Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

In 2013 I blogged about how financing conditions had tightened aggressively for small and medium sized corporates (SMEs) in peripheral Europe. Three years later, we’ve seen the introduction of targeted longer-term refinancing operations, QE, negative deposit rates and other efforts towards creating a financially united, cohesive, European banking union. Now feels like a good time to revisit this topic in order to assess whether credit lending activity has improved for these small businesses which, in spite of their size, are essential contributors of growth and job creation to the euro area economy.

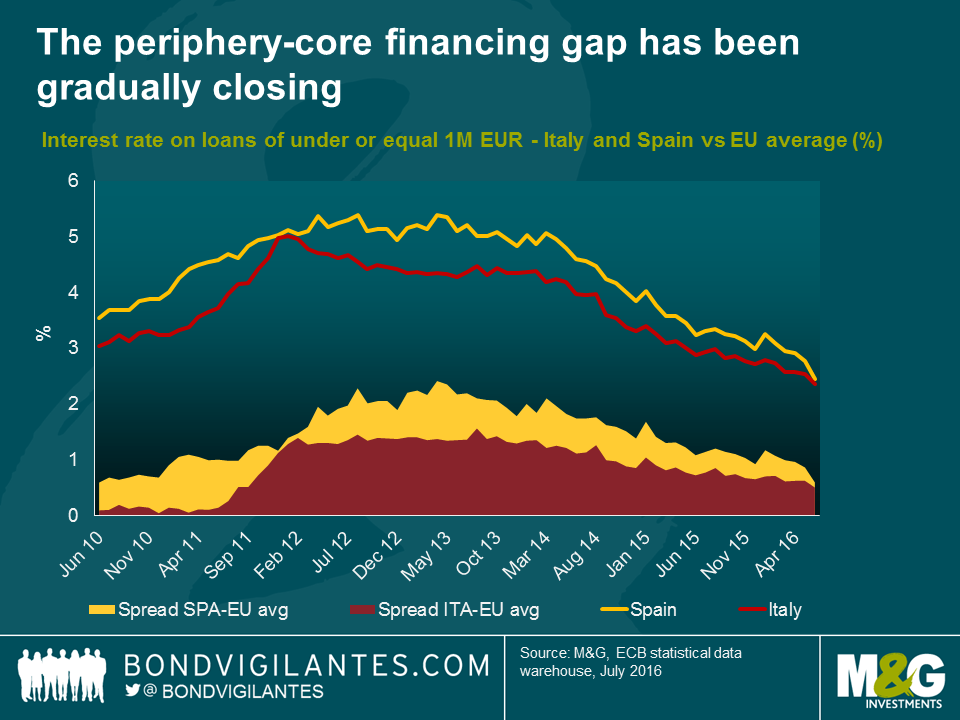

An assessment of loan interest rates could give an indication of the state of the European credit system. Back in the spring of 2013, struggling Spanish and Italian SMEs faced lending rates of 5.4% and 4.3% respectively, compared to the EU-wide average of just under 3.0%. The following chart demonstrates how the financing gap with the rest of Europe has been gradually closing with risk premiums having shrunk by 157bps and 85bps since March 2013. For Spain alone, this represents a decrease in funding costs of 52% over this period and 24% in the last 12 months alone. This improvement in peripheral SME lending rates mimics the recent trend observed in their sovereign funding costs. Continued progress towards the formation of a European banking union, some further relaxation of monetary policies, the ongoing banking sector restructuring efforts, and a revived domestic demand for credit have all been key drivers for the general improvement in investor confidence.

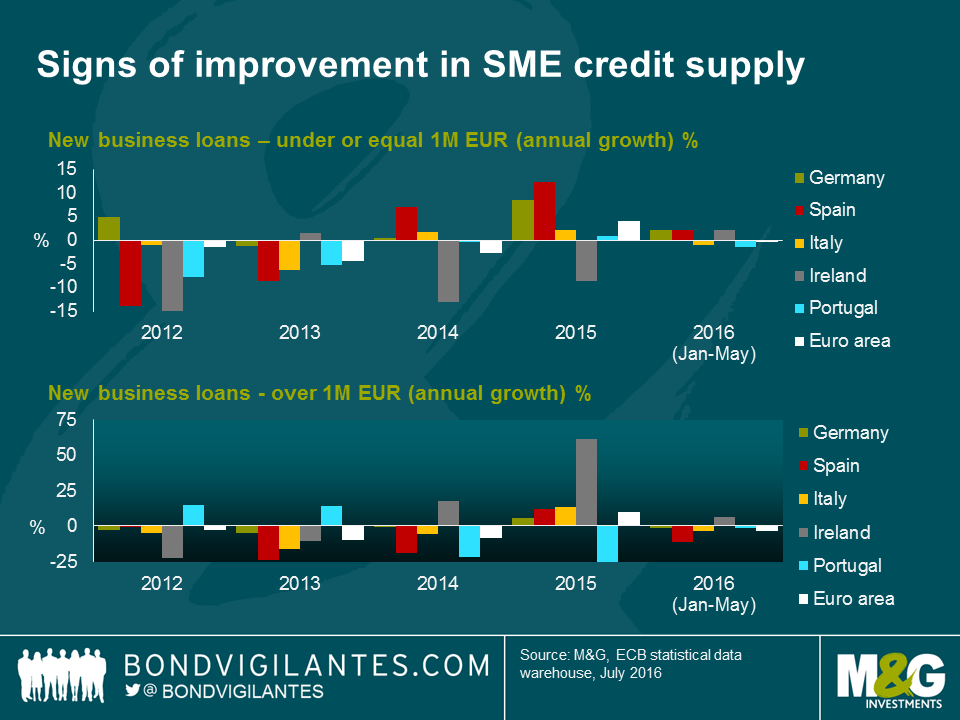

So funding is cheaper, but are SMEs utilising this? Since 2015, bank lending volume activity to SMEs (measured by new business loans worth less than 1mn EUR) has been on a rising trend. The chart below depicts annual credit lending growth rates across Europe and illustrates how the recovery in credit supply has been particularly strong in Spain, with annual lending activity growing by 7.1% in 2014 and 12.4% in 2015. Turning our attention to bank loans for larger size companies (i.e. represented by loans worth more than 1mn EUR), closer analysis reveals that lending activity has lagged that of smaller transactions (Ireland represents an interesting exception to the trend in 2015 where Irish banks increased >1M EUR corporate lending by over 60%). On the whole, a pick-up in demand did not fully materialise until 2015 and has since dropped in 2016. This could perhaps be explained by the ECB’s recent decision to enhance their asset purchase programme so as to include private corporate debt; the bigger companies with access to international financial markets have willingly taken the opportunity to substitute costlier bank lending for bond issuance at historically low interest rates.

While signs of improvement in the supply of credit have emerged, there is still some way to go. The smooth working of the transmission mechanism is of central importance to facilitate SME access to funding and it is therefore encouraging that some EU institutions have recently stepped up their efforts to address this problem. Financial innovation is welcome (to better allocate funding) and the promotion of measures that foster enterprise growth will be key to opening up alternative sources of funding (i.e. private equity, venture capital, wholesale markets). The rapidly developing FinTech or Crowdfunding industries are prime examples of incipient forms of SME lending. Progress from here will be beneficial; not only to break the strong dependence on banks, but to strengthen SME’s resilience in future economic downturns.

Now that the Bank of England has commenced purchases of gilts and committed to a programme of corporate bond buybacks, alongside similar measures being presently undertaken by the ECB, it is worth taking a step back and thinking about valuations in sterling fixed income.

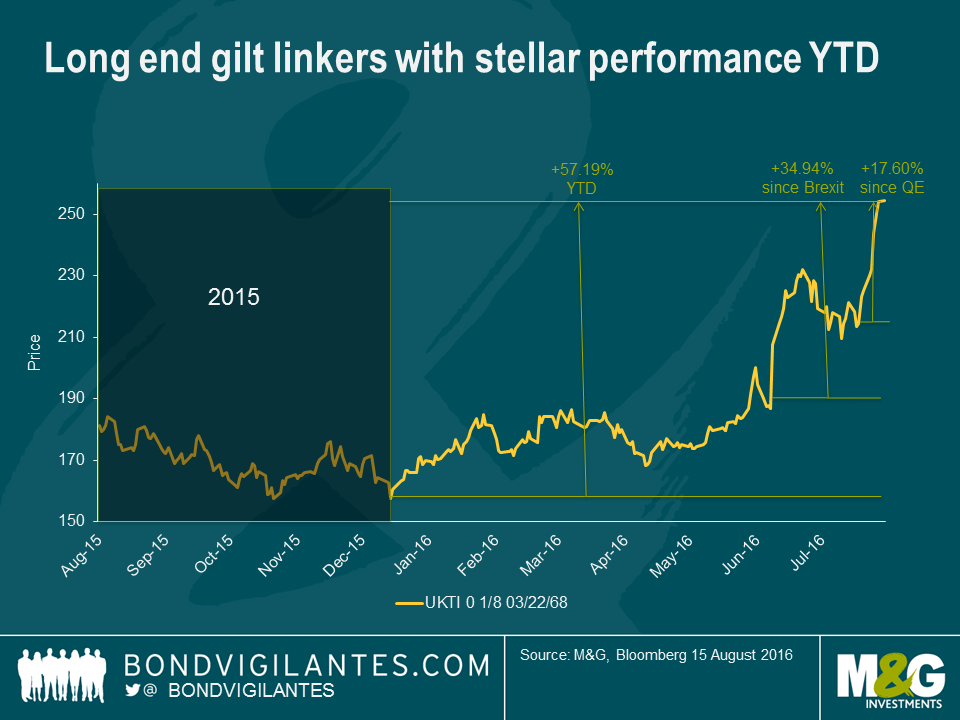

Let’s take a brief look at what has happened so far in 2016 in government bonds. The ultra-long conventional gilt has returned a staggering 52% this year. Since the result of the referendum became clear, the bond’s price has increased by 20%, and in the couple of weeks since Mark Carney announced the Bank of England’s stimulus package, the bond’s price has risen by a further 13%.

But this is not even the top performing government bond of 2016. That mantle goes to the 2068 index-linked gilt, which has seen its price rise by 57% year-to-date, by 35% since the vote to exit Europe, and by 18% since further quantitative easing was announced by the central bank. Interestingly, too, the superior price action of the index-linked bond has occurred not as a result of rising inflation or expectations of inflation; instead it has been in spite of significantly falling inflation expectations so far this year. The driver of the outperformance is solely due to the much longer duration of the linker. Its duration is 19 years longer than the nominal 2068 gilt, by virtue of its much lower coupon!

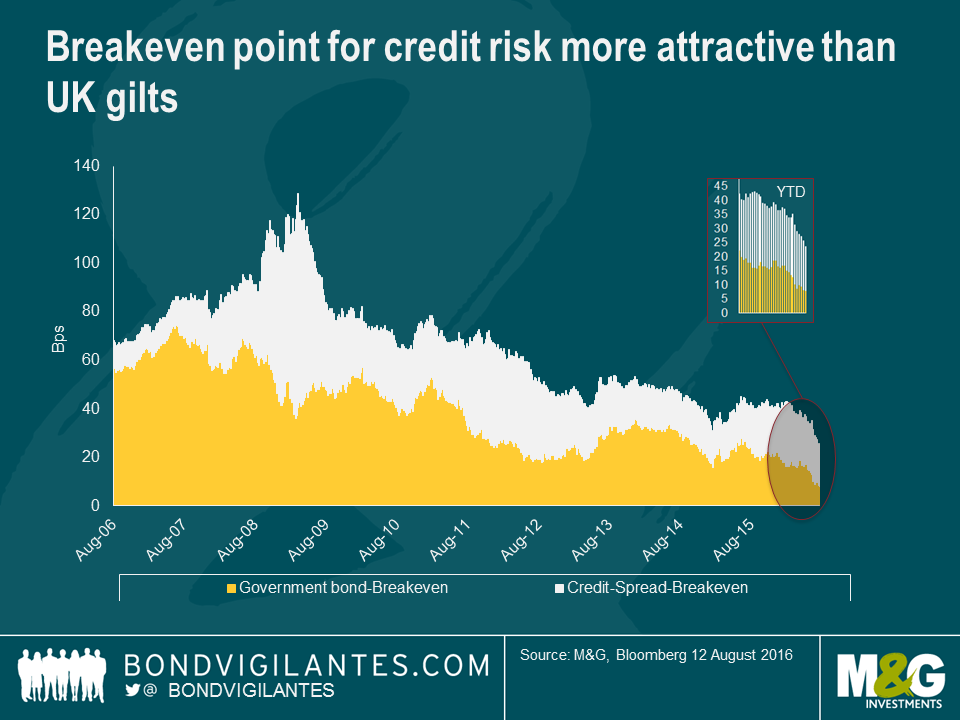

When you buy a corporate bond you don’t just buy exposure to government bond yields, you also buy exposure to credit risk, reflected in the credit spread. The sterling investment grade sector has a duration of almost 10 years, so you are taking exposure to the 10 year gilt, which has a yield today of circa 0.5%. If we divide the yield by the bond’s duration, we get a breakeven yield number, or the yield rise that an investor can tolerate before they would be better off in cash. At the moment, as set out above, the yield rise that an investor in a 10 year gilt (with 9 year’s duration) can tolerate is around 6 basis points (0.5% / 9 years duration). Given that gilt yields are at all-time lows, so is the yield rise an investor can take before they would be better off in cash.

We can perform the same analysis on credit spreads: if the average credit spread for sterling investment grade credit is 200 basis points and the average duration of the market is 10 years, then an investor can tolerate spread widening of 20 basis points before they would be better off in cash. When we combine both of these breakeven figures, we have the yield rise, in basis points, that an investor in the average corporate bond or index can take before they should have been in cash.

With very low gilt yields and credit spreads that are being supported by coming central bank buying, accommodative policy and low defaults, and a benign consumption environment, it is no surprise that corporate bond yield breakevens are at the lowest level we have gathered data for. It is for these same reasons that the typical in-built hedge characteristic of a corporate bond or fund is at such low levels. Traditionally, if the economy is strong then credit spreads tighten whilst government bond yields sell off, such as in 2006 and 2007. And if the economy enters recession, then credit spreads widen and risk free government bond yields rally, such as seen in 2008 and 2009.

With the Bank of England buying gilts and soon to start buying corporate bonds, with the aim of loosening financial conditions and providing a stimulus to the economy as we work through the uncertain Brexit process and outcome, low corporate bond breakevens are to be expected. But with Treasury yields at extreme high levels out of gilts, and with the Fed not buying government bonds or corporate bonds at the moment, my focus is firmly on the attractive relative valuation of the US corporate bond market.

Guest contributor – Mark Robinson (Financial Institutions Analyst, M&G Fixed Income Team)

The Bank of England recently announced two new measures focussed on the banking sector, which are primarily designed to improve monetary policy transmission from banks to households and corporates and, indirectly, are probably intended to stimulate loan growth. In this blog post, I’ll examine these actions more closely, and assess the likelihood of their success.

Firstly, a quick primer on the new measures: the Term Funding Scheme (TFS) allows banks and building societies to borrow four year money at “close to” the BoE base rate. Banks must maintain or increase lending volumes; else face a penalty funding cost of at most base rate + 25 basis points. There is, therefore, more than a hint that this arrangement is, indirectly, intended to encourage the banks to keep lending. The Monetary Policy Committee estimates that initial drawdowns could, theoretically, be as much as £100bn, funded by money creation as part of the Asset Purchase Facility.

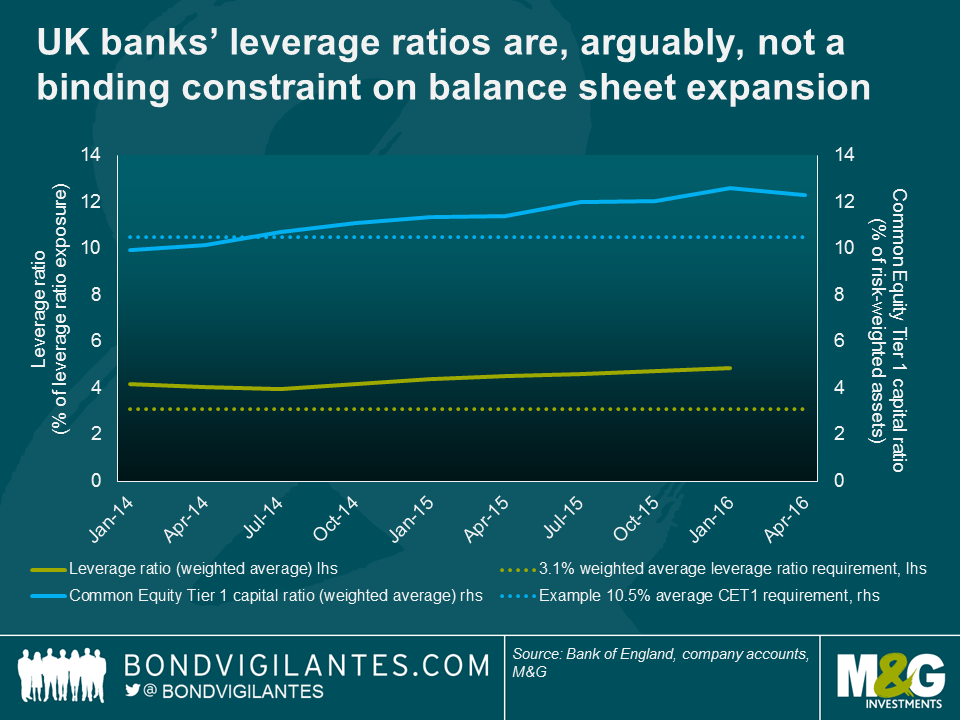

The second new measure is the exclusion of central bank reserves from the leverage ratio exposure calculation. This comes into place with immediate effect and, in theory, could encourage banks to increase leverage going into the expected economic downturn. Conscious of this risk, the BoE’s Financial Policy Committee will consult on the leverage ratio next year, and will likely increase the requirement (or its buffers) so as to neutralise the impact of the initial relaxation. Why go through this process at all, then? To remove the effective leverage penalty of holding central bank reserves, and therefore encourage the banks to use the TFS in the first place. The leverage ratio is also not a binding constraint on bank lending, something that can be illustrated using the following graph.

In the above chart, the important illustration is the difference between each curve and its respective minimum requirement (represented by the dotted lines). At an average of 4.9%, the major UK banks’ leverage ratios are already a fairly significant 58% above the average requirement of 3.1%. In comparison, the average 12.3% common equity capital level is only 17% above an assumed 10.5% requirement. The straightforward conclusion is clear: leverage, although arguably high, is not a binding constraint on bank balance sheet expansion, nor on lending. Any constraint on lending comes partly from a lack of high quality equity capital, relative to the higher risk-weighted capital requirements. Therefore, as the FPC also highlight, relaxing the leverage requirement won’t encourage an increased supply of bank loans, but measures such as relaxing the capital requirements (e.g. the removal of the counter-cyclical capital buffer, as announced in the July Financial Stability Report) should be a little more effective.

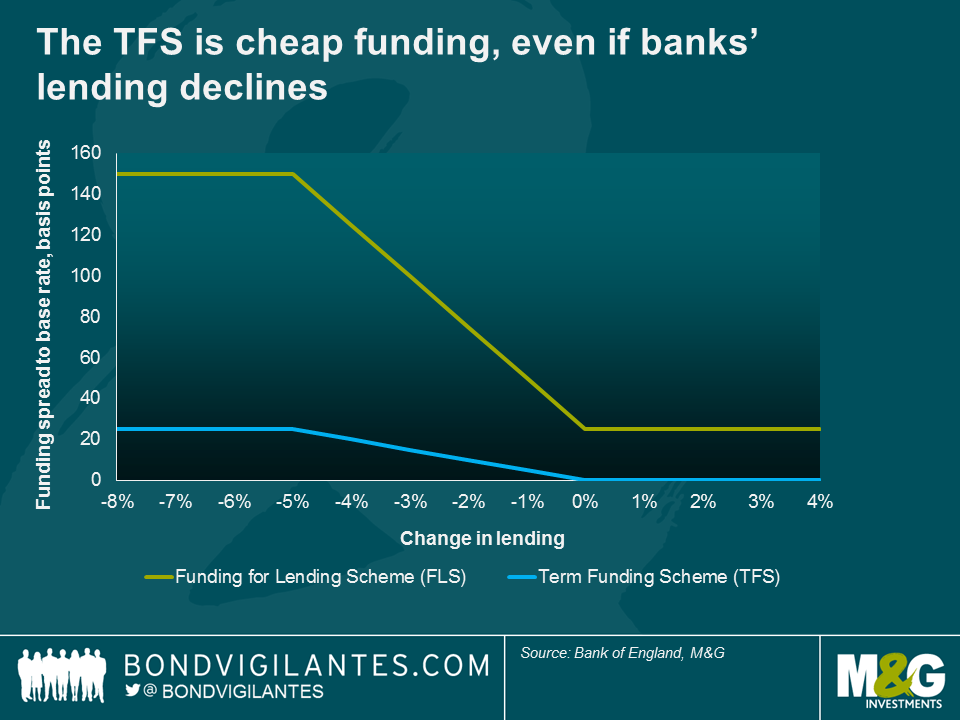

Having established that the leverage ratio adjustment seems to be designed almost entirely to encourage banks to use the TFS, let’s take a better look at this facility and its potential users. A closer examination raises a couple of problems. Firstly, we know from the major banks’ disclosures and liquidity coverage ratios that they already have fairly large amounts of cash liquidity on their balance sheets, which they are unable to put to work as loans; in part, because of the capital constraint mentioned above. The FPC highlight that the major UK banks have £350bn in central bank reserves alone, plus additional cash deposited at other financial institutions, and high quality government bond holdings. Therefore, unless they are able to quickly roll off older, more expensive funding, the UK banks simply might not want or need the extra TFS cash on offer. Secondly, as per the chart below, the penalty is not large for a bank that uses the TFS, and subsequently allows its lending to decrease: being charged base +25bp for four year funding is still cheaper than issuing a covered bond in GBP (the benchmark sterling four year swap rate is at 44bp at the time of writing), and retail savings of this tenor would cost a bank about 1.5%. On the plus side, as per the MPC’s main intention, if banks use the TFS, the monetary policy transmission mechanism should be more effective, since banks (especially small banks and building societies) have less of an excuse not to pass on the rate cuts to borrowers whilst being able to preserve their net interest margins. Lower loan rates naturally have an important positive spillover effect to consumption and confidence.

And it is this confidence that is key to the other essential element of the lending equation: the demand for loans from corporates and households. Here, the picture is weak, with the BoE’s own credit conditions survey portraying a drop in the perceived demand for corporate credit, even before the EU referendum result. Data points since then indicate falling production and confidence levels, which will likely cause loan demand to fall. The previous Funding for Lending Scheme didn’t receive much in the way of usage in its latter, SME lending, guise, with banks anecdotally citing a lack of demand for SME loans as reason not to draw down on the scheme. And, as Jim blogged about here, the BoE’s corporate bond purchases will likely make it more desirable for large corporates to borrow from the bond market; potentially reducing the demand for bank loans further still.

In summary, there are persuasive arguments that both the supply side and demand side of bank credit provision remain suppressed. As well as focussing on new banking sector policies and their implications, it’s equally important for us to keep asking the bigger picture questions: from a financial stability perspective, is it wise to indirectly encourage the banking sector to increase lending going into an economic downturn? Is the UK economy too reliant on credit, and does it need a structural adjustment, rather than its banks being used as a policy tool? Or, if the authorities don’t want to tackle the economy’s credit binge, should they do more to encourage direct or indirect lending to consumers and SMEs from asset managers and insurers instead of banks? These are questions that may become more pressing as monetary policy, and banking sector credit creation, start to reach their limits.

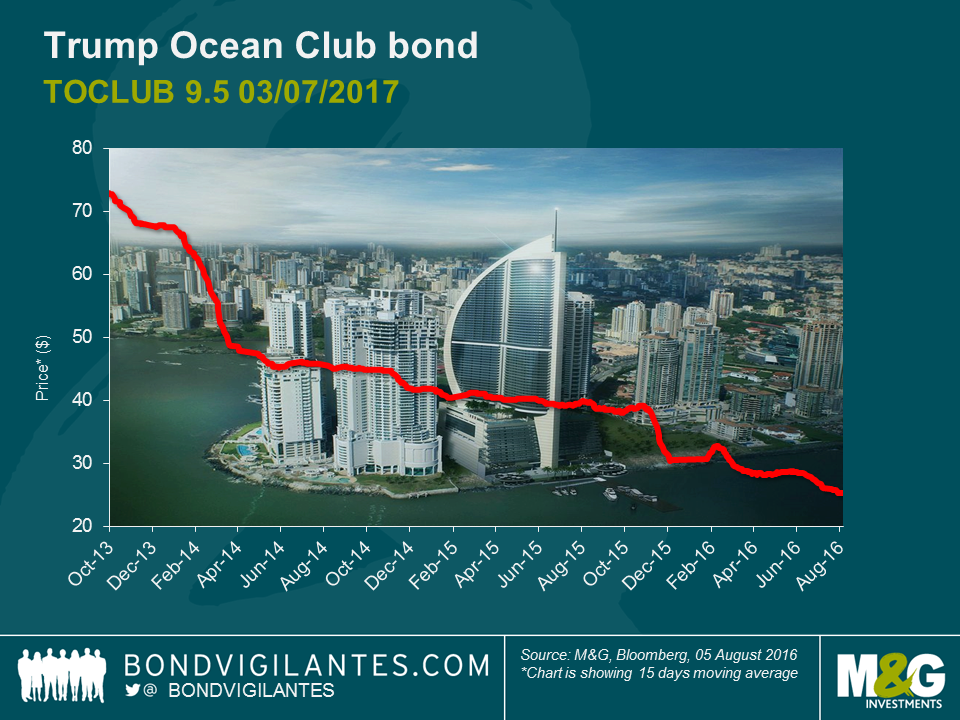

Earlier this year I gave a top-down macro assessment of Trump’s potential impact on Latin American remittances, should he become President. As the race continues, I now take a bottom-up micro view and assess Trump’s potential impact on an individual bond issue associated with the Trump Organization.

In 2007 the Panamanian real estate market was growing robustly, with prices experiencing double-digit growth. Given this backdrop, Trump Ocean Club’s $220 million bonds were issued in November 2007 through Bear Stearns and were initially rated Ba3 by Moody’s and BB by Fitch. The amount raised was used to finance the development of a high-end project in Panama, comprising of condominiums, a hotel, a casino and some shops and office space.

The developers – a Panamanian-Colombian controlled holding company – entered into a licensing agreement with the Trump Organization for the rights to use the Trump name for a fee of approximately $75 million (which was based on initial assumptions on gross sales). At the point of issue, the project was 64% pre-sold and it was expected that the rest would be sold by 2010. Given the timing of events, however, various factors contributed to difficulties. First and foremost was the US real estate crisis and the aftershocks of the Lehman collapse, which spilled over to the region. Panama is a dollarised economy, but a material share of the committed buyers were from countries whose currencies depreciated significantly, including Venezuela, Colombia and Canada, which led to some buyers defaulting on their purchase agreements. As of early 2015, just 74% of the units were sold. In addition to the adverse macro backdrop, cost overruns ended up stretching the issuer’s ability to service the bonds.

The bond defaulted in 2012 and was exchanged for a new security with a maturity extension until 2017. The new bonds are in default again, though the issuer has made some interest payments and partial tenders at low prices. It remains quoted at distressed levels.

The Trump branding continues to be used, despite the fact that the issuer has not fully honoured its financial commitments (for the name licensing fee) to the Trump Organization and the matter is under litigation. The bond issuer evidently places great value on the Trump name (the prospectus highlights “a decrease in the perceived prestige of the Trump brand name…could adversely impact our ability to market and sell our products”, as the brand was intended to “enhance the marketing and sale of our real estate products to affluent individuals”). As such, Trump’s controversial statements through his campaign could arguably have a negative impact on the brand image, and potentially on the property valuations as end-buyers shy away from the Trump-branded development in favour of other developments in Panama City. This could potentially lead to a larger proportion of the units going unsold, or being sold to investors at discounted prices.

Meanwhile in the US, building on this idea, the app Foursquare has attempted to quantify the amount of foot traffic into Trump-branded US properties over the last 1.5 years based on data sourced from its users. Foursquare found that the market share of foot traffic to Trump US properties in 2015-16 has fallen compared to 2014-15 by approximately 10-15%, particularly among women and Democratic states, which displayed even more pronounced declines (they have adjusted the data to account for the relative number of visits to Trump-branded properties versus visits to competing properties, so it reduces one-off factors such as weather-related issues. They also looked at the absolute number of visits to measure if the decrease in Trump properties’ market share was not due to one-off increases of visits to competitor properties). While these statistics are far from scientific, they do provide some food for thought.

As always, avoiding tail risk underperformers at this part of the cycle (i.e. of rising corporate and sovereign defaults) remains key for long-term performance. Bond investors have an additional reason to keep an eye on Trump.

Guest contributor – Craig Moran (Fund Manager, M&G Multi-Asset Team)

The following blog was first posted on M&G’s Multi-Asset Team Blog, www.episodeblog.com. M&G’s Equities Team also regularly post their views at www.equitiesforum.com.

These are extraordinary times in financial markets. On a daily basis we are being bombarded with news headlines of political turmoil, market gyrations, forecasts of the un-knowable, and incomprehensible new technologies.

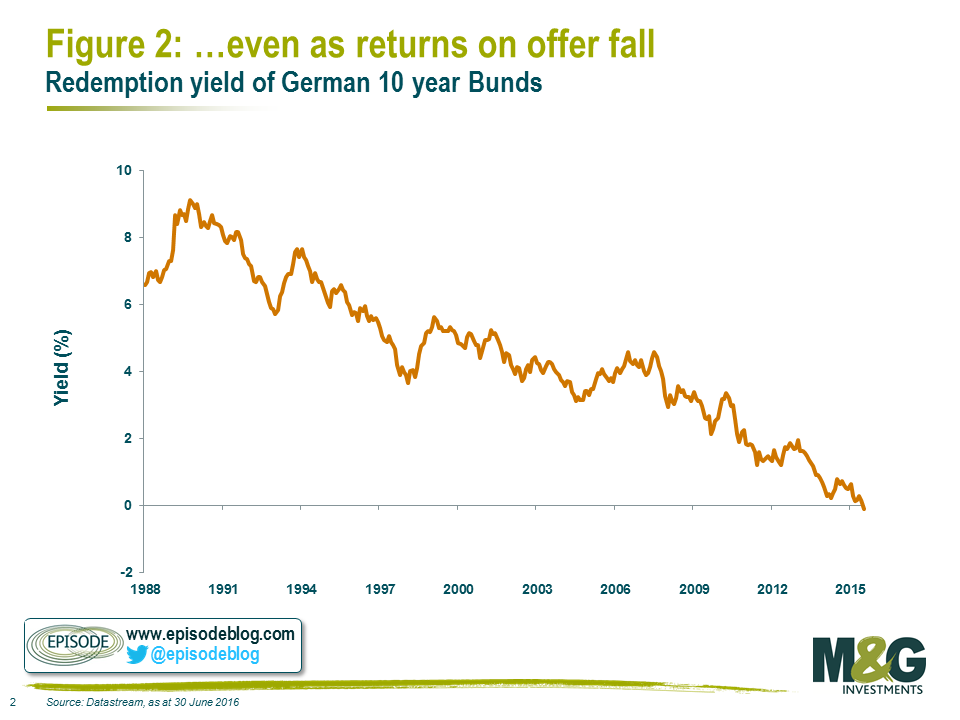

In amongst all of this chaos – one story that hasn’t attracted enough attention in financial markets was the news last week that the German government issued 10 year government bonds at auction with a negative yield. We also saw the first non-financial company (albeit state owned) issue bonds at a negative yield.

Whilst bond auctions don’t usually grab headlines, this does seem significant and as an event it perfectly encapsulates the risk averse environment that we now live in. While we’ve had bonds trade on the secondary market at negative yields, new issues with a negative yield only serve to emphasise the extreme nature of the current environment.

Bond terminology can be complicated, however to summarise the terms of this auction:

Our approach to investing involves seeking to identify and exploit markets behaving in an irrational manner. At first glance the transaction I’ve described above doesn’t seem like a rational one, but it’s important to challenge ourselves as well as the market to identify if we have a quarrel with its behaviour. So let’s examine the possible reasons why a rational person might engage in a transaction like this.

Rational reasons for buying 10 year government bonds on a negative yield

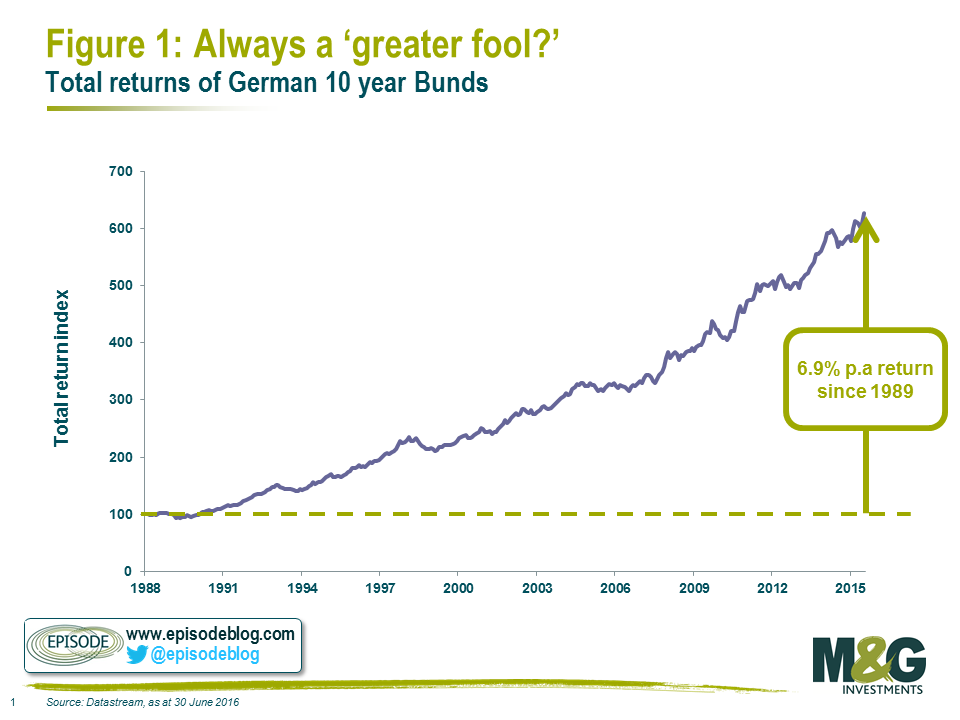

One of the main motivations for buying financial assets is to make a positive return, either in the form of income received, or to sell to someone else at a higher price. In the case of this particular transaction there is no income – so we can rule that out. The possibility of selling the asset to someone else at a higher price (a greater fool) is predicated on hoping that having accepted a guaranteed loss of over 50 cents over the course of 10 years, someone else will be willing to accept an even greater guaranteed loss over a shorter time period at some stage in the next 10 years. It’s betting that bond prices will hit ever higher highs, and yields hit ever lower lows.

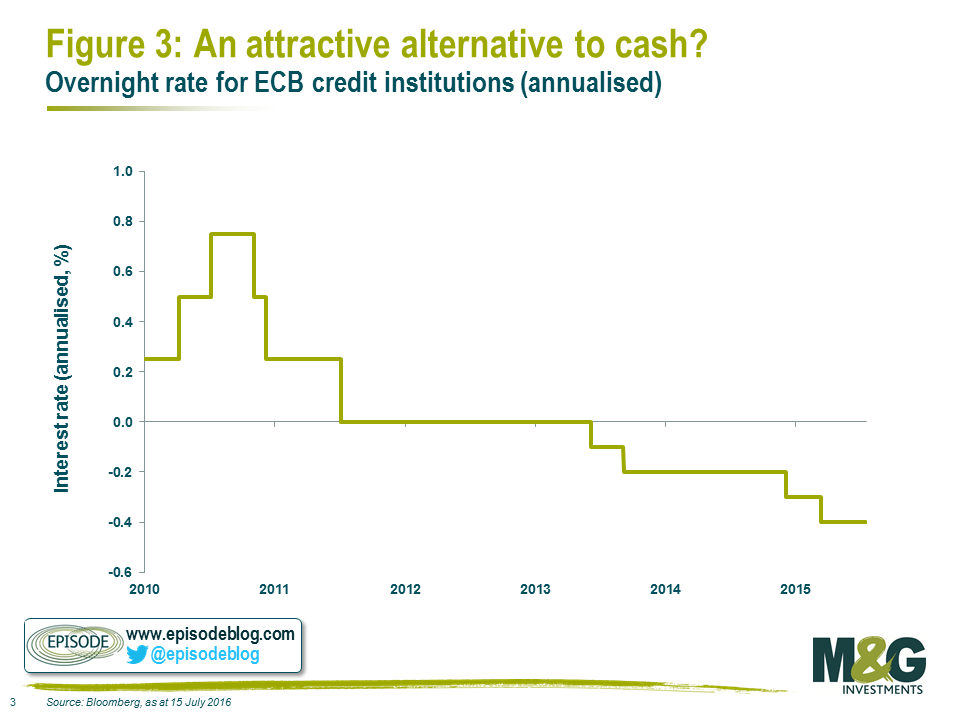

The current ECB Deposit rate is -0.40%, so storing your money overnight with a European bank will cost you an annualised rate of -0.40%. So suddenly the yield on the German government bond at -0.10% annualised doesn’t sound so bad, right? Especially if at some stage that overnight deposit rate might go even lower, although lately it seems policy makers seem to be growing weary of taking cash rates even lower.

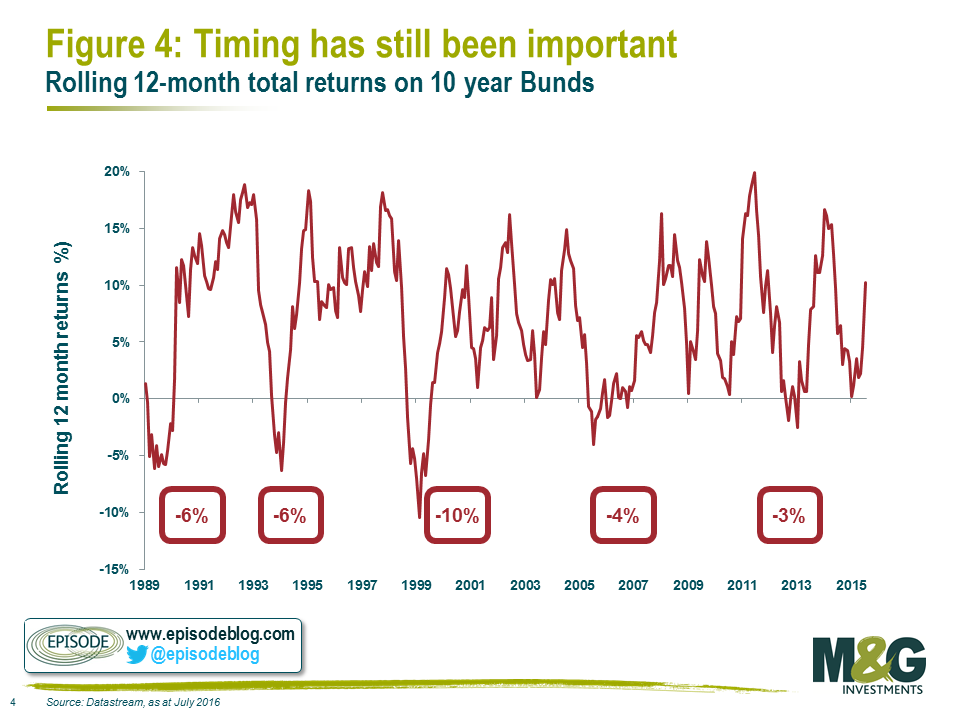

However, even though the bond offers superior yield (less bad at least), in order to guarantee this outperformance you need to hold the bonds for the full 10 years and have cash rates stay where they are now.

Should rates change, or you want access to your cash prior to the 10 year expiry, you are beholden to the market as to what price you will be able to sell your government bond for at the time you want to sell it. The bond has a duration of 10yrs, so should interest rates, or expectations of interest rates move only 1%, we could see a fall of up to 10% in the price of the bond.

Even in the 30 year bond bull market there have been plenty of occasions where transacting at the wrong time would have been an expensive exercise.

A cash proxy shouldn’t expose you to such timing considerations. Even if institutions are using the Bunds as places to store cash over the very short term, it seems a potentially expensive gamble to take given a modest yield advantage.

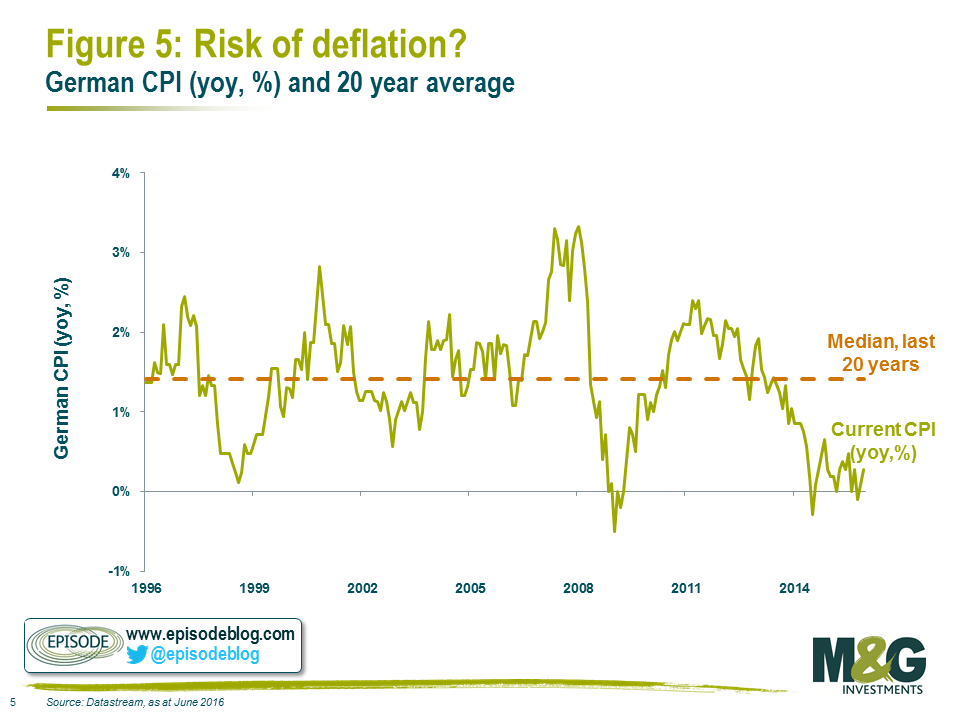

Conventional economic thinking suggests that money available to spend today is worth more than money available in the future, thus investors should be compensated for deferred consumption. If, however, you are in a regime of falling prices, it may be the case that 100 euros 10 years from now has more purchasing power than 100 euros today.

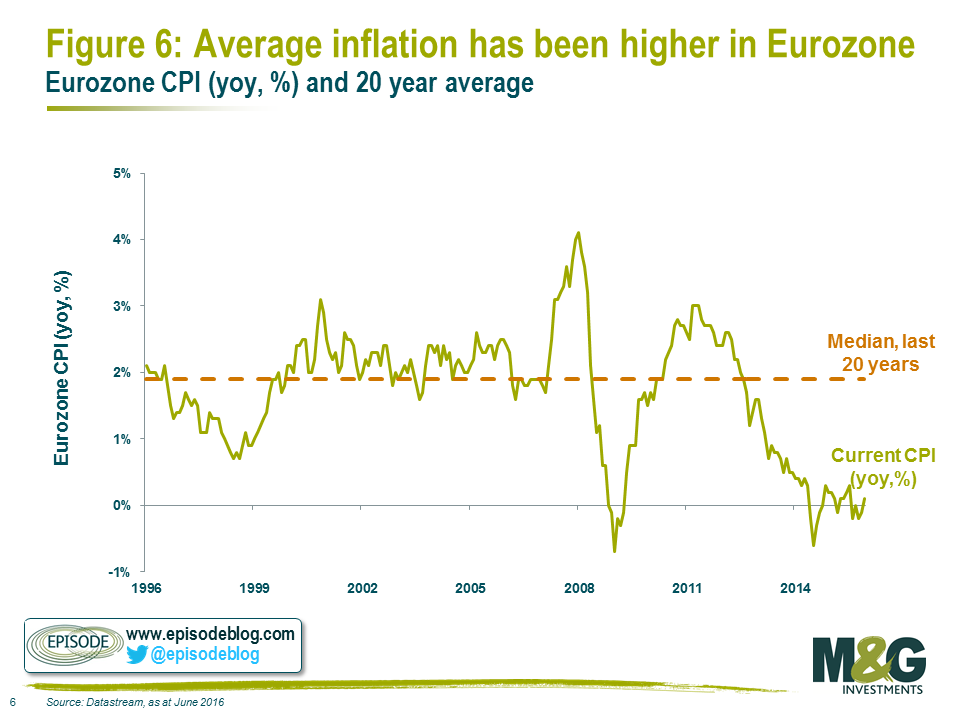

This is the chart of German CPI over the past 20 years. Despite multiple economic crises, it has spent very little time below zero (deflation), and averages around 1.4%.

Even looking from a Europe-wide perspective, the current level of inflation is lower (-0.1% versus +0.3% for Germany), though the long term average is higher at 1.9% (versus 1.4% for Germany).

Given the history of European inflation, and knowing that policy makers globally are doing everything in their power to avoid deflation (due to over-indebted balance sheets across Europe), a bet that deflation will persist over the next 10 years in order to compensate for negative yields today seems to be a bold one.

Other reasons for buying 10 year government bonds on a negative yield

Today’s regulatory environment continues to favour the purchase of government bonds vs other assets, however into the medium term it’s difficult to envision regulators encouraging banks and insurance companies to purchase assets with guaranteed negative returns. The fact that there’s a non price-sensitive/economically motivated entity temporarily distorting asset prices should always pique the interest of free market participants.

This is a combination of points 1 and 4. Currently there is a non price-sensitive buyer in the market for European Government bonds. Any unencumbered buyer of these bonds in the auction is hoping that the ECB will continue to buy these bonds at ever higher prices disregarding the economic payoffs of doing so.

Or could it be…

One thing that most market participants would agree on is the fact that there is a high probability that you will get your money back if you buy these bunds – albeit slightly less than you initially paid. It seems today the most likely reason investors are buying this bond (and many, many others at similar yields) is certainty. As we’ve stated before, return of capital has replaced return on capital as investors’ main priority.

This is where our biggest quarrel with the market lies. Safety, or certainty, like everything else – has a price. A guaranteed negative return on an asset held for 10 years seems like far too high a price to pay today for this perceived safety, especially given where the same ‘safe’ asset has been priced historically, and where it could trade again should risk preference or fundamentals change even modestly.

When it’s difficult to find any rational reason for buying something, should rational investors be thinking about selling it instead?

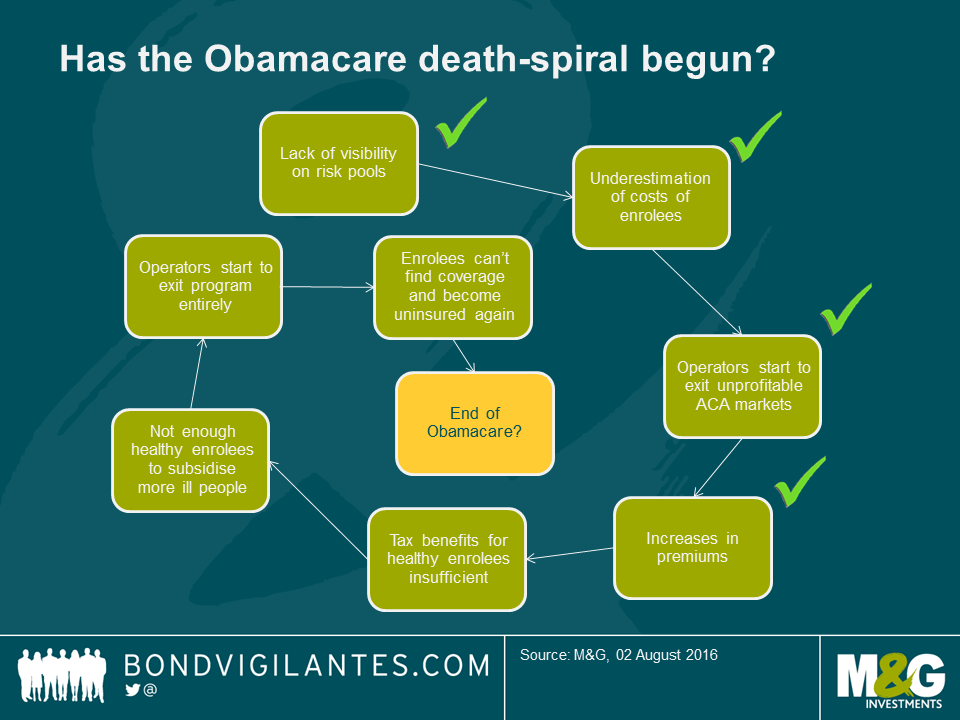

As the rhetoric of the U.S. presidential race heats up over the summer campaigning months, one topic we are likely to hear much on is health care. Health care in the U.S. is always a highly charged political subject, and now even more so with extra scrutiny on prescription drug prices and continued debates over the Affordable Care Act (ACA) or Obamacare. Obamacare is deeply unpopular with the Republican Party and Republican Party candidate Trump has called for its repeal if he is elected. We don’t want to discuss the politics of Obamacare, but could it fall over on its own?

Last week Humana (HUM), a large U.S. health insurance company, announced that it was exiting individual ACA insurance plans it was offering in eight states citing unprofitability. This follows United Health Group (UNH), another large health insurer, who announced in April they were exiting ACA plans in most states it operates in for similar reasons.

These ACA plans were one of the key mechanisms by which Obamacare sought to extend health coverage to the uninsured. Under the ACA, private health insurance companies like HUM and UNH offered coverage to the uninsured who would face tax penalties if they did not enrol (although in most cases they received tax credits to offset the cost of their premiums). However, the legislation mandated that insurance companies could not ask enrollees any medical history questions and they had to accept all enrollees, including those with pre-existing conditions. As such, the program was criticised on the basis that without knowing how sick the people enrolling in the plans were, it would lead to an insurance death spiral, i.e., not enough healthy enrollees subsidising the care of those actually filing claims.

A couple of large insurers exiting the program does not portend that a death spiral is imminent, or even likely, but it is a worrying sign and recently many companies have announced meaningful premium increases in their ACA plans. Politico’s Blog, The Agenda, sums up the issues facing the program nicely.

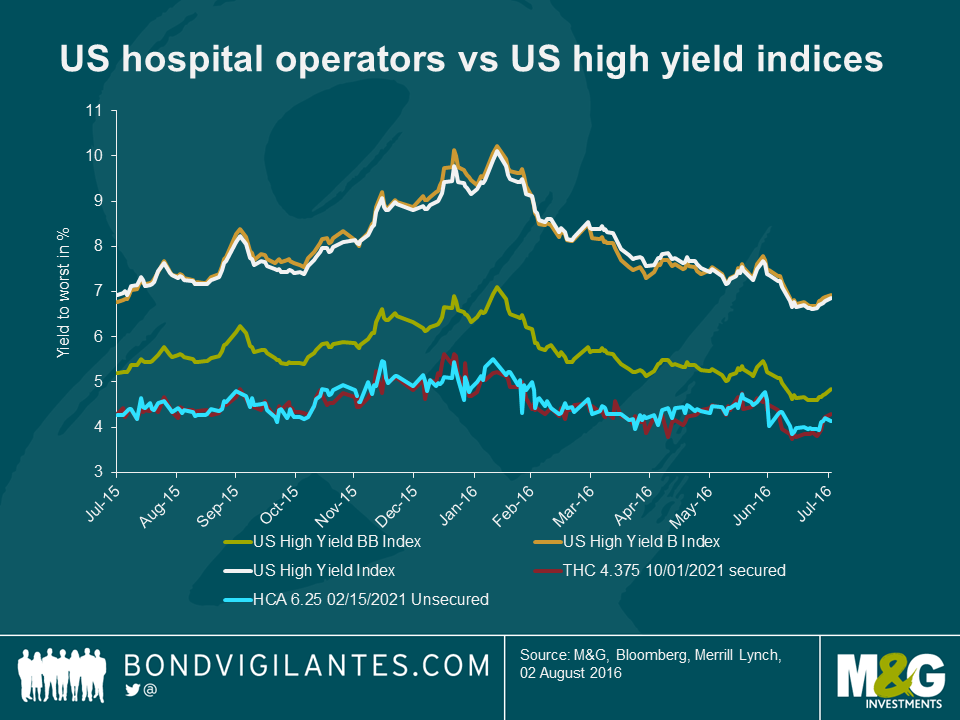

Death spiral or not, if more and more companies exit ACA plans or if enrollees drop coverage on their own due to rising premiums (and just pay the tax penalty), it’s possible that there would be a spike in the uninsured population at least in the near-term. The knock-on effect could impact U.S. for-profit hospital operators who were significant beneficiaries of ACA enrolment. With more patients having health insurance than previously, this reduced hospitals’ bad debt burdens and aided their profitability. Should that trend reverse these operators could face earnings headwinds.

This matters to high yield bond investors as health facility companies’ bonds represent a meaningful 5% portion of the Merrill Lynch Bank of America U.S. High Yield Index. And with over $43 billion in bonds outstanding, the bonds of just the top three hospital operators HCA Inc., Community Health Services (CYH), and Tenet Healthcare (THC) are the 2nd, 10th and 23rd largest issuers in the index, representing over 3% of the Index, meaning that they are likely widely held among investors.

These companies’ bonds have always been considered reasonably safe heavens as investors liked the defensive characteristics associated with health care companies in general. As such, these bonds typically trade inside the broader indices.

If investors start growing concerned about the earnings headwinds these companies could be potentially facing, they also need to weigh up if they are being adequately compensated at these levels. Now add to the mix the political rhetoric of the campaign and the impact on bond volatility. Surely if Trump surges in the polls, uncertainty surrounding the future of Obamacare will intensify regardless of what is happening with the ACA plans, and this could lead to volatility in not only hospital company bonds but many related health care companies as well such as insurers and pharmaceutical companies.

Post the Brexit referendum we are in an economic purgatory. The brexiteers are looking forward to a democratic led revitalisation of the economy, while the bremainers fear that the “little England” mentality will leave us isolated and depressed. Most people have an opinion, and the economic opinion that matters the most is that of the Bank of England (BoE). The market has absorbed the news of Brexit and adjusted: sterling down, foreign earning equities up, and UK government bond yields down to record lows.

The BoE now has the opportunity to publish its thoughts this Thursday on Brexit in its Inflation Report. The market is assuming that the Bank of England now has to act to prevent the severe crisis risk it outlined in previous press conferences. However as the UK is currently around two and a half years from departing the European community, the BoE has time on its side: half a year of pondering the implications of Brexit, and then two years of full membership to consider post-Brexit.

The first thing the BoE will consider on Thursday is where the UK economy was before the referendum. The answer is the economy had low unemployment, strong real wage growth, and a consumer boom as typified by the record trade deficit. Looking forward, the new government is likely to implement fiscal stimulus, the BoE may ease monetary policy through a combination of lower interest rates and unconventional methods, and the fall in sterling will provide an economic tailwind. In layman’s terms, we have a healthy economy, operating at near full capacity, that is about to be given a shot in the arm from a fiscal, monetary, and exchange rate perspective. On the negative side, the UK economy is going to experience some potential slowdown in two and a half years’ time, as barriers to trade with our neighbours are likely to be implemented. With some associated falls in potential capital expenditure and consumer confidence before this.

The tailwinds look capable of more than matching the headwinds over the next two years. Indeed, if you are a business and have any spare capacity that needs to be used ahead of the Brexit deadline (for example a UK based car manufacturer), the logic should be to produce at full speed before the trade barriers are increased, especially given the fall in sterling. It looks like UK exporters are in a great position until the spring of 2019.

The BoE’s own forecasts pre-Brexit show inflation returning to or above target over the next couple of years. The problem the BoE now faces is that the benefits of Brexit (looser fiscal policy, looser monetary policy, and the lower exchange rate) will occur well before the potential headwinds in 2019. The monetary authorities like to work in a counter cyclical fashion, however the economic damage that could occur from the decision to leave could well be delayed. In fact acting aggressively early could well result in a mini boom, which will make the eventual delayed event of Brexit appear even more severe. For these reasons, the BoE should not be too aggressive in easing monetary policy on Thursday.

The chances of a recession and deflation in 2019 will depend on how the UK economy adjusts to its new role in the world. Or just maybe, in two and a half years’ time market mechanisms such as the exchange rate and the fact the UK has had time to prepare for leaving the EU will mean the market will be focused on new issues and not an event that could seem like a distant memory.

We have written about quantitative easing (QE) many times over the years, yet there remains more to be said: the great QE experiment is not yet over. Given the result of the EU referendum, speculation is rife as to whether the Bank of England will embark on another round of QE to stimulate the UK economy; arguably making this a good time to debate the efficacy of such strategies.

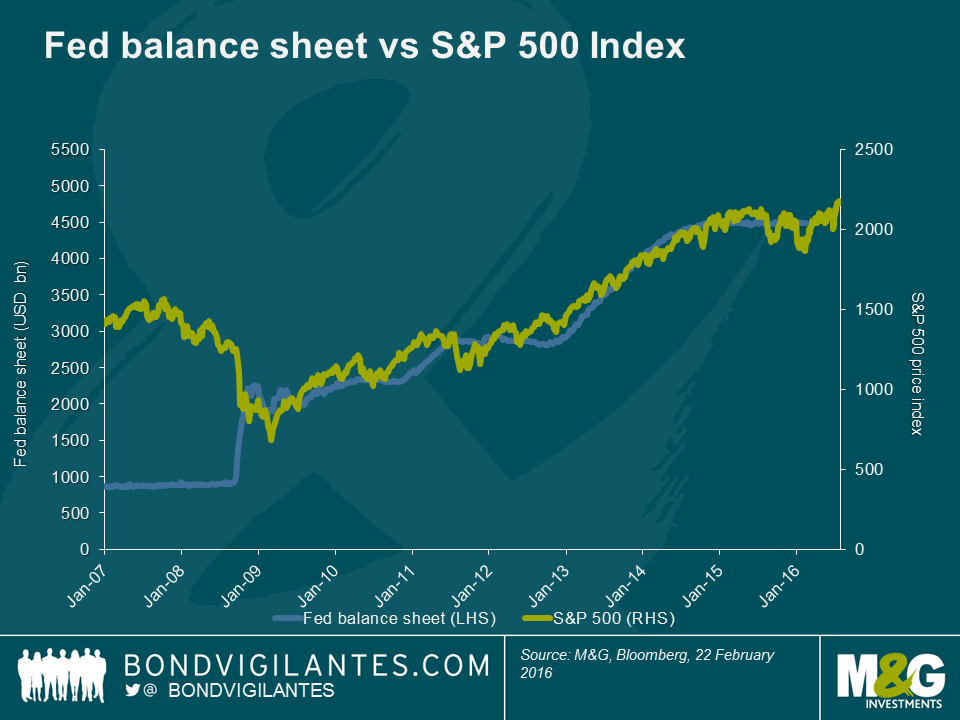

It’s safe to say that the most surprising aspect of QE has been the lack of inflation, but central banks which have undertaken – or are still undertaking – QE claim that it has worked by preventing deflation through portfolio rebalancing. The shift in funds into riskier assets has led to higher stock markets. My take on this? Central banks are over exaggerating their claims at best, or grabbing at straws at worst.

Let’s take the US model experience as an example. I agree that the Fed’s balance sheet and S&P 500 index have been positively correlated since 2009, but I would argue that the relationship is casual, not causal. The Fed announced its QE programme only after US stock markets had collapsed to cheap levels, and stopped it only once those markets had recovered. As such, the Fed seemed to use the S&P index as a temperature gauge for the economy (“the share price of the country” as it were), rather than the index appreciation being the direct result of the QE activity undertaken. QE started when stocks were cheap, and finished when they became fair value.

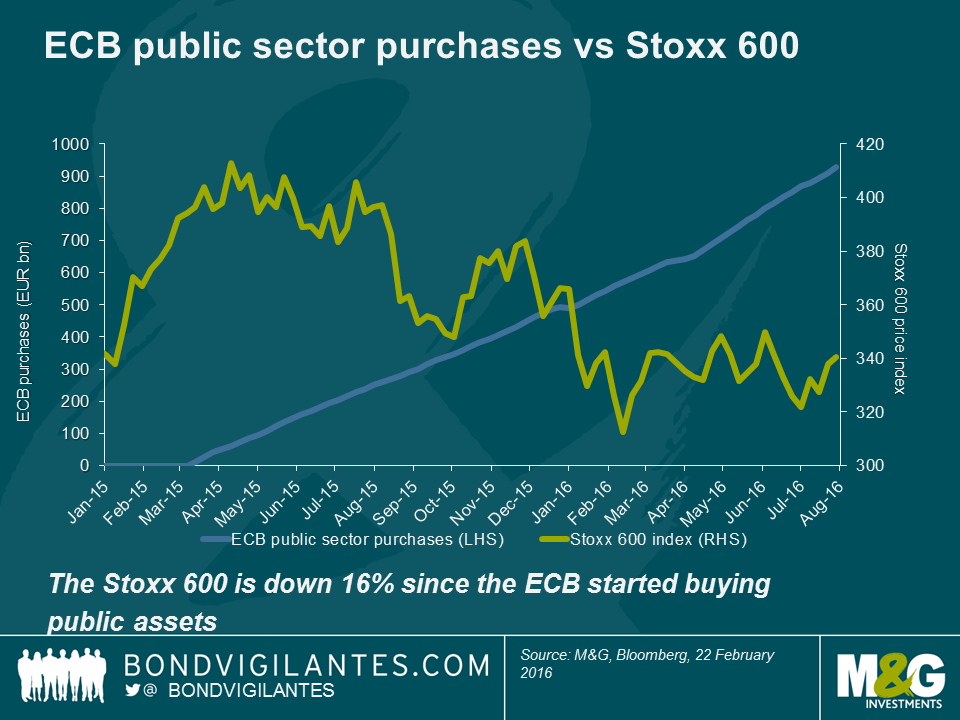

Not yet convinced? The above chart demonstrates a coincidental relationship, but what about other economies? The QE experiment in Europe was initiated in March 2015, a time when the Stoxx 600 equity market was much more buoyant, and not trading at distressed valuation levels. It seems ludicrous to argue that a causal link has been in play in Europe. This is illustrated below.

So what have we learnt? QE appeared positive for risk assets when their valuations were depressed in the US, but had little impact when equities were fairly priced in Europe. Because interest rates have already fallen to a large extent (thereby lowering the discount rate that equity investors use), investors will not be able to boost the present value of future cash flows. This means that it is difficult for equity market valuations to increase to the same extent as previously when yields collapsed. Given the sluggish economic outlook and potentially higher interest rates in the US, it is also difficult to argue that profits in the future will be much higher as well.

QE does have some economic effects; it’s just (I’m not ashamed to say) still difficult to discern just what these are. It hasn’t yet been inflationary (even though the basic principles of QE suggest that increasing the supply of money should reduce its value) and I believe that the link to stock market strength is somewhat illusory. Arguably, the greatest effect of QE has been the reduction in bond yields across the curve and not a portfolio rebalancing into riskier assets. In theory, the portfolio rebalancing effect is most powerful when investors view equities as an alternative to bonds. Given the difference in volatility characteristics of both asset classes, it is unlikely that this will ever be the case (some investors still choose to buy negative yielding fixed income securities for example). If the Bank of England is hoping that QE will prop up the UK economy and inflation through a causal link then the current economic data supporting this theory is mixed at best.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.