Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

M&G and bondvigilantes.com proudly present the scariest charts on the global economy. Some will make you laugh, some will make you cry. You will be amazed, you will be enchanted, you will be mystified, you will be amused. Of course, the following is not for the faint of heart. You have been warned.

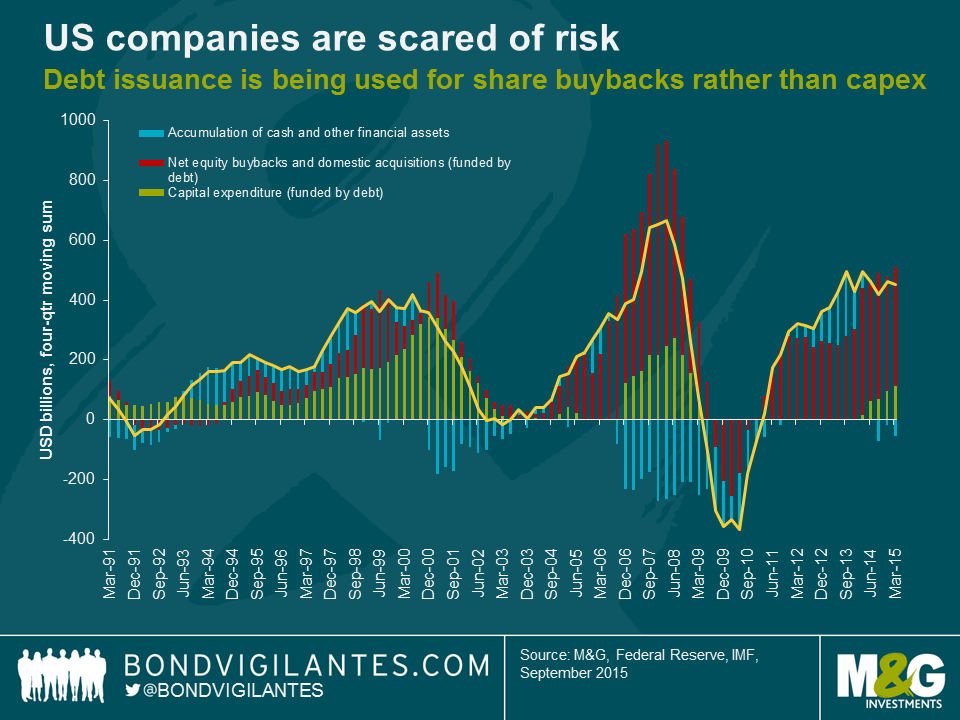

There has been a glut of corporate bond issuance since the financial crisis, as companies have issued debt at low interest rates. What have companies done with all that cash that capital markets have leant them? Overwhelmingly, US companies have embarked upon equity buy backs and M&A activity, which has helped shift the equity market higher. Only a small amount of proceeds raised by US companies in bond markets have been used for capital expenditure. This suggests that corporations remain hesitant to take risk, even in an environment where many perceive that the US economy is ready to withstand higher interest rates.

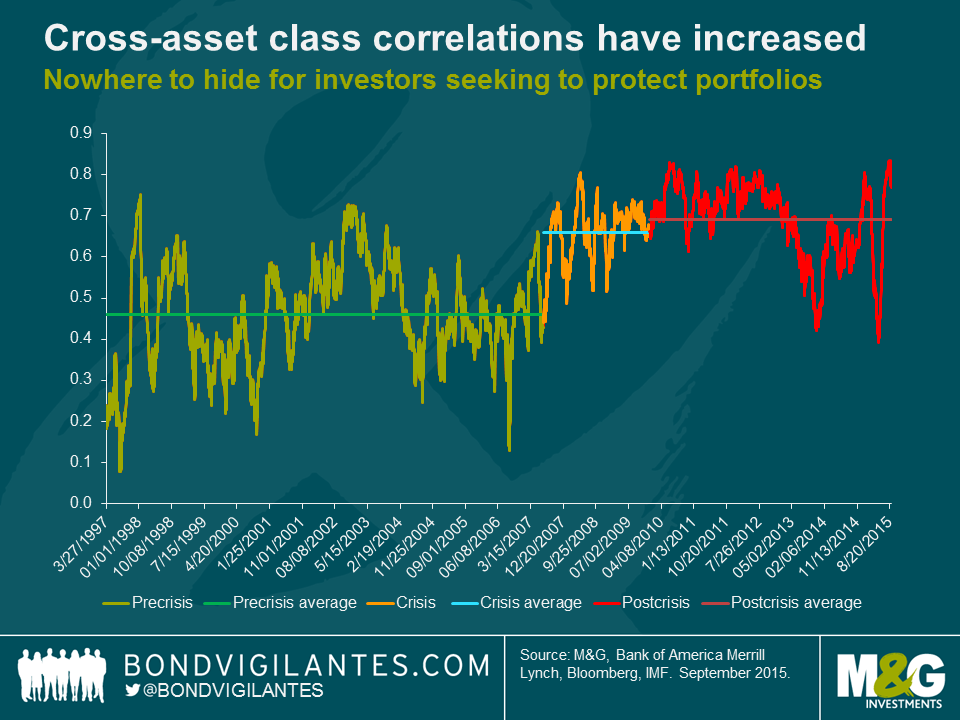

In the old days, an investor could expect the bonds in their investment portfolio to do well when equities sold off and vice versa. Not anymore. Analysis by the IMF shows that asset classes are increasingly moving in the same direction, meaning that the famous rule of investing – diversification – no longer applies to the same degree that it once did. Worryingly, the tendency for global asset prices to move in unison is now at a record high level and correlations have remained elevated even during periods of low volatility. A large scare in investment markets could really test the fragility of the financial system should asset values deteriorate across the board.

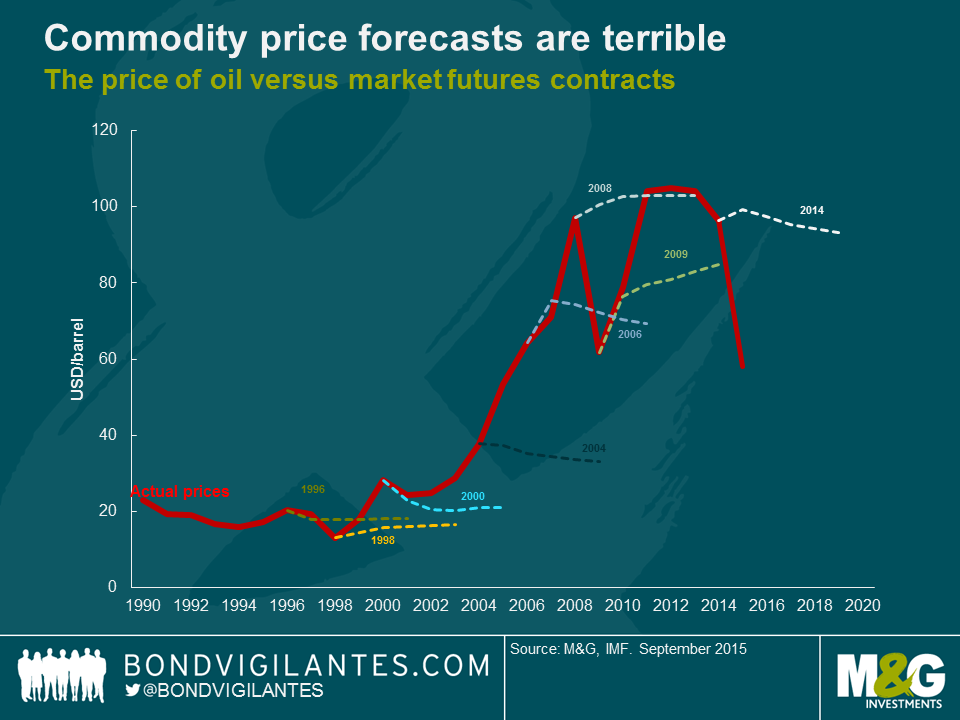

Commodity prices are highly volatile and unpredictable as evidenced by futures market pricing for crude oil. This poses a significant challenge for policymakers in resource-rich countries. In the majority of commodity-exporting nations, a large share of government revenue is provided by the resource sector. The current shock to commodity prices could put severe pressure on government balances, particularly in geopolitical hotspots like the Middle East, Russia, Nigeria and Venezuela. Those forecasting (hoping) that commodity prices rebound may be disappointed.

The notional value of derivatives in the global financial system is around $630 trillion. To put this in comparison, the value of global GDP is $77.3 trillion. Whilst $630 trillion is a huge number, it does overstate the dangers lurking in the global derivatives market. The notional amount does not reflect the assets at risk in a derivatives contract trade. According to the BIS (Bank for International Settlements), the gross market value of the global OTC derivatives market is $20.9 trillion (close to a third of global GDP).

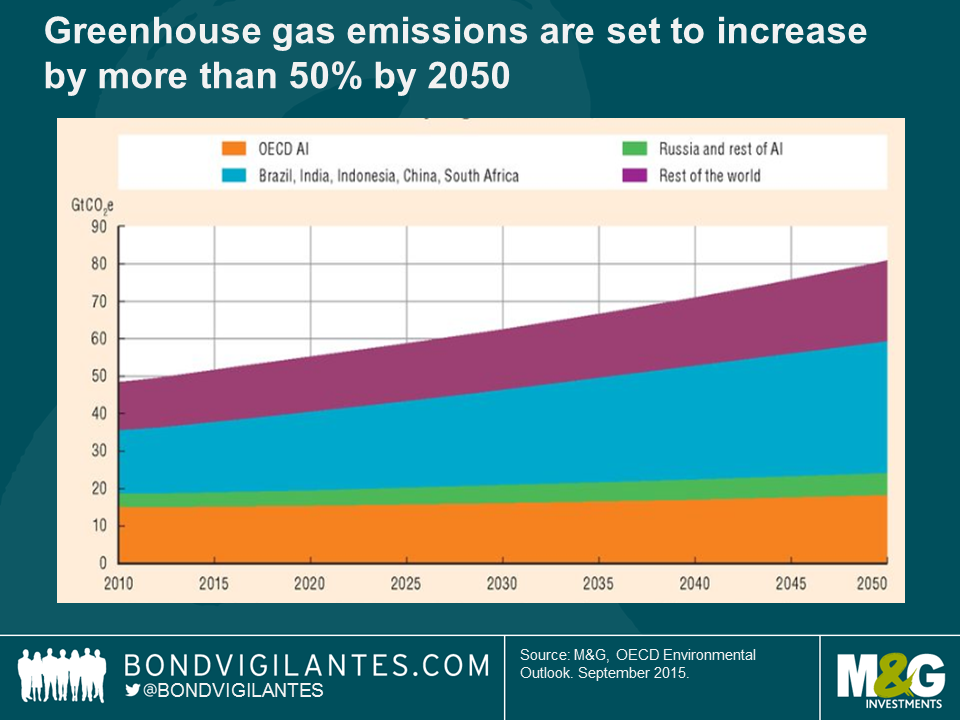

And finally, the scariest chart of the lot. Global greenhouse gas emissions continue to increase, putting further pressure on the environment. The OECD estimate that greenhouse gas emissions will increase by more than 50% by 2050, driven by a 70% increase in carbon dioxide emissions from energy use. Energy demand is expected to rise by 80% by 2050. Should this forecast prove accurate, global temperatures are expected to increase by between 3-6 degrees Celsius. This is expected to alter precipitation patterns, melt glaciers, cause the sea-level to rise and intensify extreme weather events to unprecedented. It could cause dramatic natural changes that could have catastrophic or irreversible outcomes for the environment and society.

From an economic perspective, the main problem with attempting to reduce carbon emissions is that the developed world must find a way to subsidise developing nations to adopt (more expensive) renewable energy technologies. This could cost hundreds of billions of dollars. Developing countries argue that the developed world should bear the brunt of any emission cuts, as emissions per capita in richer nations are higher.

Fortunately, there are actions underway to attempt to limit the increase in greenhouse gas emissions. Eighty one global companies signed a White House-sponsored pledge to take more aggressive action on climate change. Later this year, France will be hosting “COP21/CMP11”, a United Nations conference aimed at achieving a new international agreement on the climate in order to keep global warming below 2 degrees Celsius. And for the innovators, there is a $20m carbon X prize on the table for anyone who can develop technologies that will convert carbon dioxide emissions from power plants and industrial facilities into valuable products, like building materials, alternative fuels and other everyday items.

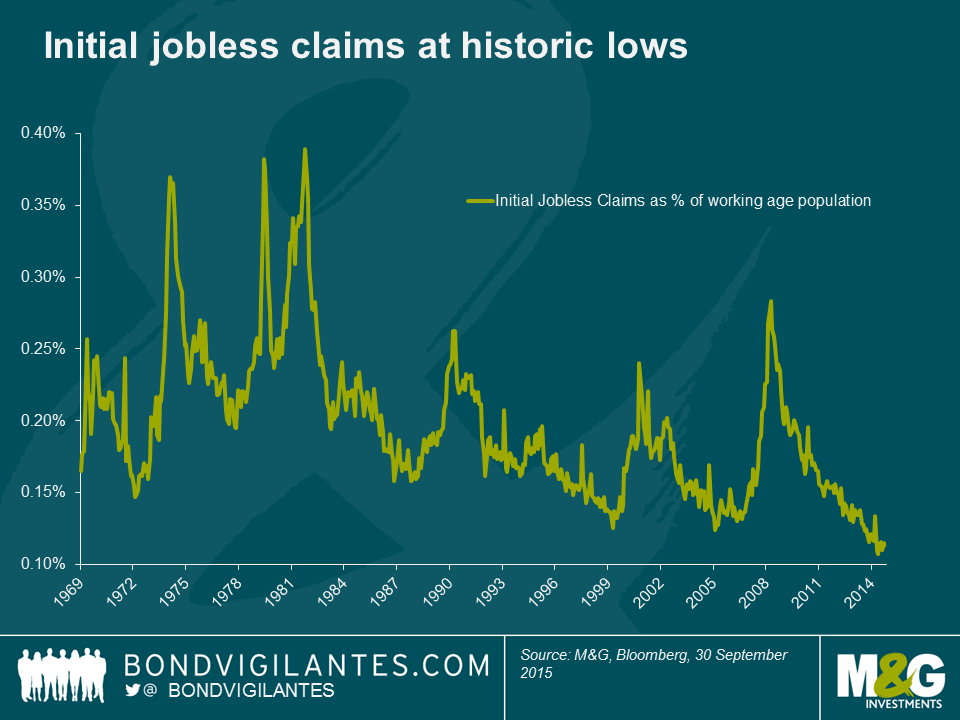

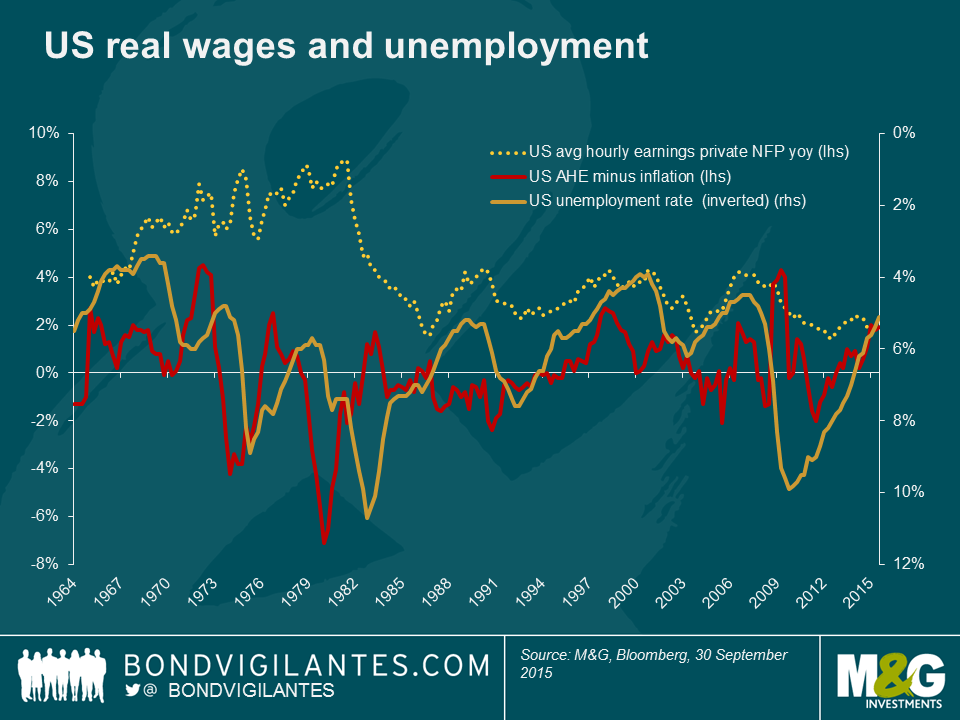

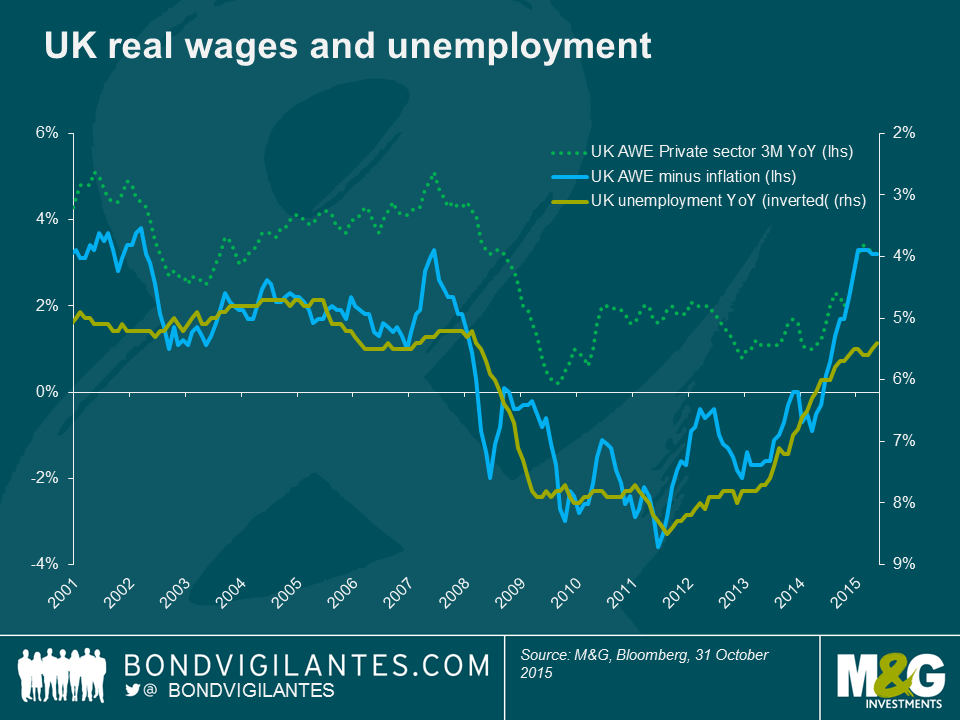

One of the first rules of economics is that the equilibrium market price is generated by relative supply and demand. Limited supply or excess demand should result in an increase in price. One of the questions that has arisen in the post financial crisis world is why have wages not increased despite unemployment heading towards historically low levels? Given the improvement in data such as headline employment, jobless claims, and the JOLTS (Job Openings and Labor Turnover Survey) data, the US economy should be experiencing higher wage pressures by now.

Thinking back to my tutorials from ex Bank of England guru Charlie Been, economists should not only take note of supply and demand when examining equilibrium rates. There was also lots of discussion of both nominal and real wages when examining the relationship between labour market equilibriums, and the cost of that labour.

Nominal wages in the US and UK are at historically low levels, implying that the relationship between supply and demand in the labour market is different this time. However, when we look at the relationship expressed as the real cost of labour it can be seen that the relationship between a tight labour market and rising wages is indeed present as expected.

Those that argue that the current low rate of wage growth in nominal terms is the true depiction of the labour market would have to reflect on the problem of the mid 1970s experience, when a weak labour market was accompanied by rapid nominal growth in wages of 7 to 8 percent as seen in the US chart above. I argue that the labour market is tightening and wage growth is there in real terms. Looking at the data, it can be seen that the real cost of labour is more correlated with the unemployment rate (inverted in the charts above) than the nominal wage rate. The UK chart shows that nominal wage rates were pretty flat during the economic collapse and recovery in the UK, while real wages responded accordingly to the weakness and subsequent strength of the labour market.

We can therefore argue that the current data, and likely future data, imply the Phillips curve is still alive and well. The challenge the central banks face in hitting their inflation targets is that the price of other stuff (mainly oil) has (temporarily) collapsed, thus the strength in the labour market is currently masked. The economic rules of excess supply and demand are amply demonstrated in the depressed commodity markets, the low yields available in the QE-led European bond markets, and in the labour market.

The Fed and the Bank of England should recognise that labour data suggests rising inflationary pressures. Further attempts to strengthen growth via loose monetary policy will enable inflation targets to be hit sooner than would otherwise be the case, but once the deflation outside the labour market halts, central banks will be faced with the traditional problem of reducing (not increasing) inflation. This need for higher rates in the future implies that long term government bond yields near record lows do not need chasing.

Part of the ABC of Latin American debt series

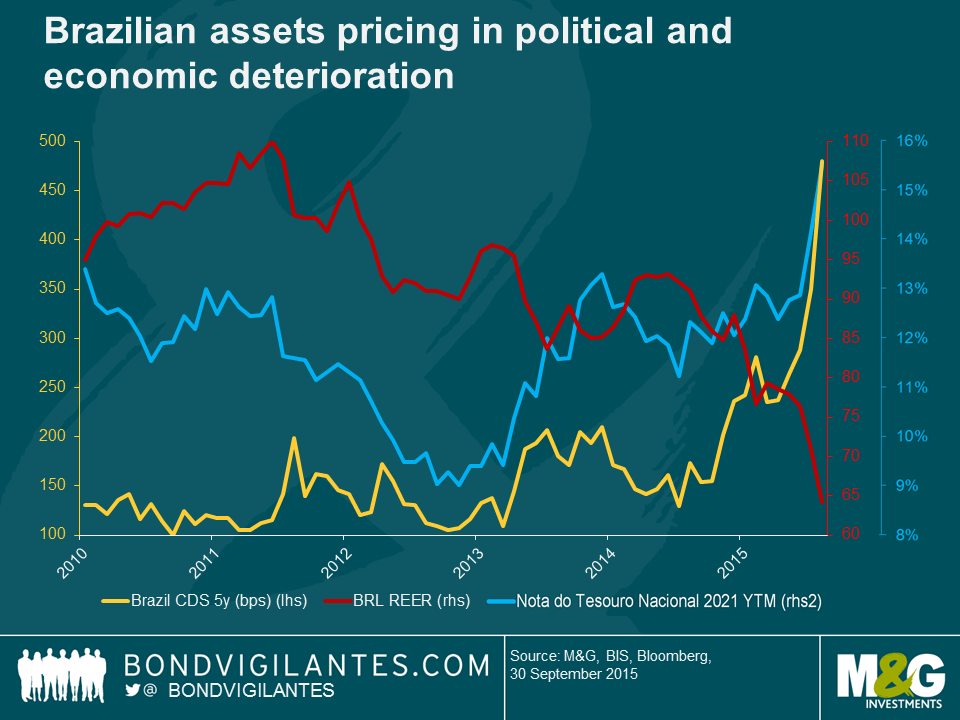

Brazil currently finds itself caught in a destructive trap between politics and economics.

On the political front, it is impossible to trade the daily noise and headline risk. The possible impeachment (45% probability as a guesstimate) of Rouseff would still be subject to various steps and legal challenges and could take a minimum of 6-9 months. Three hundred and forty two votes are needed and the opposition only has about 280 votes at the moment. In the meantime, Congress would be fully distracted and the economy would continue to struggle until the uncertainties over who is in command are cleared. The ultimate goal of the opposition is to weaken the PT (Workers Party) as much as possible ahead of the 2016 midterm and 2018 presidential elections.

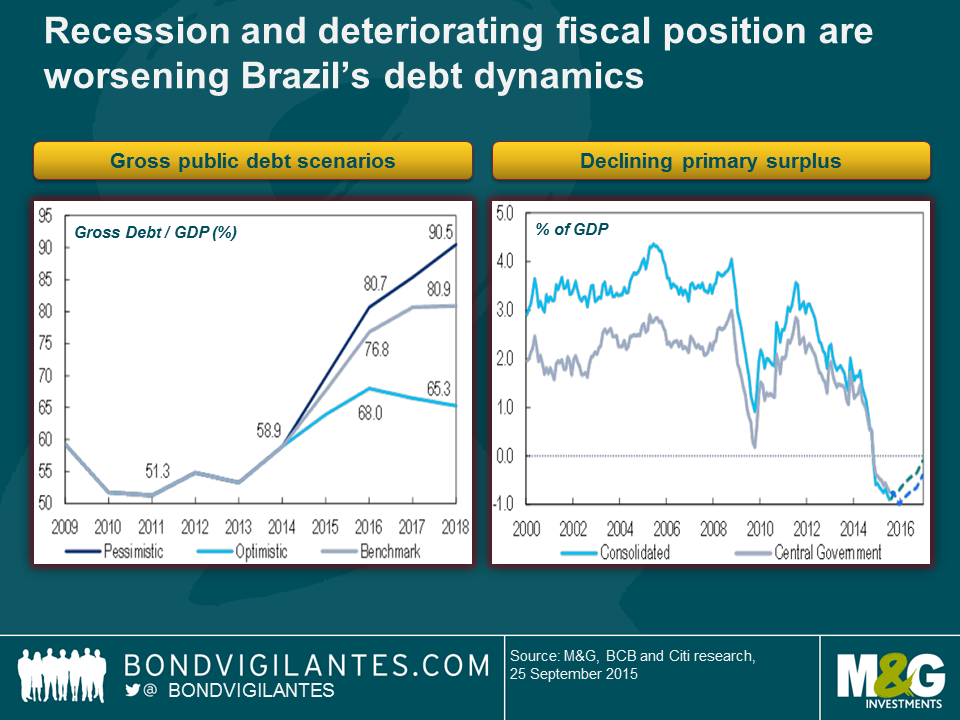

At the same time, local economists think that the economy is still three quarters away from bottoming out. Consumption is pressured by falling real wages and rising unemployment and investment is frozen until there is clarity on the political direction of the country. Net trade can make a small contribution, but not enough to turn things around as Brazil is a closed economy. In the meantime, the fiscal deterioration has been severe as revenues have an elasticity higher than one and more than 90% of expenditures are non-discretionary items that cannot be easily cut without congressional approval. Even a new administration, if weak, may not have enough support to de-index pensions and benefits from past inflation, which could allow Brazil to deflate itself out of a fiscal crisis. There is no chance of this happening under the current political environment. Other structural reforms, even if passed (e.g. public sector social security and pensions) would be a positive signal, but would only produce benefits in the long term. Additional tax increases to reduce the fiscal gap prompted an inconclusive but lively discussion of whether Brazil had already reached the optimal point on the Laffer curve –ie where further tax raises become counter-productive. The CPMF bank tax, which in theory can collect near 1% of GDP is unlikely to be passed (despite the carrot of sharing part of it with cash strapped local governments) as the opposition is conditioning this on spending cuts on politically sensitive areas (such as pensions), which the government is unwilling to tackle due to its low popularity and voter backlash. Brazil, like many other countries in the region, desperately needs growth to shore up its fiscal accounts.

Debt, as a result, will continue rising to 70-80% of GDP under the current path of primary deficits, negative growth and one of the world’s highest real rates.

Roll-overs, however, are not under threat at the moment, but the domestic debt could shorten further (in the 1980s, most of it was rolled overnight). A few state governments are also facing difficulties in servicing their debt, not to mention the Petrobras scandal (see Charles’ EM quasi-sovereign blog here).

The Central Bank is in an unviable position of facing near double digit inertial inflation (some of the proposed tax increases to reduce the fiscal deficit would push it even higher) in a recession and their reaction function appears to be tolerating higher near term inflation until there is greater clarity on the political and fiscal situation. I sense rates will be on hold for a while, despite inflation being way above the 4.5% target and 6.5% upper limit. The pressures to ease will intensify should inflation start declining.

On the positive side, Brazil’s current account will likely continue improving as the tourism deficit declines (see my earlier blog) and imports compress further. The Real has seen a large adjustment and is no longer overvalued, though I think it could weaken still further should Finance Minister Levy leave and there is further weakening in the fiscal accounts or pressure on the Central Bank to start easing prematurely. Despite ongoing currency interventions, Brazil’s gross reserves ($370 billion) remain above IMF recommended levels, under normal conditions. Capital flight has been manageable thus far. However, should that accelerate or should conditions worsen to the extent that the market starts demanding dollar spot as a hedge and not the counterparty risk of the Central Bank swaps ($110 billion notional), the reserve buffer can quickly dwindle.

Asset price levels as of late September (spreads, local rates and the currency) seemed to have priced a lot of the near term bad news. The pain trade was for positive news as the market was very defensively positioned. We have seen since then some short covering and a partial recovery of asset prices.

The consensus is that an impeachment of President Dilma would produce a market rally. If that happens, it could make sense to fade the rally as post-impeachment governability would still be difficult under a new (and possibly unelected) government, and many of the challenges will require deep structural reforms, particularly on the fiscal side. My take away is that things will get still worse before they get better.

It has been quite an eventful year for emerging markets. The fall in oil and commodity prices, the prospect of higher interest rates in the US, the corruption scandal in Brazil and of course the growth slowdown in China have all contributed to increased uncertainty for the asset class. Naturally this uncertainty has impacted performance, weighing down on returns of both hard and local currency debt. For example, despite staging a strong rally in October, EM local currency bonds in US Dollar terms are still in negative territory by about 10% in 2015. In hard currencies, even though the headline JP Morgan EMBI Global Diversified Index is up close to 3% this year (also in US Dollars), dispersion in returns have been significant with for example Russian bonds up more than 20% while Brazil has fallen almost 10%.

Performance aside, even more interestingly and unknown to many investors has been the growth behind the scenes of a rather unique segment of the emerging markets debt world: quasi sovereign bonds. Quasi sovereign bonds are bonds issued by companies who are in majority owned by governments. In this regard they exhibit both features from the corporate as well as the government universe. Their growth has been quite phenomenal in recent times, with gross issuance going from $40 billion in 2005 to over $180 billion in 2014. In addition, the asset class also boasts one of the highest Sharpe ratios in emerging markets.

In this edition of the M&G Panoramic Outlook, Charles de Quinsonas – Deputy Fund manager on the M&G Emerging Markets Bond Fund, explains in more details the intricacies of this emerging asset class and the opportunities that it presents.

Please click here for the M&G Panoramic Outlook web page.

Two things last week that made me go “hmmm”. Firstly: having written a blog on the impact of El Nino on global inflation (here), Anthony was contacted by a company who then came in to see us to discuss their business. Using data from NASA and EU satellites, they produce earnings estimates for retailers, and forecast economic data. By counting cars in Big Box parking lots from space, they generate estimates for the number of shoppers (footfall), and numbers outside of typical ranges usually point to a forthcoming revenue surprise. They can estimate output from car manufacturers, and judge the speed of infrastructure and building construction versus plans. They also monitor magnetic and electric fields around, for example, power generation plants, and take CO2 readings by region (we were given a teaser that recent Chinese CO2 data are pretty interesting – but we don’t subscribe, so…). This is all fascinating – but raises lots of ethical and legal questions, as well as making me think about the future of traditional statistics (and fund management).

So ethically, is it fine to examine somebody’s shopping habits from space? Legally, do we have privacy rights, and if somebody is counting your trucks from orbit to get an edge in buying or selling shares in your company, is this insider trading? And how do traditional statistical agencies respond to the development of “new” statistics which may be able to give an accurate GDP number in real time rather than waiting months to release a number that is not believed, and then revised many times. We’ve written about the Billion Prices Project, an internet-pricing derived real time CPI number several times, and I suppose the Li Keqiang index is an example of even government officials using alternative data to “nowcast” GDP numbers. It feels though that technology is going to have a significant impact on our ability to understand (or at least measure) the economy, even though its impact on the economy itself remains confusing (“You see computers everywhere except in the productivity statistics” – Robert Solow).

Secondly, and still on the theme of technology and its impact on investment management, I got an email from another company offering me the following service. How would I like a live link into the ECB Draghi press conference on Thursday? This link would likely be 8 seconds quicker than the Bloomberg and CNBC feeds, and 20 seconds faster than if I watched via the ECB’s own website. It’s not quite Flash Boys, but it could be that the investment industry is about to get a lot more techy. Subscription to Wired anyone?

And for those who don’t know where the blog title (sort of) comes from, you’re in for a treat.

I just spent two weeks traveling Latin America around the IMF meetings in Lima. The region is navigating through various shocks: lower commodity prices, deteriorating balance sheets, growth and fiscal deterioration, an urgent need for structural reforms and significant political challenges. There is plenty to write about, so in the next couple of days I will post a series of blogs focused on the ABC of Latin American debt: Argentina, Brazil and Colombia.

First stop, Argentina. Below is a summary of my trip, including what I believe are the key country issues and my impressions around them.

After a sleepless 13 hour red-eye flight from London, I decided to take it easy on my first day and make my touring day an educational one. The Argentine Congress and the External Debt Museum – both being related to market developments – seemed good visits for a warm up into my investor trip.

Officially back to the main purpose of my visit, the general elections happening this Sunday were one of the first topics to come up in conversations. There seems to be general consensus that the next administration will be better than the current one, which has helped Argentina’s hard currency debt to be the fourth best performing sovereign YTD. Although the elections are very close, there is the possibility that Daniel Scioli, the candidate who is closer to the existing government, wins in the first round. If he doesn’t, he will face a second round in November versus one of the two pro-market candidates (Mauricio Macri and Sergio Massa – Macri is currently ahead on the polls). I still think that Scioli will make it in the first round.

It is crystal clear what the country’s challenges are and what needs to be done. What is less clear is how gradual Scioli will be in addressing these challenges and how long his honeymoon with the markets will last. I expect the markets to allow him between 3 and 6 months before they start getting impatient and begin to test Scioli’s gradual and non-confrontational style.

Argentina faces a couple of challenges:

First, net international reserves have reached very low levels. Argentina’s access to the capital markets has been severely restricted due to the ongoing dispute with the debt holdouts. Until this is sorted, capital controls (“cepo”) remain in place, hindering foreign direct investment and maintaining elevated spreads as the country’s liquidity buffer vanishes. An agreement – at least with the main holdouts – is a necessary but not sufficient condition for stabilising the country’s challenging macroeconomic outlook. This would allow the country to gradually lift the capital controls, allowing for some foreign direct investment to resume and for the country to issue new external debt to recompose its reserves. An agreement will need to be rectified by the Argentine Congress, which despite no candidate achieving an absolute majority, is expected to pass. The devil is in the details.

Second, in addition to the holdout agreement, Argentina needs to move towards equilibrium in three areas:

a) The official exchange rate is clearly overvalued and will likely be devalued to some midpoint between the current official rate (9.50) and the parallel market (16.00), with a dual-exchange regime also being a possibility;

b) Real interest rates (Badlar) remain in negative territory and will need to rise for the devaluation to have some anchor;

c) The fiscal position (-6 to -7% of GDP) is unsustainable in the medium-term, unless growth rebounds strongly. At best however, we will see an adjustment of 1-2% through spending cuts and energy subsidy reduction in late Q1 2016.

In conclusion, I expect Argentine debt to continue to trade near current levels over the next few months, assuming a Scioli victory (and a rally should the opposition win, which is currently not priced in). I also see a binary scenario after Q2 2016: a sell-off to 12-13% yields should the issues listed above not be addressed adequately, or a rally to under 8% yields should they be.

Recently Claudia and I were in Lima for the annual meetings of the IMF and World Bank. Unsurprisingly (given the host nation and history of the meetings) the majority of sessions were on the developing world, in particular Latin America. Claudia will shortly be posting a series of more detailed blogs on the LATAM countries she visited, so I’ll focus more globally.

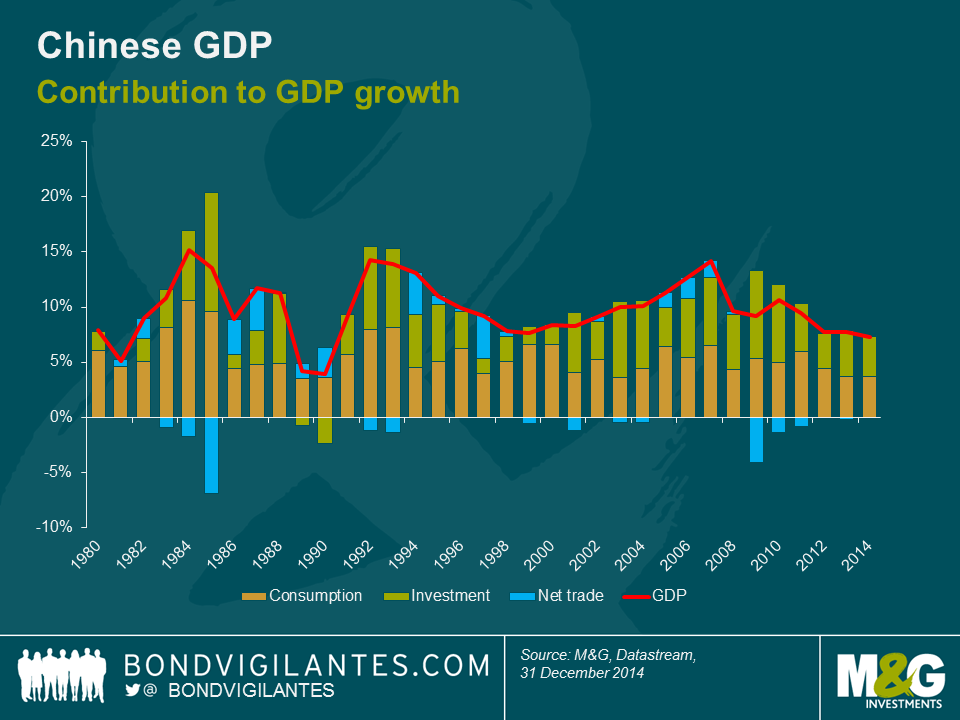

In aggregate, the IMF is predicting global growth this year to be slightly lower (at 3.1%) than last, and then strengthen to 3.6% in 2016. Within this, they are expecting a pickup in developed world growth while the developing world will slow. The IMF give a number of factors as to why the developing world is slowing, but by far the most discussed was the impact of what is happening in China.

Chinese growth is slowing, but the growth projections for this year and next are still 6.8% and 6.3% respectively. Other than India, you would be hard pushed to find a large country with higher predicted growth rates anywhere in the rest of the world. The real story is how that growth will be achieved. China appears to be moving from an investment/construction led economy (which needs a lot of imported raw materials to continue to grow) to one in which domestic demand and consumption play a larger role in economic growth (something we have highlighted in the past here and here).

It was highly likely that this shift was going to happen at some point – the growing middle class were bound to start enjoying the increased wealth they have accumulated sooner or later. Anyone who has visited a shopping mall in Beijing in the past couple of years couldn’t fail to notice the proliferation of high end boutiques – I struggled to find a tie that cost less than £100 when I was there last year.

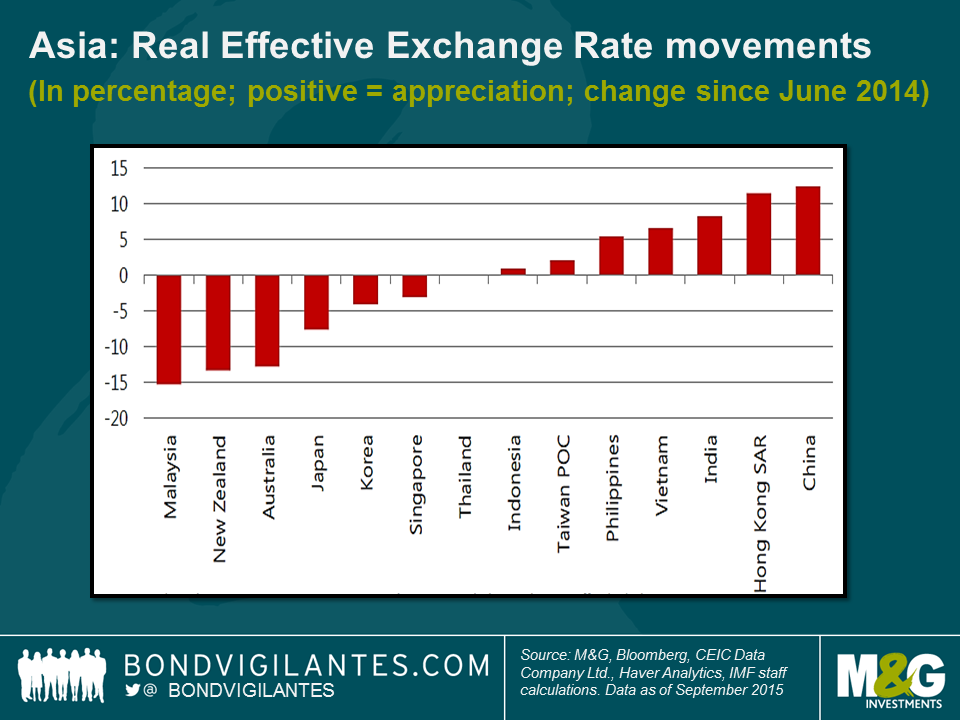

The effects of lower Chinese import demand have been felt most acutely in other parts of Asia and in South America countries which rely on commodity exports for a large part of their revenues.

The IMF acknowledged that these “spill over” effects on Asia were larger than they had expected, and since the old export led growth strategies had run out of steam, Asia would need to find new engines of economic growth. Whilst the depreciation of some of the region’s currencies has been “appropriate and helpful”, more needs to be done. They recommend that governments in the region work hard to improve infrastructure, increase labour market flexibility and strengthen the rule of law.

Regarding Latin America, my main takeaway was that weaker global commodity demand and the spectre of higher inflation could lead some previously well performing countries into a period of stagflation. Left unaddressed current account deficits, political populism and poor productivity could lead to problems for more countries in the region than just those where they are already sadly apparent.

Sessions on the US and Europe were few and far between which I take to be rather positive. I should point out that these meetings have traditionally been EM focussed so maybe one shouldn’t expect too much time devoted to developed market issues. However, if there are major problems in the developed world they tend to elbow their way into the discussions – I was told that Greece was the main topic of conversation at the spring round of meetings, for example.

All the sessions I attended on the US were dominated by the upcoming presidential election and the various candidates currently vying for the support of their respective parties. The general sense that I got was that the economy is ticking along nicely, most people were bored of predicting the timing of a Fed hike and therefore there wasn’t really very much to talk about.

Over in Europe, the feeling was that a lot of the recent drivers of volatility have receded for the time being – the situations in Greece and Russia/Ukraine are less of a risk now than they were before. I’m not sure I necessarily agree that the risk of something bad happening has decreased, but I think it’s certainly true that the market seems to be less focussed on the risks than it was.

The risks the IMF did highlight for Europe were (again) slowing demand from China and the relatively high levels of non-performing loans (NPL’s) that are still on banks’ balance sheets. They went as far to say that the recent economic recovery is unlikely to last more than 18 months if the NPL issue isn’t resolved. They believe that we are likely to see more QE from the ECB, and that European QE has been more effective than the US or Japanese versions as the term premium there fell a lot more. On a slightly brighter note; the increased participation rate in the labour market means that the 10% unemployment rate isn’t as gloomy as it may first appear. They also suggested that there is a need for structural reform in the Eurozone as potential growth is too low.

I appreciate I have painted some pretty broad strokes and that within each economic area there are countries that face totally different challenges and opportunities. There were some common themes that ran through my entire trip, however. Structural reform and improved productivity are pretty much universally necessary across the globe, and that the changes that are happening in China are here to stay. That said, I agreed with Christine Lagarde – the Managing Director of the IMF – when she said that the changes in the Chinese economy are healthy, and in the longer run will prove to be positive for the rest of the world too.

First of all thanks to Business Insider. Every now and then we come into work to find hundreds of new Twitter followers have joined us overnight – this week it was thanks to BI listing us second in its round up of finance Tweeters. It’s a great list and pretty much everyone on it is worth a follow – I’d also recommend following Business Insider’s European markets editor Mike Bird (@Birdyword) if you are twittering-up.

Next, inflation. With energy directly representing 10-15% of CPI baskets in the developed economies, oil prices obviously have a significant feed through into headline inflation rates. The second round impacts are less visible, but transport costs in particular will be important in pretty much every other area of the inflation basket whether goods or services. In the US you expect the feed through from higher or lower oil prices to be more significant than in Europe – this is because Americans generally pay little tax on petrol at the pump, so changes in prices are much more direct than in the UK or Eurozone where the bulk of the pump price is fuel duty and VAT. In the UK for example, for a litre of unleaded petrol costing £1.10, roughly 58p is duty, and 18p is VAT, so the non-taxed element is around 30% of the pump price. As WTI and Brent crude oil prices have plummeted over the past year (Brent fell by 57% from August 2014 to August 2015), inflation has flirted with 0% at a headline level in the UK, US and Eurozone. Looking at recent Eurozone numbers, the energy component of the CPI fell by over 7% year on year. Despite the second round effects, all other major components were up (goods, food, and services – the latter up by 1.3% over the year).

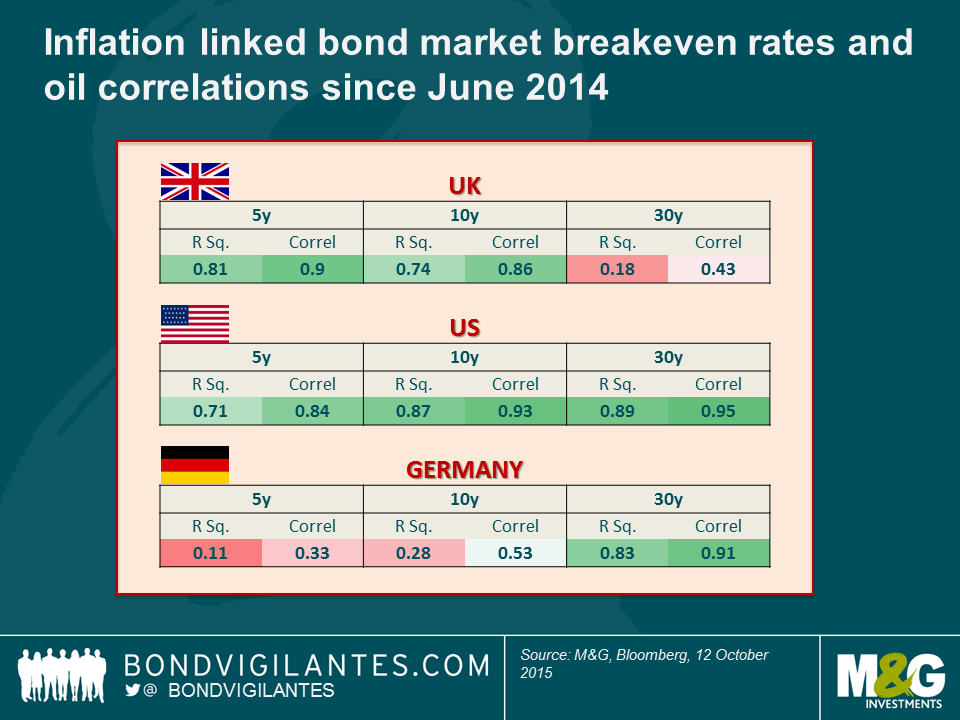

As these deflation fears rose, the price of inflation protection fell. Inflation linked bonds experienced a rocky summer, and the market measures of inflation expectations that policymakers follow closely – the 5 year breakeven rate expected in 5 years’ time – signalled danger. By the end of September, following the Fed’s talk of global slowdown as it held rates, the US TIPS market was expecting average headline CPI of just 1% on average for the next 5 years. Thinking about the next couple of years, a bear can make a good case for oil prices exercising downward pressure on inflation rates. There’s oversupply from US shale (and even those HY energy names that aren’t profitable below $50 per barrel still pump – any revenue is better than none, it’s their fixed costs and debt service that’s problematic, not marginal costs), and after years of sanctions Iranian oil is about to hit global markets. With China and EM demand slowing too, you wouldn’t be surprised to see oil prices lower in a year’s time. If oil fell to $25 then you’d expect to see the energy component of CPI to see another 7-10% fall, keeping headline annual rates towards zero. So you could make a case for short term breakeven rates of inflation to justifiably be correlated with oil prices. What is harder to explain is why the oil price and 30 year breakeven inflation rates are so highly correlated.

The table above shows that there has been a very strong correlation between 5 year breakeven inflation rates and the oil price since the middle of 2014 in the US and the UK. So far so good. But intriguingly the correlation with 30 year breakeven inflation rates and the oil price in the US is HUGE. 95% with an R Squared of 0.89. This was the highest correlation we found anywhere in the developed inflation markets. Why should current levels of oil prices impact expectations for the next three decades of US CPI? To have the same annual impact on the US inflation rate next year, oil has to fall to $25. The next year it needs to half again to $12.50. Then to $6, to $3, to $1.50 etc etc. I think there is an argument that energy costs trend lower – we’ve written about developments in renewables, batteries and fusion nuclear power on this blog– but even in a scenario that all energy becomes free, that impact disappears from the CPI numbers a year later too. So in the US, 30 year breakevens have fallen from their long term average of 2.4% two years ago to 1.67% now as the oil price halved. I don’t think it makes sense for markets to say that US policymakers will be unable to hit their 2% inflation target over the next 30 years on the basis of a one year movement in energy prices. It looks irrational.

Whilst we are talking about inflation, I remember that some years ago the Bank of England discussed receiving tons of letters about the lack of fivers in cash machines and in general circulation, and made it a goal to get more five pound notes out into the wild. At the time, I thought this was a very disinflationary signal – the public demanded smaller denomination notes than were generally available. Well, the Central Bank of Ireland has announced that it is trying to do away with both the 1 and 2 cent coins, and introducing rounding up or down to the nearest 5 cents (we wrote about getting rid of 1 and two cent coins in 2012). This is the opposite of what the BoE was trying to achieve, and is a small sign that we perhaps shouldn’t be that worried about deflation in Ireland any time soon. 28 October is Rounding Day.

Robots. I recently went to a breakfast with “Rise of the Robots” author Martin Ford to discuss his thesis that whereas in the last long phase of human development, machinery and technology replaced tools, the next phase, happening right now, is seeing machines (robots) replace workers. I am not entirely sure how you make a distinction, and I’ve seen research that suggests that technology has always destroyed millions of jobs, but has simultaneously created more. Where he might have a point is that this wave of technology is replacing “middle class” and “white collar” jobs to an extent not seen before, and that this might be a double whammy in that not only are jobs hollowed out, but the great consuming class is left poorer – robots don’t buy stuff, and the reduction in overall demand will be very damaging for society. Martin points to US labour force growth being 2 million+ per year, and expects significant social problems if robots are shrinking the available jobs pool for us puny humans. Wealth accrues to the robot owners, and vast numbers of people will be unemployed. A “basic income” might be required to allow living standards to be maintained (and to allow us to keep buying stuff). Martin might be right about the US, with its strong demographics and growing work force. But what about us poor aging Europeans, let alone Japan, or China, where the one child policy bakes a demographic nightmare in the cake. The working-age share of the global population probably peaked in 2012, after four decades of growth. Might robots be entirely necessary to do the work for us whilst we sit in old peoples’ homes? Interesting book though.

Two other recent reads: “Fields of Fire” by James Webb, the best of the Vietnam war novels I think, and “Doing Good Better” by William MacAskill. MacAskill’s book probably deserves a blog of its own; the book focuses on the most effective ways to give to charity and raises both fascinating moral issues and concepts like “micromorts” (the amount of time that you will, on average, lose from your life by partaking in an activity like motorcycling or smoking). TL;DR – you can save a life for a donation of about $3000, maybe less. Give your money to the best organisations that distribute mosquito nets and anti-parasite medication.

A book I can’t face reading is the new Morrissey novel. His autobiography was ace, but the reviews for “List of the Lost” are so universally bad that I am leaving it on my shelf. I do have exciting Morrissey news however. I was present at the very first Morrissey solo gig at the Wolverhampton Civic Hall in December 1988 (watch it below), and at the end of September he played what he claims might be his last ever UK concert, in Hammersmith. Having failed to get on stage in 1988, I’m pleased to announce that I made it over the barriers during Suedehead last month. Reader – the man himself shook my hand.

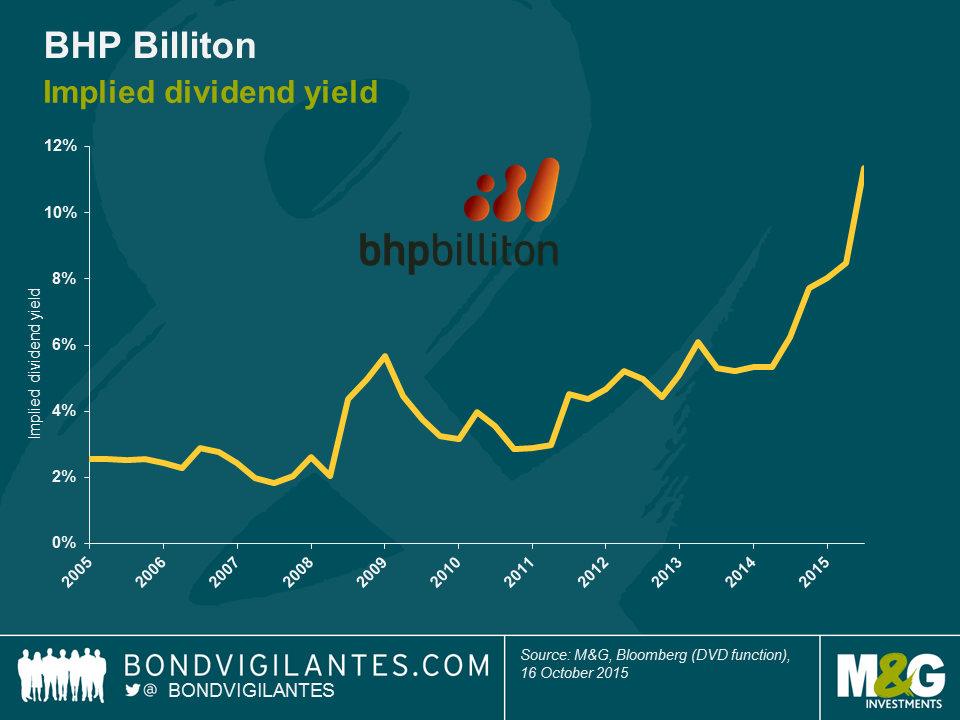

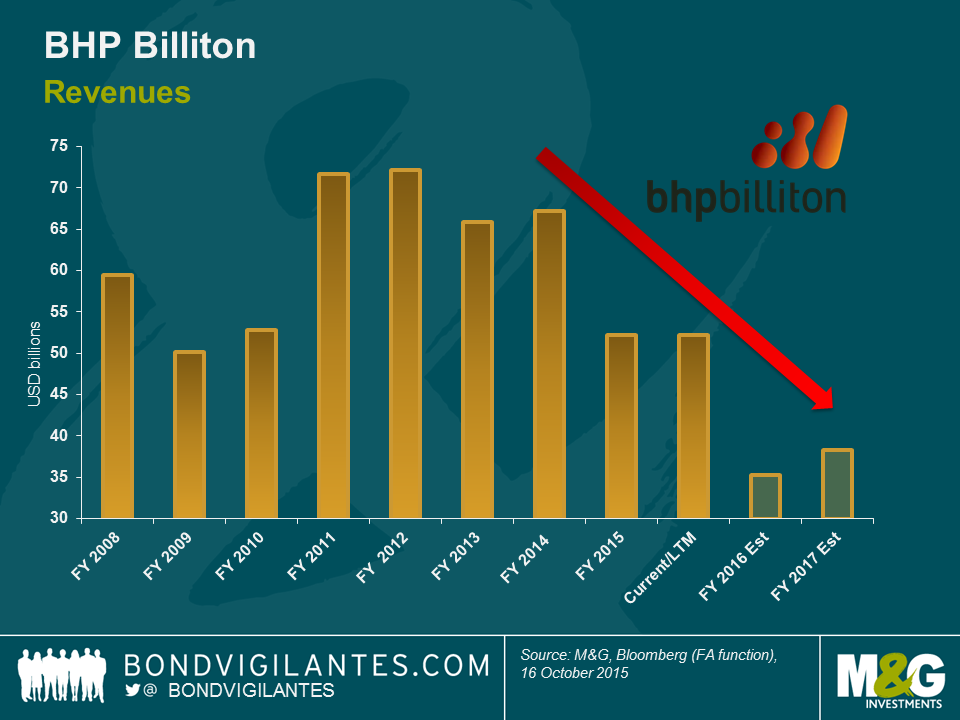

It has been a rough ride for metal and mining giant BHP Billiton. Revenues have come under persistent pressure due to weakening commodity prices. Despite one of the strongest balance sheets in the sector, promises made to shareholders have proven tough to keep.

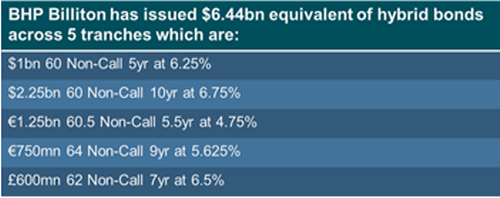

With these commitments in mind the company turned to a nervous bond market earlier this week for some $6.44bn equivalent of hybrid debt funding as outlined below.

Back in May 2015 BHP spun off certain assets into a new business – South32 – whilst assuring investors it would be able to maintain the company’s dividend in line with its policy to ‘steadily increase or at least maintain the dividend per share.’ At current prices and despite a significant cost cutting exercise, the company will be free cash flow negative to the tune of -$2.5bn after maintaining said dividend. With little sign of a near term recovery in commodity prices and a commitment to a solid single A rating, it would seem management have somewhat backed themselves into a corner. A sceptical equity market has watched the implied dividend yield climb significantly through 2014 and 2015 to an elevated 10% area today.

Locking in a blended cost of hybrid debt funding at 6% for a minimum of five years, primarily to maintain the dividend in the face of commodity weakness, may well prove to be a costly error. With an interest bill set to rise by $160m per annum (before tax shield savings), perhaps a near term cut to the dividend would have been a more appropriate response which frankly is already discounted by the market.. Companies often pay special dividends when times are good and turn to bond markets when times are tough. The reason is that reducing the dividend can be a costly exercise for existing equity owners which is a short-sighted strategy in my opinion. Cyclical companies – like BHP – should leave themselves scope to respond to both cyclical downturns as well as upturns. No one can tame the commodities cycle.

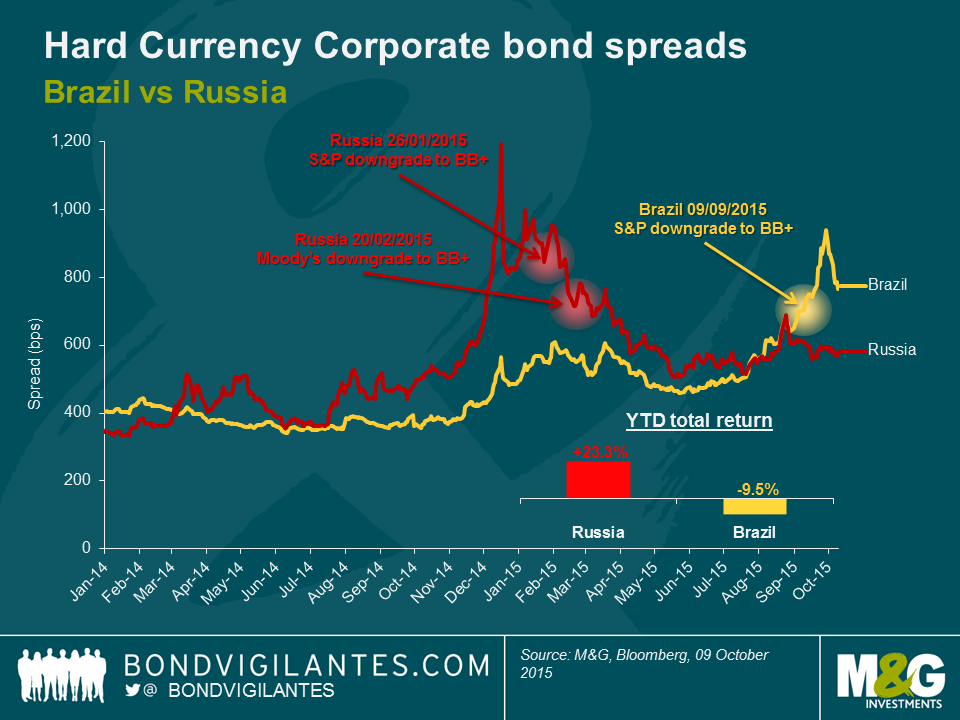

Brazil has been facing the perfect storm since the re-election of Dilma Rousseff in October 2014 and asset prices in Latin America’s largest country have collapsed. Credit default swaps on Brazil 5-year sovereign debt in US dollar and hard-currency corporate bond spreads widened to as much as 545 bps and 938 bps respectively, as at the end of September 2015, which is higher than during the 2021/12 global financial crisis and the highest since Brazil’s 2002 crisis. The adequate level of foreign exchange reserves – one of the few positives for the country – did not prevent S&P from downgrading Brazil’s sovereign rating to junk last month, which as Claudia wrote, was inevitable given the weak macroeconomic and political environment.

Against this backdrop, many bond investors are looking at Brazilian assets in the same way they opportunistically eyed Russia at the beginning of this year. Russia, which was downgraded to junk by both S&P and Moody’s respectively in January and February of this year, has generated one of the best returns year to date in the emerging market debt universe. Russian hard-currency corporate bond spreads have tightened by more than 30% (or 273bps) year to date despite the ongoing economic sanctions from Western countries, low oil prices and weak Ruble and Russia 5YR CDS has rallied 32% (180bps) year-to-date to 370 bps as at 9th October 2015.

When looking at corporate bonds as per the above graph, Brazil’s recent widening in spreads with a peak after the September sovereign downgrade to junk shows some similarities to what Russia experienced earlier this year in January/February when a number of Russian corporate issuers became fallen angels to speculative grade. While they never recovered their investment grade ratings, Russian corporate bonds then outperformed the rest of emerging markets. Will Brazilian corporate bonds follow the same path in the short term? This is unlikely as Brazil is not Russia.

First, the macro picture is very different. Although both economies have plunged into recession this year, it was the result of external factors for Russia while Brazil is arguably facing more domestic headwinds than external threats. The Russian economy has been hard hit by the international sanctions and low oil prices. For Brazil, political issues (an out-of-favour President and the massive Petrobras corruption scandal) are arguably at least as detrimental to investor sentiment as low commodity prices are to its negative terms of trade.

Second, Russian issuers have shown incredibly resilient credit fundamentals in the current economic environment. The weak Ruble has been helping exporters (oil & gas, metals & mining, chemicals) to improve their competitiveness as their costs are in local currency and their revenues are in US dollars. Facing a virtually closed primary market over the past 12 months, Russian issuers have also shown strong discipline in keeping leverage down and maintaining adequate cash levels in order to meet debt maturities. Finally, the scarcity of bonds has been helpful from a market technicals point of view. In Brazil, this is quite the opposite. Many issuers have significant external debt on their balance sheet and the weakening Real has materially increased debt levels in US dollars and interest expenses for domestic players with no hedging in place. Leverage is on the rise as both debt levels increase and earnings reduce on the back of the recession in Brazil and weak commodity prices. In addition, the “Lava Jato” (Car Wash) corruption scandal is likely to remain an overhang on almost all corporate debt issuers in the country.

In this context, we expect default rates to increase in Brazil. Unlike Russia, which has been broadly a macro call in the first 9 months of this year, credit differentiation in Brazil will be critical and bond returns uneven. There is no doubt that some opportunities for decent returns have emerged among unduly punished bonds, but Brazilian corporate bonds as a whole are unlikely to generate such strong returns in the short term as those seen in Russian credit so far in 2015.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.