Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

S&P placed Brazil’s foreign currency ratings (BBB-) on negative outlook yesterday, only one small step away from junk. S&P’s negative outlook implies that there is a probability higher than 33% that Brazil’s rating will be subject to a downward revision in the next 18 months. According to the statement, S&P “could lower the ratings if there were further deterioration in Brazil’s external and fiscal indicators resulting from what we might view as a backtracking by Brazil from its commitment to its stated policies and from the various policy corrections underway.”

In our view, a rating downgrade is inevitable. Brazil is suffering from challenges on a number of economic fronts, including a recession, high inflation, rising debt levels, a weak fiscal framework and negative terms of trade caused by weak demand for commodity exports. On the political side, the controversy caused by the massive Petrobras corruption scandal is resulting in political instability and investor aversion. It is difficult to see many positives in Brazil at this point in time apart from the fact that foreign exchange reserves remain at adequate levels when measured by various metrics. In addition, the Central Bank has been reducing the amount of currency intervention through swaps, a credit positive.

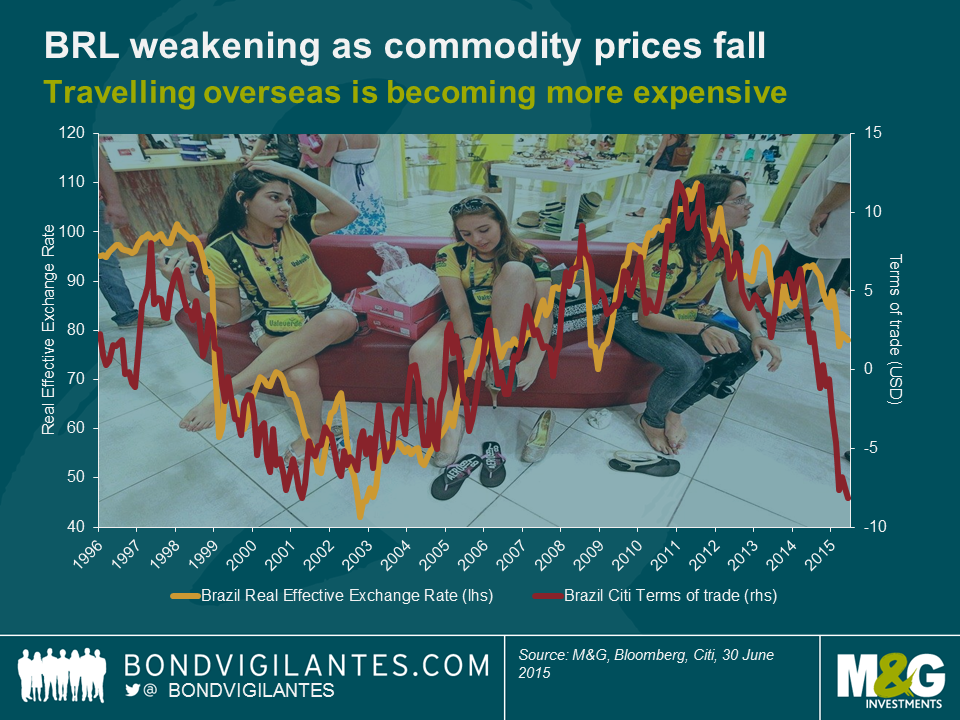

If we examine the current account trends, one factor that has deteriorated over the past decade has been the travel component. While the amount spent by foreign tourists in Brazil has remained relatively stable, the main deterioration is the result of Brazilians travelling abroad and spending their hard earned cash. This has been driven by the Real’s real appreciation.

It is interesting that the travel deficit did not begin to improve as the Real started to depreciate in 2011. One explanation can be that real wages were still rising until early 2014. With the economy now in recession, real wages have begun to fall and unemployment (a lagging indicator) has started rising as well.

Given these factors, we believe that the travel deficit will start shrinking over the next few quarters. If Brazilians stopped travelling overseas and chose instead to travel domestically, they would be accomplishing two things: reducing the current account deficit and stimulating the struggling domestic service economy. While that is a small step in context of this complex macroeconomic environment, every little bit counts.

The Euro Summit meeting in Brussels that took place a couple of weeks ago seems to have finally provided some temporary closure to the Greek debt crisis. The dreaded Grexit scenario was avoided (at least for the moment) and the Greek government was able to repay its arrears to the IMF and the ECB using the €7.2 billion bridge loan provided by the European Council. Looking ahead, this short term loan gives Greece and its creditors a bit of breathing room to establish a “Memorandum of Understanding” around a more comprehensive bailout package, estimated to total approximately €85 billion over the next three years. In terms of concessions made by the Greek government, Prime Minister Tsipras was forced to cross many of his Party’s “red lines” on taxes and spending cuts, and these austerity measures will probably continue to exert pressure on the Greek economy for the coming months and years.

Whereas the lengthy negotiations until now have focused primarily on the reforms to be implemented by the Greek government, I find it quite interesting that very little progress has been achieved on providing some type of debt relief to the Greek government and its people. Indeed, despite having already been significantly reduced in 2012, Greek debt to GDP has soared again from less than 130% in 2009 to over 180% today, and according to the IMF should peak at 200% within the next two years. Even more alarmingly, debt dynamics in Greece continue to look extremely worrying, as continued slippage on the fiscal side and disappointing growth numbers (the European Commission recently reduced its growth forecast for Greece for 2015 from 2.5% to 0.5%) mean that the situation will continue to get worse before it gets better. More recently, the forced closure of the banks and imposition of capital controls only exacerbated the country’s woes, as a larger than anticipated capital injection in the Greek banking sector will now be required to keep it afloat.

Because of these recent developments, it now seems a widely accepted notion that the Greek government debt is unsustainable in its current form. This was not only mentioned fairly explicitly by the IMF in its update to its “preliminary draft debt sustainability analysis” (published last July 14th) but also by many people involved in the matter, such as the EU’s Economic and Financial Affairs Commissioner, Pierre Moscovici. The crucial and hotly debated issue now is whether relief on Greek debt should be provided via an upfront reduction in the amount of Greek debt (also known as a “haircut” or “debt forgiveness”) as requested by Tsipras and the Greek government, or through a debt restructuring (the preferred option for the Eurogroup led by Angela Merkel), which would keep the total value of the debt unchanged but would involve extending the maturities of the debt and lowering the interest costs.

Since the beginning of the crisis, Angela Merkel and her Eurozone partners have always said that debt forgiveness was out of the question for Greece, and this intransigence has caused them to receive quite a bit of criticism from international observers and from the Greek people themselves. To be fair, it is true that the idea of debt forgiveness does have some drawbacks:

Personally I find this argument to be a bit dubious coming from the same Angela Merkel who replied to David Cameron’s push for EU treaty reforms last 29th of May “where there’s a will, there’s a way”. Anecdotally, she repeated the same phrase to Tsipras on the 12th of June when negotiations were at a standstill, so she seems to be enjoying this expression at the moment. Nonetheless, the reality seems to be that the Lisbon Treaty can be amended for David Cameron’s reforms on European immigration and pensions, but not for Greece’s debt relief requirements.

I think this a shame because, despite the drawbacks, there are a couple of compelling arguments in favour of a haircut:

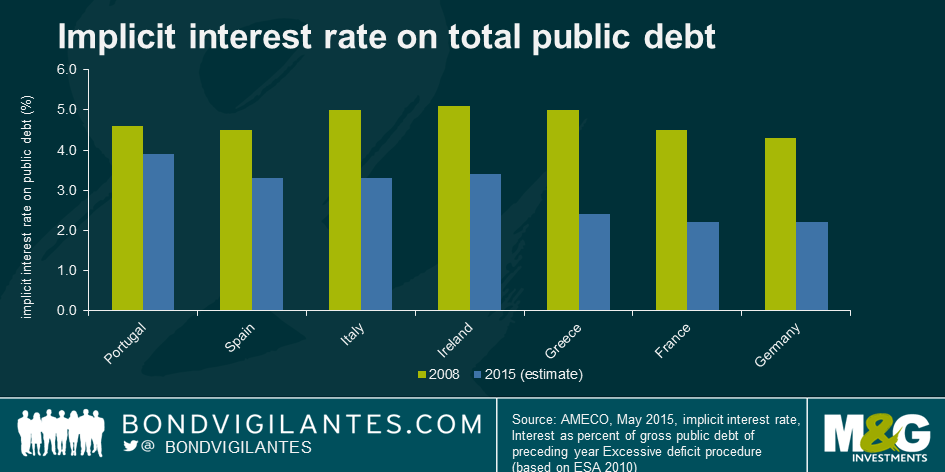

1. Given that Greek debt was already restructured first in 2010 and then again in 2012, the average interest rate that the Greek government currently pays on its debt is already quite low (around 2.4% according to the European Commission), only 0.2% higher than France’s and Germany’s, as the chart below shows:

In addition, the average maturity of the debt is also already quite long, at over 20 years. Because of this, not only would a restructuring only marginally reduce the cost of the debt, but also extend for several decades Greece’s financial tutorship and the need for austerity measures. For example, reducing the average interest rate on Greek debt from 2.4% to 1.4% and extending the average maturity of the debt by 30 years (as certain institutions have recommended), would only reduce the net present value of the debt burden by approximately 30%1. This would be a step in the right direction, but probably wouldn’t give Greece a whole lot of breathing room either.

And should interest rates be lowered and maturities extended for Greece, what will be the reaction of the populist parties in Europe? Surely their case for debt relief is almost just as strong whether that relief is provided via debt forgiveness or through a restructuring?

2. As we enter the 7th year of the Greek recession, one can argue that the country and its people have reached the end of what they can endure in terms of austerity measures. A Greek haircut would allow for some much needed increased spending in the short term, in view of boosting investment and reducing unemployment.

Hopefully, Germany and its Eurogroup partners are sensitive to the potential benefits of debt forgiveness, and have refused to consider this option so far because they believe the timing is not right. Indeed, with the upcoming national elections in Portugal,Spain and Ireland ,as well as the German federal elections in 2017, now is arguably not the best time to crystallise a loss on loans made to Greece.

In this respect, Germany’s strategy probably makes sense, and one can only hope that in a few years’ time –if Greece has demonstrated a strong commitment towards reforms and political pressures have abated in Europe– the idea of debt forgiveness may be back on the table. At this moment, maybe we will even hear Angela Merkel use her favourite catchphrase again… because where there’s a will, there’s a way… isn’t there, Mrs Merkel?

1 Assuming a flat discount rate of 2.4%

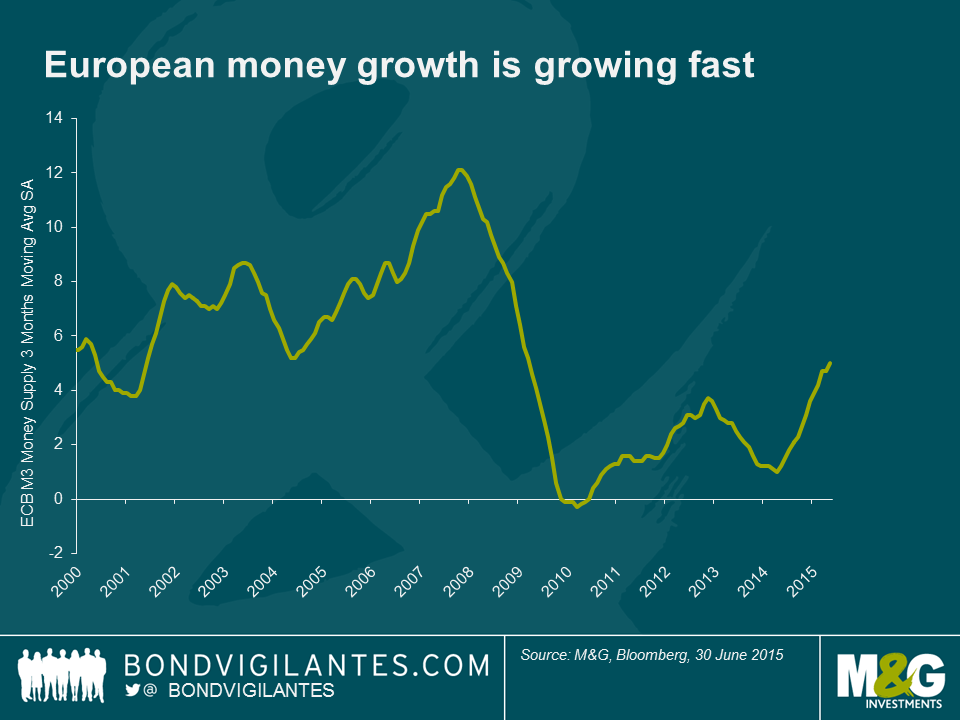

It has been difficult to filter through the noise of the Greece situation these past few months. But when you stop and have a look at the economic backdrop, things don’t look as bad as some of the alarming headlines might have you believe. Some significant economic headwinds have turned into tailwinds, which will likely drive European growth for the next 18 months.

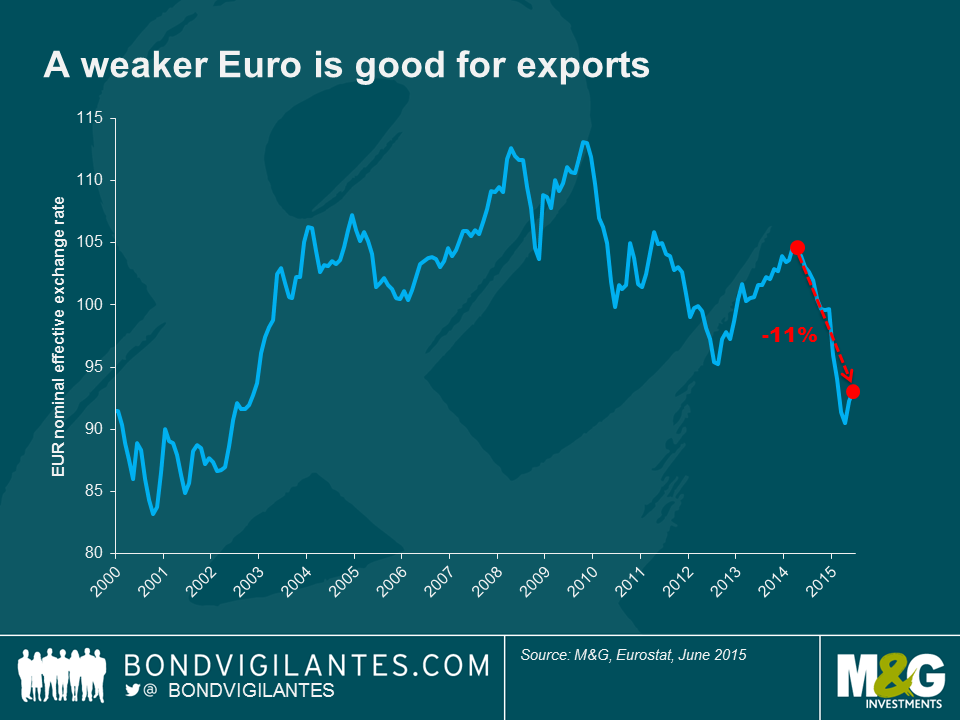

In April, the Euro had fallen to its weakest level in 12 years. Today it remains 11% weaker on a nominal effective exchange rate basis compared to its most recent high point in March 2014. The move higher in the US dollar, caused by expectations that the FOMC could hike interest rates in September has been a big factor in the move. Equally important has been the ECBs commitment to maintain quantitative easing until September 2016. With two of the world’s major central banks maintaining opposite monetary policy stances, it is likely that the Euro could continue to weaken over the medium term. At this stage, there is no reason why the US dollar couldn’t reach parity with the Euro.

This weakening represents a significant easing in monetary conditions and would be extremely welcomed by the European Central Bank. A weaker Euro means stronger export growth, an increase in earnings for European companies, stronger labour markets and rising inflation. This is a major advantage the European economy has at the moment.

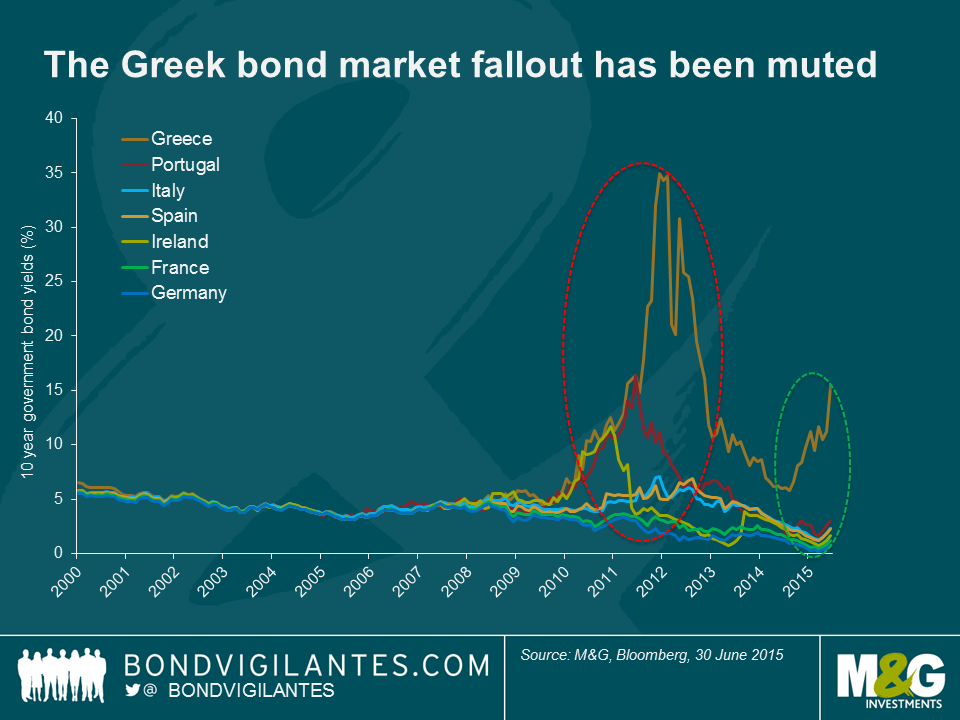

The periods of January 2010-January 2012 and September 2014-January 2015 show how market thinking on Greece and the peripheral nations has evolved in a relatively short amount of time. Between 2010 and 2012, European sovereign bond yields (and particularly those of peripheral issuers) were highly correlated and absolute yield movements were of a similar magnitude. This is in stark contrast to government bond yield movements more recently, where the market treated Greece as an isolated example and bond yields for other European nations fell. It is not a rash statement to say that bond investors today are much less concerned about the Euro falling apart and have faith in the European authorities and their mission to complete Europe’s Economic and Monetary Union.

Whilst yields have risen across the Euro area from the lows visited in April, this is likely the result of rising inflation expectations and economic growth rather than a rise in credit risk premia. The stability witnessed in the bond markets for Ireland, Portugal, Spain and Italy is encouraging to households and corporations alike who will be more likely to consume or invest based on a stable outlook. Indeed, we have seen a large number of European companies issuing debt, locking in low interest rates, terming out their debt and looking to invest in growing their operations.

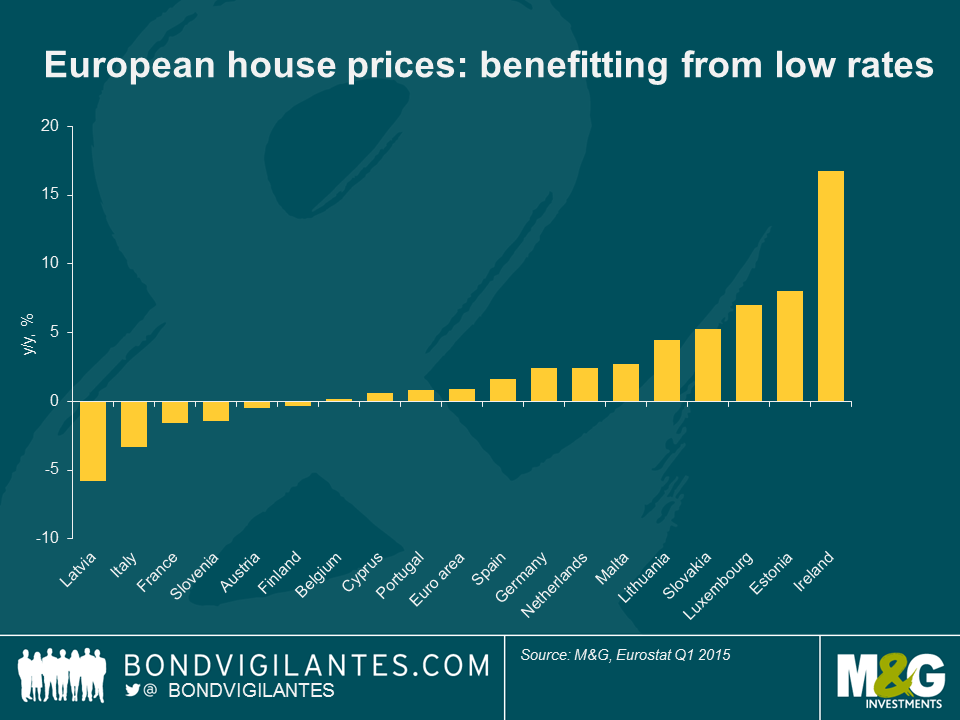

The outlook for the European consumer is undeniably strong. Low interest rates, falling unemployment (the Spanish economy created over 411,000 jobs in Q2 2015, the highest number since 2005), rising household net wealth through higher asset prices, record real wage growth in Germany and the fall in oil prices all bode well for the consumer.

As well as making it easier to borrow, ultra-low interest rates boost asset prices by reducing the discount rate on cash flows from assets, such as dividends and rents. In addition, house prices are on the rise across much of Europe helping to boost household wealth. This is helping to increase the feel-good factor and confidence across Europe, something that is an intended consequence of QE.

Beware those that think the Eurozone project is doomed to failure. As I have argued previously, there are a number of strong arguments in favour of the euro surviving, not least the fact that no country within the European Economic and Monetary Union has left. With all the talk around politics, one thing that is regularly overlooked by markets is the political desire to maintain the euro area and single currency is extremely strong. Of course, there is still a significant amount of work to do in order to achieve a full economic and monetary union and the situation with Greece is not fully resolved. Despite this, the three “C’s” of currency, confidence and consumption will boost the European economy in the short-term and should ensure a self-sustaining economic growth profile for the largest economy in the world.

Mike Riddell, who worked in and around the bond team here at M&G for the past twelve years, has decided to move on. We can’t say where to yet, but it’s to another big bond fund manager and it’s a good move for him. Normally we’d ask the airbrushing team to have him removed from the official histories, but he did a great job for us and we are all sad to see him go.

Mike did a great job running government bond portfolios for clients, as well as writing some of our most popular blogs (lots of good and prescient stuff on China, emerging markets and peripheral Europe).

Apart from declaring that he was a shoe-in to run the 400m for Wales at the 2014 Glasgow Commonwealth Games (coulda woulda shoulda) he never let us down. Journalists and future clients should note however that his famous “Blue Steel” publicity photograph does not reflect the reality of Mike today. See below.

Good luck Mike!

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.