Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

It has been a while since we last uploaded a video from one of our U.S. research trips. Richard and I recently travelled to New York to meet with various local analysts and strategists. The timing of the trip could not have been better: the Federal Reserve needs to decide whether and how to continue its rate hiking cycle and event risk in the economy is high. We had the opportunity to discuss a wide range of topics from current state of the U.S. labour market to the looming US presidential elections to corporate bond valuations. We’ve put together two short videos to share some of our thoughts on these various topics.

In the first part of the video which we post today, I review some of the key risks and opportunities within US investment grade healthcare space. Despite favourable long-term prospects for the sector, corporate bond investors continue to face certain risks. Richard will subsequently address the state of the U.S. economy in the second part of our video.

The UK has voted to “Leave” the EU. We’re seeing some significant moves in fixed income assets first thing this morning as financial markets had very much discounted a “Remain” outcome, in line with the last opinion polls and in particular the betting markets which had heavily backed that outcome. The biggest market movements though have occurred in the FX markets where the pound fell from nearly 1.50 to 1.36 versus the dollar, lows not seen since 1985. The US dollar index has rallied by nearly 3%, and the big winner in this “risk off” scenario has been the Japanese yen, itself now up 3.6% against the US dollar. The Euro is performing badly as both the economic and political implications of the “Out” vote are digested – will European growth be hit, will other EU nations hold their own referendums, what will become of the periphery and the banking sector? The Euro is down by over 3% against the dollar. In a risk off morning, the other big losing currencies are those in emerging markets. The Mexican peso for example is 6% weaker.

Within bond markets themselves, the US 10 year Treasury has rallied by 25 bps (more than two points) overnight, and the 10 year bund has moved sharply back below zero – now trading at a new record low of -15 bps. This follows Thursday’s sell-off in government bonds in anticipation of “Remain”. Gilt markets will also rally when they open at 8am, and all eyes are on the Bank of England which has committed to keep the banking sector awash with liquidity. I wouldn’t rule out a rate cut from the BoE later this morning, perhaps to 0% from 0.5% (although this would likely trigger a further sell off in sterling). A likely ratings downgrade for the UK has been flagged in advance in the event of a “leave” vote – markets have generally not punished downgrades on highly rated sovereigns (for example the US when it lost its AAA rating). There is no significant default risk for a nation which can print its own currency.

The “losers” in bond markets are the riskier fixed income assets. As further EU breakup fears grow, Italian and other peripheral government bonds are underperforming. Italian and Spanish 10 year bond yields have risen by 30 bps so far this morning. Peripheral financial bonds are perhaps 60 bps wider in spreads at the senior level and up to 130 bps wider at the subordinated level. Banks in general, even in “core” nations, are also performing poorly relative to traditional corporate bonds. Senior bank debt is 50 bps wider, and subs are 100 bps wider. Corporate bonds are anything from 20 bps to 80 bps wider. There has been talk of institutional buying at these lower levels, although we are sceptical that there has been much trading so far today. Emerging market bonds are all much lower. Turkey’s US$ debt is off 2 points, South Africa 3 points and Hungary 6 points. The high yield market was extremely weak initially, with the Crossover index at one point 120 bps wider. It’s retraced some losses and is “just” 80 bps wider now.

Fundamentally the sell-off in risk assets presents some opportunities for long term investors. Credit markets were already discounting a much higher level of defaults than we believed likely, and today’s moves increase the over-compensation for default risk. However, with liquidity likely to be low today (and potentially for some days to come as the implications of yesterday’s vote become clearer) the chance to pick up bargains might be limited.

What about the economy? Well 90% of economists expected a “leave” vote to be negative for UK growth. Some say that even the uncertainty leading up to the vote took up to 50 bps off GDP growth. Certainly investment intentions are likely to be delayed by businesses, and households may become more cautious. A recession can’t be discounted. With the global growth outlook also now likely weaker we expect the US Federal Reserve to be on hold. No rate hikes for the foreseeable future. UK inflation is a different matter. A fall of this magnitude in the pound will lead to higher import prices. After years of inflation being below target, it should move higher than 2%. However in the interests of growth and financial stability this is unlikely to provoke a response from the Bank of England: as mentioned earlier a rate cut is more likely in the first instance.

Finally I am cross that there was nowhere open to buy caffeine on Cannon St at 6am this morning.

This year is the 10th anniversary of the Bond Vigilantes blog. When we started it back in 2006, rates in the UK had just risen to 4.75%, the US housing market had seen price rises of between 5% and 12% for more than 6 years in a row, and Twitter was a just few months old. Nottingham Forest finished 4th in the Championship, and the Scissor Sisters were number one in the charts with “I Don’t feel Like Dancin’”. As part of what will be a lengthy birthday celebration, potentially stretching into 2017, Bond Vigilantes is delighted to be Festival Partner at the FT’s Festival of Finance.

We’ve been attending this brilliant event for the past couple of years (when it was called Camp Alphaville), and therefore can wholeheartedly recommend that you come along too. Set in the grounds of the HAC in the City, it’s your chance to watch and take part in scores of discussions on topics such as the end of free internet, tax inversion, football finance, the cashless society, and capital controls. Guest speakers include Peter Praet (ECB), Andy Haldane (BoE) and our very own Richard Woolnough.

A few of the M&G bond team will be there, so come to the coffee stand for a chat. All proceeds from coffee sales over the day will go to Alzheimer’s Research UK.

If you haven’t got a ticket yet, then Bond Vigilantes have a special discount code for you. Follow this link and enter the code BV10TH to receive 20% off your ticket price. This competition is closed.

We also have one ticket to give away to a lucky winner. This golden ticket will go to whoever guesses (predicts?) correctly the 10 year bund yield at midday, UK time, on Friday 24th June (the day after the Brexit vote). I’ll use the Bloomberg generic bund yield GDBR10 rounded to 2 decimal places (i.e. currently 0.06%). Email your prediction here. Good luck.

18+. UK residents only. No employees. Exclusions apply. Closes 24/6/16. One prize available. This competition is closed

The results are in

The 10 year bund yield at midday, UK time, on Friday 24th June was -0.11%. The nearest estimate was from Thomas Sanders, who predicted -0.09%. Congratulations to Thomas – your prize of a ticket to the FT Festival of Finance is on its way out to you.

The year is 2020 and King Henry IX, the recently installed head of state of the United Kingdom of Northern England, Wales and Northern Ireland stands in a room overlooking the Trent River. Most of his subjects still refer to him simply as “Harry”. His popularity with the electorate is seen as a key factor behind the surprise victory for the monarchists in the recent constitutional referendum for the latest sovereign entity to be carved out of the United Kingdom. Following the secession first of Scotland in 2018 and then the South of England a year later, after the so called “SEXIT” referendum, King Henry is now the constitutional monarch of a territory encompassing the North of England, Northern Ireland and Wales. As he looks out of the window, the Prime Minister continues with his weekly briefing,

“So you see your majesty, I’m afraid that the Governor really has no choice, a further cut to interest rates and allowing a devaluation of the Northern Pound is the only option in light of our fiscal position.”

The King nods to acknowledge the statement, albeit with little real understanding of what Prime Minister Andy Burnham has just said.

“This will probably mean more inflationary pressure in the short term, but a weaker currency will help our exporters compete more effectively. Nevertheless, your majesty, I feel I must bring up the fiscal pressures your government is feeling.” The Prime Minister pauses.

Harry turns around, picking up on the embarrassed tone in the Prime Minister’s voice. “Let me guess,” he says, “more cuts to the Royal Budget?”

“I’m very sorry your majesty, but we’ll have to start making more economies. I’m afraid it’ll mean further delays to the construction of the new palace here in Stoke “

Harry turns back to look over the River Trent. On the far bank, the new Houses of Parliament were taking shape in the centre of Stoke, but the future site of his palace remained untouched nearby. It is still being used as a car park for the local Lidl supermarket. How did I end up here, he ruminates, in Stoke of all places. After all the debate about where the new capital was to be located, the politicians were deadlocked between Birmingham and Manchester. Consequently the “M6 Compromise” started to take shape, with an expanded Stoke-on-Trent as the nation’s new purpose-built capital, midway between the two.

“Also, we’ll need to cut back on the regular trips to Los Angeles.” Prime Minister Burnham continues, “The flights will just get more expensive if the Northern Pound continues to slide against the dollar. I understand this may not go down well with Her Majesty, but I can only apologise for this, my hands are tied.”

Harry visibly winced. He would have to break the bad news to Queen Kendall (nee Jenner), who liked to jet back regularly to visit her family in Beverly Hills and appear in episodes of their long running reality series. Perhaps they could film more episodes here at home, he thought, after all their son, Prince Kanye, was due to start school soon.

The above snap-shot of a balkanised United Kingdom in the near future may seem far-fetched, but with the contemporary political debate about the UK’s membership of the European Union and the continued stresses and strains within the Eurozone itself, I thought it might be interesting to consider if there were potential economic fault lines within the UK too.

The currency union that underpins the UK is able to function given the regular and persistent fiscal transfers from the South East of England and London to other areas within the country. These transfers help redress the inevitable internal economic imbalances of a currency area and are part of a well-established political settlement. However, what if this political settlement was ripped up by a disgruntled electorate in a fit of economic localism, and with it the mechanism for fiscal transfer? In this instance, what would be the optimal currency areas for a de-constructed UK?

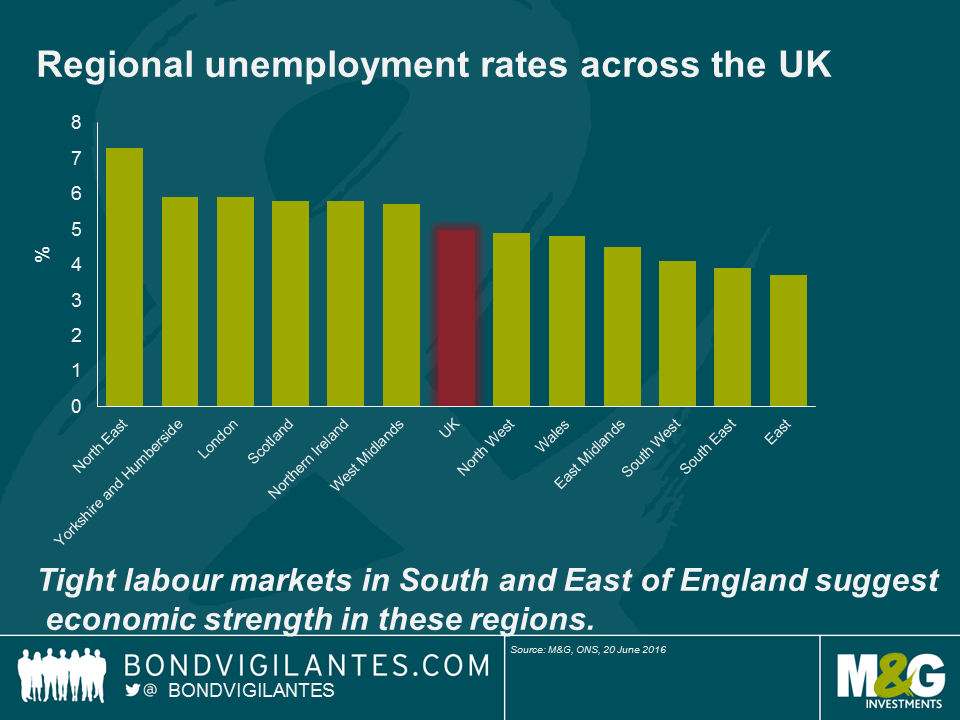

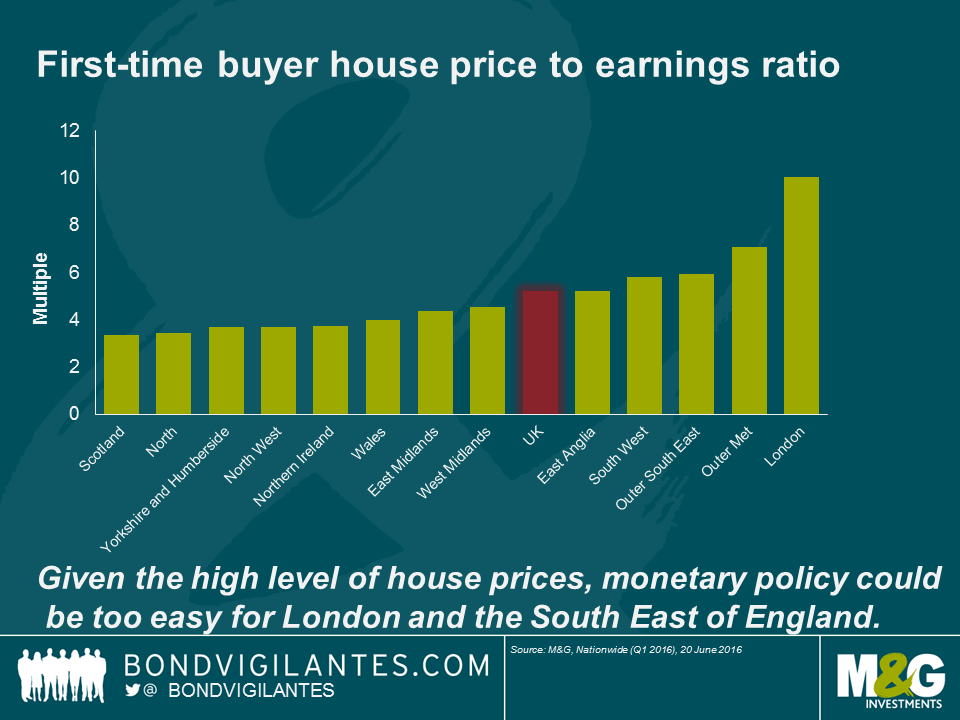

To answer this, I looked at two readily available regional statistics: unemployment rates and house price to earnings ratios. This first is to determine regional differences in the labour market and the latter to determine where low interest rates are having the biggest impact on asset price inflation. The logic is that areas that currently have low unemployment and a high house price to income ratio would arguably benefit from a tighter monetary stance, and vice versa for areas that have significantly higher unemployment and a much lower house price to income ratio.

In terms of unemployment rates, the first thing to note is that with the exception of the North East and the East of England, there is relatively little unemployment rate disparity which may suggest a lack of regional fault-lines. Indeed, it came as a surprise to me that London has a higher unemployment rate at 5.9% than the national average. Nevertheless, when we look at the three regions with the tightest labour markets (arguably well below an estimated UK NAIRU rate of c.5.0-5.5%* suggesting monetary policy is currently too loose) there is a definite geographical bias towards the South and the East of England.

This regional picture is also evident when we look at the break down of house price to earnings ratios. The South and East of England all have a higher than average ratio, but of course London is the most distorted of all at roughly twice the national average.

Taken together, this suggests that the UK could be broken into two optimal currency areas in the event that fiscal transfers became impossible. The South West, South East, London and the East of England forming one area and Northern Ireland, Scotland, Wales, the North of England and the Midlands forming the other area (roughly speaking a line from Gloucester in the West to Kings Lynn in the East would mark the border).

However, what is encouraging from the above, is that with the notable exceptions of the South East and London housing market and high unemployment in the North East, the lack of huge regional disparity elsewhere suggests the UK is not obviously a sub-optimal currency area as it stands today. There are regional differentials, but it doesn’t seem those differentials are sufficiently large to merit a monetary split.

Over the last few days and weeks, as the odds of a vote to leave in the referendum have moved from a remote possibility to somewhat less so, market participants have spent more and more time wondering about how they are positioned going into the vote, relative to their benchmark, their peer group, or their risk budget. The significant moves that we have seen in recent trading sessions show pretty clearly that many were not content with their positions or risks going into the vote, as evidenced by a pretty clear period of volatility and risk aversion with selling of credit risk and a rally in government bonds.

Only a couple of weeks ago, the credit markets were frantically fighting to get hold of reasonable quantities of the significant amount of new issuance we were seeing from investment grade companies. A few weeks later, issuance has ceased and sellers of these much sought after bonds seem to be outnumbering buyers, given the back-up in credit spreads seen in recent sessions. The simple conclusion is that as the odds of Brexit rise, investors feel the need to reduce risk and are selling corporate bonds.

Playing devil’s advocate, let’s imagine that a portfolio manager has sold credit risk and raised cash ahead of next week’s vote. The portfolio manager is now feeling very satisfied at this moment in time as risk aversion has increased, resulting in a widening of credit spreads. However, the vote outcome is binary: either Britain votes to leave, or to remain. If the vote is to remain, then we can reasonably expect a significant retracement of the spread widening we have seen since fears of a leave vote rose.

If this proves correct then our imaginary portfolio manager is under-invested in credit and the credit risk that he or she sold will now need to be bought back, potentially at more expensive levels. Even if spreads did not rally in the event of a leave vote, then to replace the bonds that were sold, the portfolio manager will have to pay the prevailing bid-offer spread.

In other words, those selling credit risk now are predicting a vote to leave. This decision will benefit a bond portfolio as spreads rise, or as the leave probability increases, or if the leave vote were to occur (at least for a period of time, however long or short). But it does not work in the event of a vote to remain, and incurs costs on the bond portfolio.

Now let’s think about what to do with our duration positioning going into the vote. This, in my opinion, is an even harder call to make than with credit. Which way will gilt yields move in the event of a leave vote? On the one hand, the period of economic uncertainty that would result could see growth and inflation fall, which would argue clearly in favour of further falls in government bond yields. On the other, international investors currently own more than a third of the gilt market. What if these investors decide they no longer want to own sterling, or to own the same amount of sterling? Whilst my hunch is that the knee-jerk immediate response to Brexit would be for sterling to weaken and for gilt yields to rally further, how long would these moves last? Could we end the day with higher gilt yields and no change in the pound? Either way, the direction of travel of gilt yields is highly uncertain to me, which makes hedging or positioning duration for the referendum a very tricky call.

In my opinion, owning short dated breakevens is the most prudent way to go into the vote from the perspective of duration positioning. Firstly, if you believe that the currency is likely to weaken then you should own exposure to inflation linked bonds that will, especially at the front end, see higher inflation expectations from import inflation. This will support index linked valuations relative to nominal bonds. In other words, front end breakevens are likely to rise if sterling weakens. Secondly, putting the currency to one side for a moment, if yields rise (either on a leave vote as foreign sellers of gilts emerge or on a remain as risk appetite recovers and rate hikes are brought forward), then one would typically expect breakevens to rise. In this scenario, index linked bonds also outperform nominal bonds.

If yields fall on the other hand, a scenario most likely to happen in the event of a vote to leave due to risk aversion, then whilst typically breakevens fall, and so index linked bonds are underperforming nominal ones, at least owning breakevens means having a pretty decent link to nominal yields. It is difficult to create a scenario in which nominal yields rally strongly following a leave vote and index linked bonds fall in price (this scenario would be one in which inflation fears aggressively collapse, so it is not impossible, but it is unlikely).

So I believe that given the binary nature of the result, in which we are either in or out (what odds on 50:50, and what happens then?), the best way to be positioned in terms of duration ahead of the vote, outcome and aftermath is to own short-dated inflation linked bonds. It is not binary, as whilst owning breakevens means you are positioned for higher inflation, if breakevens fall following the vote and nominal yields fall, you are still linked to nominal yields and are likely to see the price of your bonds rise.

If the currency weakens after the election result, then import price inflation will lead to rising inflation expectations. And if the currency doesn’t weaken following the result, it has still been on a downward trajectory since last November which is yet to feed through into RPI, and the ugly current account deficit suggests on a medium term, fundamental basis, that there is more weakness ahead for sterling.

Finally, there are a number of reasons to choose front end index linked bonds. Firstly, front end breakevens are the cheapest on the curve. Secondly, the front end of the index linked curve is most likely to reflect inflation surprises and outcomes (such as oil base effects, sterling weakness, wage growth in the bonds’ prices); and lastly, because with gilt yields at all-time lows, it is prudent to keep interest rate risk at a relatively low level at this juncture.

I attended a conference last week where European Central Bank (ECB) bashing was approaching fever pitch. The crux of the argument goes a little something like this:

“The ECB have lost the plot. Monetary policy has become impotent. The ECB is at the lower bound and the law of diminishing returns results only in an ever greater misallocation of resources, punishing savers and rewarding speculation, whilst losing credibility with markets and the wider public. Furthermore the ECB’s willingness to placate markets only serves to relieve pressure on much needed structural reforms.”

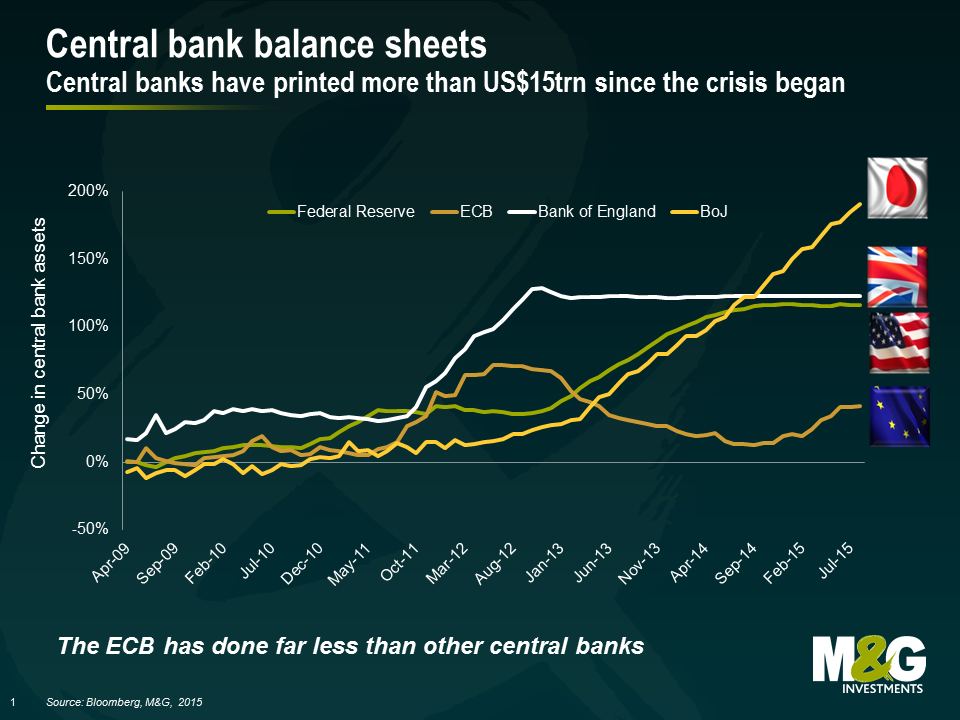

In my opinion, there could be some truth to the diminishing returns argument. It appears that each subsequent Federal Open Market Committee (FOMC) quantitative easing programme had a lesser impact than the previous on long bond yields, a key barometer of QE programmes. But the market has had to concede that the lower bound for monetary policy is not zero – 2 year yields in Germany, France, Italy, Spain, Sweden, Netherlands, Switzerland and Japan all sit well below. And the ECB has shown it has further room to expand its balance sheet by further scaling up its non-conventional measures. Let’s not forget that the ECB has still done considerably less than US Federal Reserve, the Bank of Japan, and the Bank of England. This might help explain why the Eurozone recovery has lagged that of the other major economies.

I believe the ECB should have done more monetary stimulus in order to support the Eurozone economy and done it sooner in order to meet its sole objective of achieving price stability. The ECB hoped that economically uncompetitive States within the Eurozone would pursue difficult structural reforms in order to become more competitive in the international marketplace. This hope has been misplaced. Whilst the heavily indebted nations of the Eurozone had taken some action, it is now clear that high unemployment rates, growing public and private sector indebtedness, and a fall in household consumption is what the ECB should have feared most. The irony is, it had all the monetary tools to assist the ailing Eurozone economy sooner. To those of us that don’t sit on the ECB’s Governing Council, it appears that the ECB has consistently and intentionally run tight monetary policy in order to avoid moral hazard in financial markets. This has come at the cost of supporting the real economy and failing in achieving its primary task – an inflation rate of below, but close to, 2%.

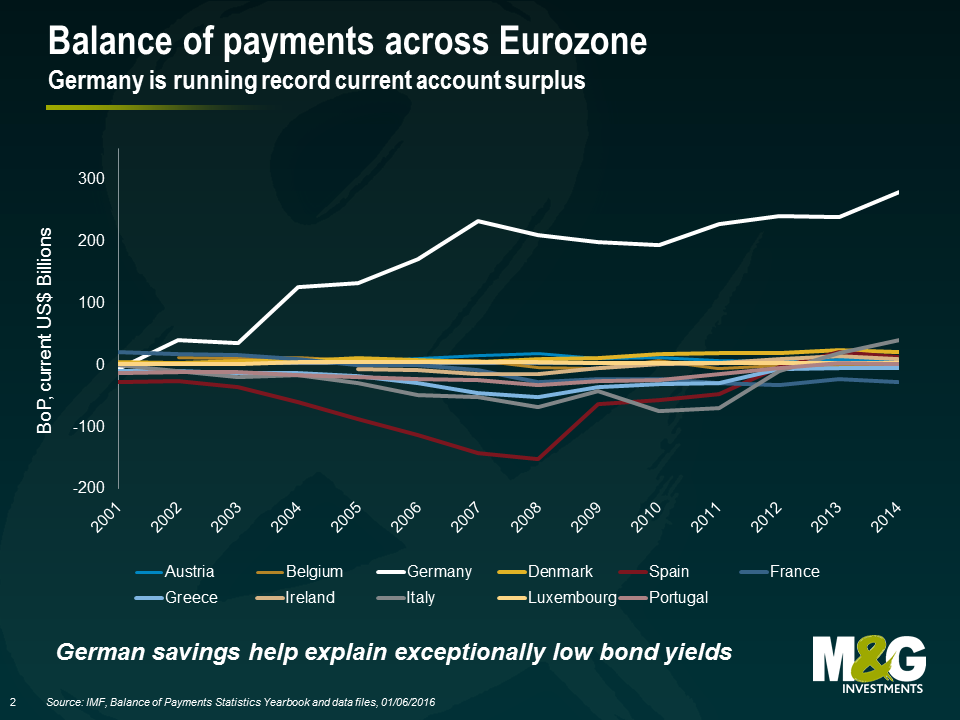

Of course, the ECB was dealt a bad hand to begin with. A currency union of diverse economies, absent fiscal union, is a fragile union at best. At the heart of the Eurozone’s fragility is Germany’s often overlooked and consistently growing current account surplus. Germany’s current account surplus is almost 9% of GDP. This is in violation of the European Commission’s Macroeconomic Imbalance Procedure, which limits surpluses to +6% of GDP. Martin Wolf from the Financial Times has labelled Germany as ‘the Eurozone’s biggest problem.’ Germany has the capacity to now borrow at negative or close to zero yields, yet the public investment in Germany is the second lowest in the OECD (1.5% of GDP), while net public investment has been negative since 2003. As we have pointed out previously, Europe needs a German fiscal stimulus package but won’t get it.

As the Eurozone’s largest economy and creditor Germany has been a major proponent of the Eurozone running a budget surplus. In order to acquire funds to service high debt levels, countries like Greece, Portugal, Spain and Ireland have had to attempt to move their fiscal balances from deep deficits to surplus positions. In order to achieve this, governments have had to implement harsh austerity measures, encouraging saving rather than investment. Consequently whilst Germany enjoys low unemployment rates, rising wages, higher house prices and a cheap currency; the Southern European economies have been mired in economic stagnation, recession and depression.

Addressing these fundamental fragilities is at the heart of the issue for the Eurozone. Ultimately this will require either large fiscal transfers from north to south, significantly higher inflation in Germany or many years of mass unemployment in Europe’s weaker economies.

Nearly ten years from the start of the financial crisis in 2008 it doesn’t feel like we are any closer to a real solution. Until politicians are willing, or more likely forced, to take some very difficult decisions the ECB will have to continue to shoulder the load and act as the de facto fiscal agent for the Eurozone. The criticism of its actions will continue.

Here’s the latest in our series of interviews with the authors of interesting and important new books on economics, politics and investing. In it, Pippa Malmgren – a global strategist and former economics advisor to President George W. Bush – talks about “Signals”, her book about the challenges facing the global economy today both on a state level (China, Russia, the US) and for households. In both cases the tensions that are emerging might be blamed on central banks for allowing consumer prices to rise but wages to stagnate. The “signals” she refers to can help us to spot global trends way ahead of the official statistical data: “shrinkflation”, when companies keep prices steady but reduce the size of the goods, being just one example. This is a topic we’ve thought about a lot, and as always I’d like to provide a link here to our seminal academic paper on the number of “feet” in a packet of Monster Munch.

You can watch Pippa’s video below. This, and all of our other author interviews (including Adair Turner, TV’s Ed Conway, and Martin Ford) can also be found on our YouTube channel. We also have 5 copies of Pippa’s book to give away in our competition. To win a book, answer this question:

I have on my desk a “Grab Bag” sized packet of Monster Munch maize snacks. Once the competition has closed at midday UK time on Tuesday 21 June I will carefully open this packet in front of the cameras and count the number of “feet”. Nearest to the correct number of feet wins. “Damaged” feet will count as whole at the judges’ discretion (for example two half feet equals one foot). Snack dust and broken off toes will NOT count. If it matters, the Monster Munch are Flamin’ Hot flavour. This competition is now closed.

The results are in

Our Monster Munch grab bag contained 16 feet (see photographic evidence of the bag’s contents and Nico, our official counter, below). Only Michael Stanley correctly guessed 16, with next nearest guesses of 17 feet from Colin Donlon, James Pridmore and Peter Sainsbury, along with Richard Swain and John McLaughlin who guessed 13 feet. Congratulations to our winners – we will be in touch shortly to get your prizes out to you.

We are a little bemused following the latest US Employment report. The headline figure of +38,000 jobs for May (expected: +160,000) disappointed the market, with Treasuries rallying and a June/July rate hike off the table in most economists’ views. A decline in the participation rate to 62.6% helped the unemployment rate fall to 4.7%, the lowest level since 2007, while average hourly earnings rose to 2.5% year on year.

It is well known that US Employment reports (especially the headline payrolls number) should be taken with a large pinch of salt, as the report is often subject to large revisions and has a margin of error of almost 100,000 jobs. Additionally, the Bureau of Labor Statistics estimates that the seven-week long Verizon strike had an effect of weighing on payrolls by around 35,000 jobs. These jobs may well be added back to the employment numbers next month.

Of course, this is speculation. However, unlike most reactions to the employment report, we don’t think the FOMC will be worried that the US economy is slowing. Nor do we think that May’s employment report is an indication that the US may be headed for recession. Using the unemployment rate as an indicator of possible recession, the US has not historically entered into a contractionary environment until the three-month moving average crosses the three-year moving average. As the chart indicates, there are no early signs of this recession indicator turning for now.

If the US economy is continuing to expand, then there could be another reason why the payrolls numbers were disappointingly low. That is, the economy could be getting close to full employment (as an unemployment rate of 4.7% would suggest). This means that employers are finding it difficult to hire suitable workers for the jobs that are available. If this is indeed the case we would expect to see labour cost measures, like the Employment Cost Index (currently 2.4% yoy), quickly start to rise over the remainder of 2016.

The market is now pricing in a rate hike in December (moved out from July). This appears too cautious to us. As Richard has outlined previously, employment markets are healthy and the economy is probably very close to full employment. Given the inherent lag in monetary policy, it is important that the FOMC reaffirms its stance of gradually removing policy accommodation. Otherwise, it risks tapping on the brakes too late.

At the start of April I wrote about some of the unintended consequences of central banks setting negative interest rates. I also promised to update the blog as we spotted more interesting implications, and asked readers to submit examples too. Thanks for those who got in touch. Here are some more of the interesting things that happen when the zero lower bound ceases to exist, as well as links to some theoretical thinking on negative rates.

Please post any more sightings of either unusual economic or market behaviour as a result of negative rates, or links to interesting academic work on the subject, into the blog comments below!

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.