Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

The financial world is a scary place. Debt, disinflation and deteriorating growth have plagued investors over the past year, plunging bond yields into negative territory in a number of countries. Perhaps most frighteningly, it is now eight years since the financial crisis and central banks in the developed world continue to employ an ultra-easy monetary policy stance. With government bond markets currently resembling a freak show at an extended point in the economic cycle, the next global recession could be around the corner. There is no need to watch scary movies this Halloween, as the following makes for some frightening reading.

Developed market government bonds have been one of the best performing asset classes in 2016, confounding many predictions at the start of the year. In general, the right trade has been to own long duration assets, indeed the longer the better. Year after year investors predict that bond yields will rise and year after year bond yields make new lows. Of course, there are some very good reasons to expect this trend to continue.

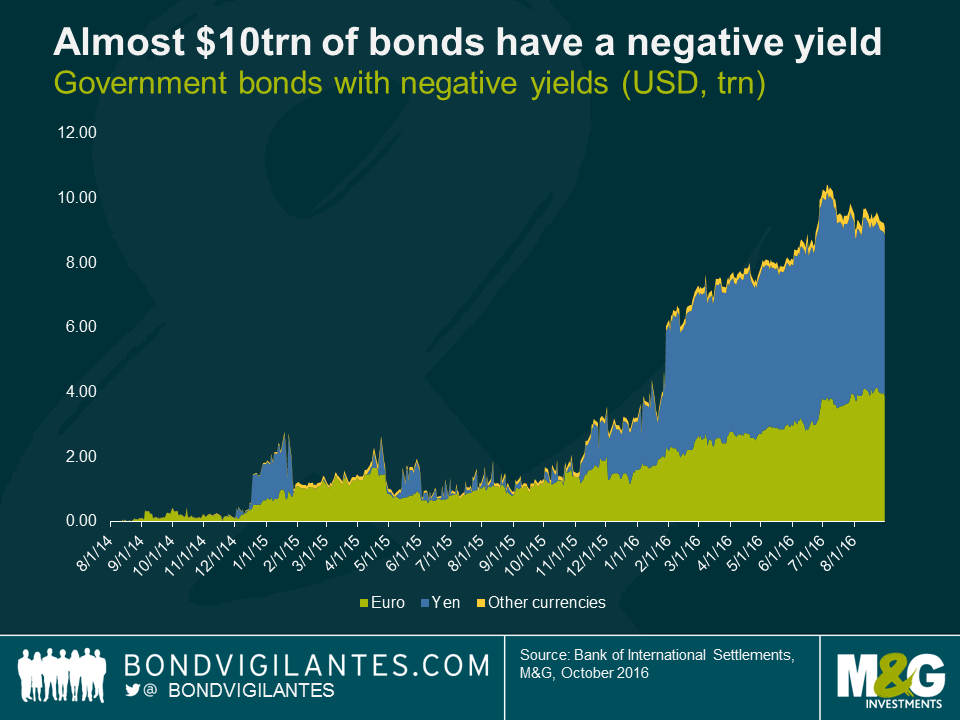

However, bond markets now expect that monetary policy normalisation won’t occur until some point in the distant future. Low inflation means that central banks continue to support their heavily indebted and ailing economies, resulting in almost $10 trillion worth of developed market government bonds trading with a negative yield. As a result, many companies – including banks – are struggling in this low (and negative) interest rate world. These companies are finding their existing business models challenged in an environment of low growth and tighter regulation. Pressures in the financial system are building, and it is unclear how these issues will be resolved.

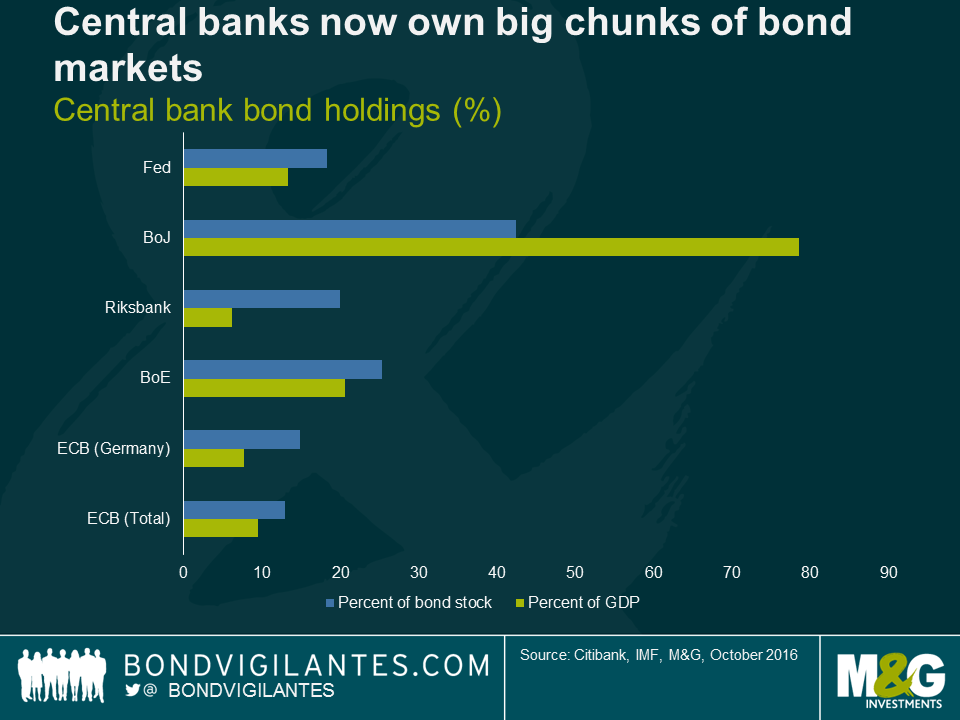

Central banks’ sizable purchases in government bond markets through quantitative easing means that term premiums (the extra amount that investors demand for lending at longer maturities) have been pushed further into negative territory. It was once inconceivable that investors would pay for the privilege of lending to a government. Now this phenomenon is commonplace not only in government bond markets but also for some recent corporate bond issuance.

It isn’t only central banks that are at the bond buying party. Demand continues to increase for long duration assets, from other large institutions like pension funds and insurance companies. The combination of central banks, pension funds and insurance companies has limited any sell-off in bond markets, reducing yields across the bond curve. Aging demographics mean that safe haven assets may continue to remain in demand, forcing investors into riskier assets if they want to generate a positive real return.

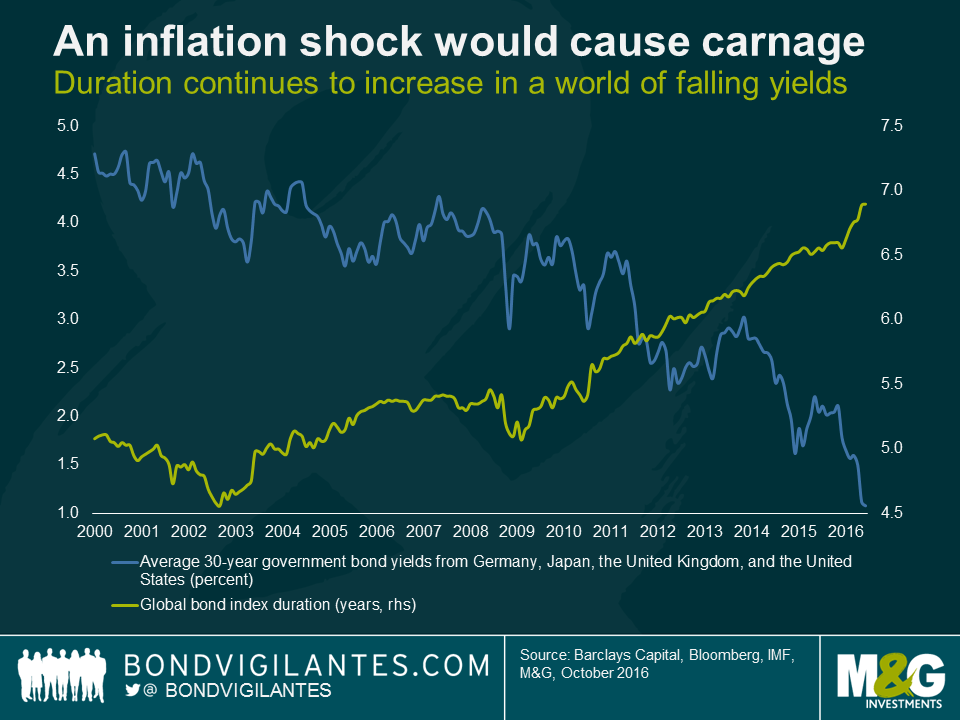

Despite the negative yield environment we now find ourselves in, how central banks react to the next inflationary shock will have huge ramifications for bond investors. With global bond portfolio duration close to 7 years, investors could face large capital losses if rates were to increase in a meaningful way. This raises a number of important questions. Will central banks hike rates in an environment of stagflation? How will politicians react when the paper losses on QE bought portfolios held at central banks are reported in the media? Could central bank independence come under threat? As many banks and insurance companies own long dated assets, will financial instability increase when long-dated bonds experience large capital losses?

Currently, the market is more focused on secular stagnation than inflationary concerns, but with oil up almost 100% from the February lows and trade protectionism starting to begin to carry favour in government buildings around the world, a global inflation shock might be closer than many currently expect.

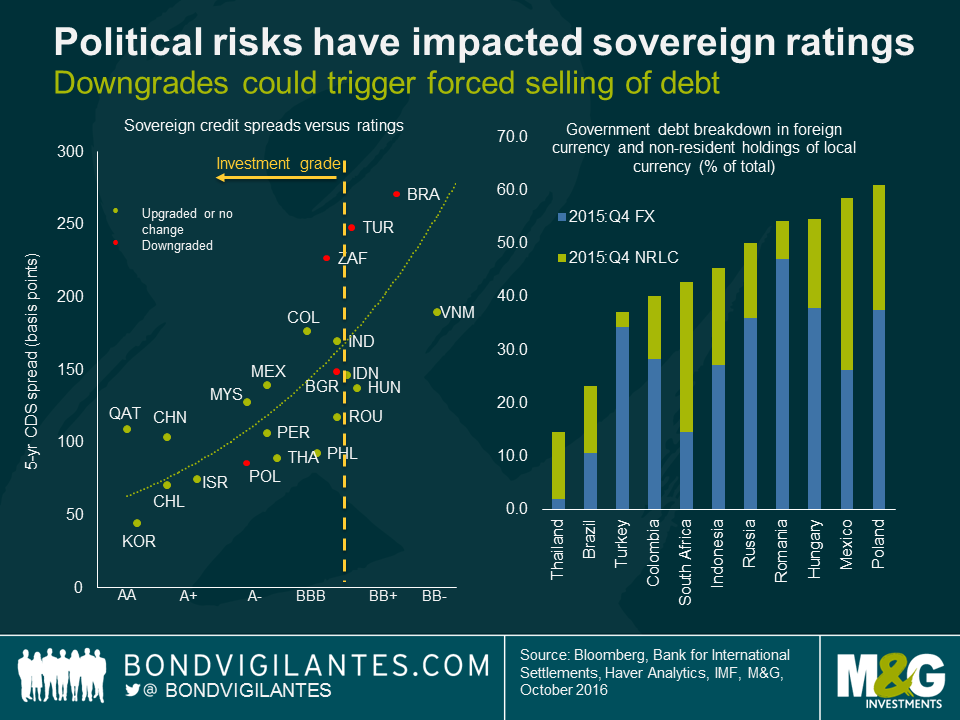

Several emerging market sovereigns have been downgraded over the course of the past year, with rating agencies highlighting political uncertainty as a major factor in the decision. The impact of the downgrade has been felt immediately, with heightened volatility in bond markets the result.

Large inflows into emerging market bond markets has left some countries vulnerable to increased political risks from abroad. Mexico is a good example given the current uncertainty surrounding the U.S. presidential election. Many emerging markets are also vulnerable should the US dollar strengthen, a possibility given the U.S. FOMC is by far and away the closest of any of the major central banks to hiking interest rates. An additional risk is the possibility of a large emerging market nation being downgraded from investment grade status, causing forced selling of hard currency debt by foreign investors.

The most dangerous four words in finance are “this time is different”. And when it comes to credit booms, they don’t tend to end well.

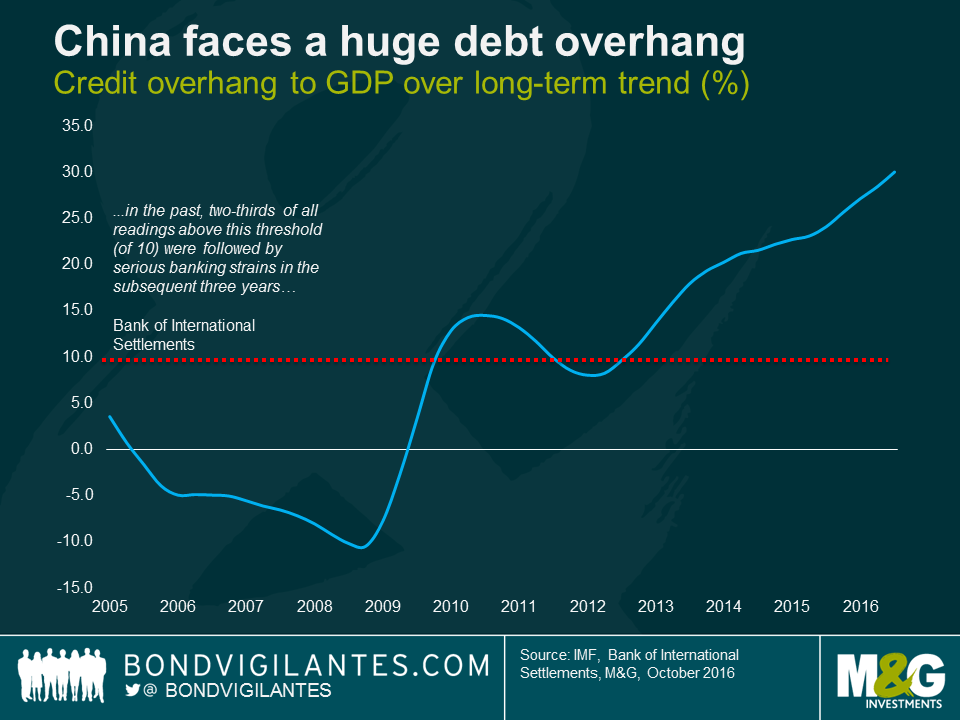

One measure economists look at to determine excess credit growth is a country’s credit overhang. This measures the difference between the credit-to-GDP ratio and its long-term trend. It has proven to be a reliable indicator, with the Bank of International Settlements stating that “in the past, two-thirds of all readings above this threshold (of 10) were followed by serious banking strains in the subsequent three years”. China’s credit-to-gross domestic product “gap” now stands at 30.1 percent, the highest for the nation in data stretching back to 1995, suggesting the banking system could already be coming under severe pressure.

Numerous warning signs are flashing amber or red in the Chinese financial system, given that huge swatches of renminbi have gone into financing large-scale real estate projects and new production capacity for industrial sectors of the economy. This toxic combination of high and rising debt in a slowing economy tends to lead to an economic deterioration. As authorities continue to chase economic growth, capital is funnelled into unprofitable projects and overcapacity. Eventually, prices begin to fall and borrowers face large capital losses. Additionally, much of the finance available for investment projects was made available through the shadow banking system, which is more susceptible to a sudden stop in capital flows and a run on deposits.

Happy Halloween.

This week on BVTV Nicolo Carpaneda discusses what’s behind the recent sell-off in government bond yields. He takes a look at some surprising updates from the US and asks the question: who is suffering one of the hardest recessions in history? Nicolo also previews the week ahead in the bond markets. Tune in to find out more. Happy Halloween!

This week on Bond Vigilantes TV:

Tune in for the charts and blogs that are making headlines in bond markets.

Last year we blogged with our key takeaways from the IMF and World Bank meetings and this year is no different. Claudia Calich and I tag-teamed between the Washington based events, participating in the many wide ranging discussions that took place, so we’re doing the same here. Claudia will be providing the emerging market coverage, while I share some insights from developed markets, alongside discussion on China.

1) China: Taking a backseat after driving markets last year

In contrast to last year, conversations on China stirred surprisingly little concern. After the large market movements and bouts of volatility experienced in August 2015 and earlier this year – triggered by China’s FX rebalancing, rising corporate defaults and accelerating capital outflows – the concerns about a “hard-landing” appear to have abated. Instead, much was made of the improvement in central bank communication and the currency having been relatively stable versus the target basket this year. Sentiment also remained positive regarding China’s rebalancing towards a service economy, which has been gaining traction, as the credit expansion and increasing consumption share of GDP has provided a floor to growth, offsetting any investment slowdown. This sentiment coincides with the uptick we’ve seen in the Li Keqiang Index this year (the oft regarded “better” proxy of Chinese economic growth).

The country is not without its foibles, but given that China has an array of policy tools, expectations are that these should alleviate any macro shocks. Policy will therefore focus on growth stabilisation in order to maintain momentum into the Party Congress leadership transition which takes place in October next year. After a period of stability, it is hoped that structural reforms (e.g. with respect to state-owned enterprises and banks) will take centre stage.

2) Japan: The ongoing broadening of QE

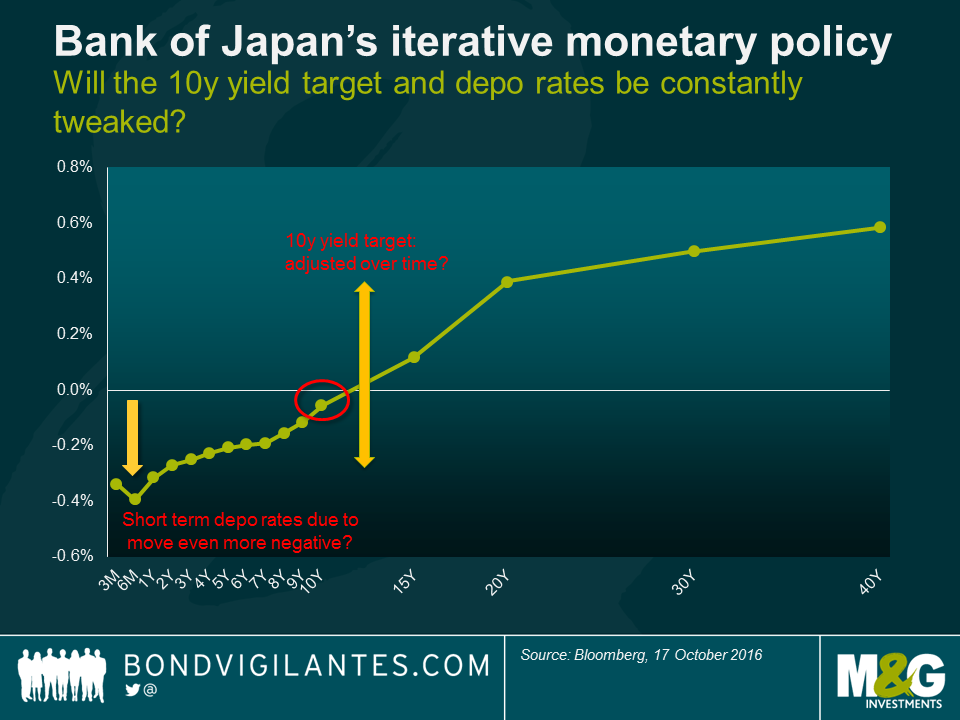

Discussions surrounding Japan focused on the efficacy of the newly unveiled “QQE plus yield curve control” policy, where the Bank of Japan is shifting focus away from the monetary base towards an aim to keep 10 year yields at around its recent level of 0%, as well as a commitment to overshoot its 2% inflation target. My gut feel is that the goalposts will continue to be a lot more flexible compared to the comparatively fixed targets of the western world. In pursuit of its objectives, I expect Japan’s monetary policy to continue to be a creative work in progress (we’ve already had Quantitative Easing, Quantitative and Qualitative Easing (QQE), QQE + Negative Interest Rate policy and now QQE + YCC). Indeed my main takeaway is that it’s all up for negotiation. The BoJ won’t sell JGB’s if it needs to drive the 10 year yield up, but will instead purchase less via its QQE programme. This suggests that the current target of ¥80tn of annual JGB purchases will have to formally change over time. Short term rates could be adjusted lower into negative territory should inflation expectations fall. It also felt as though the 10 year yield may be a moving target which evolves over time. The longer term aim is clearly to engineer a steeper yield curve, but it will be interesting to see whether the BoJ are successful, especially since it’s been difficult enough for the developed world to generate 2% inflation in recent years, let alone an overshoot.

3) UK: Uncertainty and politics dominate

If I was given a dollar every time I heard the political buzzwords “Brexit” and “Trump”, I’d have returned with a lot more than a $2 tin of IMF branded mints. It is however understandable that these were the issues at the forefront of investors’ minds, especially since the meetings took place during the final month of the US election campaign and at a time where sterling lost 2.5% of its value against the dollar (given Theresa May’s conservative party conference comments resulting in heightened fears of a “hard Brexit”, or as HSBC preferred to call it: a “continental Brexit” versus a “full English Brexit”). The concern that the UK might not get its way in negotiations is a view I’m sympathetic to. Certainly, discussing this issue in Washington meant that I could get more of a birds-eye, non-UK view. Stating it simply, the UK will be negotiating against a bloc of 27 EU member states and if the UK is to be granted any type of concession, unanimity amongst the 27 is required; this is a high hurdle. Other discussions concerned the potential period of stagflation the UK may find itself in, given the 18% deprecation we’ve seen in sterling versus the dollar since the referendum, teamed with the ongoing uncertainty which may harm growth and investment going forwards.

4) Europe: Will continue to muddle through, but more must be done

The IMF recently revised this year’s growth forecast for Europe from 1.6% to 1.7% and 1.5% for next year, the slowdown in 2017 being Brexit related. Although there have been murmurs that the ECB may be about to taper, the view was that monetary policy has been sufficiently accommodative and will remain so due to the stubbornly low rate of inflation which is forecast to remain below target at 1.1% next year. Taper talk seemed very much off the table.

With regards to fiscal policy, the challenge is that there is very little fiscal space available; even if Germany were inclined to do more, it was argued that there would be little impact on the rest of Europe, especially the periphery, since trade links are so weak. Attention should instead turn to structural reforms. Key concerns surround issues that have been in play since 2021/12; namely high debt burdens, NPLs, refugee and immigration. The cohesion of the EU could also come under the spotlight given Brexit negotiations as well as the political events on the horizon in Italy (referendum on Senate reform on 4 Dec) and the 2017 elections in France and Germany.

The meetings were a great one-stop-shop, hearing from a variety of central bankers, ministers and economists, covering the most pertinent issues. Anecdotally, learning about the culinary preferences of some of the world’s most influential policy makers was also memorable. For the record, Mark Carney favours pizza, Wolfgang Schäuble likes French food, Yi Gang likes everything and I rather liked Christine Lagarde’s response to where she would like to go for dinner; “I will take YOU for dinner and I will cook”. Key takeaway: the IMF and World Bank conferences definitely provided food for thought.

In this week’s edition:

Tune in for the charts and articles that are making headlines in bond markets.

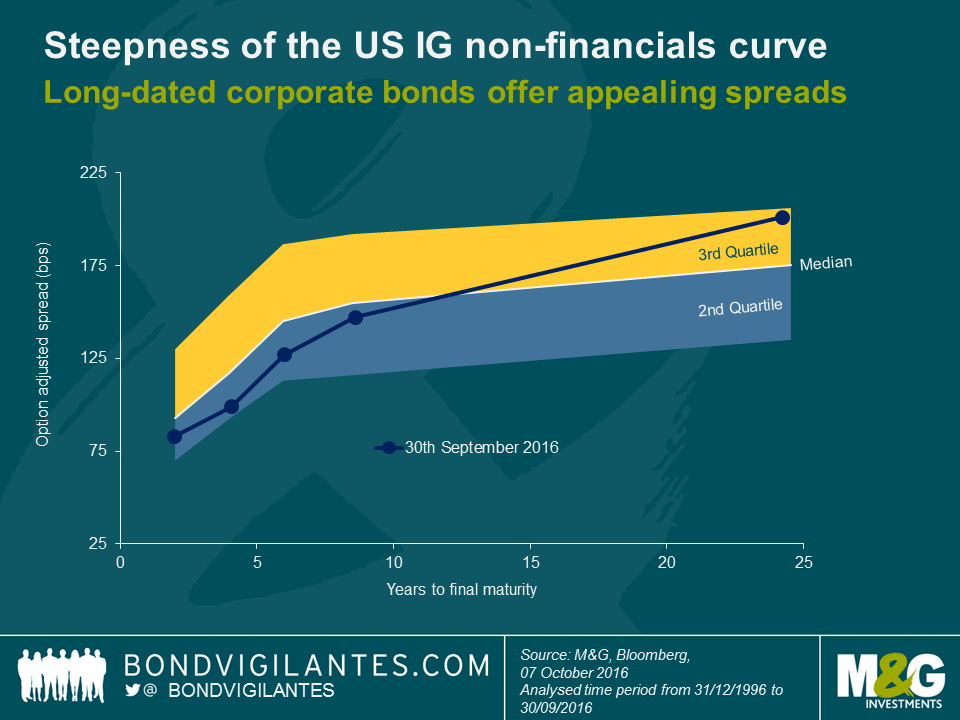

In a recent blog post, Ben discussed relative valuation opportunities in the US investment grade (IG) corporate bond market. Today, the long-dated segment of this market looks increasingly attractive given how steep credit spread curves in the US dollar IG space are at the moment.

The chart below shows the credit spread curve, as of 30th September, of US dollar denominated IG-rated non-financials against the middle 50% of spread observations over the entire history of the constituent bond indices since year-end 1996. Credit spreads for bond maturities below 10 years are currently beneath their historic median values. On the other hand, the spread level for long-dated credit nearly touches the top end of the range at 201 bps, highlighting the current curve steepness. In fact, looking back at the last 20 years’ worth of spread history, long-dated spreads have been tighter than today in 71% of all cases!

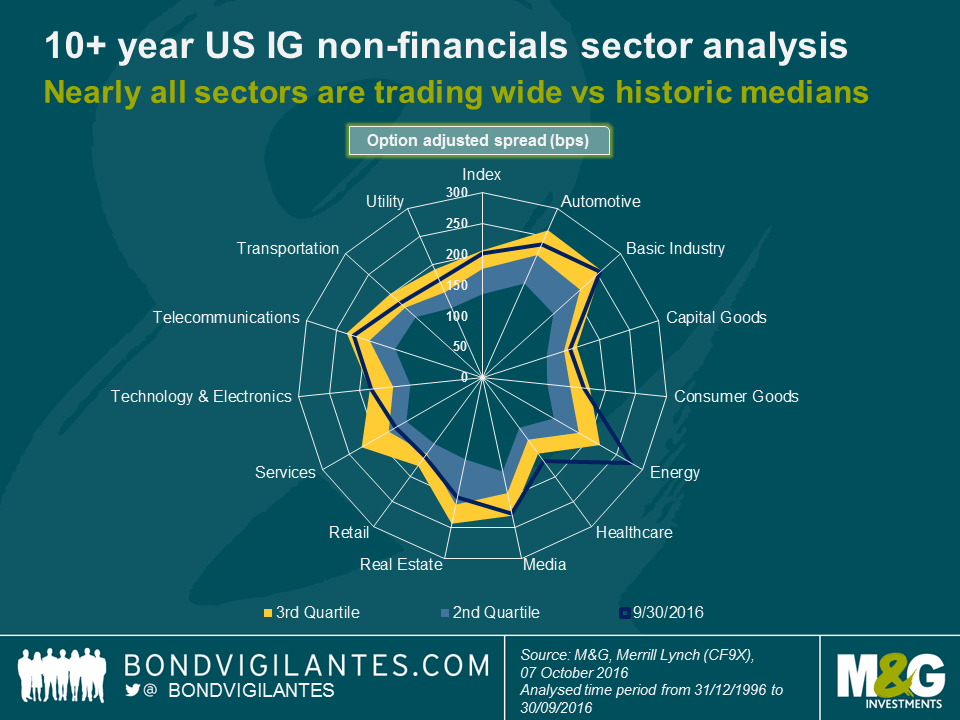

The following chart illustrates that attractive valuations of long-dated US dollar corporates are wide-spread across industry sectors. With the exception of real estate and services, all other sectors within the 10+ year IG non-financials space are trading in the 3rd quartile and, thus, above their historic median values. Furthermore, spreads for two sectors – energy and healthcare – rank even beyond 3rd quartile. This is not all too surprising considering the rather sluggish oil price recovery and political risks with regard to drug pricing, respectively.

With this in mind, it is fair to say that credit spreads of long-dated US IG corporates today provide a decent carry, particularly at a time when large parts of the government bond universe are trading at historically low or even outright negative yields. With attractive valuations like this, what could possibly go wrong?

Well, for instance, the high spread duration of long-dated corporate bonds makes them particularly susceptible to spread widening. The carry provided by the credit spread can act as a “cushion” for investors but will only absorb capital losses up to a certain point. In the case of the US non-financial 10 year+ corporate bond segment, which trades at a spread level of 201 bps and has a spread duration of 13.7 years, spreads can widen no further than 15 bps per year, all else being equal, before the carry generated from the credit spread is wiped off by capital losses. In a distinct risk-off episode however, as the one we experienced in the first quarter of this year, spiking credit spreads would seriously impact valuations of long-dated credit, at least temporarily.

Spread duration, like most other risk factors, is a double-edged sword, of course. If spreads continue to grind tighter, investors will enjoy capital appreciation on top of the credit spread carry. Considering current valuations of long-dated US Dollar corporates, we see potential for further spread compression in the medium and long term. Given how steep the spread curve currently is, there is reason to believe that long-dated credit is likely to relatively outperform short-dated corporates.

One factor that might prove to become a technical tailwind for long-dated US Dollar investment grade credit is the Bank of England’s newly launched Corporate Bond Purchase Scheme (CBPS). The eligible bond universe, as of 7th October, is distinctly long-dated in nature with a weighted average maturity of 13.5 years. In fact, around 55% of CBPS eligible bonds mature in more than 10 years and c. 25% even only after more than 20 years. Sterling investors who look for these maturity characteristics might find themselves increasingly crowded out by the CBPS. As the Euro investment grade universe is distinctly shorter-dated, they would not have much choice but to turn to the US Dollar market, exerting further downward pressure on credit spreads at the long-end.

A touch over 60 years ago BBC newsreader, Richard Baker, introduced Britain’s first ever television news bulletin. Richard wasn’t allowed to appear on screen for months, for fear that any inappropriate facial expressions could compromise the truth. Instead, the viewer saw still photos of any events that were deemed news worthy. Of course today BBC News has become a global institution, with news bulletins reaching millions of people around the globe.

It is in this vein of broadcast innovation that today we launch BVTV. Basically, we’ve decided to have a go at producing a short video, reviewing the week that was in bond markets and having a look at this week’s major economic events. And unlike Richard, I was allowed to appear on screen.

I have been overwhelmed by a sense of déjà vu of late. Talk of rates not rising again this cycle (US), ever again (Europe), or even being cut even further (UK, Japan) prevails. Quantitative easing continues apace and could be set to broaden further, be that in its duration or via the inclusion of new types of assets. Economic growth appears to be stalling, corporate profitability is showing late cycle declines, inflation remains practically non-existent. I could go on. Everywhere you look there is pessimism about the global economy, concern about monetary policy having – perhaps long ago – reached its limits, and new reasons to buy government bonds and risk free yields.

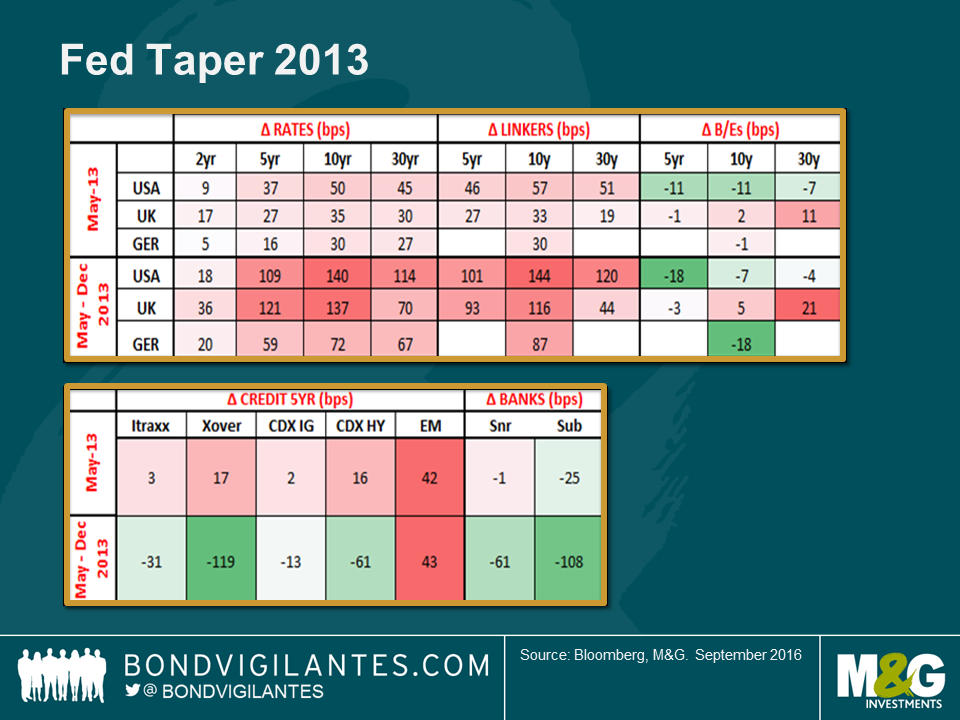

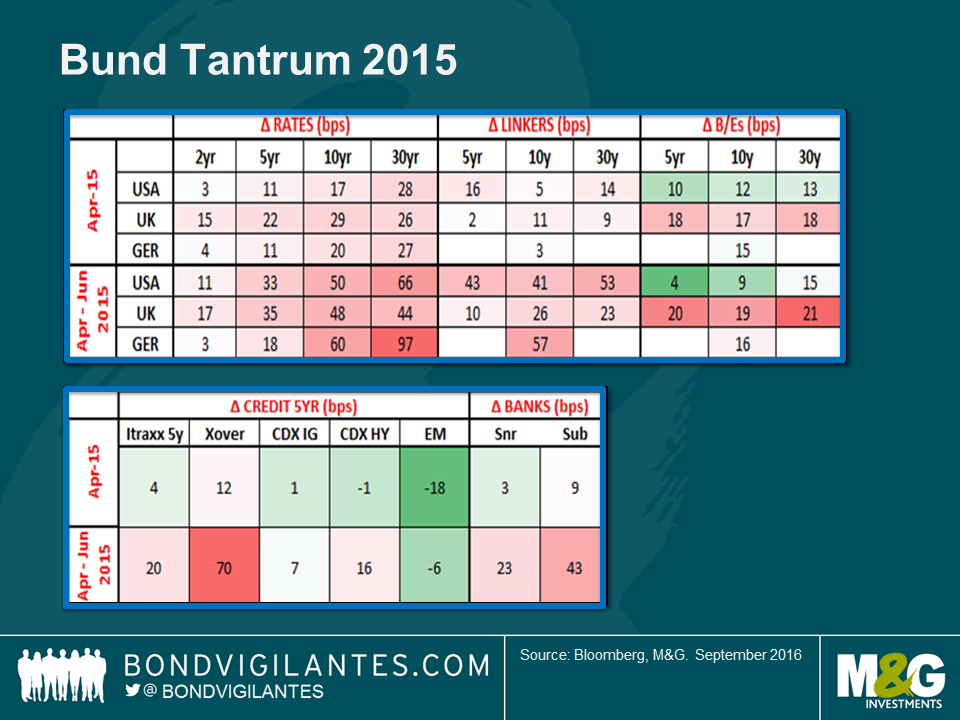

I was recently having a conversation with my colleague Anjulie about valuations and the outlook for government bonds, and in doing so, realised that I felt unnerving similarities between now and the first few months of 2013. Back then, there was talk about ‘QE-infinity’, the Japanification of the US, rates never being hiked again; anyone else see any parallels? Anjulie’s view, more correctly than mine, so far, was that despite yields already being historically low, given the extraordinary central bank action, the case could be made for rates and government bond yields creeping lower still. I felt differently, and said that it would be a worthwhile exercise for us to go and look back at the ‘Taper Tantrum’ and ‘Bund Tantrum’ of 2013 and 2015. Perhaps we could learn something from these episodes that could be applied to today? Anjulie put together the below slides and her findings are worth discussing.

Following the insignificant comments made by Ben Bernanke in an afterthought to a speech in May 2013 (in which he referred to tapering off the rate of purchases of government bonds and mortgage backed securities; MBS), the bond market awoke and had a proper tantrum. As the chart shows, 10 year treasuries sold off by 50 basis points in May alone, and by 140 basis points in the eight month period May – December 2013. Bunds and gilts were dragged down with treasuries, in spite of the fact that there was no talk of ‘tapering’ in Europe and the UK. Index-linked bonds were hit too, in a resolutely negative manner. Credit, though, was more mixed, with an initial widening in credit spreads in May reversing very strongly by the end of 2013, except in emerging markets which took the utterance of the word taper downright negatively.

One word, taper, was enough to cause these massive moves in government bond yields. It wasn’t a change in policy, as rates didn’t move and the rate of QE purchases did not change. So we asked ourselves what actually drove the changes. In my opinion, the takeaway from this episode was that the “this time it’s different” arguments had hit fever pitch (i.e. arguments about why monetary policy was never going to reverse course, which had been used to justify positioning reaching extreme long levels in government bonds and fixed income generally). As the realisation dawned that zero rates and constant QE were not necessarily going to carry on forever, everyone rushed for the door, fast.

The bund tantrum of April 2015 was similar in that UK, German and US government bond yields all rose significantly, with bund yields up 20 basis points in April and by 60 basis points in the April to June period. The story in credit was much more mixed though, and it is difficult to draw anything from this period, other than to observe that bank bonds took rising yields to be starkly negative. How different it feels today!

Looking back at this tantrum it is hard to put one’s finger on the catalyst which caused sell off in government bond yields. Yields on 10 year bunds touched 0.1%, and two months later they were back at 1%, incurring a loss of around 9 percentage points. In this case, I would postulate that positioning had moved very long given negative inflation prints and the start of QE. At 0.1%, long term valuation considerations came back to the fore and investors started to sell. And then everyone did. Again, fast. Whatever the reason, the sell off serves as a stark reminder: sentiment can change suddenly without the need for an obvious trigger.

As I mentioned at the outset, I see many parallels between today and the periods preceding these sell-offs. “This time it’s different” arguments – how rates can’t rise, QE can’t stop, inflation can’t be seen anywhere on the horizon, and government bonds can’t fall in price – abound. These are being used as justifications for buying yields and duration, even at a time when starting valuations are at extremes. We saw the same in early 2013 and in the early parts of 2015, albeit the starting point for valuations in the build up to these two tantrums were not as extreme as they are today. Being aware of these similarities, and remaining fully aware of current valuations, to my mind, argues for caution in these times.

Earlier this year we interviewed both Robert Gordon (here) and Martin Ford (here) about their books examining the impact of technology on the modern economy. In the latest of our author interviews I talked to the Economist’s senior editor and economics columnist Ryan Avent about his new book, “The Wealth of Humans”, that develops this same theme. In particular he looks at how we will be able to cope with an absence of work for large portions of society. With less work, and stagnant incomes, do we need a massive, and ongoing, redistribution of wealth to avoid unrest?

As always, we are giving you a chance to win a copy of Ryan’s excellent book. We have five copies available. Email your entry to bondteam@bondvigilantes.co.uk by midday UK time on Tuesday 11th October. Here’s the question. Adam Smith in the Wealth of Nations (Ryan Avent’s title is a nod to it) says that we shouldn’t expect our dinner to arrive from the benevolence of which three professions?

The results are in

The answer to the competition question was ‘Butcher, Brewer, Baker’. The winners are:

Sujay Shah – BMO Global Asset Management

Moyeen Islam – Barclays Capital

John McLaughlin – Brewin Dolphin

George Harper – Brewin Dolphin

Lynn Dobson – Edinburgh University

Congratulations to you all. A copy of The Wealth of Humans by Ryan Avent is on its way out to you.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.