Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

I was joined by Chris Clemmow (Fixed Income Dealer, M&G Investments) this morning for a quick chat about global credit markets. Chris is at the coal face of bond markets, and is a primary source of market information for the fund managers at M&G. Tune in for a discussion of the prevailing market dynamics of the investment grade bond market, and a look at what happens when Article 50 is triggered by British PM Theresa May later this week.

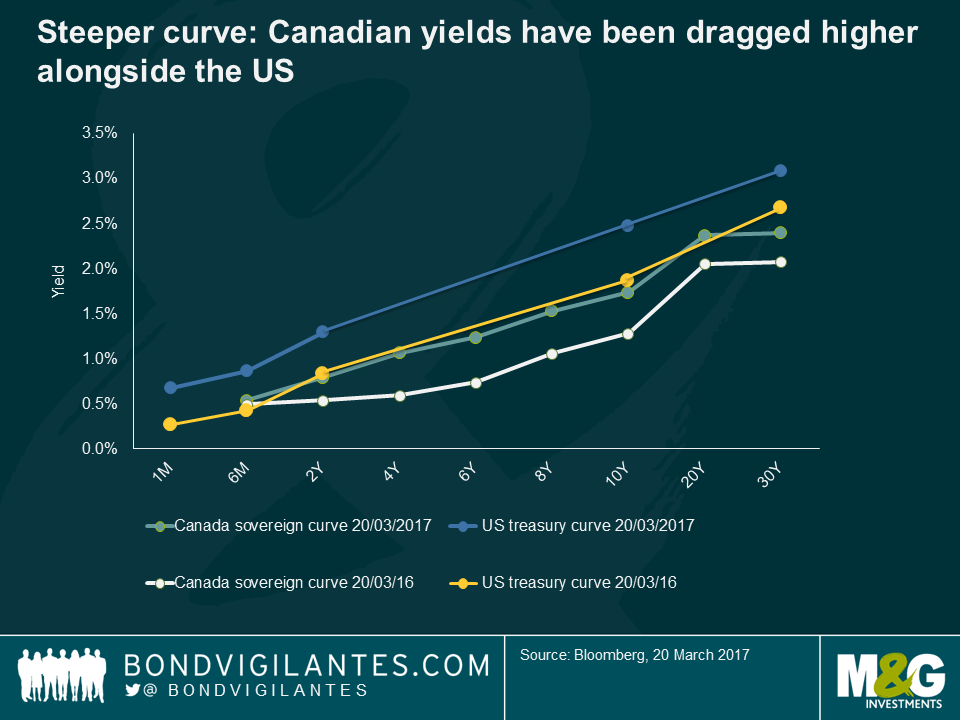

Yields on Canadian sovereign bonds have been dragged higher in recent months, with the yield on the 10-year bond recently reaching 2 year highs. This sell-off appears to reflect the US reflation narrative, rather than the economic fundamentals of the Canadian economy.

The market currently thinks the Bank of Canada will remain on hold throughout 2017, pricing in only one rate hike – a 20 basis point move – in 2018. The stance of the BoC, much like the ECB, BoE and BoJ appears increasingly at odds with the outlook for US monetary policy.

Unlike the US however, with the unemployment rate at 6.9%, this remains elevated compared to the pre-crisis years and the BoC continues to highlight the level of slack which remains in the labour market. Although headline inflation has picked up in recent months, this was downplayed by the BoC at its latest meeting, with wage growth remaining sluggish and aggregate hours worked weak.

Though the market is leaning towards pricing in a rate hike, there are a few key downside risks to this view.

Firstly, oil. The fall in the oil price detracted from Canada’s GDP growth in both 2015 and 2016 and the recent leg lower could potentially provide an ongoing headwind. Hearteningly, analysis from RBC suggests that oil is less of a concern today insofar that the price would have to drop below $25 before companies started to shut their operations. However, a price above $70 would be required for brownfield investment and above $100 for any significant greenfield investment – a significant hurdle.

Secondly, the strength of the domestic economy is an obvious concern for policymakers. The aforementioned labour market slack alongside disappointing non-energy export and lacklustre investment growth remains an area to watch (though the previous $11bn of fiscal expansion in infrastructure spending has fallen rather flat, as take up for funding new projects has been disappointing). Other noteworthy factors include a housing market where prices continue to surge nationally (particularly in Toronto) and the increasing indebtedness of consumers (as RBC pointed out, non-mortgage credit market debt to personal disposable income ratio reached a new high of 167.3% in Q4).

Finally, and perhaps most significantly, U.S. economic policy will have a significant impact on the Canadian economy. If trade tensions heighten, or the U.S. were to implement or make inroads with respect to a border adjustment tax to fund consumer tax cuts, the terms of trade shock could detrimentally affect the Canadian outlook. On the other hand, the U.S. administration’s fiscal plans remain unclear, and any fiscal boost to the U.S. economy could have a positive spill over effect on the Canadian economy.

As it stands, it is difficult to argue with implied market rates – Canadian monetary policy will likely remain stagnant, creating a larger gulf between US and Canadian policy. Over the longer term however, risks to the downside for the Canadian economy are not yet dissipating, so it’s just as likely that the next move in interest rates could be a cut. As such, a bullish view on Canadian government bonds and a bearish view on the currency is perhaps warranted.

Tune in to our latest edition of BVTV, where this week I discuss:

We often use Twitter to share the charts that we think are interesting, but probably don’t warrant the extra analysis of a blog. With this in mind, I’ve had a look to see which charts were most favourited or retweeted by our followers at @bondvigilantes and provided a little more detail than 140 characters can allow.

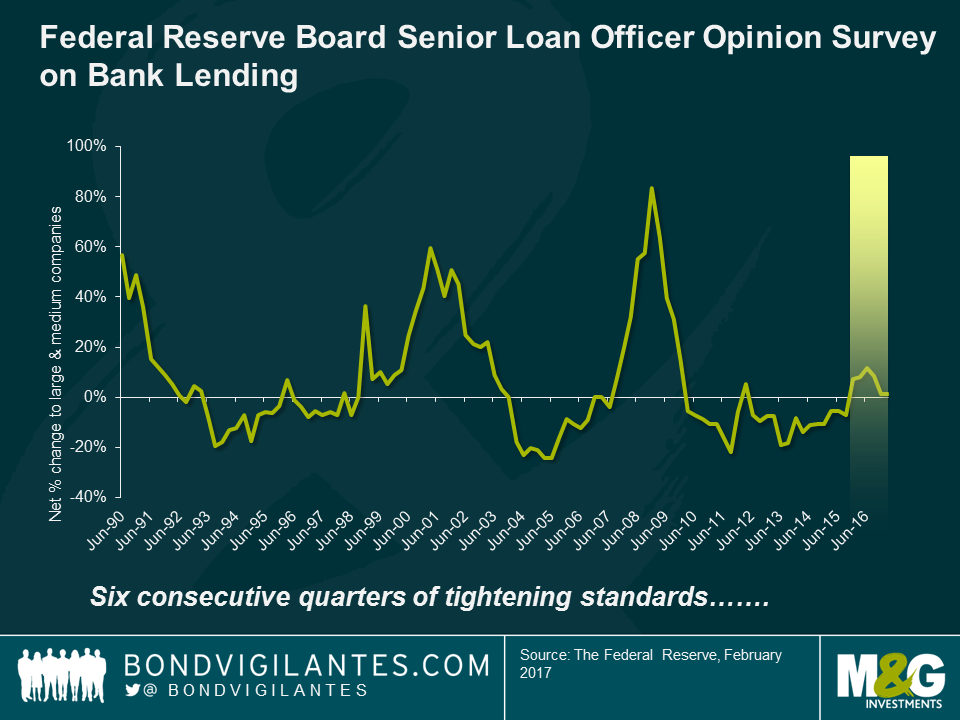

Every quarter, senior loan officers of large US banks are asked by the Federal Reserve how their standards for approving business loans have changed from the previous quarter. Looser standards suggest credit is easier to obtain, so companies and individuals can invest and spend, which leads to higher economic growth. A tightening in standards suggests credit is harder to obtain, and hence economic growth may slow.

Lending standards and growth in loans and output are negatively correlated, so lending standards can be predictive of economic growth. As the chart above shows, it is rare to see US banks tighten standards for six consecutive quarters outside of a recession, and with the FOMC likely to hike interest rates on Wednesday, credit may become increasingly difficult to come by, particularly if the firm or individual has a poor credit rating.

In a world where many fixed income investors are paying to lend to developed market governments, and corporate bond yields are around all-time lows, emerging market bonds are increasingly being viewed as an area for investors to allocate to in search of higher returns. The universe of emerging market fixed income issuers is large and diverse, and non-financial EM corporate bond markets in particular have grown considerably in response to the disintermediation of banks. Local market issuance has become increasingly important in recent years (especially in Asia) as local savings institutions have evolved to support local debt markets. In global bond markets, the stock of debt issued by EM corporates is now larger than their developed market equivalents. Turning to government bond markets, the stock of developed market sovereign debt ($25.0 trillion) remains far greater than the emerging market sovereign bond market ($8.5 trillion). This reflects the lower levels of indebtedness of emerging market governments.

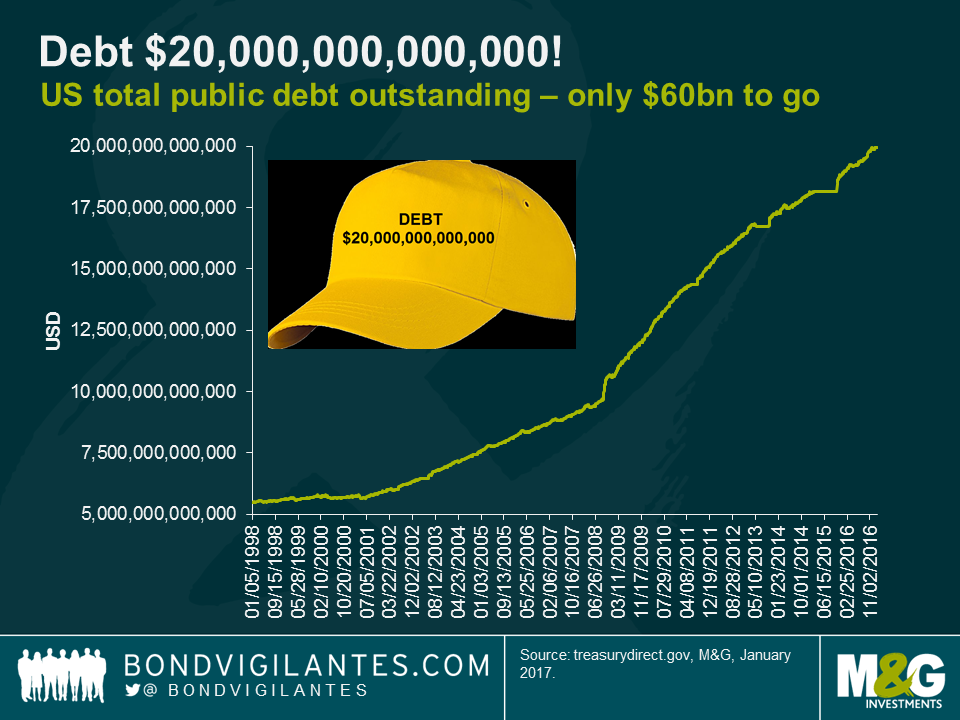

With the Dow Jones Industrial Average making headlines for closing above 20,000 for the first time, it was interesting to note that US total public debt outstanding looks set to rise above $20 trillion. Whether it does or not will depend upon the U.S. Congress raising the government’s debt limit. The level of US public debt outstanding has more than doubled since the financial crisis.

The U.S Treasury Department’s ability to raise debt will be suspended later this week, with Treasury Secretary Steven Mnuchin stating that state and local government bond issuance will begin to cease until Congress raises the debt limit. The Congressional Budget Office thinks that unless the debt ceiling is raised, the U.S. Treasury would run out of cash to pay creditors in about six months, resulting in an unprecedented US default. Whilst markets are not currently focused on the debt ceiling, the clock is ticking, and Mnuchin has made it clear that the issue is critical and requires urgent attention from Congress.

There was plenty to occupy bond markets last week, and with all eyes now turned to the Fed, this week is shaping up in similar fashion. Tune in to our latest edition of BVTV as Wolfgang Bauer and I discuss:

I was recently in San Francisco for an internet and technology conference. An array of senior tech managers spoke about their firms’ prospects, priorities and where they see opportunities. Twitter’s Jack Dorsey aside, the overwhelming focus of every session I attended over the three days was cloud computing.

Cloud computing is essentially the move away from users buying, owning and maintaining their own computer systems to a more on-demand, rental model. In the past we would buy a desktop computer, install our software and store our information on the hard drive (sat under the desk). We would use the processing unit to run the software and our calculations for us. If we owned more than one computer we could link them up – maybe via a central server – to create a network, allowing multiple users to share information, software and processing power. Moving an IT system into the cloud removes the headache and cost of buying and maintaining your own infrastructure.

Not only does operating in the cloud reduce costs, it also increases flexibility. If you need more processing power or increased storage capacity you can just give your cloud provider a call and they can (within reason) instantly meet your needs by flicking a few switches. Think of a retailer who experiences much higher traffic on their website around Christmas; if they have a cloud based infrastructure they need only pay for the extra capacity for the month or so that they need it. There’s no need for them to house and look after a large server farm, operating below capacity, for the other 11 months of the year.

As well as supplying hardware, software as a service (SaaS) is also a growth area which many of us may be more familiar with. Spotify, Hotmail, Gmail and Salesforce (currently building the tallest office in San Francisco) are some well-known examples. The benefit of SaaS is that the providers can make updates and fix bugs as and when they need to. Rather than a licencing agreement specific to one device, users pay a monthly/annual subscription fee to access the software on the cloud. This means they can access it from anywhere on multiple devices and they always have the most recent version.

Unsurprisingly, Silicon Valley start-ups were the first to embrace cloud technology when Amazon (AWS) began renting out its spare server capacity back in 2006. But now the industry is growing with non-IT focussed businesses becoming comfortable with the technology. AWS have maintained the first mover advantage, but they have some serious competition in the form of Google, Microsoft and Alibaba. All three are dedicating huge resource to their product and making an immense effort to sell their services, at an enterprise level, to CEOs and CIOs (chief information officers) of large firms.

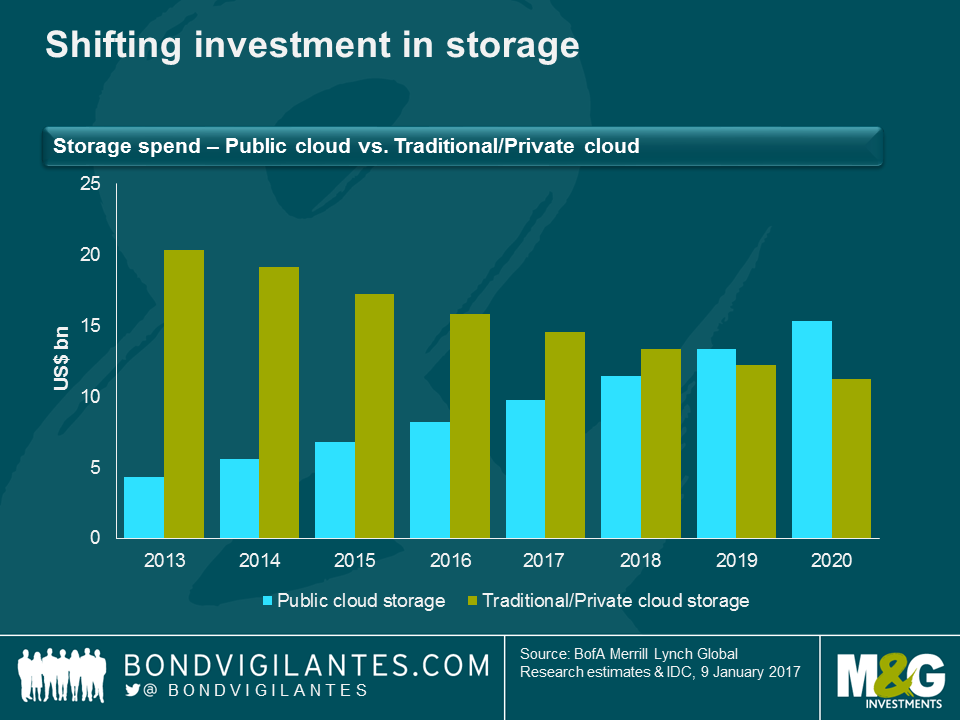

There was a lot of discussion of hybrid models (i.e. companies having both cloud and on-site infrastructure) which I think sounds most realistic in the near term, as firms will take time to get comfortable with the new technology. The chart below, from BofA Merrill Lynch, shows their estimates of how the balance of investment will shift over the coming years within the storage segment.

I think data security and reliability (as AWS’s problems last week demonstrate) will be chief among CEO/CIOs’ concerns, but assuming these can be overcome the general direction of travel is clear. Not being in the cloud put firms at a competitive disadvantage as their capex costs will likely be higher. I’m not convinced that real GDP statistics have been fully capturing the value of productivity gains from technological progress over the past couple of decades. Therefore I think it unlikely that, at a macro level, cost savings in the corporate sector will feed through to official growth, inflation and productivity numbers. Going forward however, if the majority of IT infrastructure investment is conducted by cloud companies in the future, the corresponding investment contributions to GDP will presumably accrue to those nations that host the cloud providers and/or the server farms.

What I am sure about is that a fundamental shift in how we store, share and process data raises questions over how to think about the tech giants providing these services. I’m confident this will be a high growth, high profit area in the years to come. But once the world is using the cloud for all its computing needs, and the large profit margins have been competed away, will it become sensible to think of them less as growth companies and more as utilities? In any industry when one earns monopolistic or oligopolistic power, increased scrutiny and regulation is sure to follow.

We are kicking off the week with an emerging markets special on BVTV, as I talk all things EM with my equity market colleague Michael Bourke. Tune in to hear us discuss:

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.