A quantitative analysis of US recession probabilities

Guest contributor – Jean-Paul Jaegers CFA (Senior Investment Strategist, Prudential Portfolio Management Group)

Getting a sense of when recessions are about to happen is a near impossible task, as evidenced by official institutions that often fail to forecast recessions, and organisations like the NBER (National Bureau of Economic Research) that specialises in dating US business cycles, dating recessions only with a number of quarters of hindsight.

Accepting that it is a complex task however, we can attempt to gauge potential contractions through the use of economic data sets that are cyclical and timely. There is no flawless measure and economies are rather complex, hence we choose to look at a selection of time series that measure economic conditions from different angles. Some measures used are from a business perspective, some from the labour market and some from consumers.

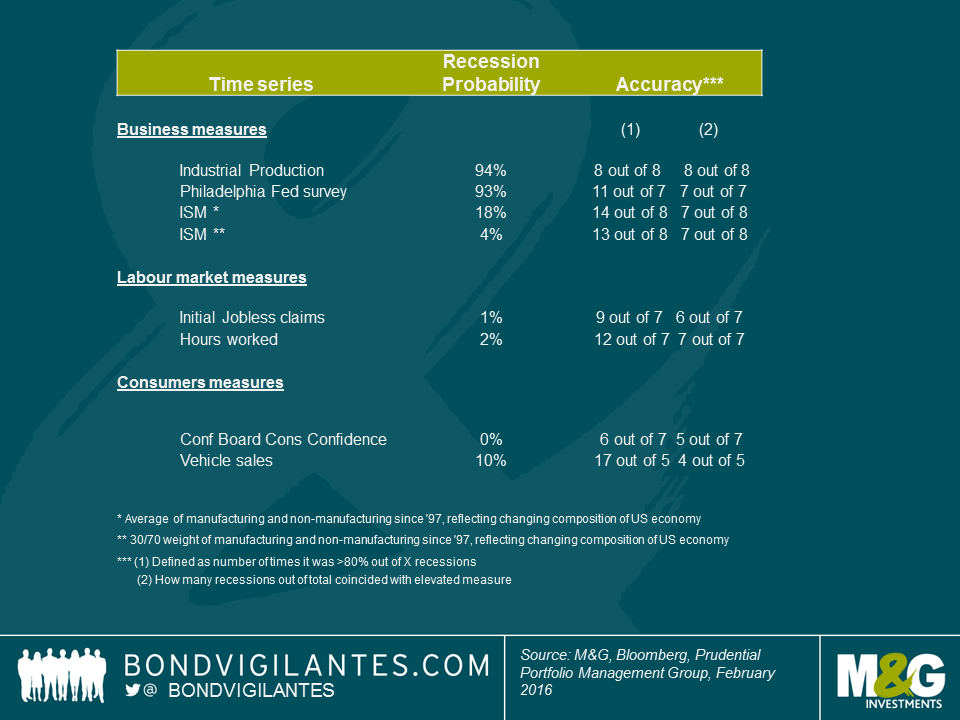

We will apply a technique called a Markov model, which solves for two-states – a high-state and a low-state (ie it estimates two distributions that best describe the aggregate distribution). It takes the most recent observation and assigns a likelihood for currently being in each of those two states. This approach is often used for detecting turning points. Our assumption here is that the low-state is representative of a recession or economic contraction. For this exercise we show the probability of the low-state (ie recession). In addition, as the measure can indicate a high likelihood of recession more often than actually happens in practice, we also list some measures on accuracy.

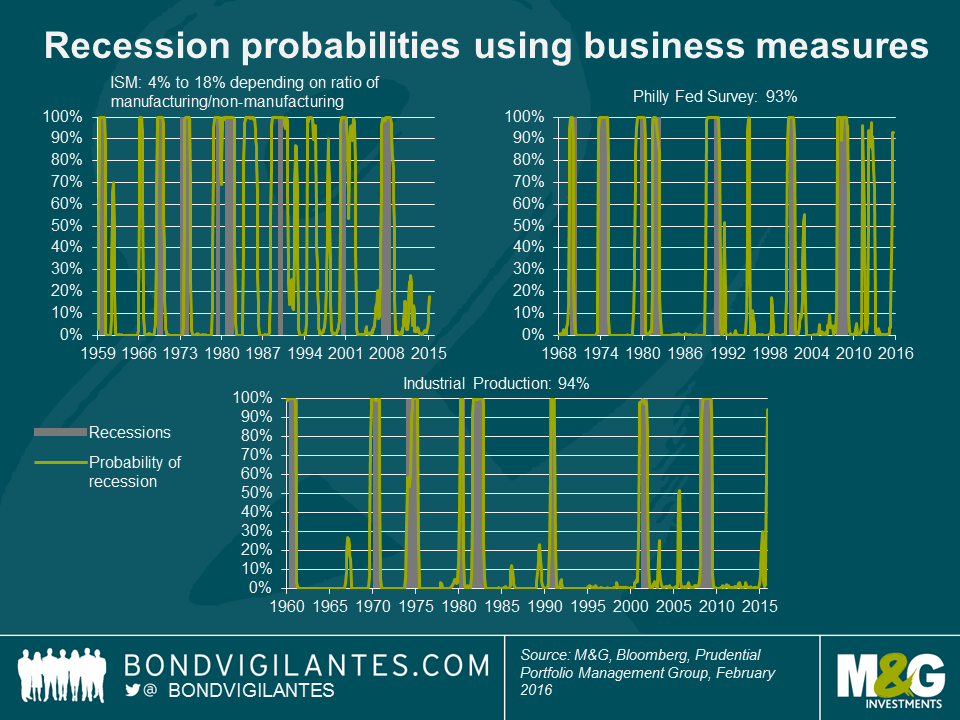

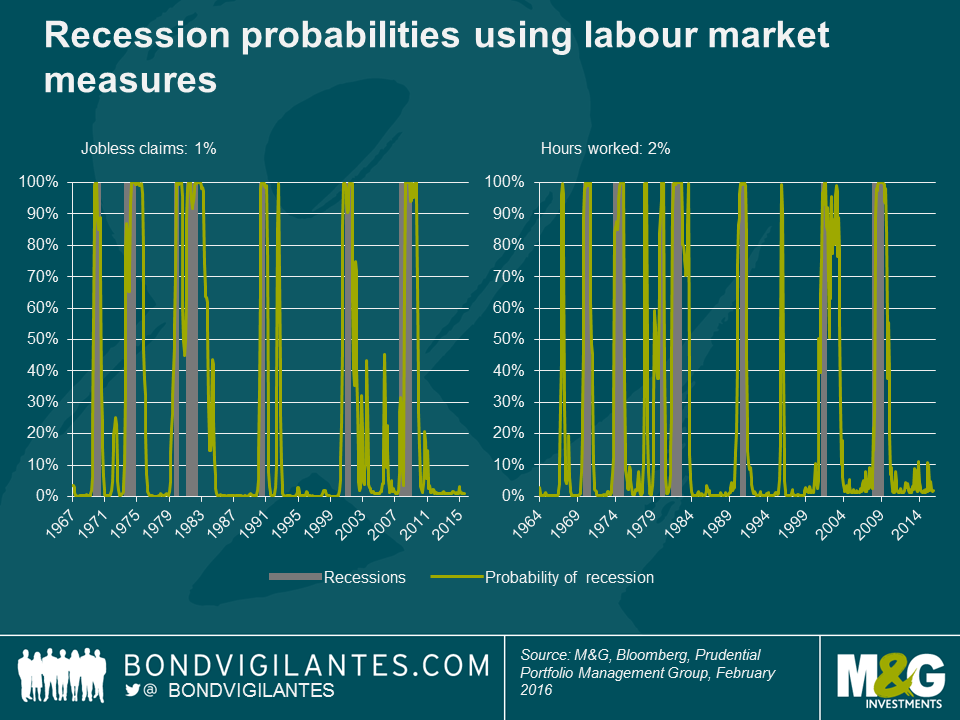

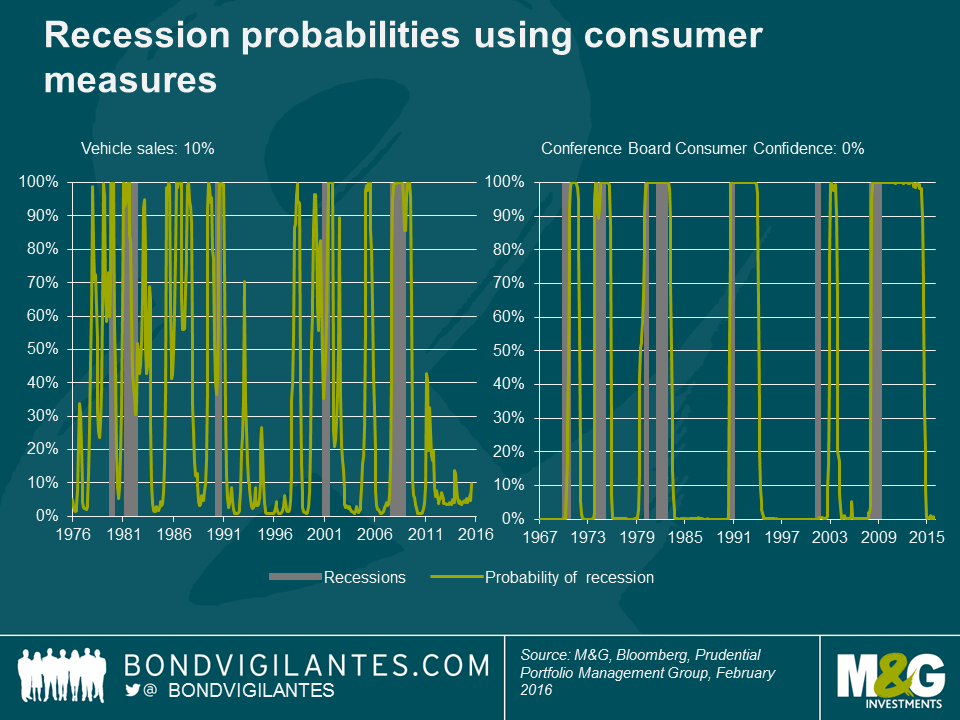

In the charts below the grey-shaded periods are recessions as defined by the NBER, and the green line is the probability as estimated by the Markov model.

We can see that industrial production has historically been a very accurate predictor of recessions, having predicted all 8 recessions since the 1960’s, whilst also giving few, if any, false signals. Industrial production has been weak recently, and based on this measure, the likelihood of recession is currently very high at around 94%.The Philadelphia Fed Business Outlook Survey, which questions manufacturers in Pennsylvania, southern New Jersey and Delaware about their view of business conditions, is also indicating a high probability of recession. It too has a fairly decent track record, although it has given some false signals in the recent past. Set against this however, using different combinations of ISM manufacturing and non-manufacturing tells the opposite story. Whilst ISM manufacturing data has been very weak, non-manufacturing (although also weakening recently) has been stronger, and a combination of the two currently indicates a meaningfully lower likelihood of recession. One of the bright spots of the US economy in recent times has been the labour market and unsurprisingly, when we use labour market measures, we find a very small probability of being in a recessionary environment of just 1% to 2%. Consumer confidence is riding high at the moment, helped by the strong jobs market and falls in gas prices, and consumer based measures also suggest low likelihoods of being in a low-state at this moment.

So an assessment of a quantitative technique on a range of time-series does currently not give a widespread indication of worryingly high likelihoods of recession. The disturbing element however, is the signal from industrial production, which has historically had a good success rate at accurately predicting recessions.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox