Has the ECB reached the limits of monetary policy?

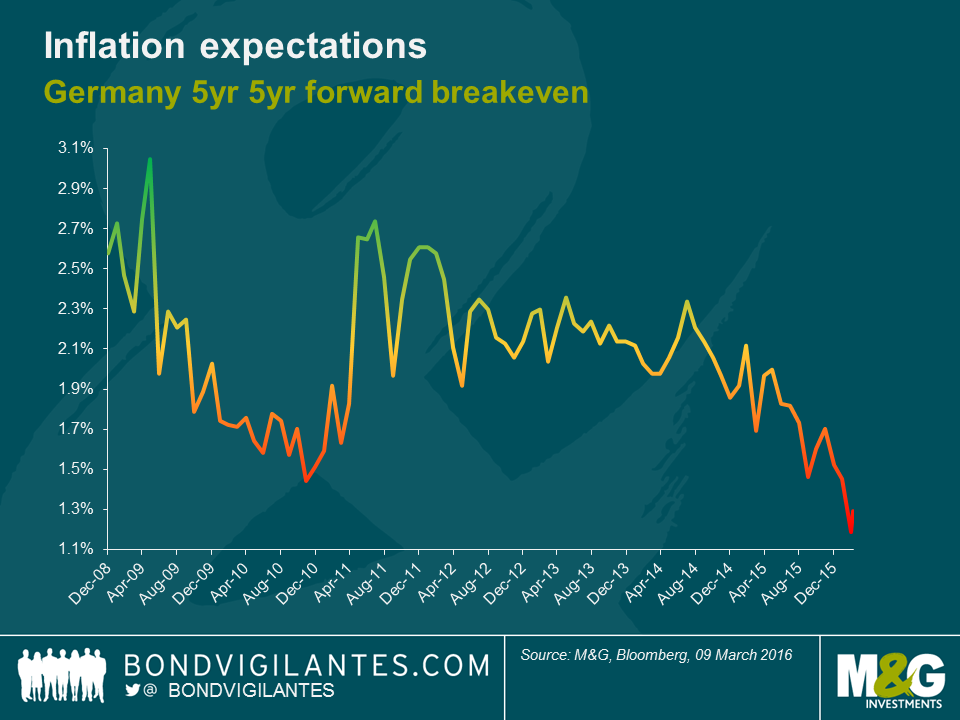

The simple answer is a no. Eric Lonergan in a guest blog has already (see here) debunked the idea that central banks are at the zero bound. And since then the market has become increasingly confident that the ECB will cut its deposit rate further into negative territory at tomorrow’s meeting. And it has reason to do so. Inflation and growth will be lower than the Bank had forecast a mere three months ago with inflation expectations also falling out of bed.

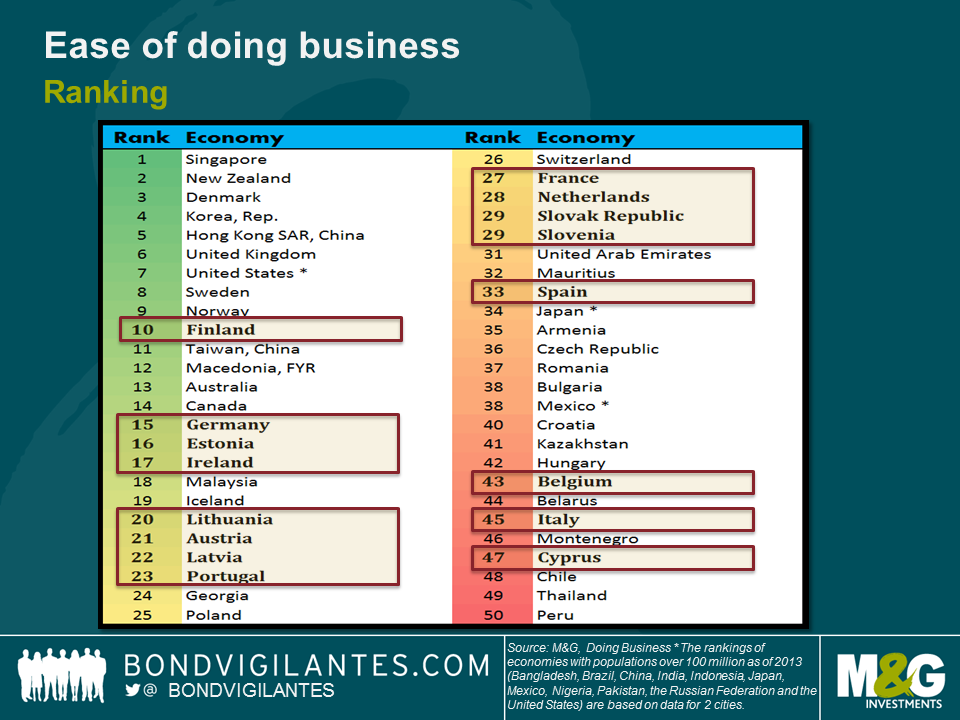

But that isn’t to say that there aren’t diminishing returns to be had from a further loosening of policy. The reality is that many of the problems holding back the Eurozone are structural in nature. And doesn’t the ECB know it. I can hardly remember a press conference when Mario Draghi hasn’t failed to mention the need to address these issues. Hardly surprising given that the Eurozone is only represented twice in World Bank’s top fifteen ‘Ease of doing business survey’. The likes of France at 27, Spain at 33, Italy at 45 and Greece at 60 makes for painful reading.

The ECB is acutely aware of the moral hazard it creates in addressing the Eurozone’s troubles purely via the monetary channel. And yet with a sole mandate to hit an inflation target of close to but below 2%, they are once again finding themselves with the unenviable task of having to do the bulk of the heavy lifting. On Thursday we will likely see a cut to the deposit rate with some sort of tiering in an attempt to address some of the challenges faced by the banking system (see Mario’s blog post), as well as an extension to the PSPP (QE programme), both in terms of size and duration. We may even see a greater willingness to buy certain corporate bonds – although this will likely be a step too far for the majority on the Governing Council.

But the reality is that increased productivity and greater innovation is much needed to drive the Eurozone. Antiquated bankruptcy regimes need to be radically reformed, red tape needs to be removed and the banking system needs to own up to further loan losses that it has yet to provision for. These changes aren’t easily achieved, not least because they require the sort of short term pain that politicians rarely have long run incentives to deliver.

Consider the case of Italy. Since the global financial crisis the Italian housing market has fallen in value by around 19% from its peak. This, combined with recessions that have left Italian GDP around 10% lower than in 2008 and rises in unemployment to around 12%, have conspired to create a large amount of c. €200Bn of non-performing loans (NPL’s) in Italy as households and companies have encountered difficulties in servicing their debt.

Unlike in other Eurozone periphery countries such as Portugal and Spain, Italy has been slow in restructuring its banks and addressing the problem with many NPLs still sitting on banks’ balance sheets. The Italian banking system is therefore considered to be weak and there have been a wave of recent high profile bank collapses that have resulted in ‘bail-ins’. With this in mind the Italian authorities have just set up a scheme to create Asset Management Companies who will then look to securitize these non-performing loans, in theory reducing a bank’s balance sheet and allowing them greater scope to lend to the broader economy. As the scheme is very much in its infancy we will have to wait to see whether it can have the desired effect.

Absent further structural change I’m convinced the Eurozone will labour under a cloak of lower potential growth and struggle to encourage investment given the need to earn an attractive rate of return on capital. Yes the ECB can likely drive risk-free rates even lower. Yes they can depreciate the €. And yes they can provide ever more liquidity to the banking system. These may all help near term. But without real reform the market will increasingly worry that we have reached the limits of monetary policy. And at some point if the market cannot be convinced otherwise, then the consequences will be significant.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox