Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Guest contributor – Jean-Paul Jaegers, CFA, CQF (Senior Investment Strategist, Prudential Portfolio Management Group)

Recently Jim Leaviss and I travelled to Tokyo to discuss local economic developments and Bank of Japan (BoJ) policy with economists and analysts based in Tokyo.

There was generally broad agreement that the potential path for Japanese government bond yields (JGBs) is asymmetric. The scope for lower interest rates was viewed as limited given the BoJ is aiming for an upward sloping yield curve and would not be comfortable if long-end yields fell by too much. Moreover, the move into negative territory with the policy rate has generally been perceived as quite negative by the wider public, affecting consumer confidence.

Market watchers have hinted at a preference from the BoJ to spend less than the ¥80 trillion rate, and a switch in policy from quantity to price targeting could be read as a way to taper bond purchases. However, there are a number of risks to the BoJ rate of government bond purchases. Firstly, if international bond yields continue to drift higher, the BoJ may be forced to increase purchases for a period of time to above their comfort level. Secondly, the BoJ risks falling behind the curve, as they attempt to balance the objectives of the yield curve control policy against the prospect of falling inflationary pressures.

One of the options to balance this risk would be to reset the yield curve targets from time to time, or to start using a ‘dot-plot’ as a guidance for yield curve targets to avoid any disruptions. However, this could be challenging in practice, as bond markets would likely take this as a negative signal and sell JGBs. The experience of the Federal Reserve in 1942-1951, where policy capped interest rates directly, shows in particular that the exit strategy is challenging.

One of the options to balance this risk would be to reset the yield curve targets from time to time, or to start using a ‘dot-plot’ as a guidance for yield curve targets to avoid any disruptions. However, this could be challenging in practice, as bond markets would likely take this as a negative signal and sell JGBs. The experience of the Federal Reserve in 1942-1951, where policy capped interest rates directly, shows in particular that the exit strategy is challenging.

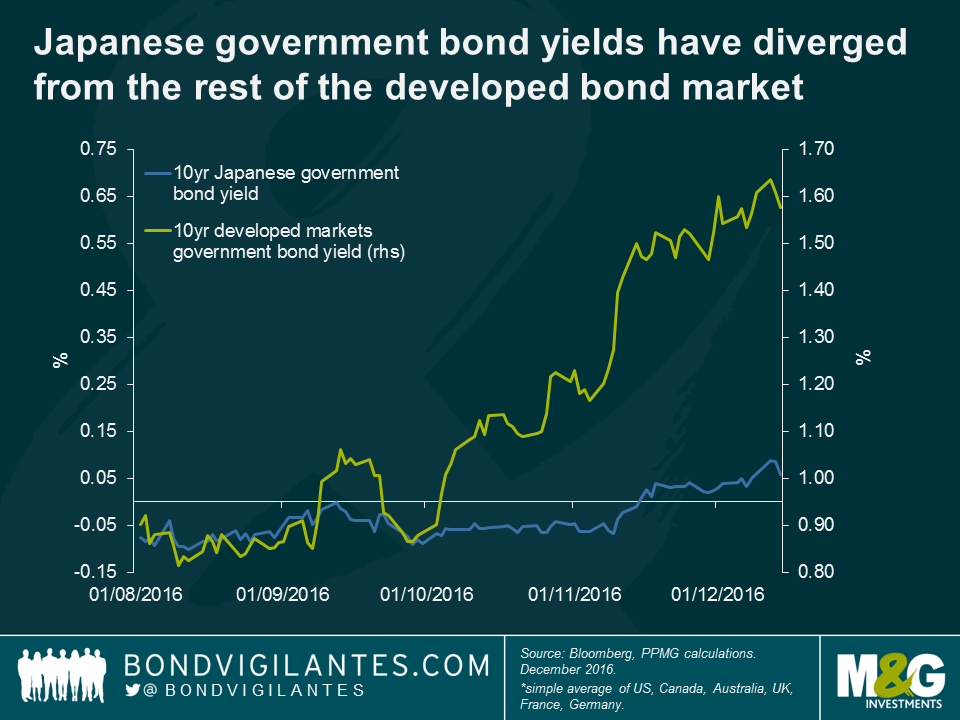

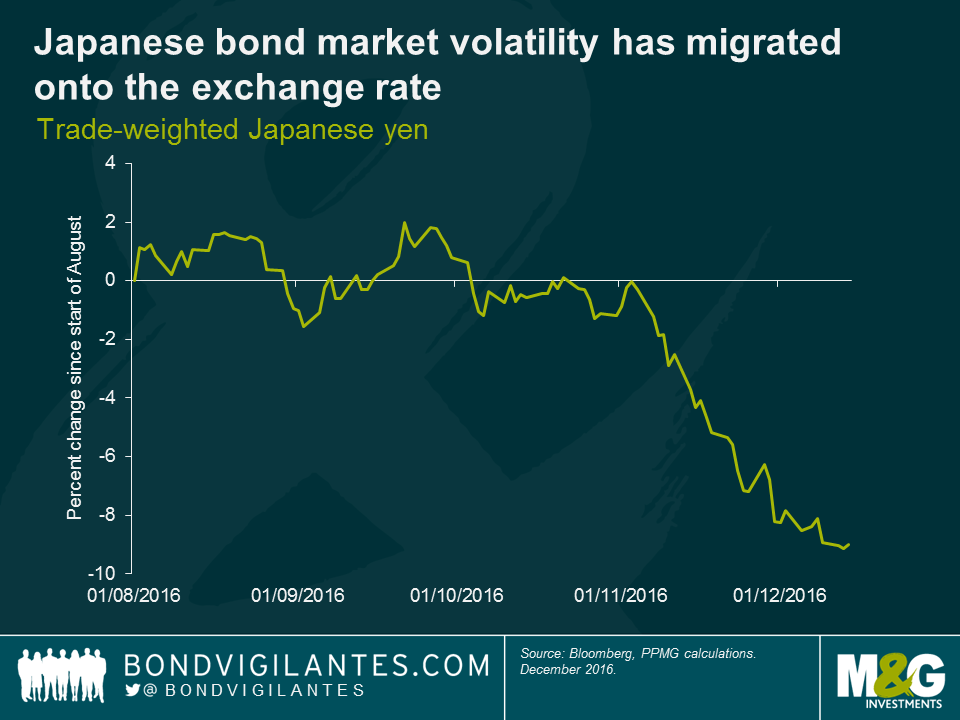

With the introduction of yield curve control the BoJ has in a way isolated the Japanese bond market from international developments. Consequently, volatility in bond markets has migrated onto the exchange rate. Given the yen is the transmission channel, a scenario of yen appreciation (for example US protectionism driving the US dollar down) would be an important element to keep an eye on.

Should yield curve control prove effective and the BoJ stick to its policy, there remains the question of how an exit strategy would look. The more one thinks about it, the more one tends to arrive at the conclusion asymmetry for bond returns is quite likely. This could be either by policy choice in an environment where global rates continue to drift up, or the result of the BoJ resetting the target to slightly higher levels. Any sign of upward management in yield curve control, in particular if the BoJ were eager to move away from negative policy rates, would signal to an investor on which side of the trade investors want to be. In the pure sense of control, such a scenario looks quite asymmetric for the investor (which for investors is a good thing), but also illustrates the challenge that increased control at a moment in time might come at the cost of less control going forward.

This content is prepared for information and does not contain or constitute investment advice. Neither PPMG, nor any of its associates, nor any director, or employee accepts any liability for any loss arising directly or indirectly from any use of this material.

What it says above.

This week on a special Christmas edition of Bond Vigilantes TV, Anthony Doyle and Jim Leaviss look at the major bond market events of 2016. They also discuss Jim’s macro outlook and the key things to look out for in 2017.

Here is the 10th annual Christmas Quiz. 20 questions, and the closing date for entries is midday on Friday 23rd December. Please email your answers to us at bondteam@bondvigilantes.co.uk. The winner will get glory, and can choose a charity from our approved list to which we will donate £100. She or he will also get a copy of the new Bond Vigilantes book, called “Bond Vigilantes – Part II”. Second prize is two copies of the Bond Vigilantes book.

Good luck! Conditions of entry are down below somewhere.

This competition is now closed.

This week on Bond Vigilantes TV Laura Frost discusses the market reaction to the Italian referendum, high yield energy issuance and the ECB.

Tune in for the charts, articles and the Bond Vigilantes team’s thoughts on the stories making headlines in the bond markets this week.

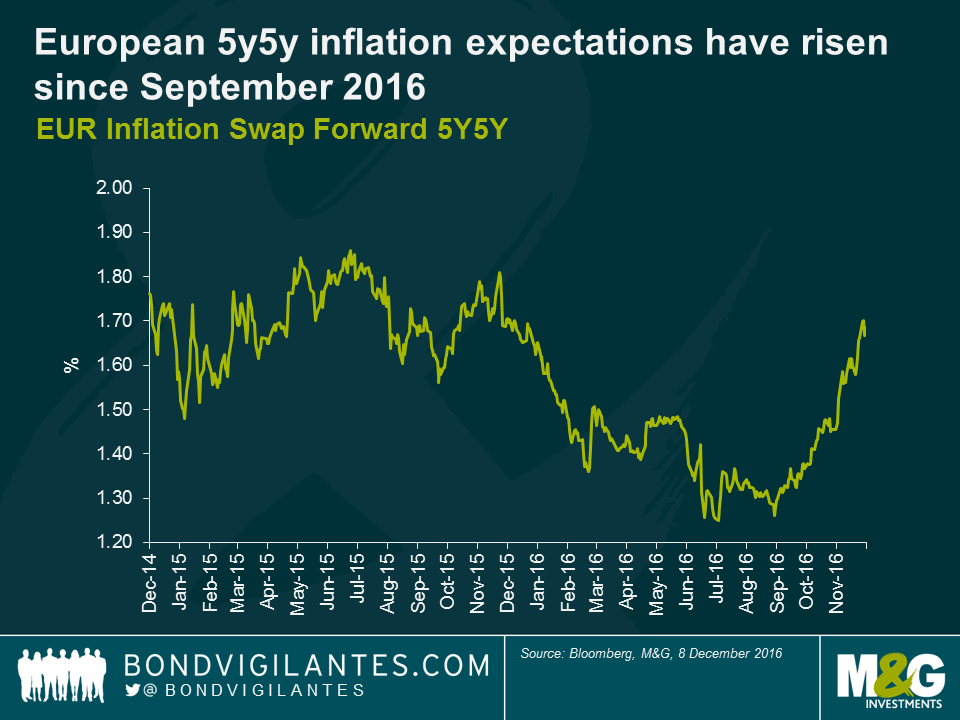

The votes are in and it’s pretty unanimous. Despite Mario Draghi’s best efforts to persuade otherwise, the market is clear that today’s announcements are tantamount to tapering. Frankly anything less than an extension of Euro 80bn per month, irrespective of the duration, was likely to have been taken as such, with scant evidence of the inflation target being achieved during the forecast horizon. Mario will have been well aware, but with market measures of inflation now discounting deflation risks the ECB hawks were always going to feel somewhat emboldened.

The reality, which we have observed before (see previous blogs), is that monetary policy has very likely reached its limits. For all the rhetoric that central banks will espouse to the contrary, the reality is that we have reached a tipping point. For each additional measure of monetary stimulus there is an equal or greater cost to be borne elsewhere in the economy- banks, insurers and savers the obvious losers.

The Eurozone may see some marginal benefit from fading fiscal headwinds in 2017 but these are unlikely to significantly move the needle. And the much hoped for structural reforms in Europe remain exactly that. This is Europe and red tape abounds.

The contrast with the US and the Federal Reserve is stark. Next week the Fed will surely hike rates. It should also find itself in a position to do so further in 2017, providing it with at least some ammunition should this seven year expansion be in its latter throws. With a US economy operating at full employment and likely to receive significant stimulus in the form of tax cuts and spending, the risk here has to be an overshoot in inflation with a central bank forced to pull hard on the handbrake.

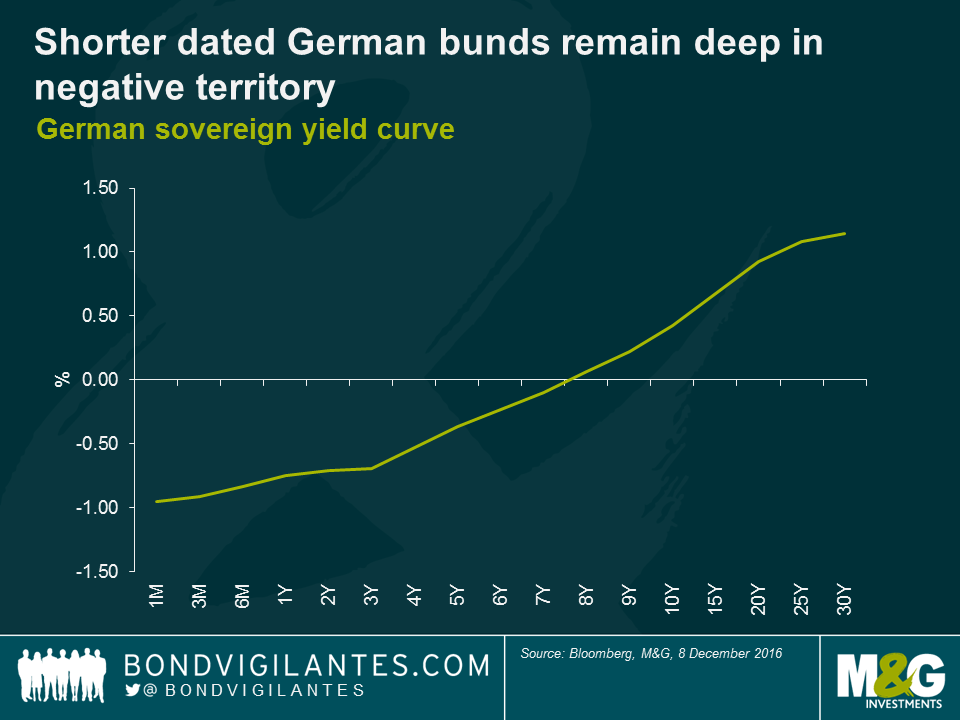

For the Eurozone, the most likely outcome for the economy is further muddle through, a very gradual closing of the output gap and no real prospect of hitting the near 2% inflation target until the end of the decade. Significant accommodation will be needed for years to come which is exactly what the shape of the German yield curve is telling us. The room to ease monetary policy in Europe if we were to run into a global slowdown in 2017/2018 is almost non-existent.

The irony for the ECB is that had it found the conviction to stimulate earlier and more convincingly it likely would have stood a greater chance of achieving its inflation and financial stability goals and, much like the Fed, would be well on its way to planning its exit today.

Guest contributor – Saul Casadio (Credit Analyst, M&G Investments)

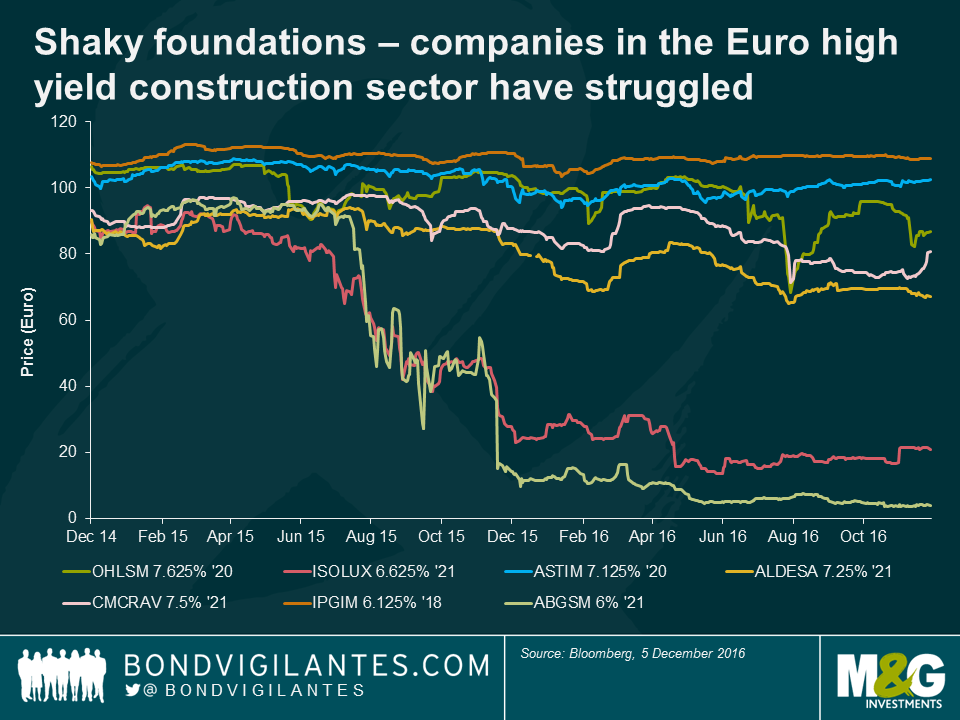

While European High Yield has delivered a robust performance over the last two years, returning on average 4.9% per year, one part of the index has significantly lagged. Over the same period bonds issued by construction companies have returned an average annual return of -18.4%. The chart below shows that, out of seven issuers in the sector, only two are currently trading above par, two have already restructured inflicting heavy losses on bondholders and the remaining three are trading well below par. In this post I investigate the reasons why the construction sector has performed so poorly compared to the rest of the market.

The use of a leveraged capital structure to fund a construction business has always been questionable. A leveraged capital structure needs a relatively stable cash flow throughout the economic cycle in order to be sustained. Construction companies, instead, experience a volatile and unpredictable cash flow. In addition, the construction business is highly dependent on the banks’ willingness to provide guarantees for the completion of works, something that is ultimately reliant on good credit ratings and at odds with a leveraged capital structure.

There are a number of analogies with a shoddy building project which explain the underperformance of the construction sector over the last two years.

The foundations were weak – Construction is a tough business. As works are typically awarded through a tendering process, a construction business operates in almost perfect competition. Entry barriers are limited to technical credentials and project size. It is not uncommon in some markets to tender for projects on a no-profit basis in anticipation of moving back into profit through modifications during execution, which is obviously a very risky way of generating profits and prone to litigation risk. Furthermore, construction works carry a significant degree of execution risk depending on the contract type (fixed-price vs volume based) and it is not uncommon for fixed-price projects to generate significant cash losses.

An unstable cash flow also compounds the fragility of the business foundations. Construction works typically feature a lumpy cash flow profile, given advance payments and final settlements. This translates into volatile working capital and gross debt. Changes in payment and collection terms, advance payments, and delays due to litigation could generate significant debt swings.

Measurements were inaccurate – reported EBITDA, one of the main key performance indicators used by investors, is only an approximate indicator when it comes to construction. The accounting method used for construction works (i.e. percentage of completion) provides flexibility in terms of profits (or losses) recognition throughout the life of a project. I would argue that cash generation is a better indicator as the cash flow statement is less subject to accounting management.

Calculations were wrong – investors calculate net leverage to assess credit risk, but this calculation is misleading in construction. Construction companies typically carry a high cash balance, but only a small fraction is available at the corporate level, as most is trapped in project companies to fund construction works. Gross leverage is a more accurate measure of credit risk in construction. Furthermore, most construction companies fund themselves through various forms of non-recourse financing, typically reported off balance sheet, possibly something not all investors spotted in the footnotes where these items are reported.

Modifications made measurement even more inaccurate – Given the challenging fundamentals of the business, a number of construction companies, looking for better ways to make money, have invested in build-operate-transfer (BOT) projects, effectively retaining the ownership and the economic benefits of the asset for a certain period of time in lieu of cash payments. This has only compounded the measurement problems discussed above as bondholders had recourse only to the construction business (and not to the concession assets), but numbers were reported only on a consolidated basis, impairing the ability of investors to monitor the operating performance of the construction business.

Suspicion of corruption – headlines of alleged cases of corruption have hit construction more than other sectors, and trading levels have reflected investors’ aversion to corporate governance issues.

A collapsed building is not worth much – Recoveries for restructured bonds have been low so far as trading performance deteriorated sharply during restructuring talks. Construction requires ongoing strong banking support to fund working capital requirements and to get guarantees necessary to tender for new works. Both are hard to get when a company is in the midst of a restructuring.

On the back of losses suffered on a few deals, investors have reassessed the credit risk of the sector and, judging by current trading levels, it would be hard to imagine a new high yield construction deal coming to the market any time soon. If that day comes again, investors should be mindful that building a leveraged capital structure on these shaky business foundations brings significant structural risk.

In our latest Panoramic Outlook, Jim Leaviss has a look at the forces that resulted in a tumultuous year for establishment politics, the ECB’s quantitative easing dilemma and the prospects for emerging markets in 2017. For the first time since the financial crisis, it appears that bond yields will come under sustained pressure as central banks gradually remove monetary stimulus. The impacts of the structural switch from monetary to fiscal policy by authorities will be far reaching, and will likely be felt in every corner of the fixed income world.

For this and more, please click here to access our 2017 outlook.

In this week’s edition:

Tune in for the charts and articles that are making headlines in bond markets.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.