Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Last week, the U.S. Federal Communication Commission (FCC) announced the results of the latest $20 billion, 600Mhz spectrum auction. Communication companies were bidding for spectrum over which they provide wireless services to their customers. The largest bids came from wireless mobile operator, T-Mobile USA, which spent $8 billion, and U.S. satellite TV provider DISH Network, which spent $6.2 billion. While the auction itself was not particularly noteworthy, this auction was viewed by industry followers and participants as a potential catalyst for wider U.S. telecom and media consolidation. If an acquisition spree is about to occur in the sector, this could have significant implications for bond investors.

Cable consolidation is mostly driven by achieving cost synergies. However, a potential merger wave is not only about synergies. Many of these companies see the strategic importance of offering a full spectrum of services and content to their customers, thereby capturing as much of a customer’s spend as possible, be it via a subscription model or on-demand services. The idea is to achieve triple-play penetration, which refers to when a single provider can bundle a customer’s voice, video and internet services in one offering. Providers also recognise the strategic benefit of adding mobile service/connectivity to their offerings, called quad-play-penetration. Consequently, not only could we see further cable consolidation, but cable operators may look to acquire wireless providers and vice-versa.

Telco and cable companies are also exploring owning their own media content to pipe through the distribution channels that they have established with their customers. AT&T’s recent proposal to buy Time Warner Inc. (and its content creators like HBO, Warner Brothers Studios, etc.) being the most recent example of this vertical integration. It’s all about offering a full suite of communication and content services in one attractive, cost efficient (for the company anyway) bundle to the customer.

These are only a few of the potential strategies that are being contemplated across the TMT universe. Our TMT analysts here at M&G compiled the following diagram that highlights the myriad of potential combinations. The diagram, of course, is purely hypothetical, at least for now, but it highlights the scale and complexity of potential scenarios across the various sub-sectors of the broader industry.

If a merger wave occurs, the implications for bond holders could be significant as well as nuanced. With enterprise values of tens-of, or even hundreds-of-billions of dollars, the purchase prices of many of these assets will be considerable. Any potential acquisition will likely come with a meaningful debt component, meaning a new supply of bonds for a market that already holds a lot of these companies’ bonds. Telecom, Cable and Media companies account for 19% of the Bank of America U.S. High Yield Index including five of the index’s top eleven issuers. These same sectors account for 8% of the U.S. Investment Grade Index. Any additional issuance from these entities is likely to pressure the prices of existing bonds.

For example, the most widely anticipated tie-up surrounds the #3 and #4 wireless operators in the U.S., T-Mobile and Sprint. Whilst not arguing for or against the merits or the likelihood of a combination, such a transaction could have a big impact on the U.S. high yield market. Sprint and T-Mobile are the #1 and #11 issuers in the index with $25 billion and $12 billion respectively in bonds outstanding. Given their weighting in the index many (if not most) high yield investors are likely to be invested in either (if not both) T-Mobile and Sprint. With enterprise values of $65bn for Sprint and $78bn for T-Mobile, one should expect material debt issuance to partly fund any potential transaction. Further, a potential deal could be constructed to preserve T-Mobile’s higher Ba3/BB ratings to the benefit of Sprint’s existing bonds, whereas a more aggressive deal (i.e. a larger debt component) in-line with Sprint’s B3/B ratings could pressure T-Mobile’s existing bond prices.

Further, should an investment grade company acquire a high yield company, the upside for holders of the high yield bonds could be significant whereas the holders of the investment grade bonds could see their bonds weaken if the company decides to tolerate some degree of credit deterioration in order to make a strategic acquisition. Similarly, should a high yield company pursue an investment grade company; downside risk would be prevalent for holders of the investment grade bonds.

The cable and telecom industries in the U.S. are champing at the bit to consolidate and integrate. The recent spectrum auction effectively placed a moratorium on M&A in the space as the industry waited for last week’s auction results. Under a Trump administration, market speculation is that the regulatory authorities’ position on M&A in the sector will soften considerably. With this most recent auction in the books and what is considered to be a consolidation-friendly administration, we may be on the cusp of an M&A feeding frenzy among cable, telecom and media companies which will have significant implications for bond investors.

Guest contributor – Maria Municchi (Fund Manager, M&G Multi-Asset Team)

The following blog was first posted on M&G’s Multi-Asset Team blog, www.episodeblog.com. M&G’s Equities Team also regularly post their views at www.equitiesforum.com.

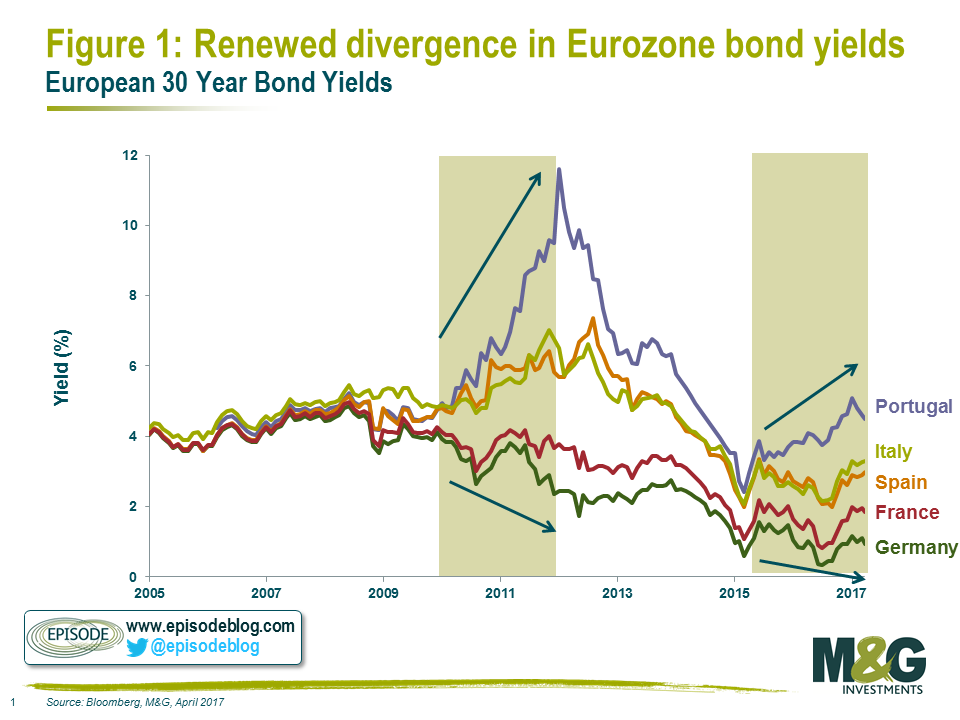

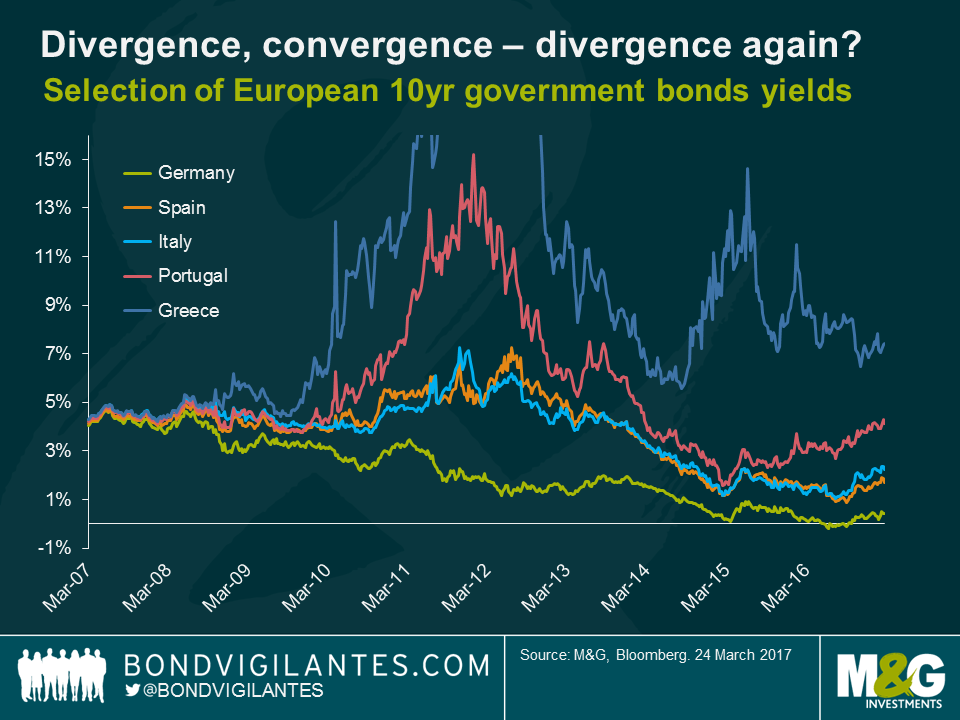

Despite the partial realignment of European long-dated government bond yields following the Euro crisis in 2012, there has been renewed divergence in yields in the last few years.

On a simplistic level, this runs contrary to improving fundamentals. While sharply accelerating Portuguese and Spanish debt levels partly explained yield moves in the Euro crisis, levels have plateaued since 2013. At the same time GDP trends have been improving, and the risk of deflation seems to have abated.

How then can we justify the increased divergence of yields across long term EU sovereign bonds?

Juan wrote in 2015 how the relationship between debt to GDP and bond yields is not a straightforward one, particularly when the sovereign is able to print its own currency. In the Eurozone this relationship is further complicated. First, debt levels become more important because individual Eurozone countries cannot control their own currencies. Second, the conditional nature of ECB support means that whether Eurozone bonds represent more of a “credit risk” or a “rate risk”, is subject to the willingness of local politicians to comply with the EU and IMF. This was evident in the experience of Syriza in Greece, and more recently was a key factor in the blow out in Portuguese bond yields at the start of 2016.

This does mean that, although fundamentals may have stabilised and even partly improved in some areas, the unstable risk characteristics of the assets themselves are subject to change. An investor’s job is to assess whether price moves reflect genuine changes in these characteristics or simply shifts in investor perceptions of them.

While the risk of default of Eurozone countries has been extensively debated ever since the crisis, there have been no defaults so far (though the Greek “haircut” can be seen as the equivalent). So the question is: are we simply overweighting the risk of default of those countries just because we have experienced the Euro crisis? Is the emotional trait of availability bias distorting our thinking and decision making?

What has changed?

2012 was indeed a genuine and profound crisis for the Euro area but we are now in a better situation and while some issues still remain, the macro environment has improved significantly, and the budgetary efforts undertaken by Portugal and others, have been material. European GDP has increased to a solid 1.8% while labour market has improved with unemployment falling below 10%. Sentiment is also improving sharply across countries pointing towards a stronger economic convergence within the Eurozone (which Mario Draghi has emphasised in recent speeches).

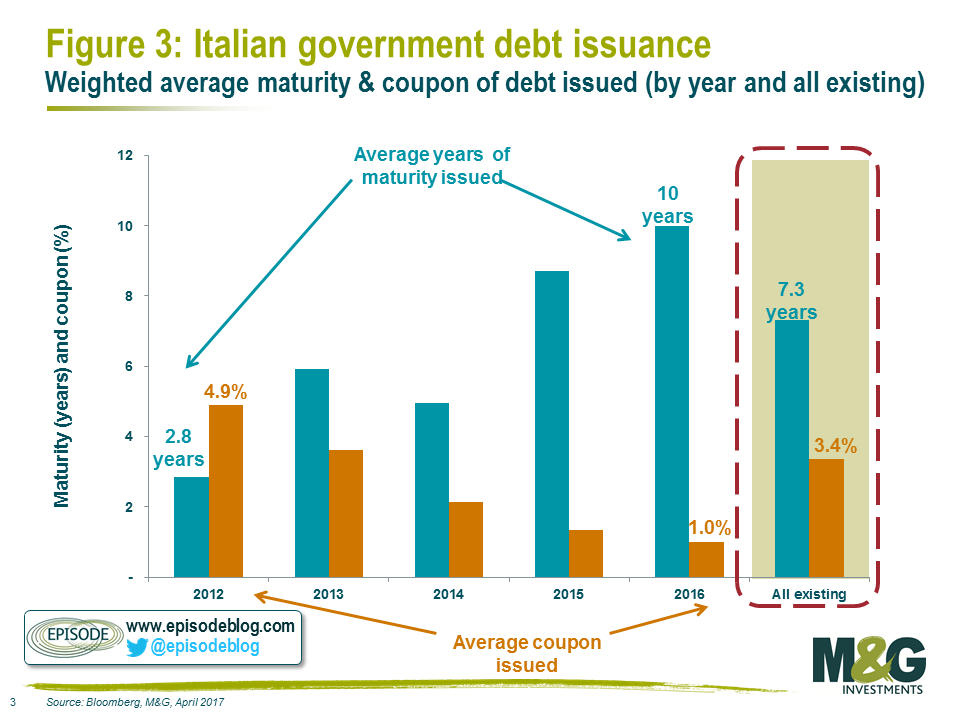

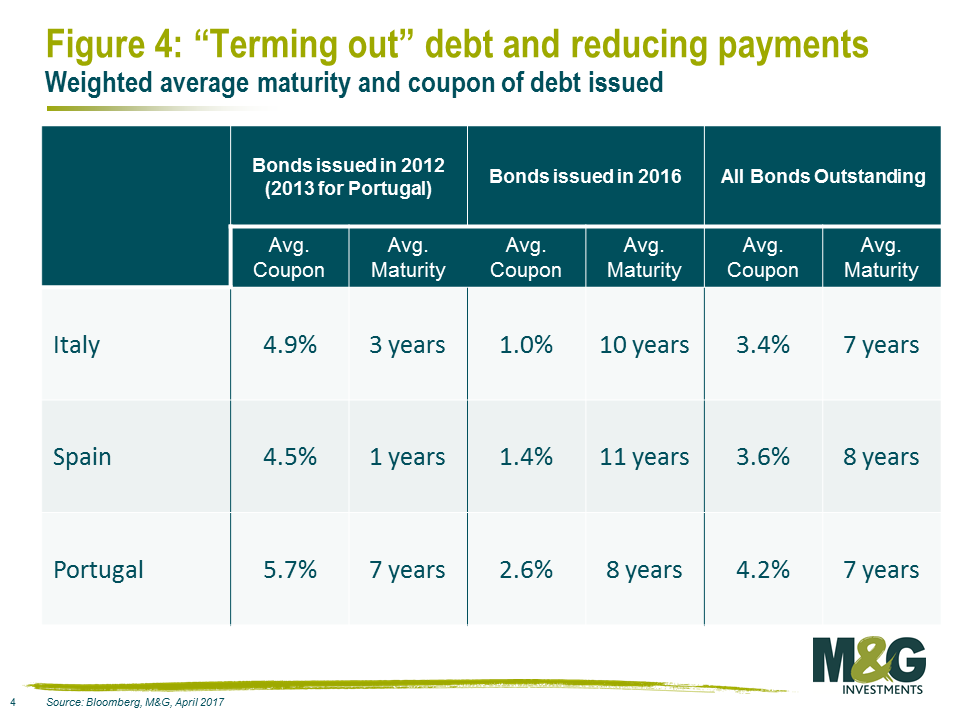

Also, thanks to the very low interest rate environment and intensive QE that followed the Euro crisis, even the most indebted countries have been able to refinance themselves at attractive levels of yields. And they have done so significantly extending their maturities in order to benefit from lower yields for longer. Although debt levels may be similar to those three years ago, with the help of the ECB, the composition of that debt has changed.

For example in Italy, the average coupon fell from almost 5% for the bonds issued in 2012 to less than 1% coupon for the bonds issued in 2016, while maturity was extended from 2.8 to 10 years on an issue size weighted average.

This trend has been mirrored in Spain and Portugal.

Taking advantage of lower yields to refinance on more attractive terms is apparently now being considered in the US (just as rates start to rise) and seems appealing (though the benefits may not be as obvious as they appear). However, with cheaper debt on their balance sheets and improving economies those European countries should be better placed, despite the many political troubles, to avoid default (and therefore deserve a tighter spread to the German bund!).

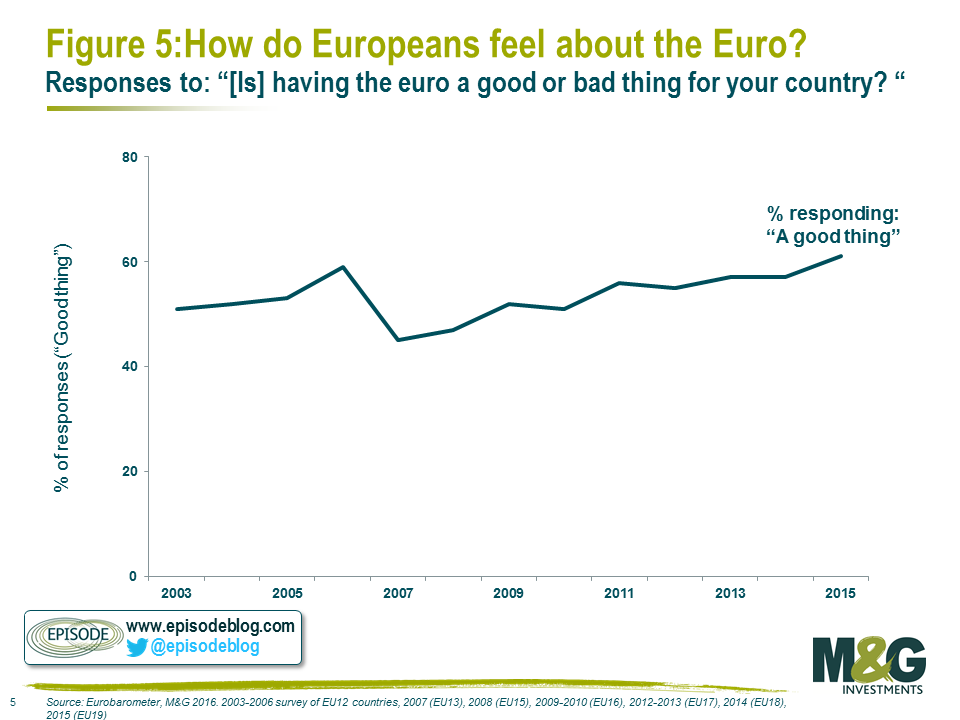

Overall, it looks like the story about bad debt dynamics isn’t compelling enough and in fact it has not been the fulcrum of investors’ attention for a while. So, what is driving prices? Certainly, the busy European political agenda has been taking centre stage. What about Marine Le Pen? And Brexit elections in the UK? Aren’t those all pointing to a greater risk of Euro area break up?

Well according to recent polls, despite the rise in populist sentiment and politicians calling for more EU referenda across various countries, Europeans might be more favourable to the Euro than some people think…

Interestingly, even within Marine Le Pen or Movimento 5 Stelle parties, leaving the Euro is one of the most divisive aspects, so much so that some people are wondering if including it as part of the programme was a good idea at all. As I discussed with regards to the Italian referendum last year, we should be wary of allowing the fact that Brexit has taken place to influence our perceptions of dynamics in other European nations.

As always, it is critical to differentiate between change in investors’ sentiment and genuine changes in the economy. We cannot know who will win the next elections or what Brexit will actually mean for Europe but we can know if we are being appropriately compensated for the risks we are taking.

It seems that the legacy of the events in the Eurozone five years ago, and Brexit last year, have played a meaningful role in influencing perceptions over the last twelve months. The economic reality is complex, but the recent divergence in bond yields seems to have been more related to these perceptions than underlying fundamentals. As such, an Italian 30 year bond yielding 3.2% or a Portuguese 30 year bond yielding 4.4% relatively to a German 30 year bonds yielding 0.9% looks more like an opportunity than a threat.

Switzerland has made headlines of late as a potential candidate to be labelled a currency manipulator by the U.S. Treasury. For those countries at risk, a report recently published by the U.S Treasury sets out three key criteria the U.S. Treasury will use in order to assess whether a country is “pursuing unfair practices”. Firstly, the country would have a significant bilateral trade surplus with the United States defined as more than USD20 billion. Secondly, a country with a current account surplus of at least 3% of GDP would receive heightened analysis from the U.S. Treasury. Finally, persistent, one-sided currency interventions in excess of 2% of a country’s GDP over a 12-month period could be a sign that a country is manipulating its currency, and therefore imposing “hardship on American workers and companies”.

According to the report, Switzerland exceeds the threshold for two out of the three evaluation criteria defined by the Treasury and joins China, Japan, Korea, Taiwan and Germany on a monitoring list of countries which “merit close attention to their currency practices” according to the U.S. Treasury.

The report also recommends some concrete actions the Swiss authorities could take in order to come off the monitoring list. These include a return to more traditional monetary policy tools, a disclosure of currency intervention data, and a greater degree of fiscal easing in the Swiss economy. With regard to the latter, while it is true that Switzerland has room to use fiscal policy to stimulate growth, the Swiss economy is heavily linked to its major trading partners and very much dependent on a competitive exchange rate. Further and greater fiscal spending, not just as a replacement of monetary policy action, could backfire with an unwelcoming appreciation of the Swiss franc, especially if Swiss growth decouples too much from the Eurozone average.

The recommendation to use more traditional interventions is easier said than done. This card has been played by the Swiss National bank before it started to heavily intervene in the currency market. The Swiss benchmark interest rate is deeply negative at -0.75% and, as I’ve blogged before, continues to hurt the profitability of the financial sector, a key contributor to Swiss GDP.

The SNB is sitting on foreign currency reserves that are close to 100% of GDP, making its balance sheet vulnerable to currency moves. Importantly, despite all the interventions, the Swiss Franc looks expensive compared to the USD on a purchasing power parity basis so it would be odd to say that the Swiss economy is gaining an advantage from having an undervalued exchange rate from a U.S. perspective. When asked about currency manipulation, SNB Chairman Thomas Jordan recently said in an interview with newspaper Schweiz am Wochenende: “Interventions are not made to take advantage of an undervalued currency, rather the contrary, to protect Switzerland against a significant overvaluation of the Swiss Franc and its negative impact on the domestic economy. International authorities are aware of this and do acknowledge.”

Going forward, there is a risk that the SNB’s persistent exchange rate alignments will be used by the U.S. Treasury to set an example of its commitment to aggressively and vigilantly monitor and combat unfair currency practices. Should that be the case, the U.S. Treasury would address their concern via bilateral engagements and, if Switzerland does not take sufficient measures to solve the issue within a year’s time, potentially use tariffs to increase the price of Swiss imports into the U.S.

If this were to eventuate, the impact for the alpine country would be significant. According to the Federal Customs Authority, the total amount of Swiss exports reached CHF210 billion in 2016 of which CHF35 billion were exported to the US. While this number doesn’t seem to be significant in comparison with the CHF94 billion shipped to the Eurozone, the picture changes when looking at net exports. Having imported goods worth CHF110 billion from the Eurozone in 2016, Switzerland actually runs a trade deficit with the Eurozone, in contrast to the trade surplus with the U.S. The U.S. also marked the fastest growing export market for Switzerland last year with an increase of more than CHF4 billion, primarily driven by the pharmaceutical industry. Imports from the U.S. rose last year, but at a slower pace of CHF3 billion which, as a result, increased the trade surplus with the United States further.

Should this trend continue, Switzerland runs the risk of exceeding the defined threshold of a USD20 billion trade surplus, the only criteria in the report where Switzerland doesn’t tick the box. If Switzerland is deemed a currency manipulator, the more prudent path for the SNB may be to allow the Swiss Franc to appreciate in order to avoid the implementation of tariffs on Swiss exports to the U.S. This may be the lesser of two evils and will allow the Swiss to avoid the wrath of the U.S. Treasury.

Bond markets are behaving like the Trump reflation trade isn’t going to happen, whilst equities seem to believe in 4% GDP growth 4evah. Today I’m joined by M&G multi-asset fund manager and author Eric Lonergan to discuss Trump’s first hundred days in office, and to think about this seeming disconnect in asset valuations.

This week it’s the high yield market’s turn under the microscope, as James Tomlins joined me this morning on BVTV. And there was plenty to discuss:

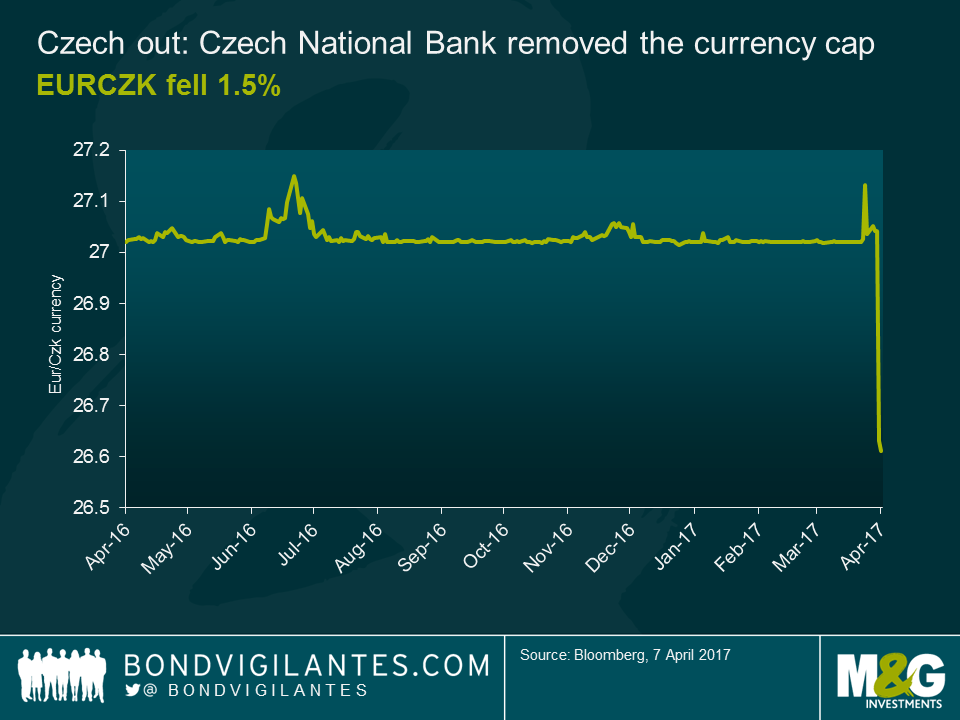

The Czech National Bank (CNB) has removed its cap against the Euro, which I blogged about earlier this year. Though the signs had been pointing to an early removal (headline inflation had been within the target range since October last year and the CNB had hardened its signalling language), the timing of yesterday’s move at the central bank’s extraordinary meeting did come as a surprise. Currency appreciation post the event has been fairly muted, with the CZK rallying 1.5% against EUR on the day.

The CNB is likely breathing a sigh of relief; the Czech Republic is an export orientated economy and thus excessive appreciation would hamper this somewhat. But where does it go from here? As I mentioned in my previous blog, when the cap was in force, the CNB would not permit appreciation beyond the level at which they intervened; approx. EURCZK 25.7 (the market closed at EURCZK 26.6), so this is perhaps a reasonable expectation regarding the appreciation ceiling.

The rates space is also interesting. The removal of the cap is a monetary tightening, with CNB governor highlighting in his press conference that “ending the cap was the first step toward gradual policy tightening”. With the market pricing in the expectation of this, the sell-off in the Czech sovereign bond curve (alongside the currency appreciation) is perhaps now pricing in more of a tightening that the CNB should have liked.

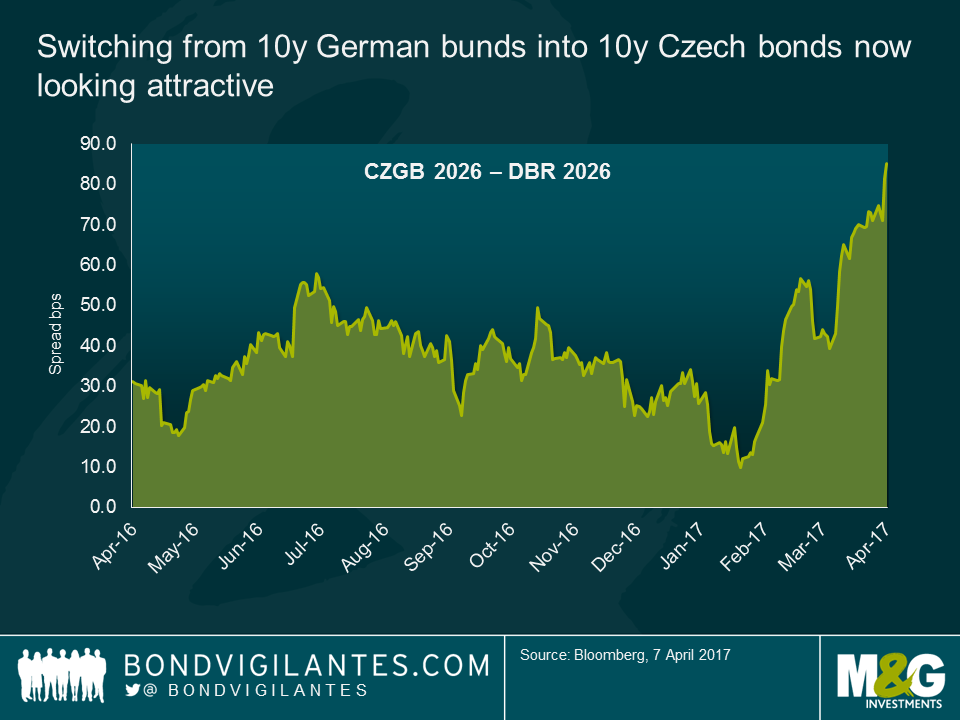

If the CNB monetary tightening is to be a gradual measured response, instead of the bear steepening that the market may be assuming, this now becomes appealing from a relative value perspective – see the graph below – but also on a currency hedged basis.

The final aspect to bear in mind is that Czech bonds will be held in the main bond benchmark indices from the end of this month. CZGBs will be included in the GBI-Emerging Market index on 28th April with a weight of 3.3%. This will create demand for the bonds for those using this index as their passive or active benchmark which will put some small appreciation pressure on the currency. Bigger moves could however occur in the opposite direction and the currency could of course depreciate from here, should the large speculative investor flows (estimated at $65bn) anticipating the removal of the cap now dissipate, which would lighten the CNB’s workload somewhat.

In maintaining the currency cap, the CNB accumulated €47.8bn of reserves which, according to its website, it will continue to invest in “high quality, safe instruments” and “will not sell the returns on those reserves for the foreseeable future”. There will be further interesting times ahead for the CNB who – either way – stand ready to intervene against extreme exchange rate fluctuations.

It is hard to remember a time when there was so much disagreement around the outlook for corporate bond markets and risk assets. Some investors remain sceptical about the underlying strength of the rally and are uneasy at the pace at which secular stagnation concerns were washed away by the election of Donald Trump. Other investors, hesitant to hold cash or in negative yielding short-dated government debt, have rotated in credit markets for fear of missing out on any potential upside returns.

With the FOMC hiking rates in March, doubts about the continuation of the reflation trade are now starting to grow. These doubts are being reflected in markets, and cracks are beginning to show beneath the surface. The following charts represent early warning signs that the momentum in risk assets may be starting to reverse.

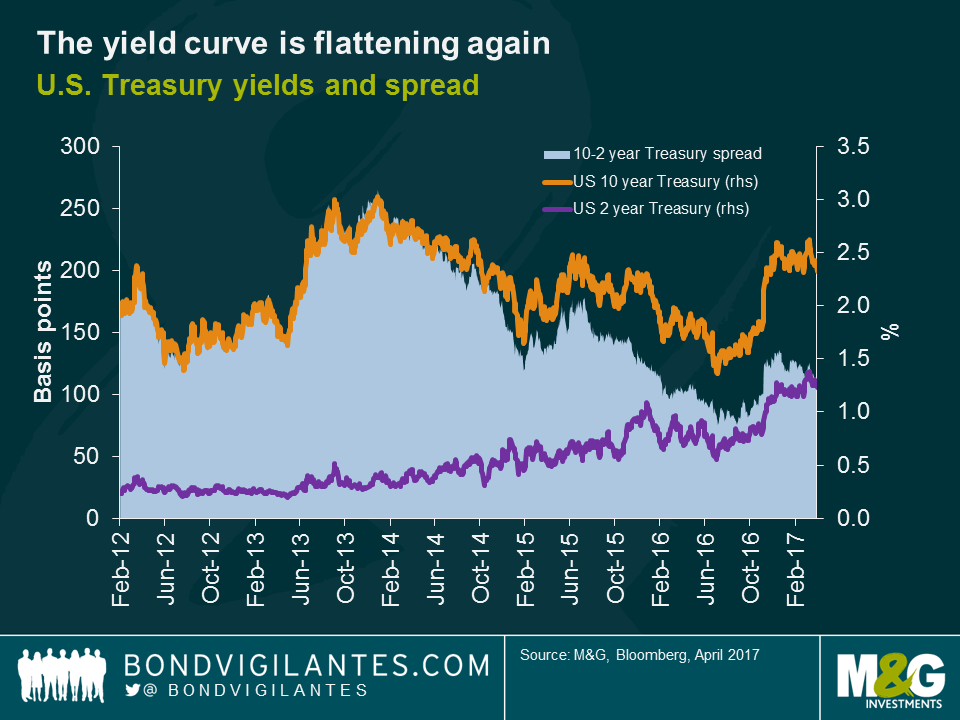

Firstly, the U.S. yield curve has flattened over the course of 2017 with the 10-2 year Treasury spread at a level not seen since the early days after Donald Trump’s election win. At 110 basis points, the yield curve has now been flattening for almost three months. Whilst the move higher in yields at the short-end of the curve largely reflects the FOMC’s interest rate hike and higher inflation, the stubbornness of the 10-year yield to rise from a 2.30-2.60% channel suggests that long-term growth and inflation expectations remain subdued.

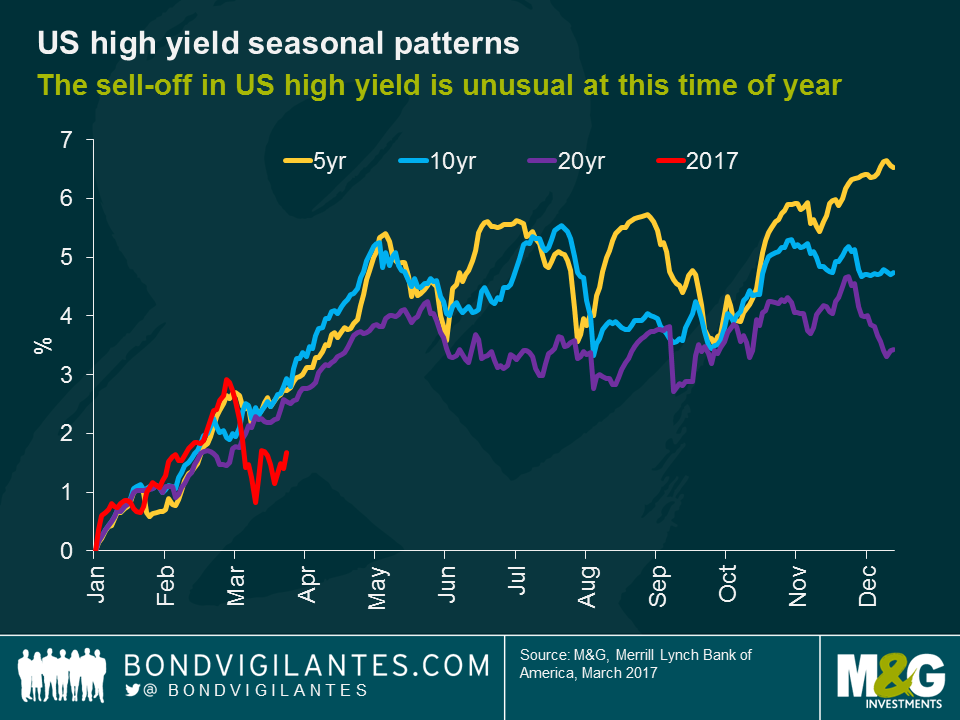

Secondly, the sell-off in US high yield is unusual for this time of year. That 5, 10, and 20 year median seasonal returns show typically the US high yield market does pretty well until around May/June, before returns tend to trend sideways until the end of the year. Looking at the 5 year seasonal pattern, the market tends to bottom out every two months from June until October, before rallying into year end. This is something I’ve previously written about here.

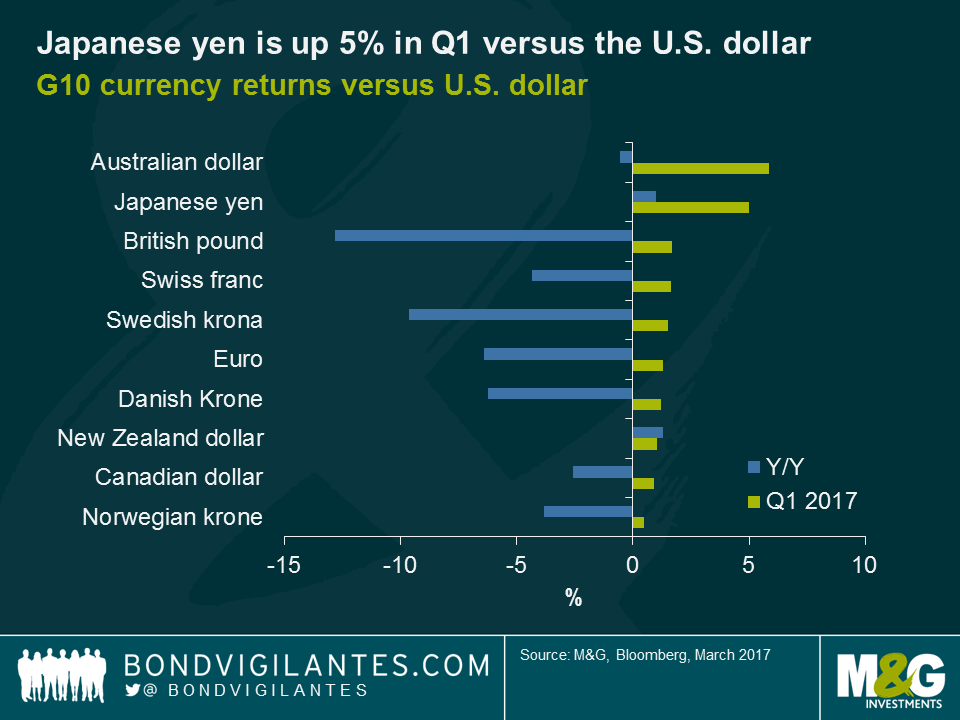

Finally, the yen has been the surprise performer in G10 currency markets so far this year. Over the first quarter of 2017, the yen is up 5% versus the U.S. dollar and 2.5% on a real effective exchange rate basis. The driver of USD/JPY in particular has been U.S. developments, with the failure of the healthcare bill raising questions in currency markets about the ability of Donald Trump to implement his fiscal agenda, resulting in a decline in USD. Japanese investors have also unwound a large amount of foreign bond purchases ahead of fiscal year-end.

Despite the rise in yen in Q1, most professional forecasters continue to expect the yen to weaken versus the dollar as interest rate differentials are expected to grow wider between Japan and the U.S. The Bank of Japan (BoJ) is expected to continue to maintain its policy of yield curve control while the Fed is expected to continue to hike rates. However, there are a number of reasons that these expectations for Japanese monetary policy may be adjusted. Firstly, the Japanese economy is performing well with incoming economic data confirming higher industrial activity. Secondly, the labour market is extremely tight, with an unemployment rate of only 2.8%. This bodes well for both wage and consumption growth going forward, suggesting increased spending on consumer durables. Thirdly, fiscal policy should prove to be mildly expansionary in 2017, with spending measures focused on public investment and cash transfers to households. Finally, Japanese export industries will continue to perform well given the upswing in the global growth cycle and continued strong demand from China and the U.S. The BoJ would most likely react to the improving economic outlook by raising their target for long-term bond yields from 0% to 0.1-0.2% later this year. Should the global upswing remain intact, and if inflation picks up due to increasing wages, then the BoJ could be the surprise central bank in 2017.

Looking ahead, international political risks will likely continue to be a focus for bond markets. French elections and the ability of President Trump to enact his ambitious political agenda are likely to be responsible for short-term swings in bond yields. Despite this, the solid global economic growth outlook suggests a bearish outlook for government bond markets in Q2 in the US and Europe. In the US, the market is under-pricing the possibility of a more hawkish Fed and higher domestic inflation. In Europe, given the improving macroeconomic environment and higher inflation readings, the European Central Bank may look to shift its rhetoric on future action and look to begin more aggressive asset tapering, leading to higher long-end rates and a steepening in yield curves. Throw in to the mix the potential for the BoJ to surprise, suddenly three major central banks are withdrawing stimulus at a faster pace than was previously anticipated. If this type of scenario plays out, it is difficult to see how risk assets like high yield can continue to generate the returns that investors have experienced since the U.S. election result.

I’m three months into my attempt to climb 100 iconic hills, bergs, kops and mountains on my bike in 2017. So far I’ve ridden up 28 of them, mostly in torrential rain.

The purpose of all this is to raise money for Cancer Research UK, as part of the asset management industry’s goal of donating over £1 million to the great cause this year. So far we’ve collectively raised over £300,000 as part of CASCAID, through a wide variety of events and challenges. You can read about some of these efforts and the work of CASCAID and Cancer Research UK on the link below.

http://www.cascaidcharity.com/

As a reminder, I’m cycling up 100 famous climbs featured mainly in Simon Warren’s excellent series of books called things like “100 Greatest Cycling Climbs” and “Another 100 Greatest Cycling Climbs”. There’s also room for a few wildcards – hills not in any of the books but that are worthy contenders, for example The Peak in Hong Kong which I rode in January (in a rainstorm).

You’ll find the evidence of all the climbs on Strava, and here’s a list of all the twenty eight climbs that I’ve done so far:

What’s next?

Having ticked off most of the hills near to London, I’m going to have to get a bit more organised and plan some weekends in the Peak District, Yorkshire and the other hilly bits of the UK for the rest of the year. I have to ride up 2 hills per week to stay on track. I’m right on schedule now, but the low hanging fruit has gone. I’m also nervous that northern hills might be steeper and longer than our soft, southern hills. Having had some company and moral support from Ali, Jeff and Pete on a few rides so far (thanks!), I’ll be making sure I round up some company for the rest of the year. If any readers fancy tackling a hill or two with me, give me a shout. I’m hoping to ride the Cat and Fiddle climb near Macclesfield with M&G’s answer to Phillipe Gilbert, Chris Elliott, at the end of June (New Order are playing at the old Granada Studios that very evening, by some strange coincidence…).

As a final incentive to donate, if I raise another £500 for Cancer Research UK, I will invest in the ultimate of “marginal gains” and shave my legs. Sadly I won’t be able to attend the workshop below at Look Mum No Hands, but if anyone has any “pro-tips”, let me know…

The German federal election in September still seems far away. However, for the first time in years, it appears possible that Angela Merkel could actually lose the election. Martin Schulz, Chancellor candidate and chairman of the Social Democratic Party, is having some early signs of success in the polls and is gaining momentum. As a result, investors in European (and UK) debt might want to refresh their memory of Schulz’s five years as President of the European Parliament.

In 2011 and 2012, in the midst of the Eurozone debt crisis, Schulz repeatedly advocated debt mutualisation in the form of Eurobonds, i.e. sovereign debt issued jointly by all member countries of the Eurozone. The rationale behind this idea is clear: troubled peripheral countries would benefit from lower funding costs. As confidence in the ability of the ECB to do “whatever it takes” to support the euro area increased in debt markets, peripheral sovereign bond yield spreads narrowed. Over the past year peripheral risk premiums have generally trended upwards, albeit at a much slower pace than in 2011/2012, suggesting that Schulz’s position could become relevant again.

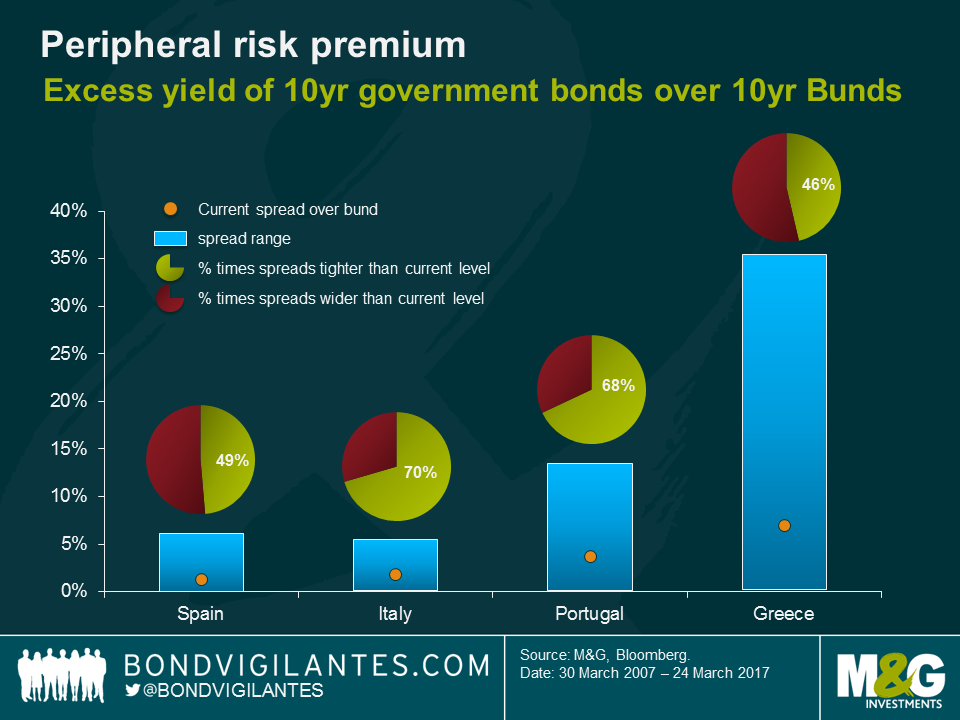

Looking at historic spread levels, the valuations of bonds issued by periphery Eurozone nations indicates heightened stress in some bond markets. The spread of Spanish 10-year government bonds over 10-year Bund yields is around 1.3%, which is close to the median over the past 10 years. The yield spread of Italian 10-year bonds is only half a percentage point higher (1.8%), which doesn’t seem much in absolute terms. However, compared to its 10-year history things look more severe: 70% of the time the spread has been tighter than today. The situation is similar for Portugal; over the past ten years its yield spread has been tighter than its current value of 3.7% for more than two thirds of the time. The Greek excess yield over Bunds of 7.0% is the highest in the periphery, but it’s actually below its own historical median. By this measure, the situation is most relaxed in Greece – a sentence one doesn’t read very often.

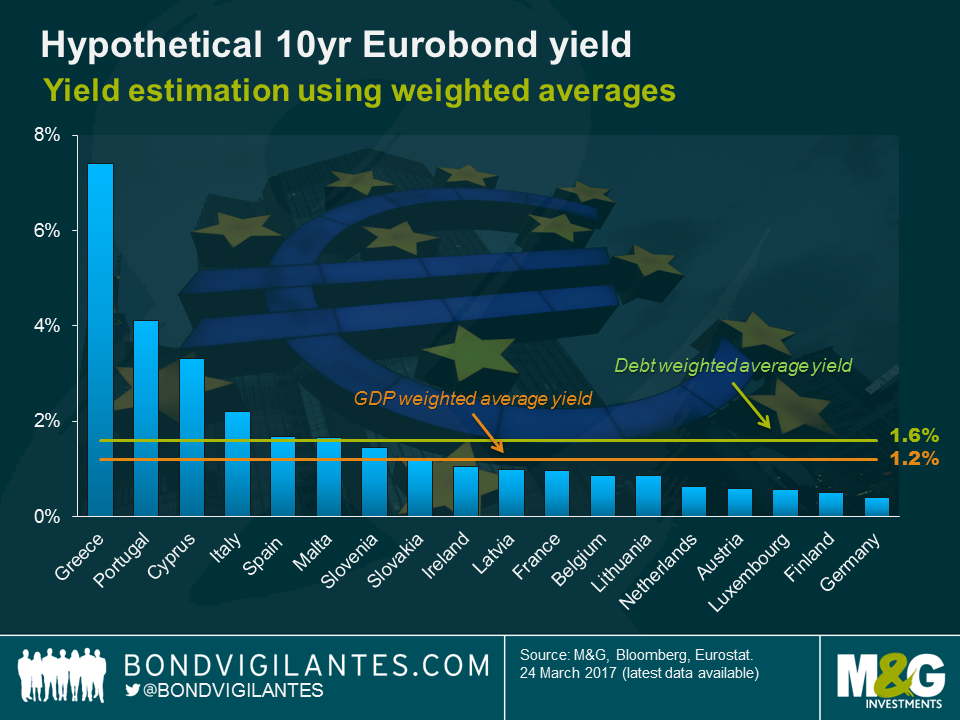

For the sake of argument, assume Schulz’s policy of joint 10-year Eurobonds is introduced. Peripheral yield premiums would disappear immediately, but what Eurobond yield should investors expect? All Eurozone countries, apart from Estonia, have government bonds outstanding, allowing us to calculate weighted average 10-year yields, which seems like a reasonable starting point. Here we have used two weighting factors: GDP and debt level. The GDP-weighted yield accounts for the economic power of countries and thus for their ability to collect tax revenues and pay back debt. A large weight is assigned to Germany due to its high GDP. Consequently, this drags the average yield down to 1.2%, which is pretty much at the same level as the current 10-year yield of Slovakia. If this was the actual yield of Eurobonds, funding costs for Germany at the 10-year point would roughly triple, whereas yields for peripheral countries would decrease meaningfully. In contrast, the debt weighted yield reflects the degree of financial leverage and the credit quality of the countries. Due to its high debt burden, the weight of Italy is large and pushes the average up to 1.6%, which is in line with Malta’s current 10-year yield and four times higher than the German 10-year yield.

Arguably the GDP and debt-weighted estimates of hypothetical Eurobond yields are too high as they ignore the enhancement in market depth and liquidity. Creating one class of joint Eurobonds would fundamentally transform the fragmented European government bond market and make it a lot more commoditised. Particularly smaller countries, whose local government debt markets might have been ignored by many investors, would benefit greatly from tapping into a deep and liquid Eurobond market.

It is unlikely that Eurobonds are introduced any time soon. Apart from the potential moral hazard created by debt mutualisation and possible conflicts with the Treaty of Lisbon, there are also major political obstacles in Germany. Chancellor Merkel, Finance Minister Schäuble and other members of the conservative parties CDU and CSU have steadfastly rejected Eurobonds in the past. And even if Schulz was able to organise a stable parliamentary majority without the CDU/CSU block after the election, would he really want to reopen the debate about Eurobonds? Unsurprisingly, the idea of Eurobonds is not exactly popular in Germany, which might explain why he hasn’t brought it up lately, now that he is running for office in Berlin. In this regard, he seems to be in line with Germany’s first post-war Chancellor Adenauer who famously said: “What do I care about my chitchat from yesterday […]”.

After a momentous week for the UK last week, Matthew Russell joined me this morning to discuss what the much-anticipated start of Brexit negotiations hold for gilt markets. Tune in to our latest edition of BVTV to hear us discuss:

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.