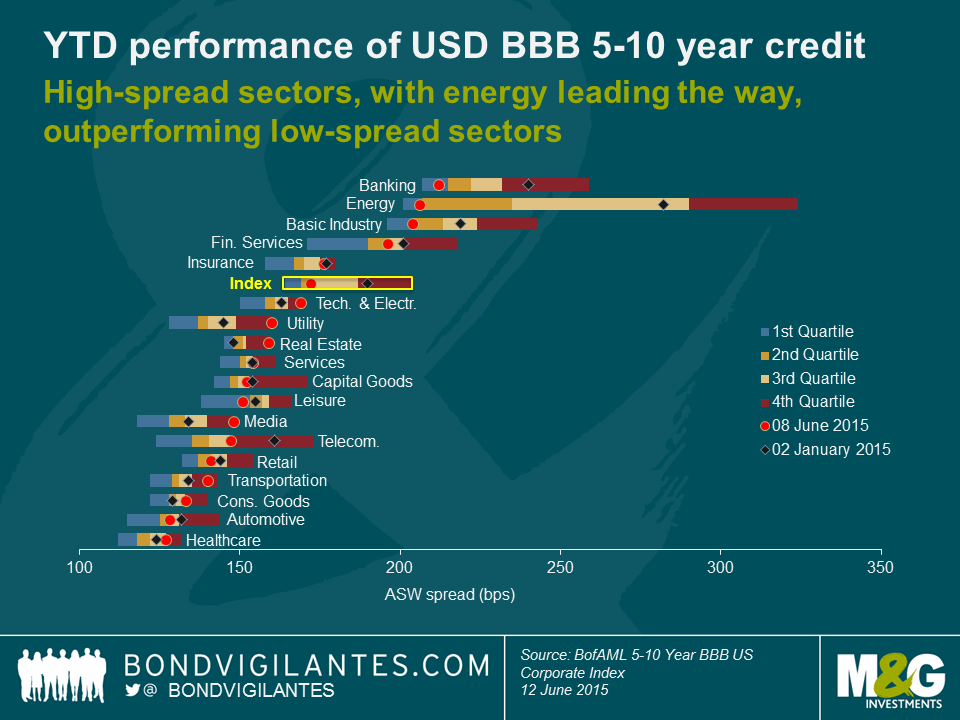

I’ve spent a bit of time in recent days looking at the performance of global investment grade (IG) credit. The chart below shows the year-to-date (YTD) ranges of asset swap (ASW) spreads for USD BBB 5-10 year corporate bond sectors.

Here are our three key takeaways:

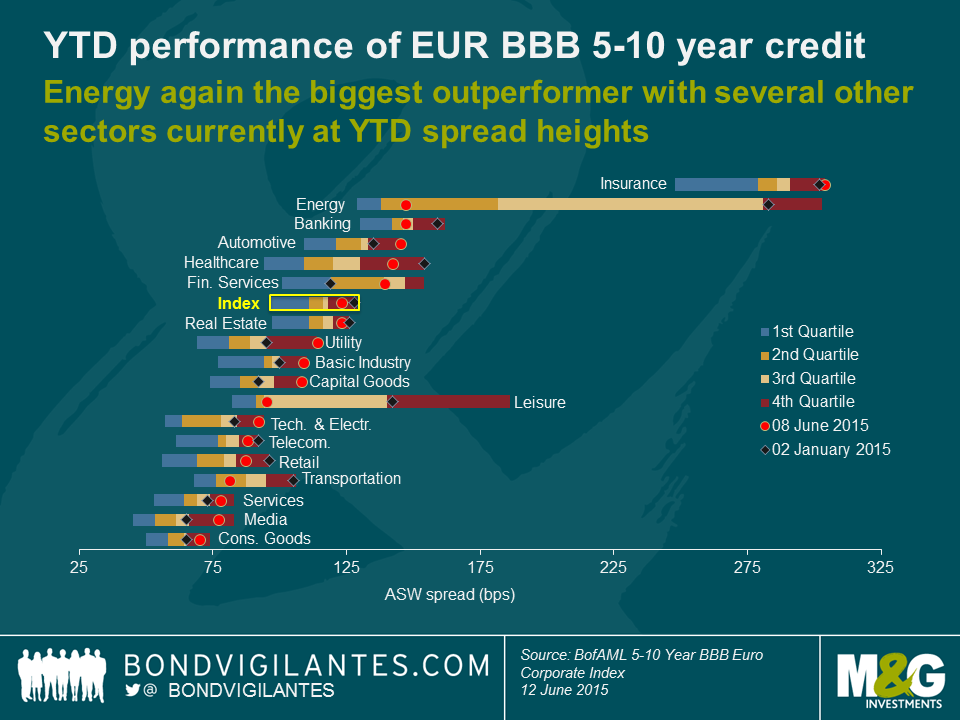

The below chart is a replication of the above, only this time I have focused on EUR BBB 5-10 year corporate bond sectors.

Our key conclusions on EUR market performance:

The above has implications for relative value investors. USD BBB credit high-spread sectors, with energy leading the way, have shown impressive YTD performance. Thus, the relative value argument for owning USD investment grade credit in these sectors is a lot less favourable for now than it had been at the beginning of the year. Banking, energy and basic industry spreads are currently located within the first quartile of their respective YTD spread ranges, indicating tight levels within the context of their most recent spread history. Furthermore, the gap between high- and low-spread sectors has been narrowing. For instance, at the start of the year USD bond investors could have earned a sizable spread pickup of 153 bps for switching from rather defensive consumer goods bonds into cyclical, volatile energy bonds. This spread difference has shrunk by more than 50% to only 73 bps by now. To us, this doesn’t look like particularly great compensation for the significantly higher level of spread volatility an owner of these types of bonds will likely experience.

Within the EUR BBB universe not a single sector is trading in the first quartile of its respective YTD spread range at the moment. In fact, several sectors are currently at their YTD spread wides (insurance, automotive, utility and capital goods) or very close (basic industry and technology & electronics). Hence, the argument can be made that these sectors are offering compelling relative value compared to their recent spread history. However, EUR YTD spread ranges might be skewed towards lower spread values due to quantitative easing euphoria in the first quarter and hence current values appear overly wide in comparison. In addition, growing fears of a disorderly Grexit and the potential fallout on the Eurozone have the potential to put upward pressure on EUR BBB spreads going forward. Finally, it should be highlighted that although USD BBB spreads have outperformed EUR BBB spreads by 13 bps YTD on an index level, there is still a decent average spread pickup of nearly 50 bps to be earned for switching from EUR into USD BBB corporate bonds.

In general we see decent relative value in IG credit spreads at current levels and remain constructive in terms of corporate bonds, particularly in the USD market. In times of still very low rates, credit spreads offer an additional source of yield for bond investors. Provided that the correlation between rates and credit spreads stays below 1.0, which has historically been the norm, this also gives rise to diversification benefits. In this context, IG credit spreads can help soften the blow for bond investors in a rising rates environment, like they have done in the first half of this year.

As value investors we would generally assert that every financial asset has its price. Few bond market offerings tick all the boxes, but if we are to be suitably compensated, and subject to certain red lines, we are generally sanguine.

Yesterday saw XPO Logistics, a third party US based logistics firm raise $2bn equivalent of debt across Euros and Dollars to part fund its acquisition of Norbert Dentressangle (ND), a French logistics player. Pro forma the acquisition of ND, the company will be a top 10 player globally with revenues of nearly $9bn, will acquire greater scale and a presence in a fragmented European market. The company enjoys multi-year contracts with high renewal rates, limited client concentration, a well-regarded management team with experience of making and integrating acquisitions and a track record of raising equity from sovereign wealth investors. Furthermore, capital expenditure should reduce over the coming years allowing for greater free cash flow generation which could be targeted towards debt reduction. Finally the company has adequate liquidity, an enterprise value of nearly $4bn, a share price that has nearly doubled in the last year, and may well continue to be supported by a multi-year sector consolidation phase.

So what is not to like? Firstly, the business carries a significant amount of debt. On our calculations the current debt load is almost six times EBITDA with the bond indenture allowing for the company to raise further debt, perhaps to fund further acquisitions. Largely though not entirely for this reason the debt is rated B1 by Moodys and B by S&P, essentially half way down the high–yield rating scale.

Secondly, the ‘asset light’ nature of the business is unlikely to result in a high recovery for creditors should the business get itself into difficulty. We would also question the synergies that can be delivered between the existing XPO business and Norbert Dentressangle given the geographic separation and would expect some integration headaches to come. Fourthly, this is an industry with historically low margins and fairly low barriers to entry. Finally, we also took issue with level of protection offered by the bond documentation. Covenants are generally loose which allows the company to incur significant debt that would rank prior to the new bonds (and further impact recoveries), guarantees are only offered from a relatively small part of the business and there is capacity to see dividends paid out to shareholders, even if this is not currently the intention.

Back to the earlier question of value. With a coupon paying 5.75% on the six year Euro notes and 6.5% on the seven year USD notes, and crucially with limited call protection which allows the bonds to be refinanced in the next few years, we ultimately took the view that this financial asset was not suitably compensating us and fell shy of our targeted yield for the name. That said, as a former colleague used to to say, ‘these yields aren’t door numbers.’ There may well come a time when we see a more attractive entry point & having done our credit work we will watch the bonds closely.

Finally at this point I should add that much of the excellent analysis that we are privy to is carried out in the first instance by our team of analysts. In this case I have Miriam Hehir to thank.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.