Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

My book of the year in 2015 was The Rise of the Robots by Martin Ford. I wasn’t alone in liking it; it was the FT McKinsey Business Book of the Year, and set the debate for a year of robotisation stories in financial markets. Last week we held a Bond Vigilantes x Technology conference here at M&G, with great speeches from Diane Coyle on Digitally Disruptive GDP (are we measuring growth or inflation “properly” in today’s online world?), Dr Wolfgang Bauer on advances in battery technology, solar and fission energy, and Martin on the robots. Tesla also brought along a couple of cars for us to play with – I mean examine the battery technology in.

If you haven’t read The Rise of the Robots yet, you must. In it Martin Ford shows how AI and advances in robotics are putting at threat huge numbers of jobs in both developed and developing markets. And whereas previous advances in machinery replaced mainly manual jobs, this next phase will also cause massive disruption to higher skilled workers, threatening both jobs and wages. The knock on impact will be a huge demand deficit – who will be able to afford to buy the goods that the robots make? In the book Martin suggests that the governments may have to expand the state safety net significantly to prevent societal disaster.

You can watch my brief interview with Martin below. And if you haven’t read the book, you can win a copy by entering our competition.

To win a copy of The Rise of the Robots, answer this simple question. Name these three robots.

The answers:

Robot 1: Metal Mickey

Robot 2: Optimus Prime

Robot 3: Number 5/Johnny Five

The winners of the competition are:

Simon Bird

Ian McCaig

Trevor Smith

Steven Smith

Graeme Wearden

Congratulations. Copies of Martin’s book will be sent to you shortly.

There’s no doubt that the oil industry has seen better days. Adding to present-day woes of price levels of $30-40 per barrel are questions about the long-term viability of the industry’s business model as a whole. Take for example the Rockefeller dynasty and Saudi Arabia, two names synonymous with gigantic fortunes built on oil. Well, the Rockefeller Family Fund just announced its intent to divest from Exxon Mobil, a direct descendant of John D. Rockefeller’s Standard Oil, and from other firms related to fossil fuels, stating that it made “little sense – financially or ethically – to continue holding investments in these companies”. Saudi Arabia made public its plans to launch a US$ 2 trillion investment fund, setting the course for the country’s post-oil future. Admittedly, it’s only anecdotal evidence but maybe the writing is indeed on the wall for the oil industry.

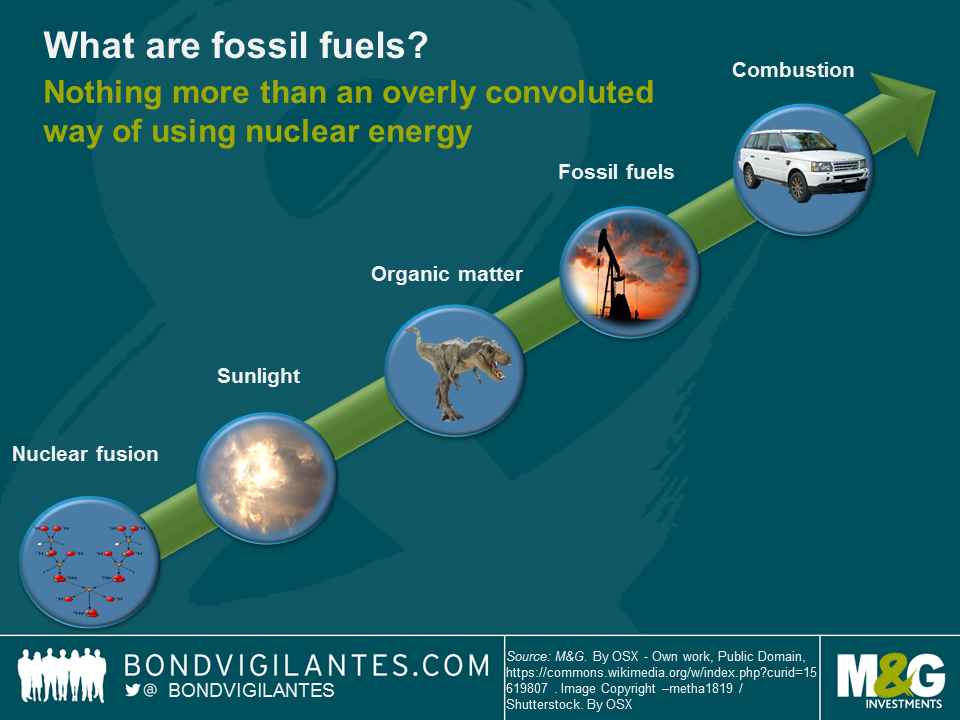

To be honest, as a chemist by training it has always puzzled me how fossil fuels have managed to acquire such a dominant position within the global energy landscape in the first place. They really aren’t such an obvious choice, when you think about it. At the core of it, burning fossil fuels is merely a long-winded and inefficient way of using nuclear energy (see chart below).

As a by-product of nuclear fusion processes in the sun, electromagnetic radiation (i.e., sunlight) is emitted. On earth, plants convert the energy contained in sunlight into chemical bonds by building up complex hydrocarbons that are metabolised (ie eaten) by animals and converted into further biomolecules. After plants and animals die, their organic matter is converted under certain circumstances over tens of millions of years into fossil fuels. In that sense, fossil fuels are renewable energy carriers, albeit running on an extremely long time-scale. We then dig up these fossil fuels, process them and eventually burn them in order to convert the energy stored in their chemical bonds into mechanical energy or heat. The whole process is hopelessly inefficient as energy is “lost” (not actually lost but partially transformed into rather useless energy forms, such as waste heat) at every single energy conversion step. The last step is particularly horrific as combustion engines have efficiencies well below 50%. And that’s not a problem that could be “engineered away” but a necessary consequence resulting directly from the laws of thermodynamics. Let’s stop there…

Oil has further severe disadvantages, for instance:

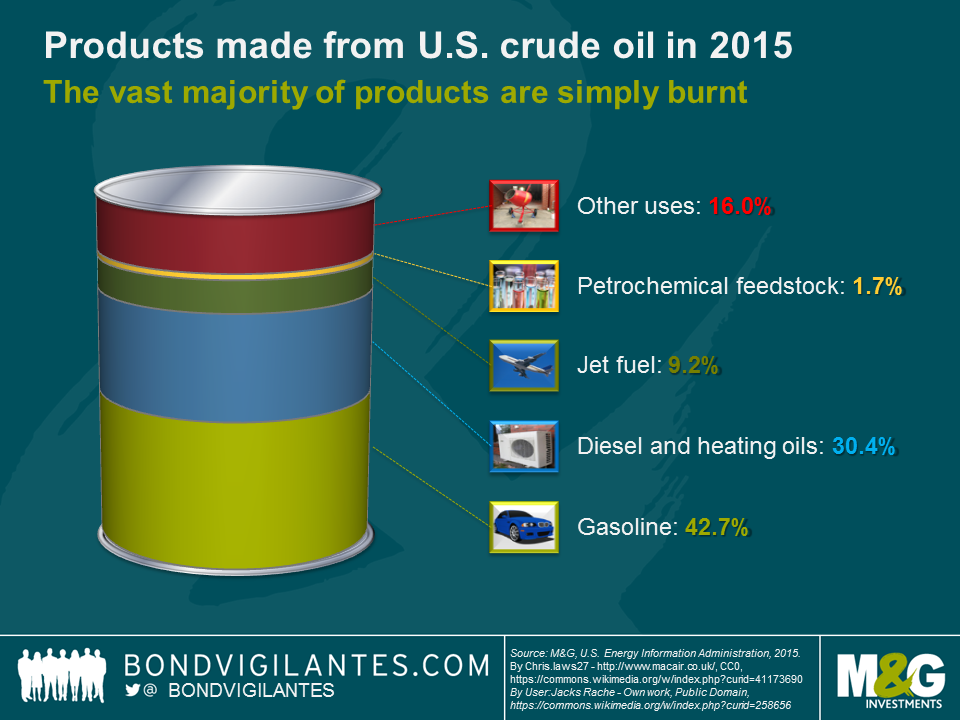

And there are opportunity costs to be considered. If we are willing to accept all the disadvantages of oil, shouldn’t we then at least try to make the best of it? Using the complex mixture of organic molecules as precursors in sophisticated polymer synthesis would be sensible from a chemist’s point of view. However, petrochemical feedstock only accounts for a small fraction (c. 2%) of products made from a barrel of U.S. crude oil (see chart below). More than 80% of the products (gasoline, diesel, heating oil and jet fuel) are simply burnt in combustion engines or furnaces, which, quite frankly, is pretty wasteful and savage.

But why are fossil fuels, and oil in particular, still so prevalent? Why are the vast majority of cars still propelled by internal combustion engines and not by electric engines? The key is energy storage, the one area where fossil fuels excel. This has profound practical implications, particularly for applications in transportation. Vehicles using oil-based fuels are relatively light. For any given range they need to carry around only a relatively small quantity of fuel. That’s the main bottleneck of “Electro Mobility” at the moment. One kilogram of electric batteries can only store a small fraction of the energy that is contained in one kilogram of gasoline, diesel or jet fuel. As long as batteries cannot be recharged while driving (still a long way off), users of electric vehicles either have to accept a smaller range or they have to carry lots of batteries, which increases weight and thus reduces efficiency.

Significant resources are currently committed to electric battery research to drive technological progress. As a consequence, batteries are catching up fast with fossil fuels (see Jim’s blog). Simultaneously, renewables, solar energy in particular, are becoming more and more cost-efficient. As soon as the energy storage gap is sufficiently small, we will reach a tipping point as there will no longer be any good reason to rely on fossil fuels. As with other large-scale technology disruptions in the past, the consequences will be significant (see chart below).

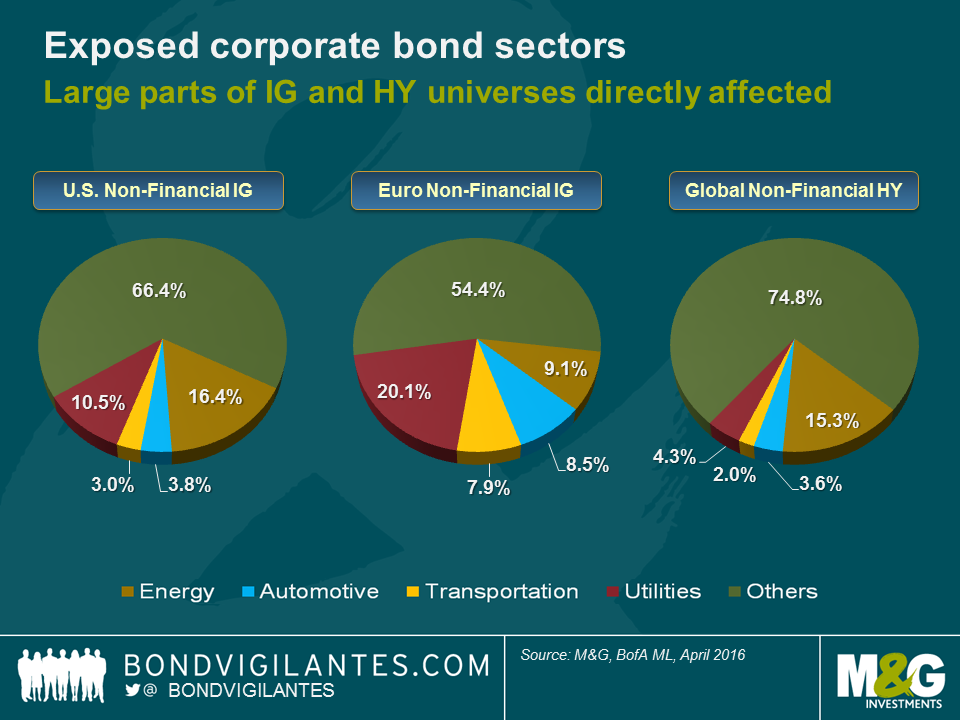

In the non-financial corporate bond space, the sectors most directly affected by the end of the fossil fuel age (energy, automotive, transportation and utilities) account for roughly a third of the U.S. investment grade (IG), nearly half of the European IG and around a quarter of the global high yield universes. There will also be ripple effects on other corporate sectors (e.g., chemicals), as well as on government bonds of petroleum exporting countries. Since energy costs are a meaningful part of price indices, there will be an impact on inflation break-even rates. And the list goes on. These developments won’t occur overnight, of course. But it is our job as long-term bond investors to think long and hard about this topic now and the opportunities and threats that go along with it.

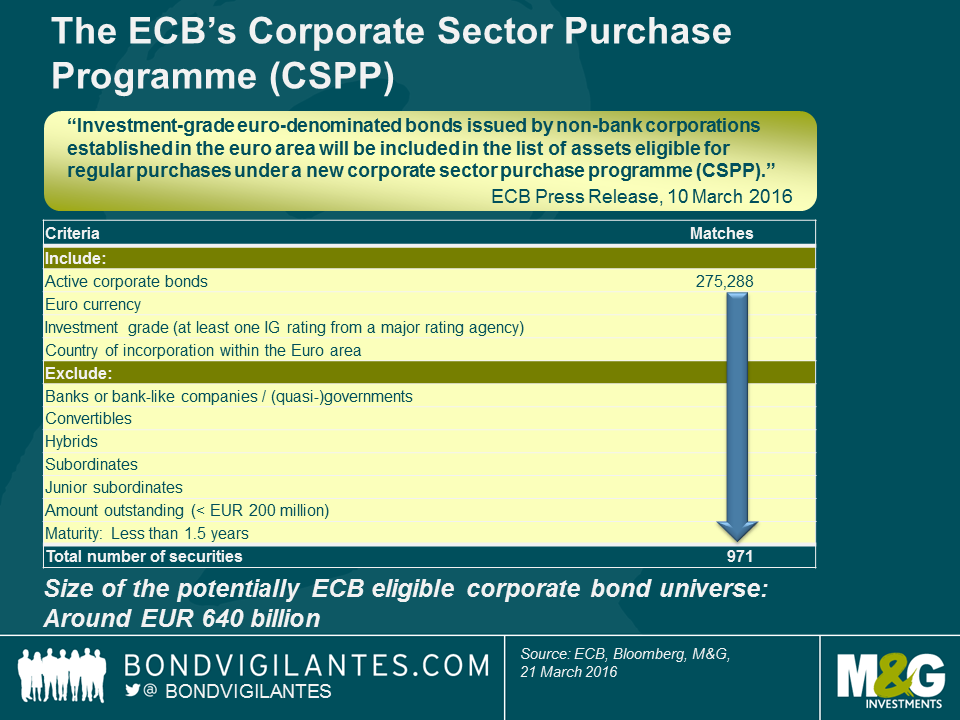

Bond markets have reacted strongly to the 10th March announcement by the European Central Bank (ECB) of its new corporate sector purchase programme (CSPP). Credit spreads of euro-denominated investment grade (IG) corporate bonds have tightened by around 20 bps on average. Still, a lot of the CSPP’s particulars are anybody’s guess at this point. The publication of the account of the last monetary policy meeting yesterday hasn’t added much clarity. So far we only know that from the end of Q2 2016, the ECB will start buying IG EUR corporate bonds issued by non-bank corporations established in the euro area. The ECB has also stated that bonds eligible under the Eurosystem collateral framework would be a “starting point” for the eligible universe under the CSPP but that further rules and restrictions might apply.

There is a lot of uncertainty around the details, though. How much will they buy each month? Will the ECB be active both in the primary and the secondary market? Will there be any capital key allocation mechanism, like in the case of their sovereign bond purchase programme? What will be the maximum percentage of each eligible corporate bond issue that can be held by the ECB? Will the ECB become a forced seller if a bond held on its book is downgraded to sub-IG territory? All of these questions – and many more – are yet to be answered.

Applying a series of filter criteria, we have screened the corporate bond universe for potentially ECB eligible securities (see table below). Our analysis suggests there could be 971 bonds on the ECB’s radar, totalling around EUR 640 billion.

Some of our filter settings are pretty common-sense (e.g., euro-denomination, exclusion of banks, hybrids and (junior) subordinated instruments), others are entirely up for debate:

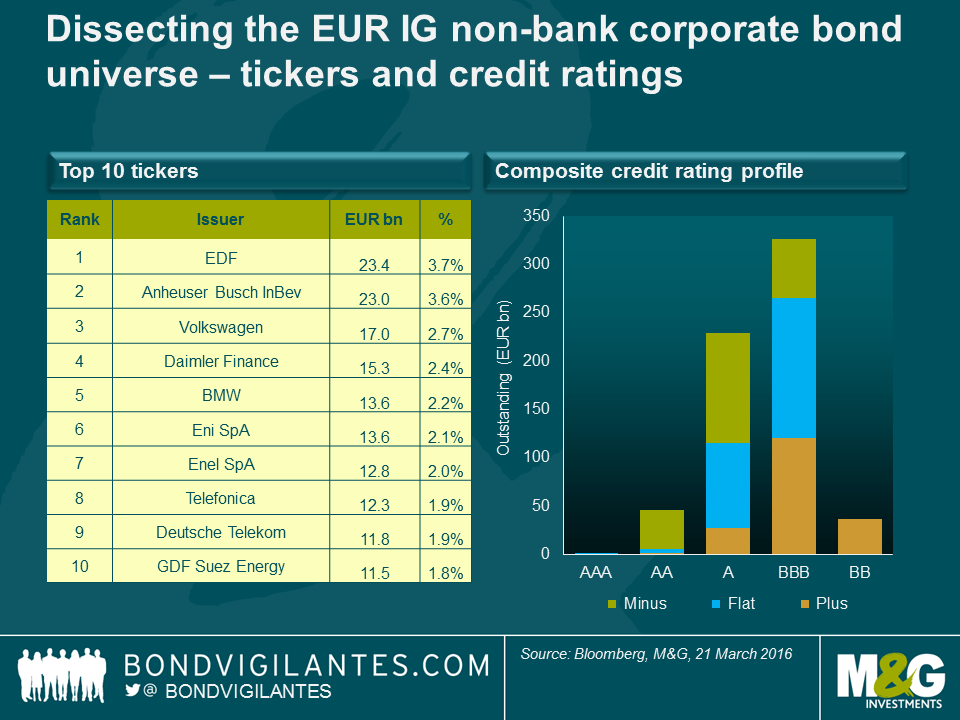

Keeping these major caveats in mind, we dissected our “best guess” ECB eligible bond universe (see chart below). The biggest beneficiaries, with particularly large amounts of potentially eligible bonds outstanding are EDF and Anheuser-Busch InBev, accounting for 3.7% and 3.6%, respectively, of the eligible universe. In terms of composite credit ratings, more than half of the universe consists of BBBs (51.1%), followed by single As (35.8%).

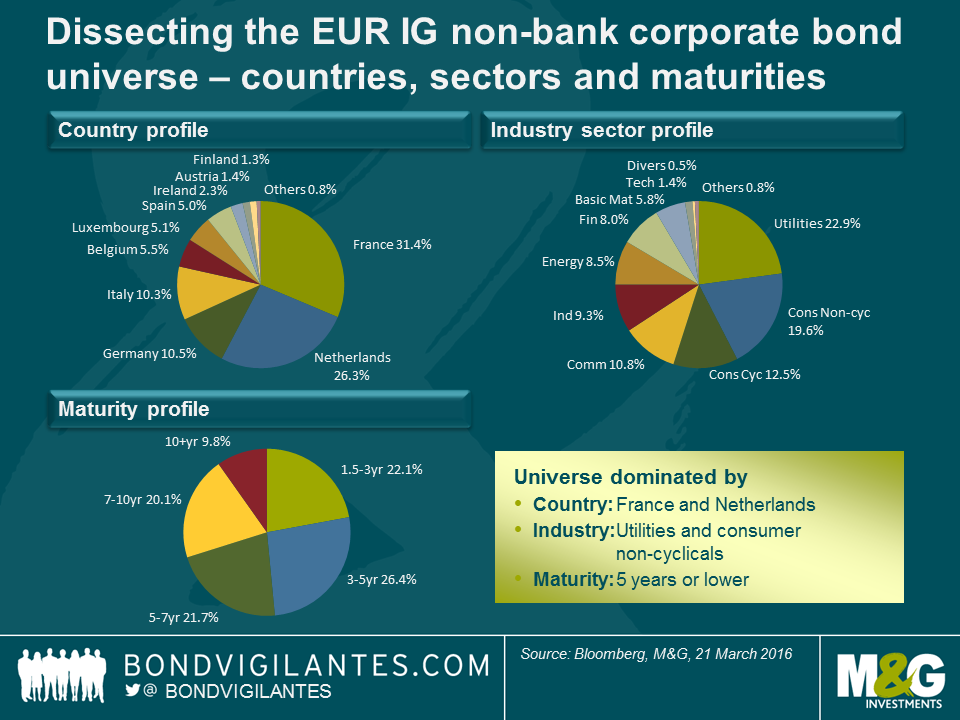

In terms of countries, French companies would be the biggest beneficiary (31.4%), as we had already predicted in 2014 (see Anjulie’s blog). The Netherlands (26.3%), benefitting from a large number of holding companies being domiciled there, and Germany (10.5%) follow in second and third place. Utilities (22.9%) are likely to be the dominant industry sector, ahead of consumer non-cyclicals (19.6%) and consumer cyclicals (12.5%). The EUR-denominated IG corporate bond space in general is relatively short in terms of duration compared to the USD IG space. Therefore, it is not surprising that c. half of our potentially eligible universe (48.5%) mature within 5 years.

So with a new buyer soon to be in the market, does this mean we should be hoovering up all the EUR credit we can get our hands on? Not necessarily. Whilst EUR credit does look good value relative to governments, spreads of EUR denominated corporate bonds, both investment and speculative grade, have been tightening since mid-February. The rally noticeably accelerated due to market euphoria around the ECB’s announcement. At this point a large portion of the expected benefits could be priced in. Valuations are arguably already stretched for certain issuers, when comparing underlying credit risk fundamentals and current spread levels.

Based on our bond screening, and assuming that the ECB can buy one third of every eligible corporate bond issue, the size of the accessible universe is “only” around EUR 210 billion. But total asset purchases will be EUR 80 billion per month, i.e., EUR 960 billion per year. When comparing these numbers, we believe that corporate bond purchases will likely be an incremental supplement to public securities purchases, perhaps to the tune of around EUR 5 billion per month. So it is entirely possible that the actual corporate bond quota, once it is communicated, could disappoint overly bullish market expectations.

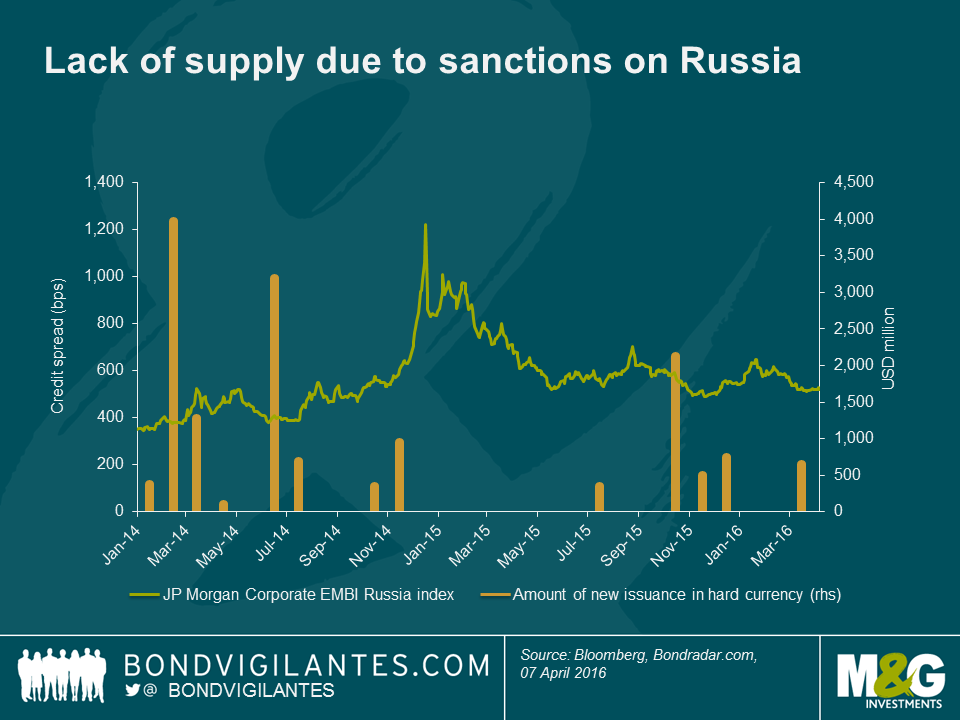

Russian corporate bonds were one of the best performing asset classes last year, with a total return for the JPM CEMBI Russia index of +26%, despite Russia’s GDP dropping by -3.7% on the back of a hugely challenging economic backdrop and geopolitical headwinds. I recently spent a week in the cold of Moscow’s early spring, meeting banks and corporates to help me assess whether the economic sanctions and low oil prices would continue to, paradoxically, benefit bond investors in 2016. Here are some of the key takeaways.

The crisis is nothing like 1998 but the economy is struggling

Importantly, sanctions have had little impact in the short term compared to lower oil prices and the resulting depreciation of the Ruble, which has made imports more expensive, resulted in squeezed margins of businesses and lower living standards for millions of Russians. The locals I talked to said the current environment is nothing like the 1998 crisis though, when the country had no reserves and a large budget deficit. But most also recognise that the current crisis is more pernicious (as a slow, prolonged deterioration) and question where a rebound could come from in the near term should oil prices stay low and the sanctions remain in place.

At the micro level, talking to various local banks is always a good start to understand the real economy. Almost all the (public and private) financial institutions I met were concerned about asset quality deterioration, in particular for corporate loan books, with an expected rise in non-performing loans. Sectors such as construction, metals & mining, automotive, commercial real estate or transport have been hit hard. It’s not much better in retail lending and appetite for risk is small. The bright spots come from (i) exporters, which have been helped by the weaker Ruble as their costs are in local currency and their revenues are in US dollars, and (ii) the food agriculture business, which benefits from the Russian counter-sanctions on European food exports to the country.

Russian corporates are resilient and refinancing risk is low in the short term

My meetings with various non-financial bond issuers (oil & gas, metals & mining, telecom and transport) confirmed the above trend but gave me a different perspective. Management acknowledge the headwinds and most of them seem to be taking the necessary steps to optimise their business for this new environment. Military history is replete with examples of how incredibly resilient the Russian people are, and the corporates I met gave me the same impression.

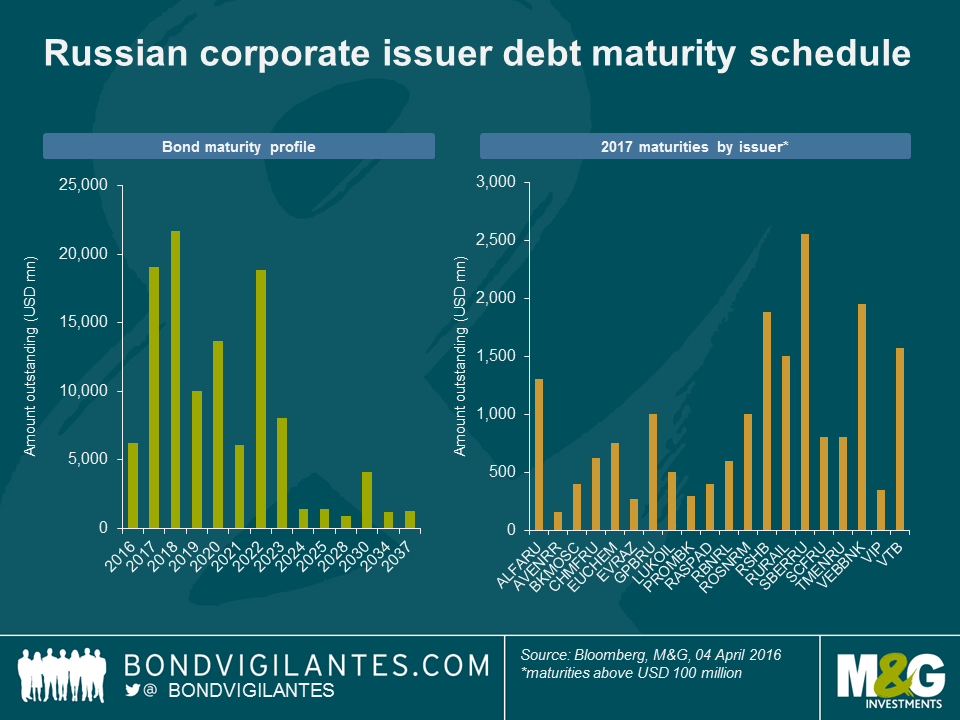

With a primary market virtually closed for the past 18 months, the sanctions have pushed Russian corporate bond issuers to financial discipline by maintaining relatively low leverage and adequate cash levels in order to meet hard-currency debt maturities. The availability of the Ruble in the country’s financial system is another contributing factor explaining how well bond issuers have been able to weather the financing sanctions by the West. In the near term, and as can be seen in the above graph, the debt maturity schedule of Russian corporate issuers (including financials) looks manageable with the largest maturities due in 2017 being mainly bonds issued by state-owned banks.

Sanctions create scarcity value but valuations are very different from early 2015

From a bond supply perspective, the sanctions have been very supportive of bond returns in 2015 and continue to help the technical backdrop in 2016. While some issuers were able to issue bonds late last year and in 2016, the local market (RUB-denominated bank loans) is expanding and hard-currency bond issuance is expected to remain low this year. In terms of demand, I would expect the picture to be very different from early 2015, when spreads reached very attractive levels (around +1,000bps) on the back of external threats (geopolitical tensions, oil price, RUB) rather than imminent risk of defaults among Russian corporates. At about +520 bps, the Russian USD-denominated corporate bond market has now come back closer to fair value levels of spreads and total returns were 5.1% in the first quarter, which was justified in my view given the fundamental resilience of Russian issuers and relatively improved geopolitics. Looking forward and playing devil’s advocate, it’s questionable how sustainable this resilience can be in a prolonged period of crisis.

Credit differentiation will be critical in a period of low oil prices and sanctions

Assuming low oil prices and sanctions remain in place, corporate fundamentals should deteriorate more significantly throughout this year and in 2017. One of the main fundamental risks to corporate cash flows in the near future is Russia’s widening budget deficit.

First, low oil and gas prices have resulted in lower government revenues. And because oil & gas companies have actually been very resilient through the crisis due to their export-driven nature, the government is contemplating raising taxes on the sector.

Second, the sanctions have prevented Russia from tapping the bond market as much as needed to fill the budget gap. Hence, the government is considering increasing the dividend pay-out ratio of state companies to 50% from 25%. For oil & gas state companies, this could be another drag on cash flows. Indirectly, the private sector and in particular steel companies could also be affected if the stretch on corporate cash flows results in reduced public investment and lower underlying demand.

In light of this potential deterioration, corporates would have to draw on their cash balances and the refinancing of the >$20 billion of hard-currency corporate bonds maturing in 2018 could become more problematic for some issuers.

The bottom line is that credit differentiation will be critical. Unlike the 2015 macro call that took place in Russia, investors should be pickier in terms of bond selection as the long-term impacts are likely to result in credit profile divergence across the Russian corporate bond universe.

Finally, one may nevertheless not rule out another macro call this year if oil prices rebound materially (upside) or, bearing in mind that Russian politics have almost always caught investors by surprise, if geopolitical tensions with Ukraine revive (downside).

The world has seen negative interest rates before – Switzerland set interest rates below zero for foreigners in the 1970s in order to slow flows into the Franc. But today’s negative rate environment is far more widespread, with Switzerland, Denmark, Sweden, Japan, and the Eurozone all setting negative policy rates. Lots has been written about the intended transmission mechanisms of negative rates – cheaper direct borrowing costs for households and businesses leading to stronger economic activity, a portfolio rebalance effect in which investors sell low/negative yielding assets to buy riskier instruments, thus reducing funding costs for companies, and, controversially, reducing the attractiveness of an economy’s currency in a world in which competitive devaluation is seen as desirable. This blog however hopes to capture some of the other consequences of negative rates, some unintended, and some creating different problems for policymakers.

I’ve started this list with 10 observations, but I plan to update it periodically as we see how the Negative Rate World (NRW) develops over the months or years ahead. I’d like to ask for your help in spotting any interesting behavioural changes and historically important news stories. You can put them in the comments below, or send us links through Twitter (@bondvigilantes) or email. Sourced facts are the best facts, but I will also consider anecdata. Some links below may require subscriptions, most don’t.

What have we missed?

A few things that I’ve found interesting over the past week or so:

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.