World Cup

The Bond Vigilantes World Cup Model

By Joe Sullivan-Bissett

19 June 2026

When the Bank of England’s Monetary Policy Committee meets next week, the market expects that they will cut rates, especially now that even outgoing hawk, Martin Weale (who has been at the Bank for 71 meetings so far, and voted to hike 12 times, and to hold 59 times) says that he will support a reduction. A resumption of the Funding for Lending (FLS) scheme is also a possibility (many economists suggest that this was the most successful policy action taken to stimulate the economy during the UK’s Great Recession). The Bank’s remit also allows it to reopen Asset Purchase Facility, better known as Quantitative Easing. The BoE bought £375 billion of gilts from 2009 to 2012. It also bought sterling denominated corporate bonds, in the Corporate Bond Secondary Market Scheme. Largely taking place between March 2009 and March 2010, £2.25 billion of investment grade, non-financial, corporate bonds were purchased.

Whilst small in scope compared with the gilt purchases, the impact on credit spreads at a time when investors had already identified post-crisis value, was large. Borrowing costs fell substantially and the new issue market for companies re-opened. The idea that the BoE might start buying sterling corporate bonds again is now being discussed, especially as the ECB is buying euro denominated bonds at a fierce pace as part of its QE programme. On the face of it though, credit spreads are trading near their historical average rather than near Great Depression levels as in 2009, and in the banking market both the availability of credit and the spread costs to large companies – those that could borrow in corporate bond markets – are benign, if not “easy”. So why would the BoE want to start buying sterling credit again?

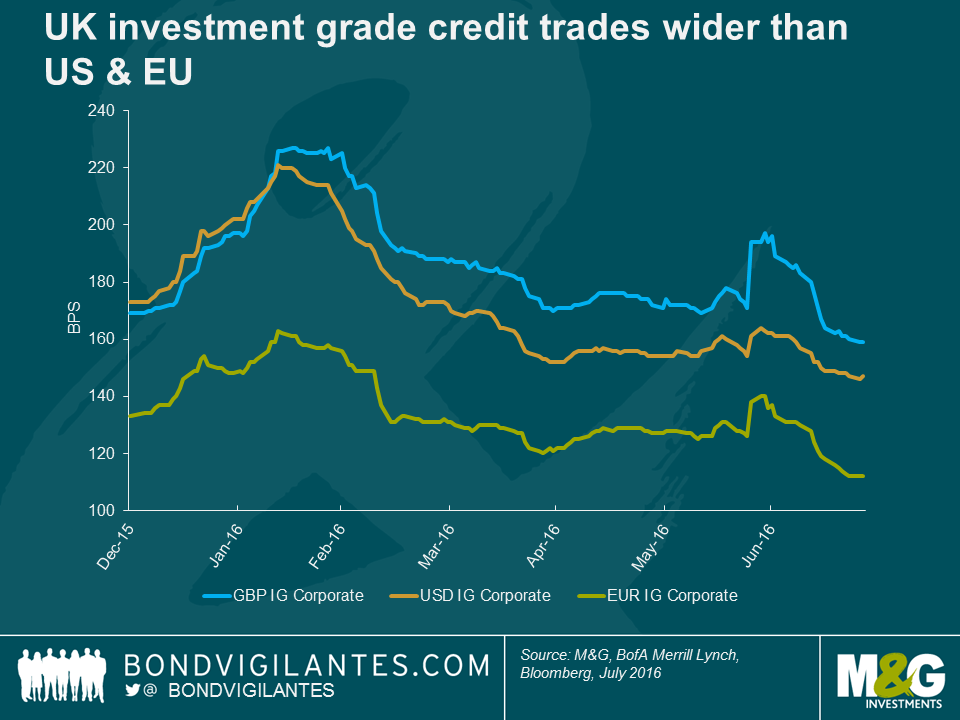

Well although credit spreads have fallen globally, especially post-Draghi’s March announcement of corporate bond purchases, sterling credit has definitely lagged. Using BofA Merrill Lynch indices to compare market levels, the UK investment grade corporate bond market trades at a spread of 161 bps over government bonds, compared to 148 bps in the US and 114 bps in Europe. Now there’s definitely a compositional bias here – for example the UK corporate bond market is longer dated and you might expect a risk premium as a result. But when you look at spreads on a “same name, similar maturity” basis, the UK corporate bond market is still wide. For example Deutsche Telekom bonds with a 2030 maturity trade with a spread of gilts plus 108 bps in sterling, or bunds plus 90 bps in euros. Johnson & Johnson 2023 bonds trade at gilts plus 40 bps, or US Treasuries plus 19 bps. Tesco 2024 bonds have a spread of 314 bps over gilts, versus the euro 2023s spread at 257 bps over bunds.

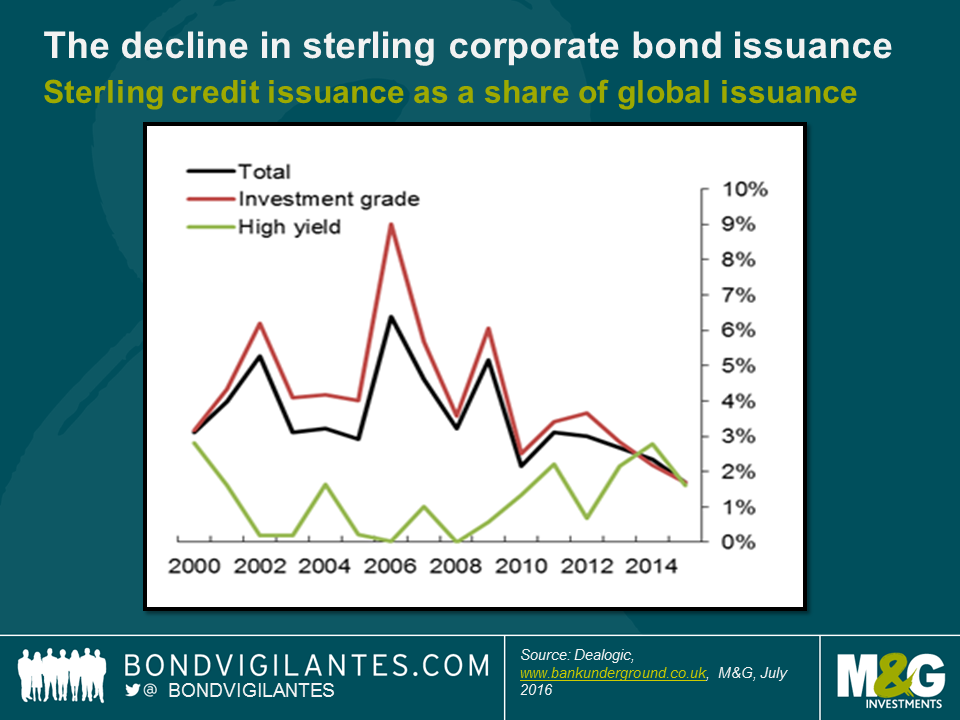

Because the UK credit market trades wider than other big capital markets, it deters corporate treasurers from issuing in sterling. It’s more expensive. Most big companies can choose where they issue debt, and they can hedge away the currency risks using swaps, leaving just the “pure” cost of the debt to consider (they must also take into account the cross currency basis swap costs, but that’s another story). This has become a vicious circle for the UK debt market. As companies see cheaper funding available elsewhere, they issue in US dollars or euros, which reduces liquidity in the sterling market, which leads to wider credit spreads, which makes it more expensive to issue in sterling. And so on. The BoE examined some of the factors behind the fall in sterling issuance on its excellent Bank Underground blog in April this year. In it they showed that annual gross sterling issuance has almost halved since 2012, and sterling’s share of global issuance last year was the lowest on record.

The BoE staff ascribe the fall in sterling issuance to three reasons. Firstly, a concentrated sterling investor base and mergers in the industry meant that some large institutions were effectively “full” of some names, and a lower number of participants meant that it could be hard to get deals done, meaning higher yields were required to entice buyers. Secondly, changes in annuity rules reduced the demand for long dated credit. And finally, the growth of the euro denominated corporate bond market since 1999 has led to it gaining “critical mass” for both issuers and buyers.

If the BoE were to restart its corporate bond programme, it could drive credit spreads down to something in line with euro and dollar issuance through ongoing, price insensitive buying. Lower UK credit spreads relative to the other major markets would provide some incentive for corporates (both domestic and global) to start issuing sterling bonds once more.

In a post Brexit world, with a threat of financial market activity moving away from London, the reinvigoration of a declining UK corporate bond market appears attractive. Whilst the reduction in financing costs for UK based corporates might be marginal, it too would be welcome if the weak post-Brexit survey data is correct in predicting a sharp downturn in economic activity.

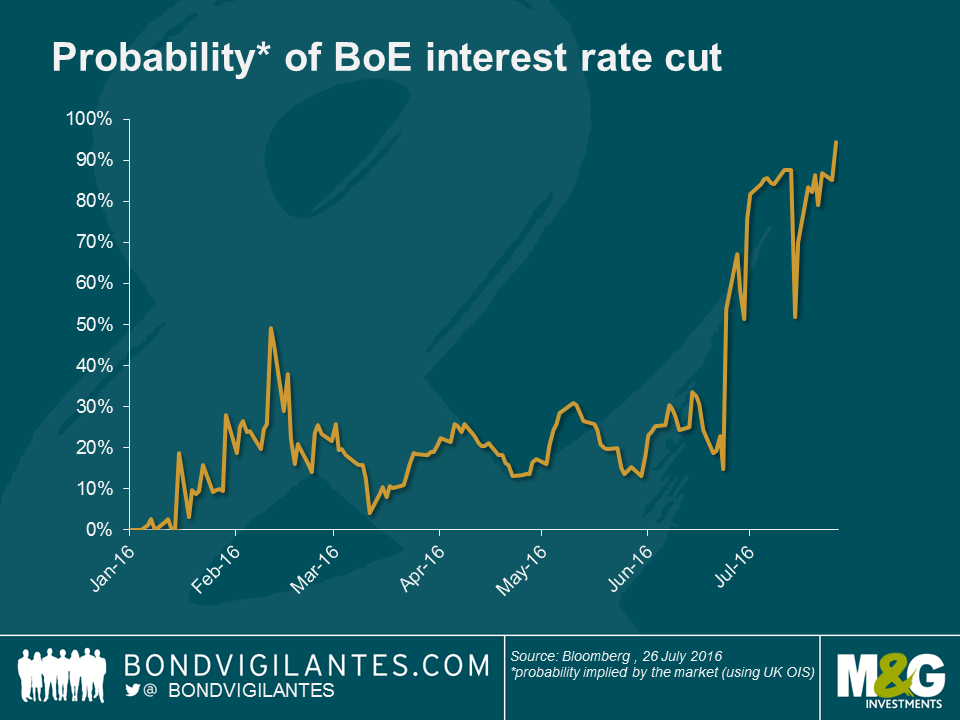

Despite keeping interest rates on hold at the 4th July meeting, the minutes of the Monetary Policy Committee indicated that “most members expect an easing in August” (even long-time hawk Martin Weale has shifted to a dovish stance). Subsequently, markets are pricing in a staggering 98.3% probability of a rate cut at the next meeting in 8 days’ time. With UK data expected to deteriorate over the next few months, market pricing seems appropriate.

However, something else that stood out from Governor Carney’s 30th June speech (other than his expectation of some summer monetary policy easing), was this: “In August, we will also discuss further the range of instruments at our disposal.” With interest rates close to zero, Governor Carney could be indicating that the BoE is limbering up to provide a bumper stimulus monetary package, alongside an interest rate cut, akin to that unveiled by the ECB in March this year.

Here are five options that could be available to the MPC.

A renewal of the BoE’s quantitative easing programme seems the most likely easing measure that the MPC could take outside of cutting interest rates; the ultimate goal of the policy being to facilitate an expansion of private bank lending, via central bank asset purchases. Should this occur, we would expect the belly of the UK government bond curve to be well supported. In particular, gilts with maturities in the 7-15yr range could benefit given that there are fewer bonds in this maturity bucket (assuming the BoE aims to make purchases in line with its QE reinvestment rules which we have discussed here) and this is the duration neutral part of the curve. More pertinent to the UK perhaps would be what Fathom Consulting have coined “Operation Anti-Twist” (based on the FOMC’s 2011 “Operation Twist”) which would entail selling long dated gilts and buying short dated gilt issues. This would engineer a steeper yield curve and could support those with longer term pension liabilities looking for higher yields.

In order to improve market liquidity in 2009-2012, the BoE purchased corporate bonds as part of its QE programme. Though this is not necessarily an imminent priority – there does not appear to be a corporate funding crisis; GBP non-financial investment grade corporate spreads did spike up, but have fallen since the referendum – this nevertheless presents a credible policy option.

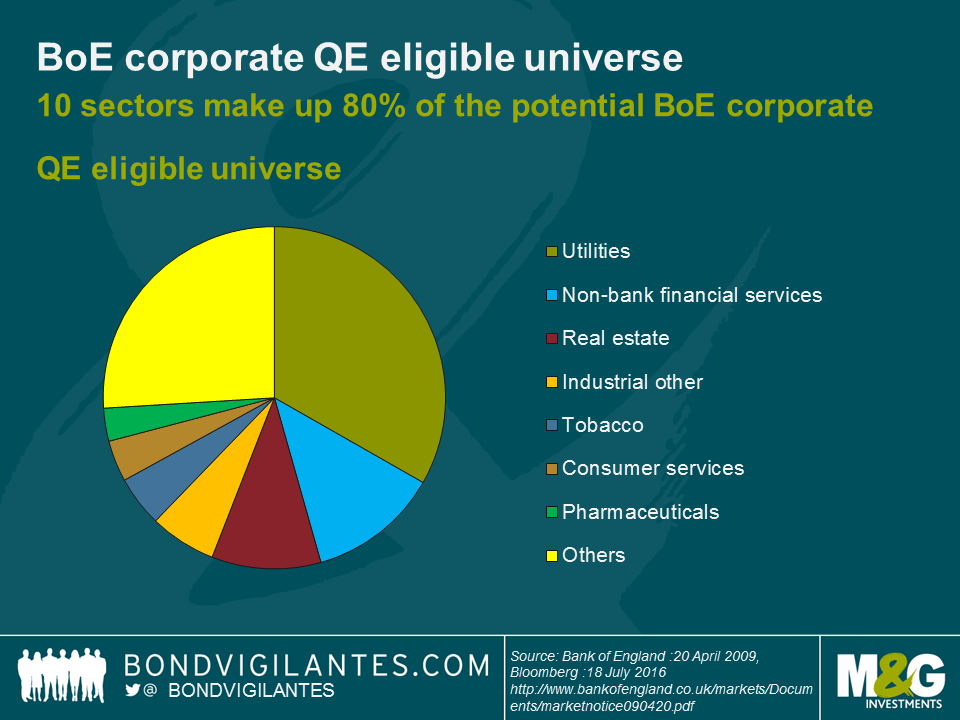

If the BoE were to resume corporate bond purchases, along the same criteria used previously (which was much stricter than that currently used by the ECB, especially with regards to rules regarding credit ratings), I estimate that the investment universe would be in excess of £100bn, with utility companies representing the lion’s share of eligible purchases. Real estate companies also appear set to benefit notably from corporate QE, which could offer some targeted support to a sector that’s already been particularly hard hit.

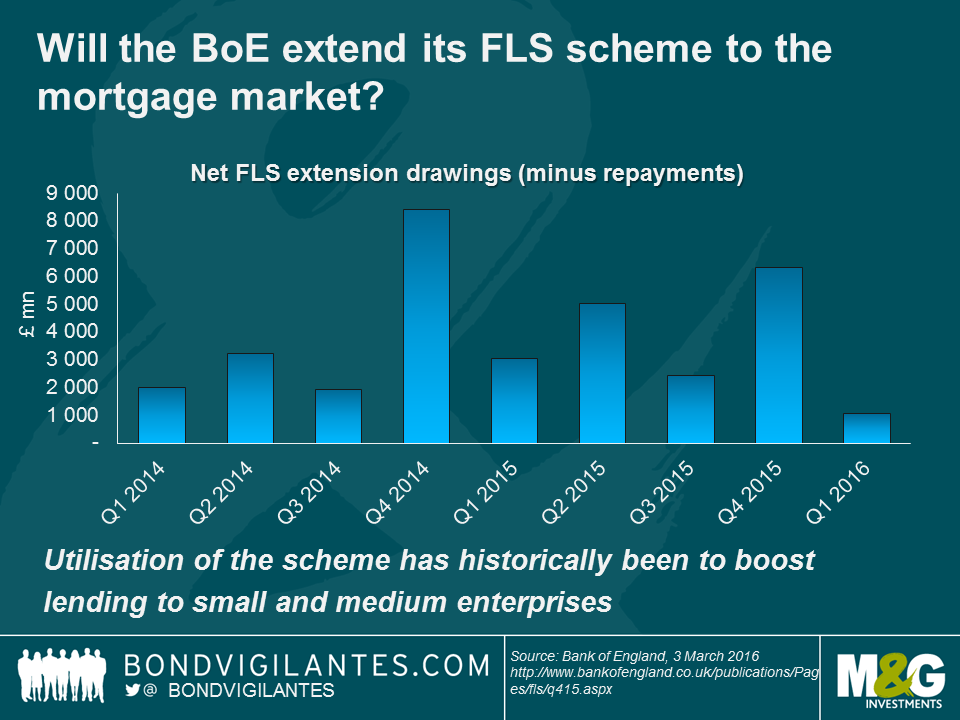

Earlier this month the BoE reduced the UK countercyclical capital buffer rate – for banks, building societies and large investment firms – to zero from 0.5% until at least June 2017. Governor Carney noted that this will lower UK banks’ required capital buffers by £5.7bn, essentially freeing up capital for them to lend to the real economy. Should upcoming data warrant it, the BoE could extend its Funding for Lending Scheme (FLS), to further ease credit conditions for households. The current scheme incentivises banks to boost lending, with a skew towards small and medium sized enterprises – arguably those who will be hardest hit from the ongoing uncertain outlook. They could however extend this scheme in a further targeted manner, for example, towards mortgage lending in a bid to subsidise loans for house purchases (should market conditions warrant this). The FLS has been extended many times since it was introduced in July 2012, with the last extension taking place in November. Though we have previously questioned the success of the scheme, we could potentially see another amendment.

Investors and markets are positioned for a low growth, low inflation world, but this could be about to change. With the limits of global monetary policy arguably exhibiting diminishing returns to scale, there is now the potential to see expansionary UK fiscal policy working alongside monetary policy. Given the reshuffling of the cabinet, Osborne’s fiscal tightening and austerity budget have fallen by the wayside and it is time for Hammond to show his hand. Given the unusual circumstances, the new chancellor could plausibly move his autumn statement to coincide with the BoE meeting on the 3rd November and offer something original. If he takes the advice of the IMF and OECD, both of which have been calling for a boost in infrastructure spending, we could potentially see the government opting for pro-growth infrastructure projects, funded via bonds that the BoE ultimately buys.

Could the BoE introduce negative interest rates, like we’ve seen in the Euro area and Japan? In theory yes, but in practice I believe that this is some way off. Negative rates are still in their experimental phase (Jim has noted some great anecdotes on this here and here) and the BoE still have some leeway with regards to traditional monetary policy. With interest rates at 0.5%, there is still space for a few cuts before we reach the zero bound and have to contemplate any unconventional measures.

Evidently there are many tools in the toolbox (and I have focused predominantly on the tried and tested), but will the BoE look to use them? Every monetary policy meeting should be noted in your diary, every meeting is ‘live’. Roll on the next BoE monetary policy decision.

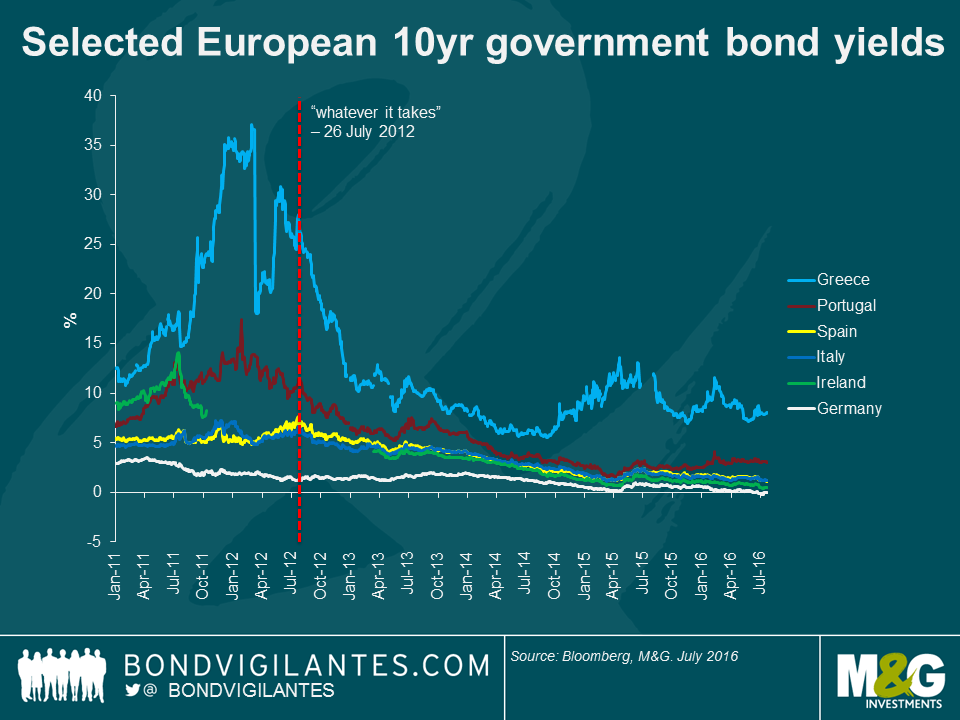

Transport yourself back to July 26, 2012. Borrowing costs for the “peripheral” European nations are uncomfortably high. Ireland, Portugal and Greece were in the process of applying for bailouts, while the Spanish banking system was dangerously close to falling over. It wasn’t a question of when an EU member would leave the single currency bloc, but who? Step forward ECB President Mario Draghi, who in an address delivered to a room full of business leaders and investors, proceeded to deliver the most important sentence delivered by a central banker in modern times – “Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it will be enough”.

The big question at the time was what is it?

Fast forward to today, and we have some understanding of what President Draghi meant. He was referring to a range of conventional and extraordinary monetary policy measures, including a cut in the ECB’s main refinancing rate from 1 to 0%, a cut in the deposit facility from 0.25 to -0.40%, long-term refinancing operations that reached over 1 trillion euros in size, emergency liquidity assistance for Greece that currently stands at 54 billion euros, and an asset-purchase programme worth 1.1 trillion euros (subsequently extended, expanded and increased by around a third). As a result, the ECB balance sheet now stands at 3.2 trillion euros (or 131% of Euro area GDP).

That’s the it. Was it enough?

Looking at peripheral bond yields suggests that it was. Investors are no longer demanding the credit premium they once were, resulting in a collapse in bond yields.

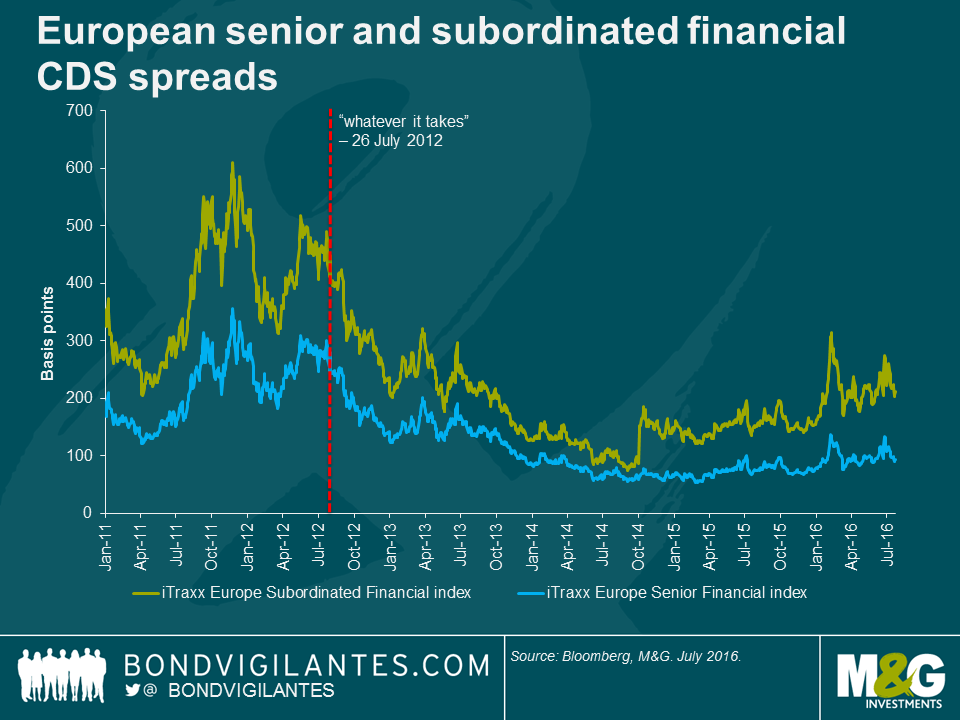

In his speech, Draghi referred to the spike in risk aversion being linked to counterparty risk. As shown below, CDS premia have collapsed in the Euro area from 2012 levels but sub-financials have been on a widening trend since Q4 2014. More recently, investors are questioning the amount of bad debts that a number of European banks have on their books and whether these losses can be sustained in some of the more fragile financial systems of the Euro area.

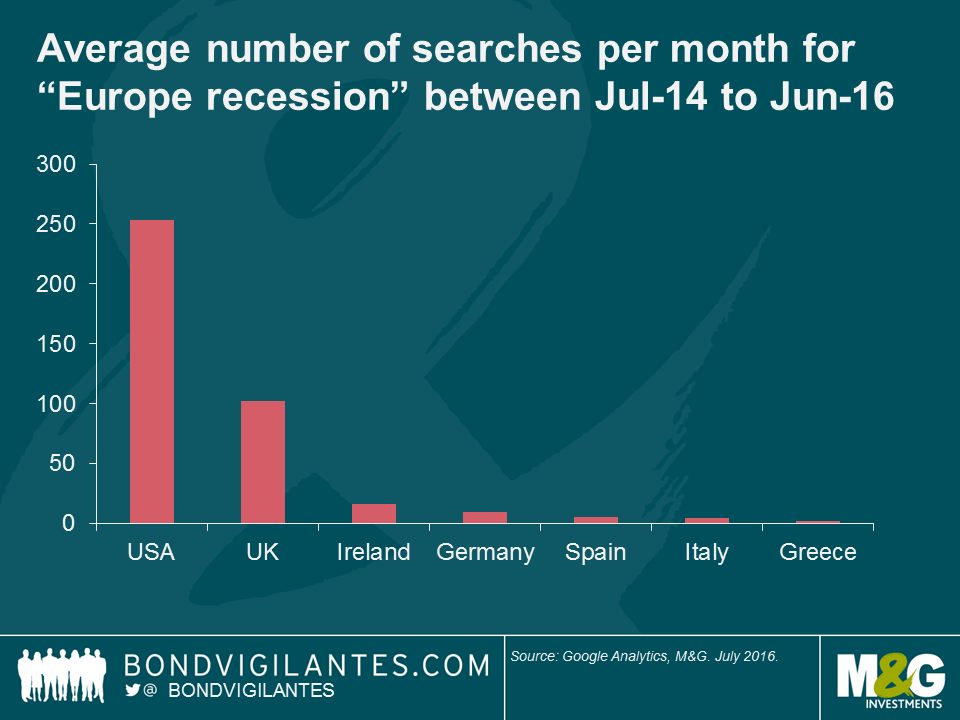

Finally, using Google, it appears that people from the US and UK are more worried about a European recession than Europeans themselves over the past two years. The vast majority of searches for “Europe recession” come from the US or UK (I also checked for local language equivalents: there are 7 searches per month on average in Germany for “Europa rezession”; and “recessione Europa” registers 5 searches in Italy for example).

President Mario Draghi brought calm and stability to very volatile markets four years ago through his speech. His words acted like a risk-off circuit breaker, and European government bond markets and the financial system benefited from that. It goes to show that a central banker with a mandate does have the ability to heavily influence financial markets. Indeed, President Draghi may have saved the single currency bloc, as it appeared the ECB was the only European institution that had the ability to act quickly, decisively and in a large enough magnitude to support the European economy in the absence of a European fiscal union.

Unfortunately, not much has changed on the fiscal front. Europe still faces some significant structural issues, with a significant divergence in economic outcomes across the Euro area member states. Brexit will also likely prove to be a headwind for economic growth. Economically, Europe is still struggling with high unemployment rates and very low inflation despite four years of extraordinary monetary policy. With the markets expecting more monetary stimulus in September, it appears that the ECB’s job of doing “whatever it takes” is still not over.

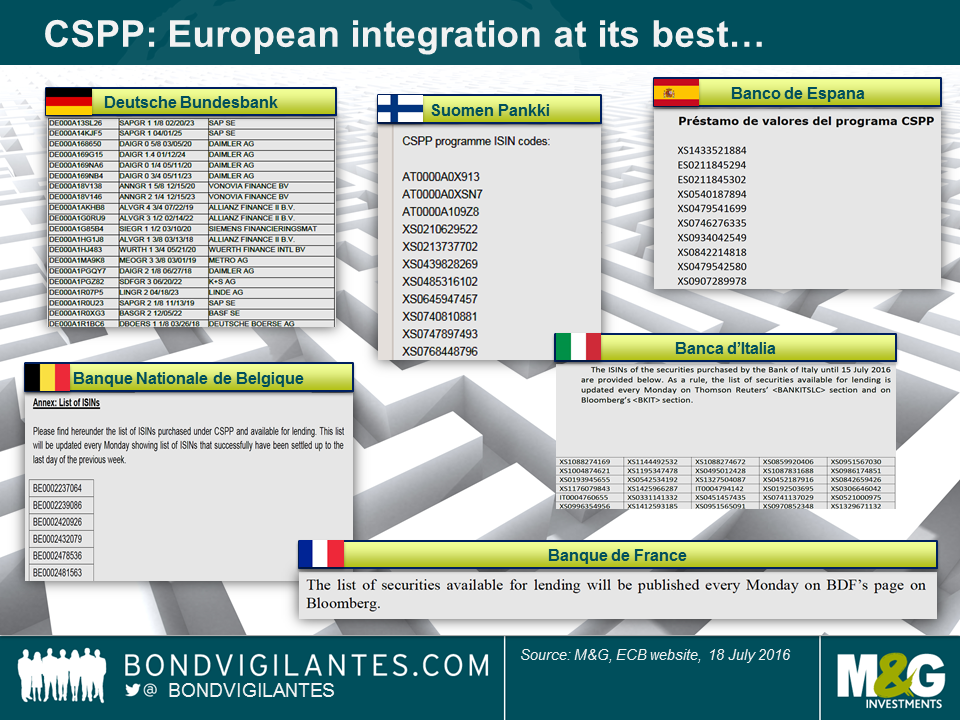

Having recently blogged about the potentially eligible universe of the Corporate Sector Purchase Programme (CSPP), we were naturally eager to find out which corporate bonds the European Central Bank (ECB) has actually been buying. On Monday, the ECB eventually published the highly-anticipated list of their bond holdings.

Except that’s not what happened. Instead of the ECB releasing a neat consolidated list, each of the six national central banks carrying out the bond purchases disseminated their statements separately on the ECB’s webpage. Apart from the blatant lack of integration, they didn’t appear to be overly concerned with consistency either (see below). In fact, they took inconsistencies to almost comic levels. Most banks chose to only state International Securities Identification Numbers (ISINs), presented in a variety of layouts. The German Bundesbank, being a stickler for details, felt the need to go above and beyond by additionally mentioning security and issuer names – Dankeschön. Banco de España did not consider it necessary to provide an English language version of their document – No importa. The other banks did, even the proud Banque de France, which however didn’t release any security identifiers on the ECB’s webpage but kindly told interested readers to do their own research on Bloomberg – Incroyable!

Before diving into the analysis, it is important to point out that we only know the total volume of purchases – EUR 10.43 billion between 8th June and 15th July – and the identity of the 458 corporate bonds that have been bought in this period. But we do NOT have the portfolio weights. The average position size is EUR 22.8 million but the dispersion around the mean is entirely unknown. To give an example, Deutsche Bahn is the most popular issuer in terms of ISIN count: 12 of their bonds have been purchased, which puts them ahead of Telefonica (11) and BMW (10). But without knowing the size of the holdings we cannot compute weighted averages and are thus unable to draw any firm conclusions with regards to the actual risk exposure towards Deutsche Bahn.

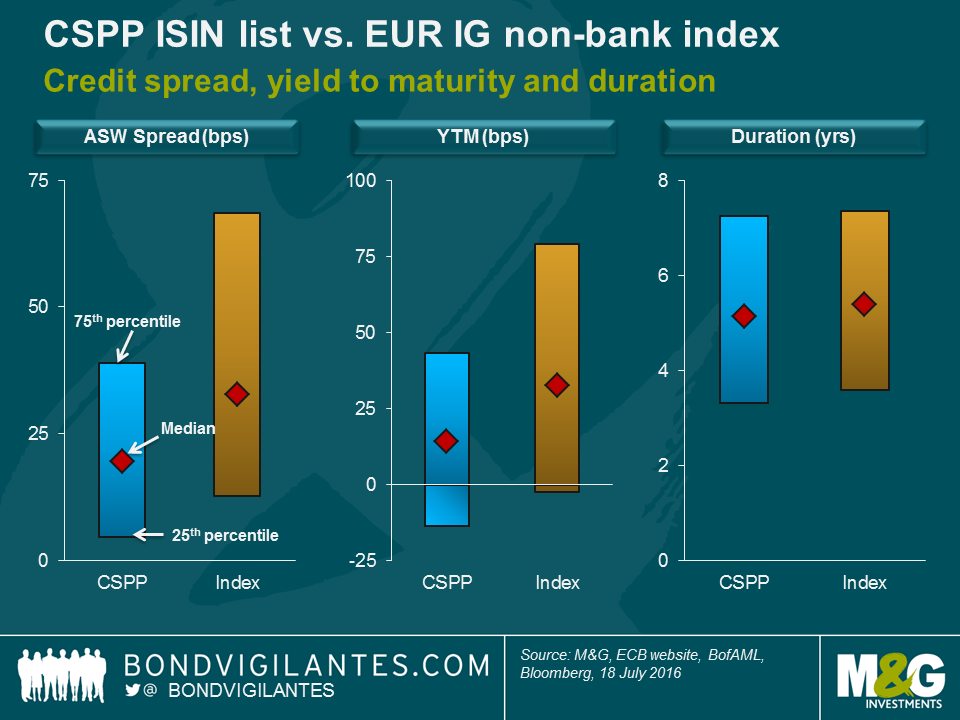

Nonetheless, we can apply basic percentile analysis to get a better understanding of the ECB’s corporate bond holdings. The median asset swap (ASW) spread and median yield to maturity (YTM) of the CSPP holdings are 20 bps and 14 bps, respectively. In comparison, the corresponding median values of the EUR-denominated investment grade (IG) non-bank index, a crude proxy for the eligible bond universe, are both above 30 bps. The middle 50% of CSPP spread and YTM values (i.e., from the 25th to the 75th percentile) are less dispersed and shifted to lower values, compared to the index. Remarkably, more than a third (c. 36%) of the CSPP bonds are currently trading at a negative YTM. This is an indication that the CSPP holdings might be more defensively positioned than the index, but as mentioned before we do not know the portfolio weights. In terms of duration, CSPP median (5.1 years) and dispersion are very close to the index.

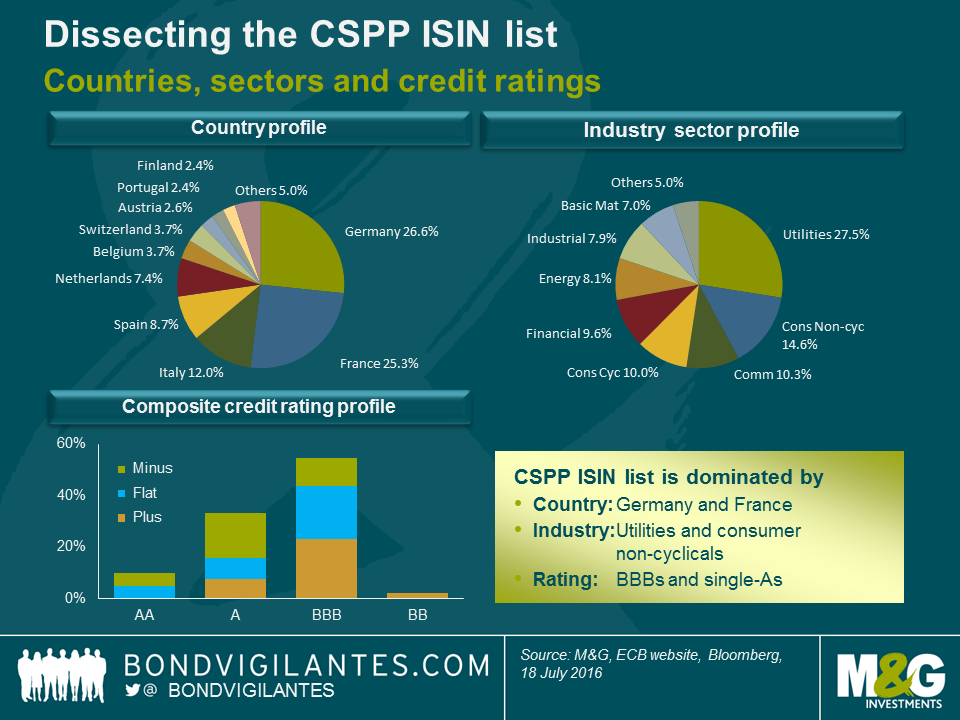

We also dissected the CSPP list further by country of risk, industry sector and composite credit rating (see chart below). Although French companies have far more ECB eligible debt outstanding than German firms, the ISIN count is pretty much neck-to-neck. Both countries account for around a quarter of the list. Only 3 bonds from U.S. issuers have been purchased, which is far less than for Swiss (17) and British (7) corporates, the other non-Eurozone countries on the list. Bonds of these companies are ECB eligible as long as they are issued from legal entities established in the Eurozone and fulfil further criteria (Euro-denomination, IG rating, etc.). Considering the sizeable amounts of eligible bonds from U.S. firms, they seem to be underrepresented. But again, at the risk of sounding like a broken record, since position sizes are unknown we simply don’t know for sure whether the ECB is really “underweight” with regards to French or U.S. corporates.

In terms of industry sectors, utilities (28%) and consumer non-cyclicals (15%) dominate the ISIN count. This is not at all surprising as the share of these sectors within the ECB eligible bond universe is similarly large. Likewise, the credit rating distribution (55% BBBs, 33% single-As) is broadly in line with the eligible universe. It is worth highlighting that the ECB made use of the loose IG eligibility criteria (a single IG rating from Moody’s, S&P, Fitch or DBRS is sufficient) and bought bonds of a couple of cross-over names with sub-IG composite ratings (e.g., Telecom Italia and Lufthansa).

In summary, there are definitely a number of interesting lessons to be learnt from analysing the CSPP ISIN list. But as tempting as it may be to draw conclusions regarding over- and underweights and thus to anticipate the ECB’s future buying activity, we have to acknowledge that we are simply lacking data. Trying to “front run” the ECB is therefore a highly difficult, if not impossible task.

In the second part of the video from our recent New York research trip, M&G’s Richard Woolnough takes a look at three more topics. Firstly, the U.S. labour market is strong and inflationary pressures are building. The Federal Reserve is currently on hold due to external events, but maybe not for long. Secondly, while the lower oil price by and large is beneficial for Western economies, bond valuations in certain business sectors have clearly suffered, creating interesting investment opportunities. And finally, given the Presidential race is probably going to be Trump versus Clinton, bond market uncertainty and risk premiums could well be higher than we are normally used to during a Presidential election campaign.

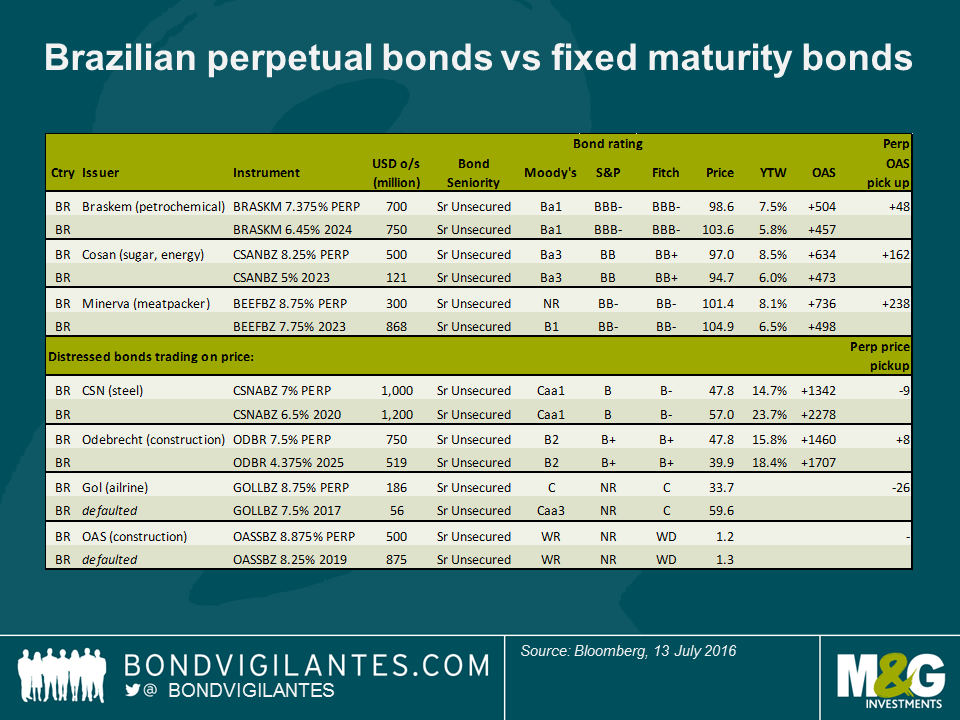

In developed markets, the vast majority of perpetual bonds are contractually subordinated, i.e. it is stated in the bond documentation that they are junior to any senior secured or unsecured debt, and as a result they tend to have lower bond ratings than senior bonds in the same capital structure because they have a lower expected recovery value. In emerging markets, however, it is not uncommon to see senior unsecured perpetual bonds. Brazilian corporates, from construction company Odebrecht to national airline GOL, have sold perpetual bonds in the past decade fuelled by investors’ appetite for yield and in order to secure long-term financing. In most cases, these perpetual bonds are contractually pari passu with other unsecured unsubordinated indebtedness of a same issuer. What developed and emerging markets have in common is that the seniority and ranking of a bond does not depend on its maturity date; two senior unsecured bonds with different maturities but same indenture will have a similar bond rating.

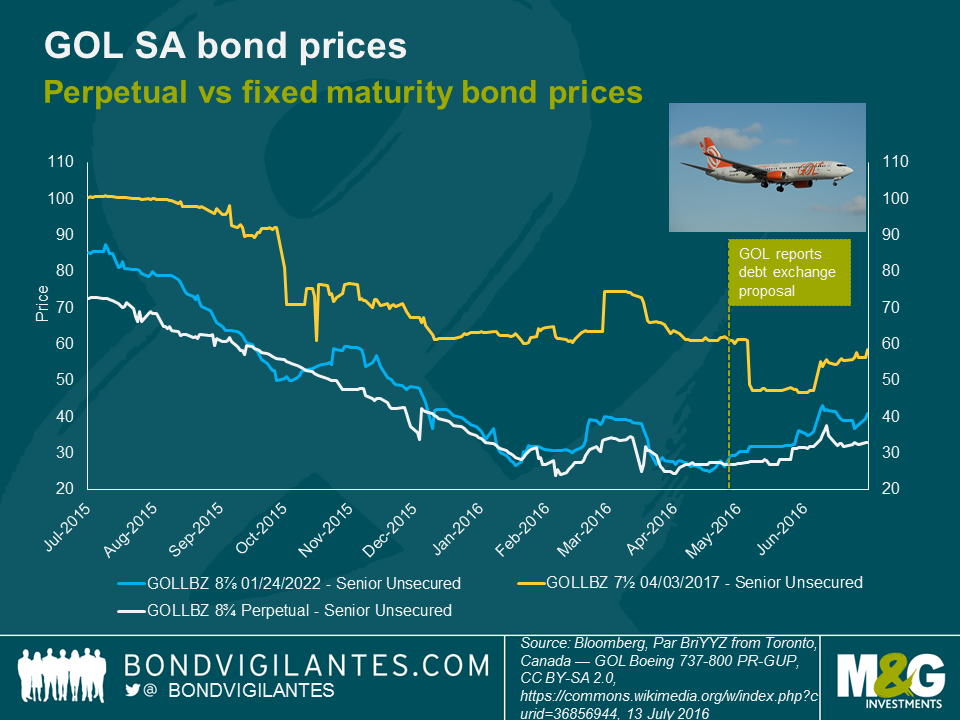

A case in point is GOL, the Brazilian airline, which issued $200 million worth of GOLLBZ 8.75% perpetual bonds in 2006. This bond had similar ranking and guarantees* than the later-issued fixed-maturity GOLLBZ 7.5% 2017 senior unsecured bonds. As a result, the rating agencies in 2007 assigned a similar bond rating to both instruments (Ba2 by Moody’s and BB+ by Fitch), assuming their probability of default and recovery value would be similar. While on paper this looked sensible because Brazilian judicial restructuring states that each class of creditors must be treated equally, the economic downturn in Brazil has proved this approach to be, in my view, the least conservative for bond-investors.

Starting in 2012, GOL experienced significant macroeconomic headwinds (recession and currency depreciation) which resulted in lower demand, industry overcapacity and financial troubles for one of Brazil’s largest airlines. Rating agencies downgraded GOL’s bonds in line with its credit profile deterioration and the perpetual unsecured bond rating was again similar to other fixed-maturity unsecured bonds. In May 2016, Gol’s liquidity position and balance sheet became unsustainable and the company launched a restructuring proposal. The private restructuring offered bondholders an exchange of their existing bonds into a small portion of cash and into newly issued bonds. However, while the senior unsecured bonds with maturities between 2020 and 2023 were all treated equally – the proposal was a debt haircut of about 45% at best – the senior unsecured perpetual bondholders were offered much worse terms with a debt haircut of 55% and full exchange into new bonds with no cash consideration.

The shorter-dated GOLLBZ 7.5% bonds due in 2017 received the best treatment with a debt haircut of about 30%. Even the early participation fee granted to bondholders for accepting the offer was less attractive (not in cash) for the perpetual bonds. Therefore, the recovery value of the perpetual bonds was below the one of the senior unsecured bonds because the restructuring proposal did not respect the contractual ranking and guarantees of the various bonds but rather applied treatment based on the maturity of the bonds.

Rating agencies seem to have taken note of the above, although arguably that was too late for bondholders. On 5 May 2016, a couple of days after GOL’s debt exchange was offered, Moody’s changed their view and decided to downgrade the perpetual bond rating to C from Caa2 while the fixed-maturity bond due in 2017 was downgraded by only one notch to Caa3 from Caa2. Moody’s stated: “The 2017 senior unsecured note is now rated at the same level (as the company’s issuer level), given its expected recovery rate, while the Perpetual notes is rated C, given its lower expected recovery rate.”

GOL’s case has significant implication for the rest of the Brazilian perpetual bond market which to me appears overpriced and overrated. In general, in a non-distressed world average spreads for holding perpetual bonds in Brazil are somewhere between 50 to 200 basis points wider than 10-yr senior unsecured bonds but this is the spread rewarding the maturity difference (uncertainty of when bondholders will be redeemed) rather than the recovery value estimate. Maybe this is because most of the perpetual bonds continue to have similar ratings than fixed-maturity unsecured bonds. For instance, this is the case for petrochemical company Braskem’s perpetual bonds (Ba1) which nowadays trade 48bps wider than Braskem’s 2024 unsecured bonds (Ba1).

In distressed credit, some perpetual bonds are even trading at cash prices higher than fixed-maturity senior unsecured bonds of the same capital structure. Construction company Odebrecht’s perpetual bonds (B2, watch negative) trade at 48 mid-price while Odebrecht’s 2025 unsecured bonds (ba2, watch negative) trade at 40 cents on the dollar. This makes little sense and it is unclear to me whether investors have priced in the fact that on paper these instruments are pari passu to other unsecured bonds but in practice are likely to be treated differently in a private restructuring.

Diligent holders of perpetual bonds in Brazil may want to notch down their bond rating internally and make sure they are getting paid for the risk they face, in particular in a country with elevated default rates and high likelihood of private debt exchanges in the next 12 to 18 months.

* The bond documentation states: The notes will be unsecured and will rank equally with the other unsecured unsubordinated indebtedness the Issuer may incur. The notes will be guaranteed, jointly and severally, on an unsecured unsubordinated basis by the Guarantors.

The guarantees will rank equally in right of payment with the other unsecured unsubordinated indebtedness and guarantees of the Guarantors. The notes will be effectively junior to the Issuer’s and the Guarantors’ secured indebtedness. Under Brazilian law, holders of the notes will not have any claim whatsoever against the Guarantors’ non guarantor subsidiaries. The Guarantors will unconditionally guarantee, jointly and severally, on an unsecured unsubordinated basis, all of the Issuer’s obligations pursuant to the notes.

I spent a significant chunk of the weekend with my head buried in a great book; Superforecasting: the Art and Science of Prediction. In this book, Philip Tetlock and Dan Gardner tell the story of Tetlock’s experiments in harnessing the wisdom of crowds to predict the direction of geopolitical and economic events. Tetlock, a renowned social scientist, and his global band of volunteer forecasters, competed in a contest sponsored by an American intelligence agency (IARPA) over four years. His team did so well that the other four academic teams in the competition were dropped by IARPA after two years.

The contest began in 2011 and involved the teams independently answering hundreds of questions similar to those that intelligence analysts assess daily, e.g. predicting the likelihood of events such as Greece leaving the Eurozone, war breaking out in the Korean peninsula or Israel attacking an Iranian nuclear facility.

The only qualifications required to join Tetlock’s team, the Good Judgement Project (GJP), were an internet connection, some free time and an interest in current affairs. The volunteers were an eclectic bunch with apparently little in common. At the end of the first year, the GJP had nearly 3,000 volunteers whose collective judgement was used to generate the team’s entries in the tournament. As time passed and the number of predictions grew, the researchers were able to vary the experimental conditions (to determine which factors improved the accuracy of predictions) and identify the volunteers who were particularly prescient.

Every prediction was assigned a Brier score which assessed the accuracy and confidence of a prediction, once an outcome was known, and each forecaster’s cumulative score was tracked. A person who consistently predicted the correct outcome with 100% confidence would receive a perfect score of zero. A score of 0.5 would represent a series of random guesses or hedged 50-50 style bets. The worst score of 2 (as far from the truth as possible) would be assigned to those consistently predicting the wrong outcome with 100% confidence.

After the first year, out of the pool of 2,800 volunteers, 60 forecasters were identified as the most gifted. They had a collective Brier score of 0.25 (versus the group average of 0.37 for the remaining participants) and were awarded the title of “superforecasters”. By the end of the fourth year, the gap had widened significantly, with the superforecasters outperforming the rest of the team by over 60% and IARPA’s own professional (control) team by over 40%.

So, what was it about the super forecasters that allowed them to beat professional intelligence analysts, with little or no prior knowledge of the subject matter and without access to top-secret information? As I read the book, I made notes of the characteristics that Tetlock thinks makes a superforecaster. Here is my (by no means exhaustive) list:

At the top of Tetlock’s list however was what he dubbed a “growth mindset”; superforecasters are more interested in why their predictions were right or wrong, rather than whether their predictions were correct. They own their failures and mistakes and are always looking for ways to improve their performance.

For me, the big revelation was that foresight is a skill that can be developed and, more importantly, improved. As the authors point out, “even modest improvements in foresight maintained over time add up”; a pertinent message for investors and fund managers. I think that this is a fantastic book. It contains many more insights, touching on topics such as how to combine and manage teams of forecasters, and comes highly recommended.

If you would like to find out if you’ve got what it takes to be a superforecaster, or you’re just interested in what the project is trying to predict right now, you can take a closer look here.

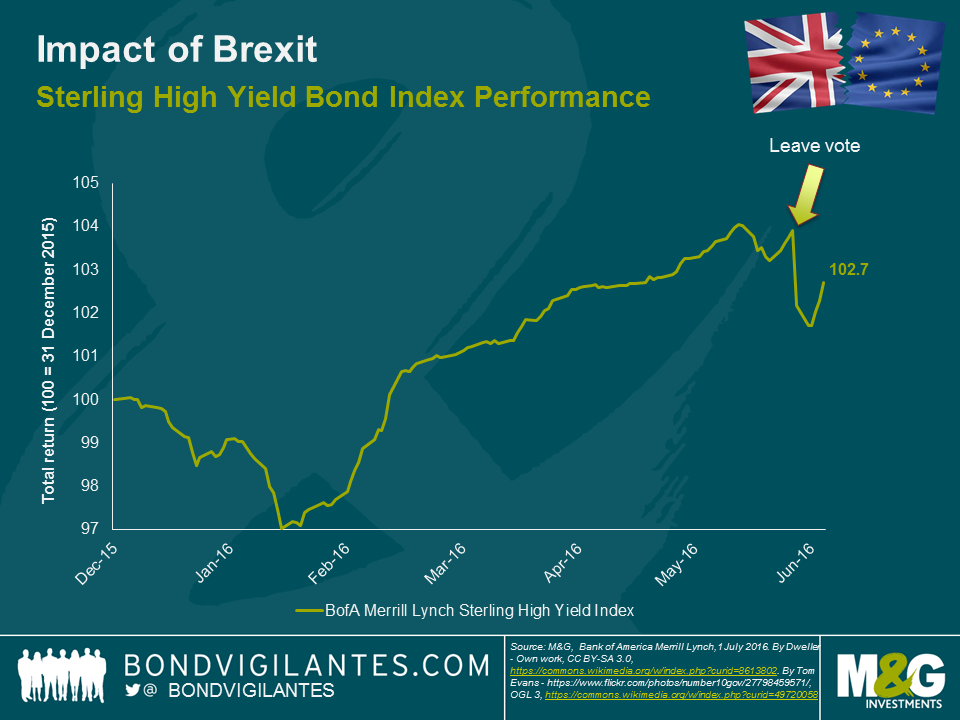

Much has been written about the impact that the referendum result has had on gilts, the pound and equity markets. In sterling high yield bond markets, we have seen some repricing with the market 2% lower in price terms since the vote. In my opinion, this has been a fairly benign reaction if you consider that the FTSE 250 is around 10% lower over the same time period. One explanation for the muted market reaction could be the expectation for further monetary easing in the near term. Governor Carney has signalled that the MPC is likely to ease policy rates over the summer. The possibility of direct central bank action in credit markets also hangs over fixed income markets at this point in time, helping to support market valuations. Of course, monetary policy can only do so much to support a deteriorating economy and Chancellor Osborne’s less austere approach to fiscal policy is also providing some hope that a possible UK recession would be a shallow one.

There could be other reasons why the reaction in the high yield market has been relatively benign. Like the FTSE 100 (up 2% since the vote), the high yield market is not a very good reflection of sentiment surrounding the UK economy. In fact, there is a significant number of international issuers that have non-investment grade ratings and issue bonds in sterling. For example, Anglo American, Gazprom, Petrobras and Enel are all constituents of this market. This has a dilutive impact on any UK-specific re-pricing of risk. Also, the supportive moves by various central banks in the aftermath of the vote has helped support all risk assets, including credit.

There will be some winners and losers in terms of the underlying issuers of these bonds and in order to forecast these, we need to make a number of qualifying assumptions. These are:

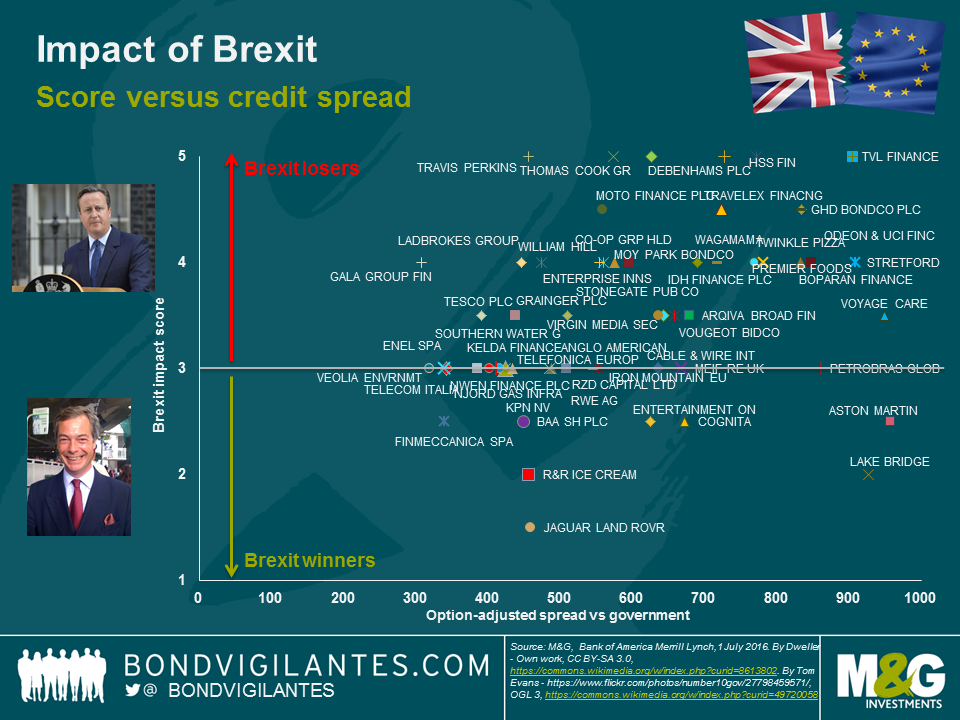

In this environment, domestically focused cyclical businesses that source their inputs from overseas are the most vulnerable (e.g. clothing retailers). Whereas, exporters of goods and services to non-EU markets may actually see a small benefit (e.g. educational service providers). The below chart plots this impact on the y-axis using a (caveat: highly subjective) numerical score between 1 and 5 (with 1 being the most positively impacted, 5 most negatively and a score of 3 denoting little or marginal impact). Current credit spreads are on the x axis to put this all in a relative value context. It should be noted that financial and distressed credits have been excluded, and of course we need to remember that spreads are a function of many other factors than purely Brexit.

We can draw a few interesting inferences from the above analysis. Firstly, most of the issuers will see a negative impact, while the number of companies that could benefit from Brexit constitutes a small minority. Secondly, when relative value is taken into consideration, the potential “winners” that trade cheaply are not without other risks. For example, Aston Martin (ASTONM) is a potential winner as a UK based international exporter and is not dependent on the European mass market. However, it has its own challenges as a small, capital constrained niche producer in a very competitive market. Brexit is unlikely to outweigh existing challenges for the business. Finally, given the muted market reaction and the likelihood of some extended fundamental challenges, the more interesting strategy to take right now is to sell or reduce exposure to the potential losers. Whilst there may be some specific opportunities, the uncertain macro environment means it is difficult to get too bullish on sterling high yield at this point in time. We would want to see a further downward adjustment in valuations before we look to put capital to work.

A few of the M&G bond team recently attended the FT’s Festival of Finance. Known as the Glastonbury of the Financial World, M&G’s Anthony Doyle brought a camera crew along and interviewed a number of speakers on the day, including Michael Pettis (China expert), Steve Keen (of “Debunking Economics” fame), Alex White (political pundit from The Economist) and our own Jim Leaviss. Watch the upcoming videos to find out which expert thinks the Eurozone won’t exist in ten years, who climbed the highest mountain in Australia because they lost a bet on house prices, and who thinks that Theresa May will be the next Prime Minister of the United Kingdom.

Last year proved a tough year for investment grade corporate bonds, with credit spreads moving wider. Fast forward six months to today and the decision of the UK referendum to leave the EU is continuing to shake markets, with European credit spreads now even further elevated. It is nevertheless important to recognise that these bouts of volatility can however present buying opportunities as corporate bonds become more attractively valued. Many non-financial European corporate bonds in particular look set to be well supported going forwards, given the ECB’s early June commencement of corporate bond purchases as part of their QE programme.

Despite the headwinds faced by the UK as it works to disentangle itself from the EU over the next couple of years, a glimpse back at the last twenty years demonstrates how the UK corporate bond market has evolved to present an interesting investment environment today.

In this edition of the M&G Panoramic Outlook, Richard Woolnough – fund manager of the M&G Optimal Income Fund, M&G Strategic Corporate Bond Fund and M&G Corporate Bond Fund – explains how the UK corporate bond market has diversified sufficiently over time in order to challenge the traditionally simplistic view of fixed income investing. Richard compares the UK with the US, Europe and equity markets, exploring the range of opportunities that the UK corporate bond market has to offer global investors.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.