Brazil is not Russia so don’t expect Brazilian bonds to deliver Russian returns

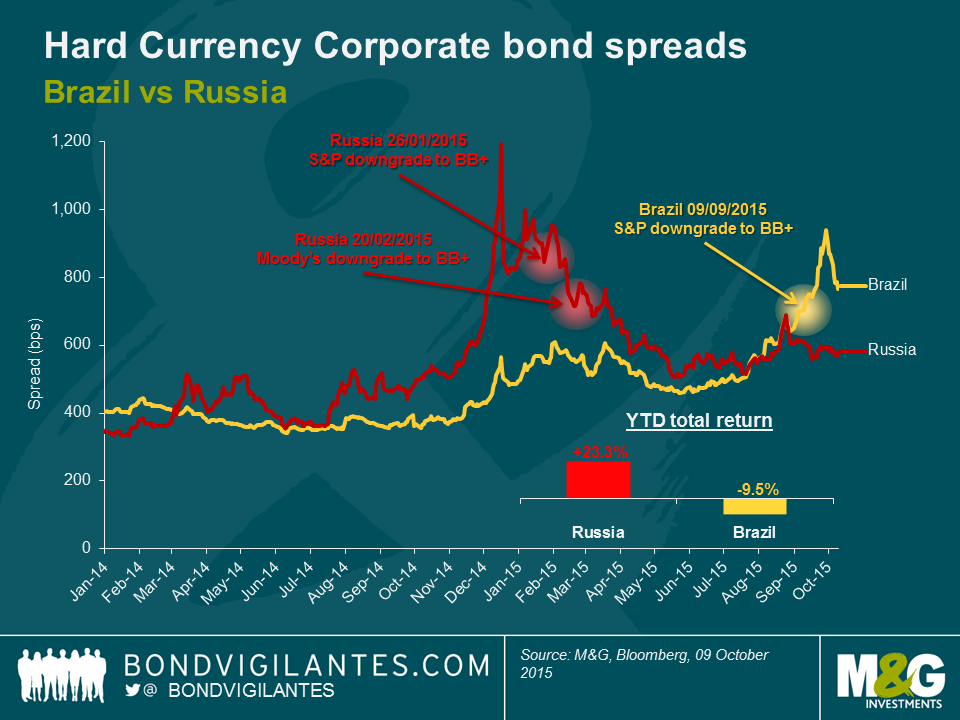

Brazil has been facing the perfect storm since the re-election of Dilma Rousseff in October 2014 and asset prices in Latin America’s largest country have collapsed. Credit default swaps on Brazil 5-year sovereign debt in US dollar and hard-currency corporate bond spreads widened to as much as 545 bps and 938 bps respectively, as at the end of September 2015, which is higher than during the 2021/12 global financial crisis and the highest since Brazil’s 2002 crisis. The adequate level of foreign exchange reserves – one of the few positives for the country – did not prevent S&P from downgrading Brazil’s sovereign rating to junk last month, which as Claudia wrote, was inevitable given the weak macroeconomic and political environment.

Against this backdrop, many bond investors are looking at Brazilian assets in the same way they opportunistically eyed Russia at the beginning of this year. Russia, which was downgraded to junk by both S&P and Moody’s respectively in January and February of this year, has generated one of the best returns year to date in the emerging market debt universe. Russian hard-currency corporate bond spreads have tightened by more than 30% (or 273bps) year to date despite the ongoing economic sanctions from Western countries, low oil prices and weak Ruble and Russia 5YR CDS has rallied 32% (180bps) year-to-date to 370 bps as at 9th October 2015.

When looking at corporate bonds as per the above graph, Brazil’s recent widening in spreads with a peak after the September sovereign downgrade to junk shows some similarities to what Russia experienced earlier this year in January/February when a number of Russian corporate issuers became fallen angels to speculative grade. While they never recovered their investment grade ratings, Russian corporate bonds then outperformed the rest of emerging markets. Will Brazilian corporate bonds follow the same path in the short term? This is unlikely as Brazil is not Russia.

First, the macro picture is very different. Although both economies have plunged into recession this year, it was the result of external factors for Russia while Brazil is arguably facing more domestic headwinds than external threats. The Russian economy has been hard hit by the international sanctions and low oil prices. For Brazil, political issues (an out-of-favour President and the massive Petrobras corruption scandal) are arguably at least as detrimental to investor sentiment as low commodity prices are to its negative terms of trade.

Second, Russian issuers have shown incredibly resilient credit fundamentals in the current economic environment. The weak Ruble has been helping exporters (oil & gas, metals & mining, chemicals) to improve their competitiveness as their costs are in local currency and their revenues are in US dollars. Facing a virtually closed primary market over the past 12 months, Russian issuers have also shown strong discipline in keeping leverage down and maintaining adequate cash levels in order to meet debt maturities. Finally, the scarcity of bonds has been helpful from a market technicals point of view. In Brazil, this is quite the opposite. Many issuers have significant external debt on their balance sheet and the weakening Real has materially increased debt levels in US dollars and interest expenses for domestic players with no hedging in place. Leverage is on the rise as both debt levels increase and earnings reduce on the back of the recession in Brazil and weak commodity prices. In addition, the “Lava Jato” (Car Wash) corruption scandal is likely to remain an overhang on almost all corporate debt issuers in the country.

In this context, we expect default rates to increase in Brazil. Unlike Russia, which has been broadly a macro call in the first 9 months of this year, credit differentiation in Brazil will be critical and bond returns uneven. There is no doubt that some opportunities for decent returns have emerged among unduly punished bonds, but Brazilian corporate bonds as a whole are unlikely to generate such strong returns in the short term as those seen in Russian credit so far in 2015.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox