Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

There has been a barrage of G7 central bank coverage in March, culminating in much talk, but resulting in – on the whole – little new action. The Bank of Japan remained on hold (after adopting a surprise negative rate policy at the end of January), the Federal Open Market Committee (FOMC) delivered a “dovish hold” (keeping interest rates unchanged while lowering their longer term rate guidance) and the Bank of England voted unanimously to keep the interest rate at 0.5%.

Some of the more interesting policy action has been in Europe where the European Central Bank (ECB) unveiled a raft of additional measures in its latest round of monetary easing, which included a further cut to its already negative deposit rate. Again, this has been well covered by market commentators. But perhaps some of the lesser discussed – though no less deserving – coverage of late has been given to the Nordics, where negative nominal rates have been a feature of some of these markets for some time. If the Nordic region is the gaping hole in your monetary policy bank of knowledge, the following discussion should go some way to address this.

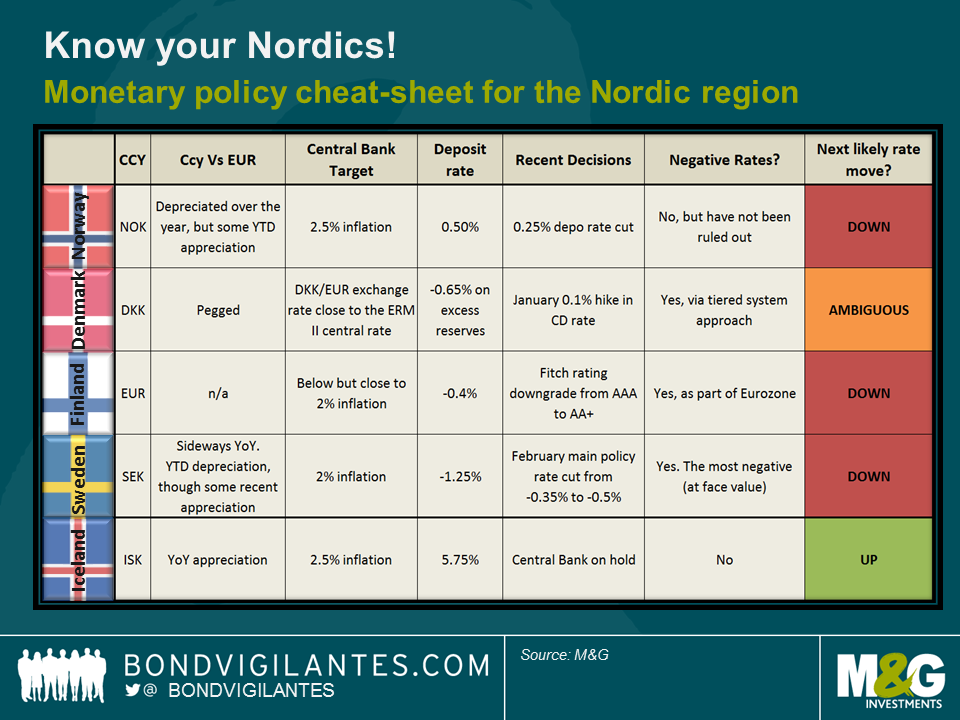

Norway: Eased in March, more to come?

On 17th March – the day after the FOMC meeting – the Norges Bank cut its deposit rate from 0.75% to a new low of 0.5%. The weaker external growth environment, looser policy abroad and renewed oil price swings were some of the reasons cited for this move.

The Norges bank has an inflation target of 2.5% and whilst the CPI inflation forecast was revised upwards in the short term (from 2.6% to 3.2% for the first quarter of this year), much of this is due to the lagged impact of the Krone depreciation experienced in line with the fall in the oil price in 2015. Given the YTD rebound in the Krone, the currency effect is likely to dissipate in the longer term. Teamed with a potentially slowing global demand environment as well as subsiding domestic wage pressures, inflation is forecast to end 2019 at 1.6%, well below target.

Like many of its developed country peers, Norway now too finds itself flirting with the zero lower bound. What is of particular interest is that the central bank has not ruled out the use of negative nominal interest rates declaring that “should the Norwegian economy be exposed to new major shocks, the Executive Board will, however, not exclude the possibility that the key policy rate may turn negative”. Perhaps one to watch in the race to the bottom.

Denmark: Protecting the peg

Several developed market economies have now embraced the negative nominal rate experiment, but it was the Danmarks Nationalbank (DNB) that was the pioneer. Unlike the majority of other central banks in the area, inflation is not the target, but its commitment to keep the DKK/EUR exchange rate close to the ERM II central rate with a narrow fluctuation band of ±2.25%.

At the start of this year, the DNB hiked rates from -0.75% to -0.65% in defence of the band. Though this move was a tightening, the bank also made tweaks to its tiered deposit system, by lowering the current account limit from DKK 63.05bn to DKK 32bn. The limit caps the amount of commercial bank reserves that can be held with the DNB at the 0.0% current account rate, while the excess above this limit gets charged at the more punitive certificate of deposit rate (-0.65%), which should stimulate bank lending – an act of credit easing.

The next move in rates is ambiguous. If there are further sizeable capital outflows and reserve shrinkage, the central bank will likely hike rates again. Conversely, should capital flows reverse and require intervention by selling DKK, the central bank could cut the policy rate or accumulate FX reserves again.

Finland: Part of the Eurozone’s quest to ease financial conditions

On the 11th March, rating agency Fitch downgraded the sovereign from AAA to AA+ naming continued weak economic performance as the driver (2015 GDP expanded by 0.4%, the lowest growth rate in the EU with the exception of Greece). With no decisive evidence of a meaningful pick-up in potential growth over the medium term, public debt dynamics continue to weaken.

As a Eurozone country, Finland works as a proxy for the ECB’s monetary policy in the Nordic region. In line with its Euro peers, Finland is on the receiving end of monetary easing as the ECB lowered deposit rates to -0.4% at the 10th March meeting. Unlike Denmark however, this is not a tiered system and banks are arguably penalised more heavily for using the deposit facility. Although the deposit rate is more likely to move lower than higher in the short term, the ECB appears to be tilting its focus towards QE and other extraordinary methods. Indeed, the expansion of QE into investment grade corporate bonds as well as the new TLTROs proffers two such measures.

Sweden: Deposit rate is not what it seems

The Riksbank’s deposit rate is hugely negative at a whopping -1.25%. At face value this looks highly punitive, although this facility is barely used. In practise, Swedish debt certificates (issued weekly with interest set at the base repo rate of -0.5%) soak up the majority of the banking sector’s surplus liquidity, with any excess dealt with in daily fine-tuning operations that cost an extra -0.1% (interest rate becomes -0.60%). As a result of this, unlike in the Eurozone where the interbank rate trades close to the deposit rate, Sweden’s interbank rate instead trades closer to its base rate of -0.5% (reduced from -0.35% on 11th February). Moving the deposit rate further negative would therefore do little to change banks’ decision making. Instead the main base repo rate is the more important focus.

Another aspect to bear in mind is the appreciation in the krona versus the euro over the past couple of months. If this continues, the Riksbank may need to extend its QE programme beyond June to prevent this from dampening inflation. The current programme of SEK 200bn represents approximately 30% of the outstanding government debt, leading some to speculate that any additional QE would be in the form of corporate bonds purchases, similar to the ECB’s recent move.

Iceland: In hiking mode, the next move is up

For completeness of the Nordic region, we turn to Iceland, which breaks the mould somewhat. Whilst a lot of the region has been battling with “missingflation”, Iceland has growing domestic inflationary pressures, a relatively high deposit rate and subsequently, a central bank in hiking mode. Though the next move in rates is likely to be up, the appreciation in the Icelandic krona alongside low global inflation perhaps gives the central bank scope to raise interest rates more slowly than was previously considered necessary.

Though one may be tempted to assume that the whole of Europe (or indeed the developed world) is suffering from low inflation and that all central banks are preoccupied with inflation targets, the Nordic region shows just how diverse policy truly is. It’s not just an issue for the G7 countries. Despite being geographically close, central bank policy in the Nordic region is incredibly varied, even when sometimes the objective is similar.

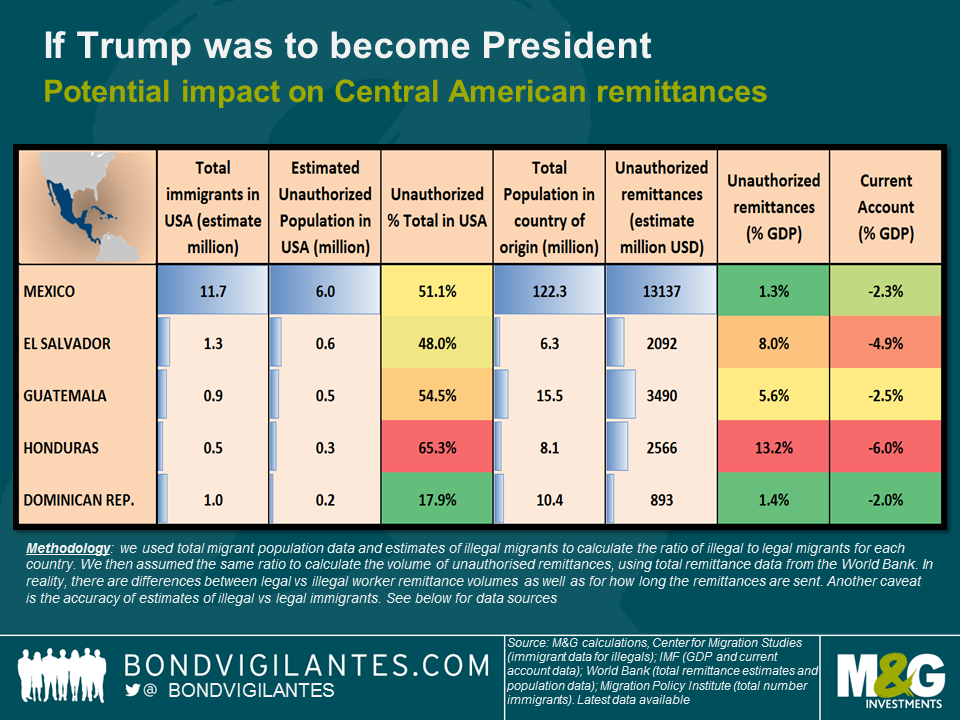

The US election campaign has surprised everyone thus far. Candidate Donald Trump has vowed to deport all of the 11 million illegal immigrants currently living in the US. He has also declared that he would impound all remittance payments derived from illegal wages. We have written before how Central America and the Caribbean would benefit from improving US growth and have been invested in various sovereigns in the region as a result. Remittances benefit receiving countries as they reduce their current account deficits and have a positive impact on domestic consumption and growth, although studies have also pointed out some negative impact through increasing income inequalities or potential for currency appreciation, making exports less competitive.

Assuming that Trump was to become President and – logistics and feasibility aside – that all the illegal immigrants be deported, how will this impact the region’s remittance flows? In the table below we used total migrant population data from the Migration Policy Institute and estimates of illegal migrants from the Center for Migration Studies to calculate the ratio of illegal to legal migrants for each country. We then assumed the same ratio to calculate the volume of unauthorised remittances, using total remittance data from the World Bank. In reality there are differences between legal vs illegal worker remittance volumes as well as the length of time they are sent for, and the accuracy of the illegal migrant data could also be questioned.

The focus of the rhetoric has centred on Mexico, as it has the largest absolute number of immigrants in the US. However, as can be seen in the table, the biggest losers would be the smaller countries of El Salvador and Honduras. Both have a much higher share of remittances vs. GDP and current account receipts because their share of illegal immigrants is higher in comparison to the size of their economies and population.

Mexico, instead, would be much more negatively affected should the existing NAFTA free-trade agreement be renegotiated, as its economy is much more dependent on exports to the US than worker remittances.

Clearly, there are other broader implications that are much harder to quantify. Larger current account deficits would lead to a combination of weaker currencies, higher debt levels and nominal price deflation in the case of dollarized El Salvador. Growth could also be lower if the increased workforce is not able to find similar opportunities at home, which would be negative for their fiscal accounts and debt dynamics. Let’s hope that common sense and the impracticality of deporting 11 million people prevails in the end.

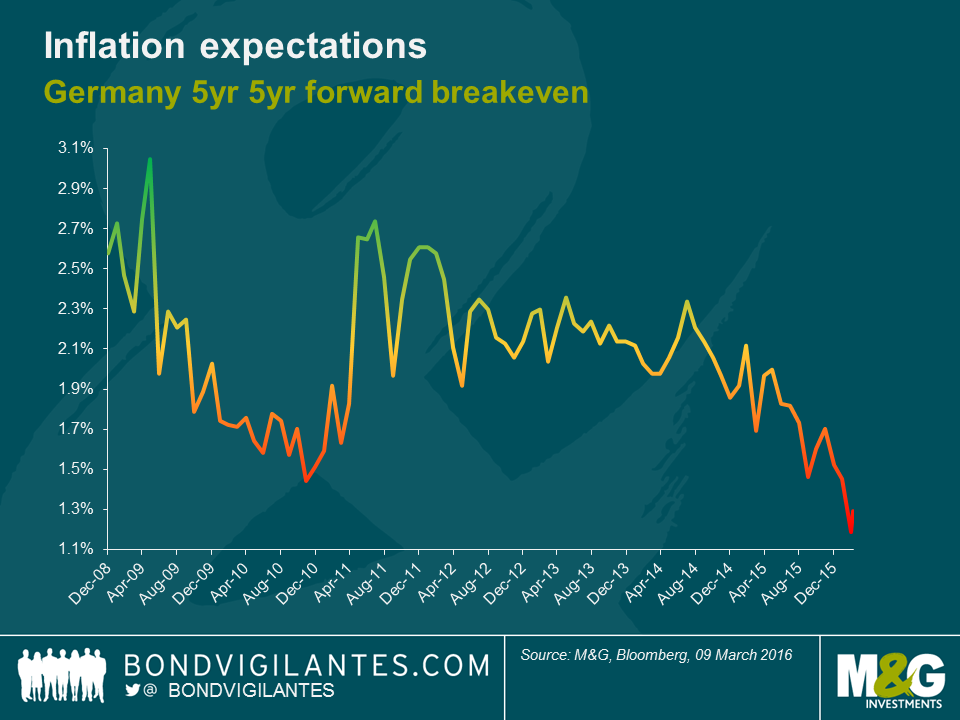

The simple answer is a no. Eric Lonergan in a guest blog has already (see here) debunked the idea that central banks are at the zero bound. And since then the market has become increasingly confident that the ECB will cut its deposit rate further into negative territory at tomorrow’s meeting. And it has reason to do so. Inflation and growth will be lower than the Bank had forecast a mere three months ago with inflation expectations also falling out of bed.

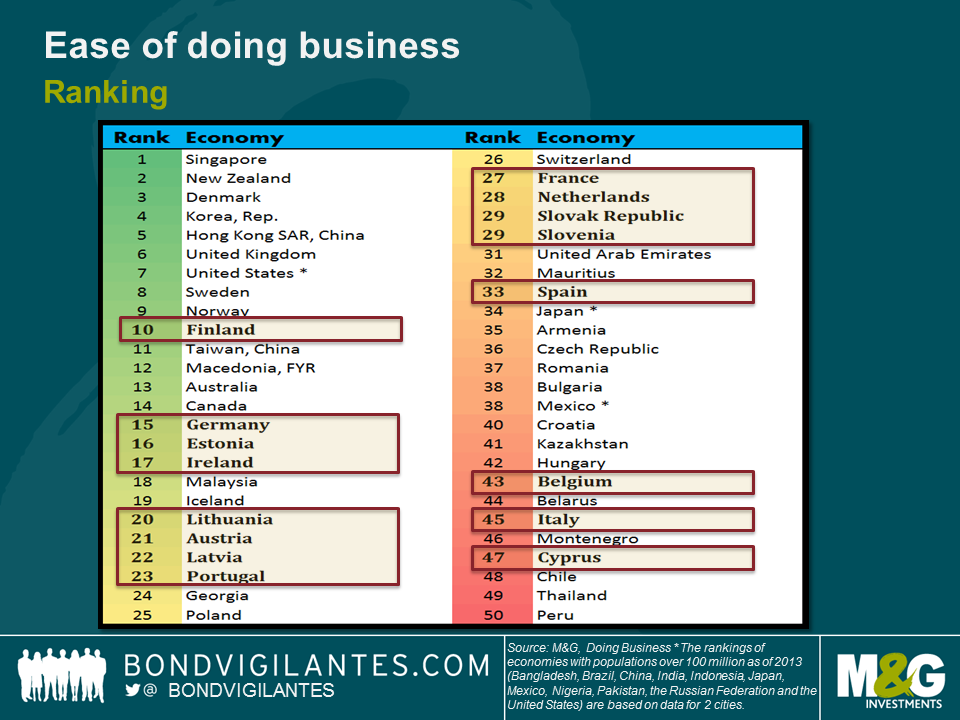

But that isn’t to say that there aren’t diminishing returns to be had from a further loosening of policy. The reality is that many of the problems holding back the Eurozone are structural in nature. And doesn’t the ECB know it. I can hardly remember a press conference when Mario Draghi hasn’t failed to mention the need to address these issues. Hardly surprising given that the Eurozone is only represented twice in World Bank’s top fifteen ‘Ease of doing business survey’. The likes of France at 27, Spain at 33, Italy at 45 and Greece at 60 makes for painful reading.

The ECB is acutely aware of the moral hazard it creates in addressing the Eurozone’s troubles purely via the monetary channel. And yet with a sole mandate to hit an inflation target of close to but below 2%, they are once again finding themselves with the unenviable task of having to do the bulk of the heavy lifting. On Thursday we will likely see a cut to the deposit rate with some sort of tiering in an attempt to address some of the challenges faced by the banking system (see Mario’s blog post), as well as an extension to the PSPP (QE programme), both in terms of size and duration. We may even see a greater willingness to buy certain corporate bonds – although this will likely be a step too far for the majority on the Governing Council.

But the reality is that increased productivity and greater innovation is much needed to drive the Eurozone. Antiquated bankruptcy regimes need to be radically reformed, red tape needs to be removed and the banking system needs to own up to further loan losses that it has yet to provision for. These changes aren’t easily achieved, not least because they require the sort of short term pain that politicians rarely have long run incentives to deliver.

Consider the case of Italy. Since the global financial crisis the Italian housing market has fallen in value by around 19% from its peak. This, combined with recessions that have left Italian GDP around 10% lower than in 2008 and rises in unemployment to around 12%, have conspired to create a large amount of c. €200Bn of non-performing loans (NPL’s) in Italy as households and companies have encountered difficulties in servicing their debt.

Unlike in other Eurozone periphery countries such as Portugal and Spain, Italy has been slow in restructuring its banks and addressing the problem with many NPLs still sitting on banks’ balance sheets. The Italian banking system is therefore considered to be weak and there have been a wave of recent high profile bank collapses that have resulted in ‘bail-ins’. With this in mind the Italian authorities have just set up a scheme to create Asset Management Companies who will then look to securitize these non-performing loans, in theory reducing a bank’s balance sheet and allowing them greater scope to lend to the broader economy. As the scheme is very much in its infancy we will have to wait to see whether it can have the desired effect.

Absent further structural change I’m convinced the Eurozone will labour under a cloak of lower potential growth and struggle to encourage investment given the need to earn an attractive rate of return on capital. Yes the ECB can likely drive risk-free rates even lower. Yes they can depreciate the €. And yes they can provide ever more liquidity to the banking system. These may all help near term. But without real reform the market will increasingly worry that we have reached the limits of monetary policy. And at some point if the market cannot be convinced otherwise, then the consequences will be significant.

Ahead of tomorrow’s ECB monetary policy meeting, the market has high expectations of rates being cut further into negative territory (consensus is a cut in the deposit rate by 10 to 20 bps). However, a report this week from the Bank for International Settlements (BIS) suggests that cutting rates further could be counterproductive and damaging for the banking sector.

The BIS’s quarterly review, points out that negative policy rates either don’t work in lowering borrowing costs for households and businesses, in which case why bother cutting; or they are passed on in loan rates, which means they must be passed on to depositors too, otherwise bank profits will fall. And if they are passed on to depositors there will be a risk of cash fleeing the banking system, which is another undesirable outcome. The paper did acknowledge that there was one potential transmission mechanism of further rate cuts without such consequences for the Eurozone – euro depreciation might be desirable, although that comes with geopolitical (currency wars) implications.

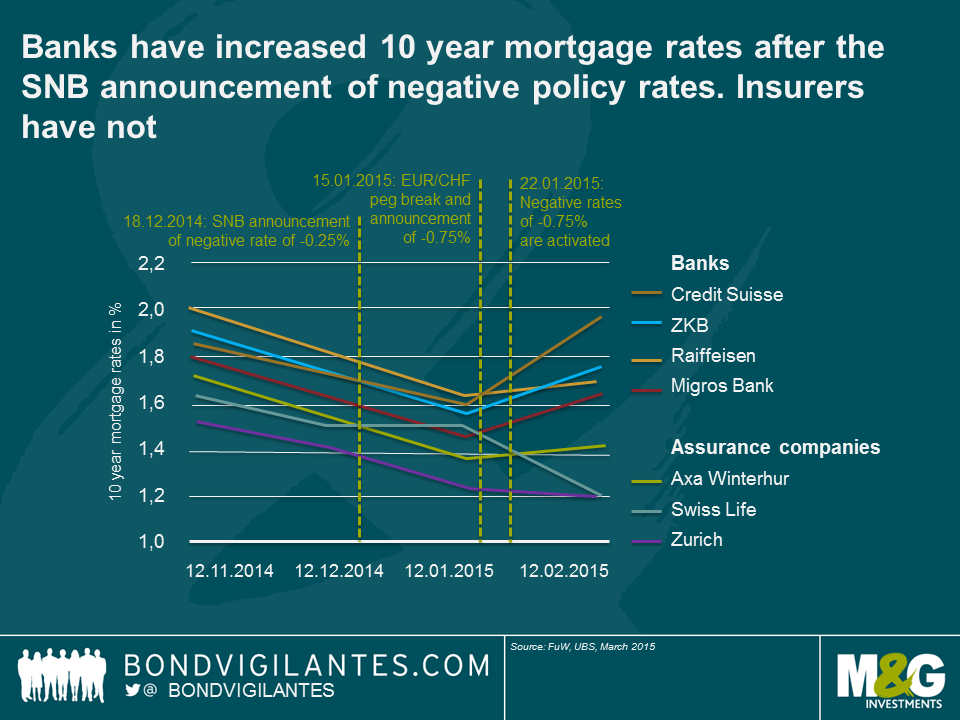

The Swiss experience with negative rates demonstrates clearly that negative rates have direct consequences for banks and can actually lead to tightening credit standards. A note published by UBS a year ago deserves attention as it shows that 10 year mortgage rates for bank clients have actually risen after the SNB has lowered its deposit rate into negative territory.

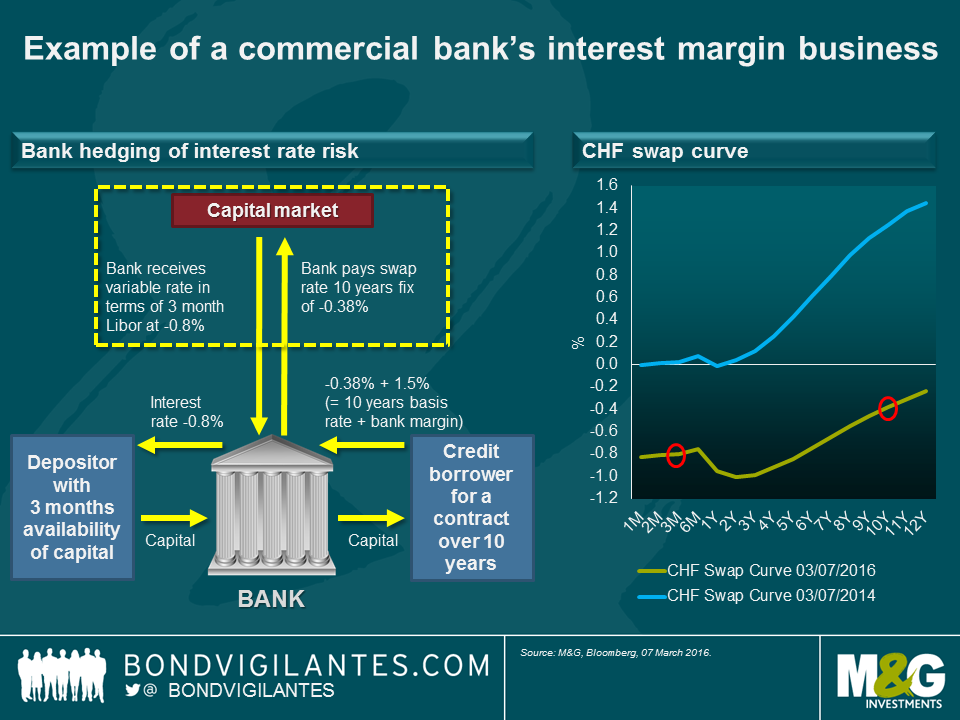

Let’s use a simplified example to illustrate a commercial bank’s interest margin business. A major task of a bank is to act as an intermediary of money. Depositors provide their money to the bank on a short term basis, for example, via savings accounts, whereas many investments require longer-term financial commitments. This process is called maturity transformation, which exposes banks to certain risks, one of which is interest rate risk. Imagine interest rates go up significantly. Savers will demand a higher rate on their savings account, but the bank has agreed a mortgage rate of 1.12% for the next 10 years, as illustrated in the example, which then would have a direct negative impact on the bank’s margin.

Fortunately, there is a capital market to hedge out the interest rate risk. Looking at the current Swiss swap curve, the bank in our example could hedge their interest rate risk by paying away the 10 year fixed part of the curve (-0.38%) to receive a variable rate, which is currently even more negative at -0.8%. In a negative interest rate environment however this process faces a problem. Banks cannot pass on the negative interest rate of -0.8% to their depositors as there is the immediate danger that savers withdraw their money and store it somewhere else, as I wrote in a recent blog.

So what can Banks do?

Either

The latter point is what happened in Switzerland according to the 2015 UBS report. After the SNB’s announcement of negative rates of -0.75% in January 2015, the price for a 10 year mortgage offered by Swiss banks increased. So the banks have increased their margin on long term mortgages to offset the increasingly negative rates on deposits, which equals credit tightening. In other words, mortgage borrowers are subsidising depositors. Assuming banks have also increased their margin on corporate loans as a result of negative rates it would likely weaken economic growth instead of accelerating it.

Swiss assurance companies offer mortgages for clients too, which complicates the situation for banks even more. As UBS points out, insurers have not been forced to increase their margin like banks did, as their deposits are usually long term investments, e.g. a life insurance contract over 10 years. The chart above shows quite nicely that the relative competiveness of insurers’ mortgage offerings has improved compared to banks since the SNB introduced negative policy rates. However, the mortgage business is not a core business for assurance companies, so we can assume they have less information about their borrowers and less extensive credit assessments compared to banks, which according to UBS increases the risk of capital misallocation and higher credit defaults going forward.

Draghi faces a dilemma. Too big a cut of the already negative deposit rates could be perceived negatively by the market as damaging for bank profitability and thus the transmission mechanism to the real economy. He has to live up to his promise of bringing inflation back without breaking the very system that – in the absence of fiscal easing – is needed to spur European companies and households in to growth.

2015 saw global inflation risk premia collapse, led by the developed world. US, UK and European annual inflation rates spent most of the year at or around zero with numerous dips into negative territory. Short dated breakevens correspondingly fell to levels that we last saw during the financial crisis (well, to be fair, they went far lower back then, but we are still at crisis levels today), and bond valuations in large parts of the world were supported by the lowflation and secular stagnation conditions that prevailed.

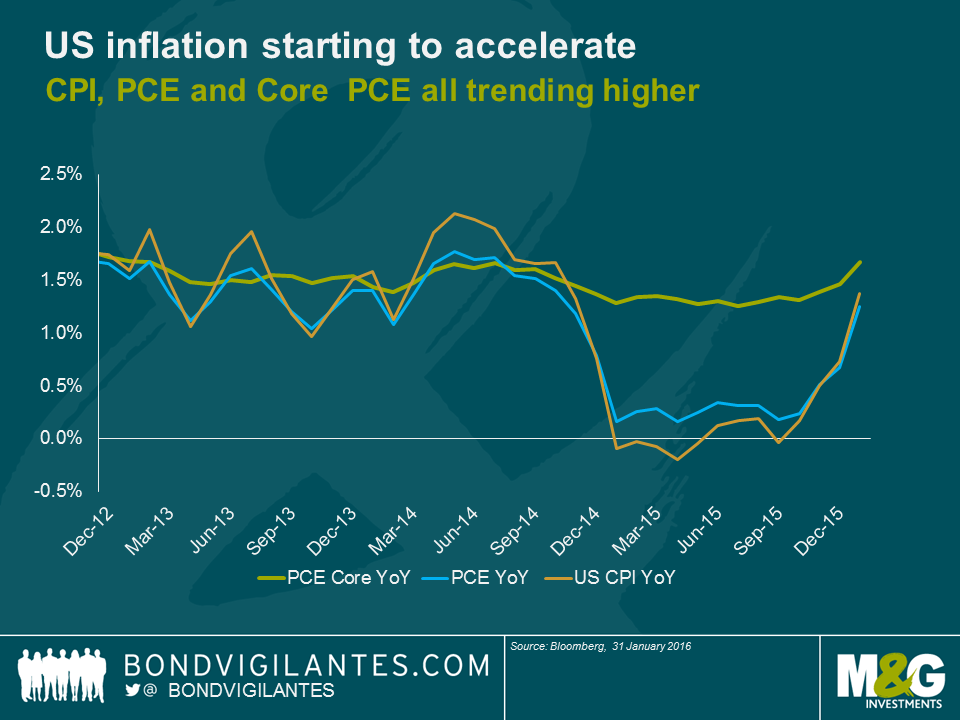

Looking back, three months of inflation releases ago (October 2015) US CPI was 0.1% year over year, the PCE deflator (i.e. the rate the Fed actually tries to target at 2% – see my recent blog) was at 0.2% and fears of deflation were rife on the back of ongoing energy and commodity price collapses, concerns of a Chinese hard landing, the coming interest rate hiking cycle and (related) strong US dollar. The start of 2016 came with a new list of deflationary forces to panic about: a renewed collapse in oil (where the second year halving in price we had once written off suddenly became much more likely), concerns of further Chinese devaluation, and growing fears that the US might even be entering a full blown recession. As a result of such deflationary noise, 5y breakevens hit post-crisis lows of 0.95% in early February.

But the inflation picture looks to have changed over the past few months. CPI is now 1.4% and Core PCE is at 1.7%, not far off the desired 2% and already above the level the Fed had it peaking at at the end of 2016.

Inflationary forces are broadening and accelerating, and it is happening fast. Recent data has shown that goods prices, in spite of the strong dollar, are now rising. Furthermore, ‘sticky’ components of inflation, the major part of which is services, are seeing price rises pick up too, currently running at 2.5%. Rental costs continue to be a source of rising prices and, interestingly, medical costs are now showing signs of life after a period of stagnation early in Obamacare’s life.

It’s true that energy costs remain a drag (and February will be a more negative month for energy contribution than January was), but in a few months’ time (provided the oil price stabilises around current levels) the negative base effects will progressively fade away. When this happens, the rebound in US inflation will exceed that seen in Europe or the UK. In addition the US labour market is tighter than anywhere else and wages are starting to behave as though the NAIRU has been reached.

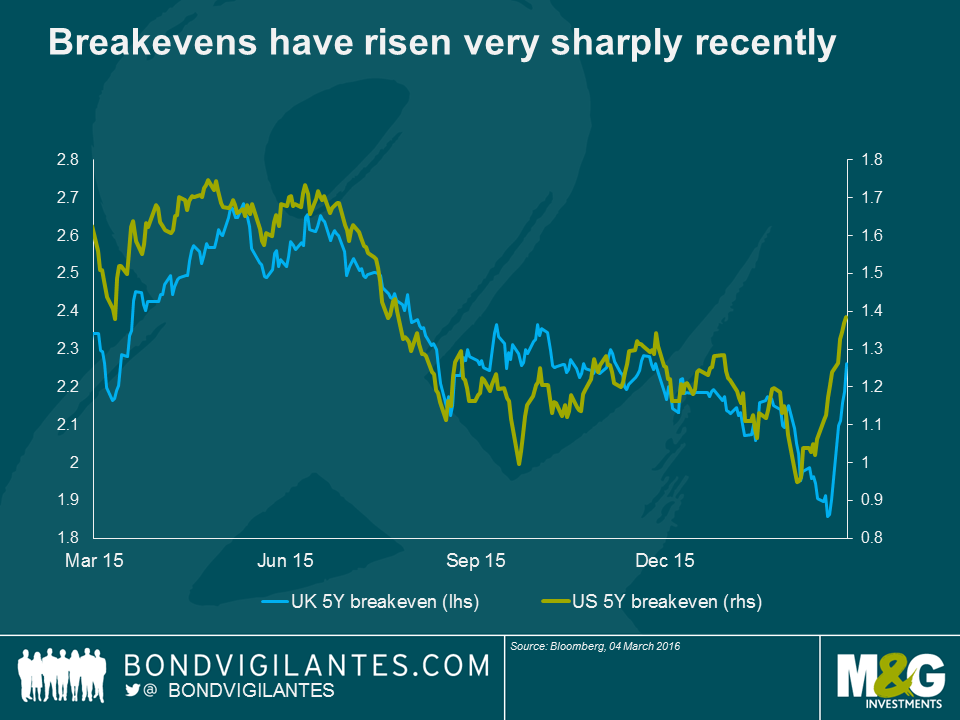

Three months ago inflation was closer to zero than to target. Today it is closer to target than to zero, and is trending higher. The bond market is clearly taking notice. As the chart above shows, US 5 year breakevens are up around 40 basis points over the past three weeks, and UK 5 year breakevens are up a similar amount. A lot depends on the oil price in the near term, but if inflation numbers continue to repair back towards target, then it seems likely to me that breakevens can go further than they have done so far; perhaps significantly so.

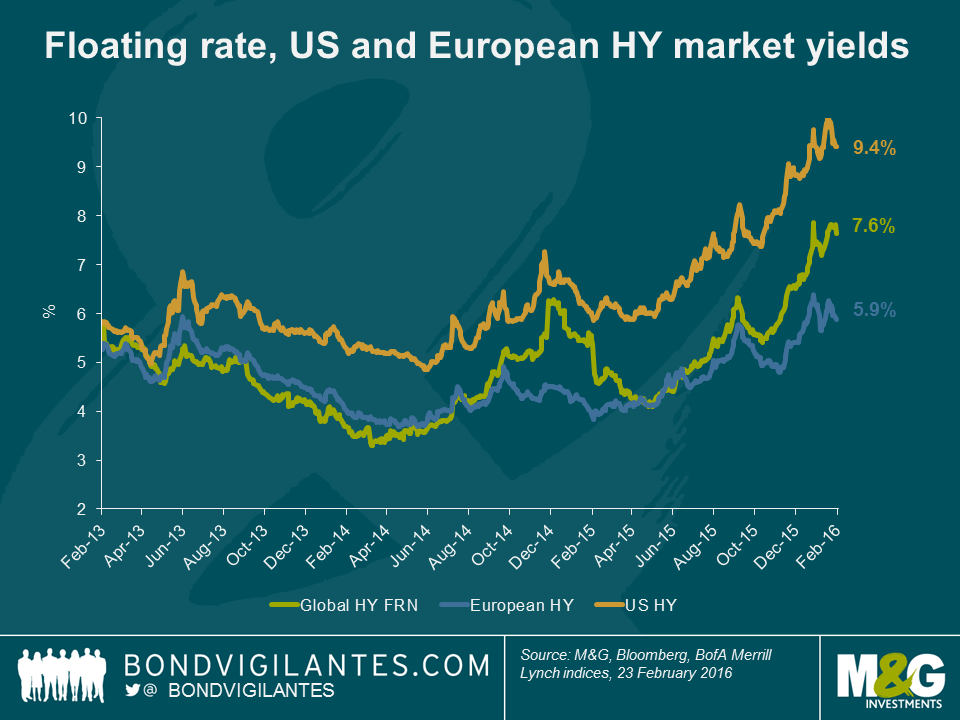

It’s been a difficult past few months for all risk assets, including the high yield markets. Weakest of all has been the US, with negative returns of almost 10% over the past year. As part of this re-pricing, spreads have widened significantly, with the US high yield market touching almost 900bps over treasuries. All-in yields also briefly peaked above 10% last month.

Underlying this has been a major and well publicised sell off in energy credits. The dispersion of returns within the market has been immense. It’s interesting to note that despite more than a 10% sell-off in January and February, the weakness in subordinated bank paper (the AT1/COCO index lost 3% for the year to 23rd February) has been dwarfed by the loss of around 37% in US Energy bonds over the same period. With the increasing prospect of further defaults, getting the sector call right last year was crucial.

So we have widening credit spreads, fears about a general slow-down in growth and deep concerns about capital destruction in a major part of the market. So a terrible time to get into the asset class then? Perhaps not.

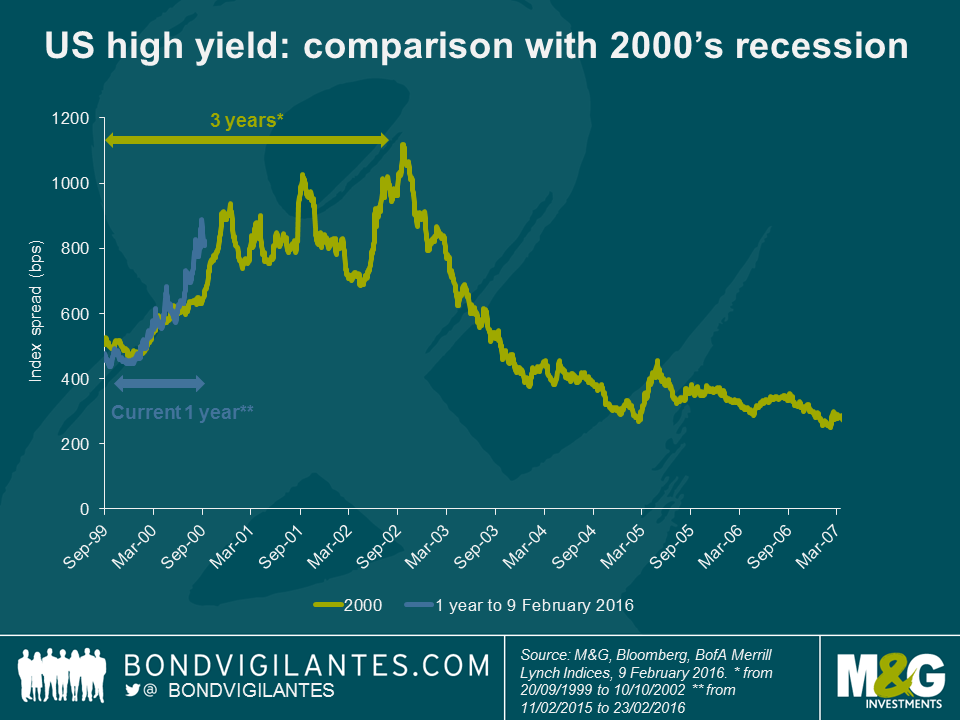

Why do we say this? First of all, there could be some interesting parallels to the high yield market in 2001. The similarities are there – it feels like we are listening to an echo from bond market history.

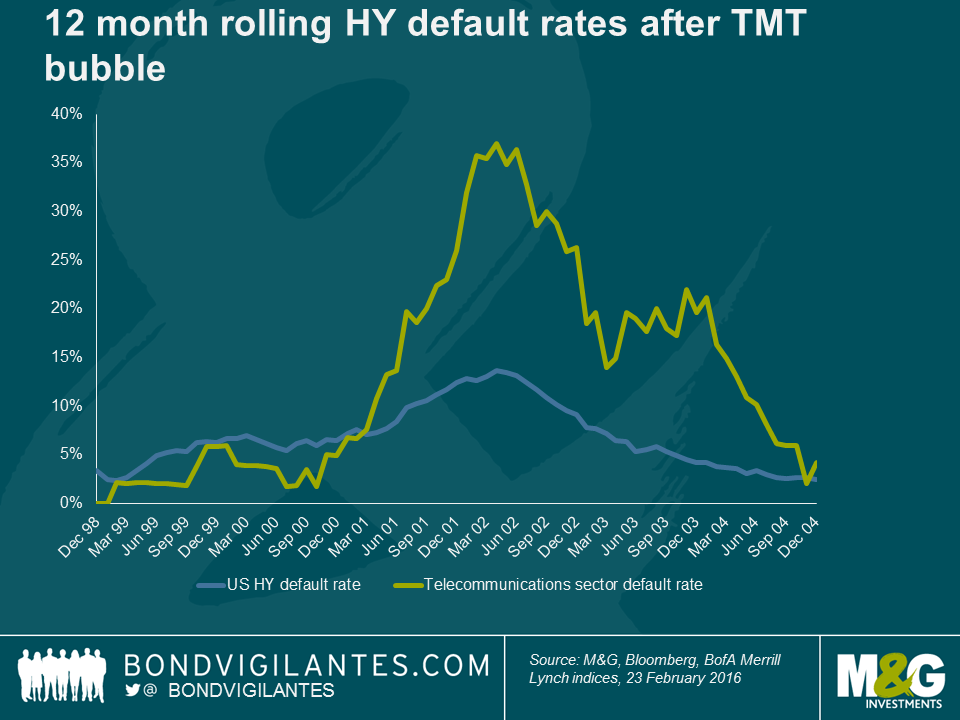

a) Then as now, one sector is the focus of concerns. In 2001 it was the bursting of the TMT bubble and the fallout from the capex splurge of telecommunications businesses, funded by an over-eager high yield market. This led to a spike in defaults and a painful few years for creditors. Now it’s the bursting of a commodity price bubble and the fallout from the capex splurge of energy businesses, funded by an over-eager high yield market.

b) As a result of this corporate overspending and loose credit discipline, there were concerns that this could adversely affect growth in the wider economy. Recessionary fears were being factored into risk premia towards the end of 2000 as they are now.

c) The initial repricing of spreads was fairly rapid over the course of 2000, but spreads remained elevated for an extended period. There was no quick snap back in risk premia. This is relevant because unlike the cycles we saw in 2009 and 2011, which saw a rapid tightening in spreads helped by government and central bank actions, the ability for policy makers to affect the same kind of move seems less apparent today. The contemporary cupboard of policy tools is looking pretty sparse. If we are entering a cycle of market weakness, there is a decent chance that this time it could last a while as it did in the early 2000’s.

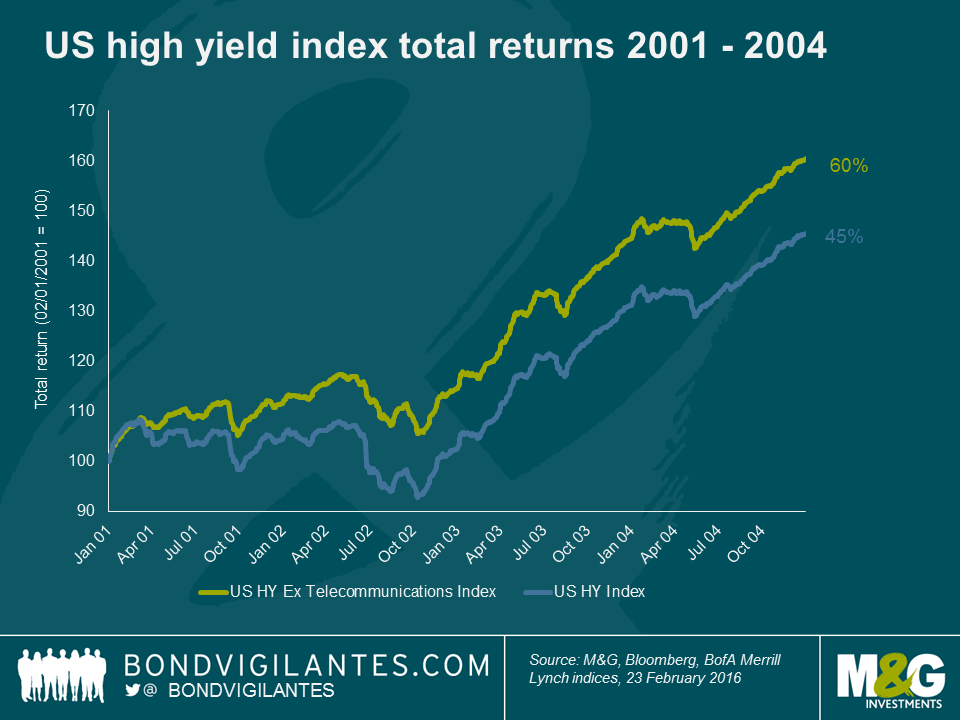

The interesting thing is that buying high yield when spreads first touched around 900bps wasn’t necessarily a bad call, even at the start of an extended default cycle. Buying into the market on Jan 1st 2001 would have meant a return over the course of 4 years, of 45% (remember – both defaults rates and spreads peaked a year later).

Also, a good sector call added significant value. If that investor bought the market without any telecommunications exposure instead, they not only saw consistently positive returns, but also a total return of c. 60% over 4 years, 15% higher than the market average.

It should be noted that the scope to achieve these sorts of returns was only possible with a significant contraction in spreads during the course of 2003 and 2004 – this generated significant capital gains on top of the high level of coupon income.

Nevertheless, being “early on the trade” when spreads first widened was not a punitive experience. The implication is that even if we do see an extended cycle play out, for the patient investor who can ride out a few bumps and scratches in the interim and get the sector call right, the total return opportunities in the high yield market are looking interesting.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.