Cracks in the reflation trade

It is hard to remember a time when there was so much disagreement around the outlook for corporate bond markets and risk assets. Some investors remain sceptical about the underlying strength of the rally and are uneasy at the pace at which secular stagnation concerns were washed away by the election of Donald Trump. Other investors, hesitant to hold cash or in negative yielding short-dated government debt, have rotated in credit markets for fear of missing out on any potential upside returns.

With the FOMC hiking rates in March, doubts about the continuation of the reflation trade are now starting to grow. These doubts are being reflected in markets, and cracks are beginning to show beneath the surface. The following charts represent early warning signs that the momentum in risk assets may be starting to reverse.

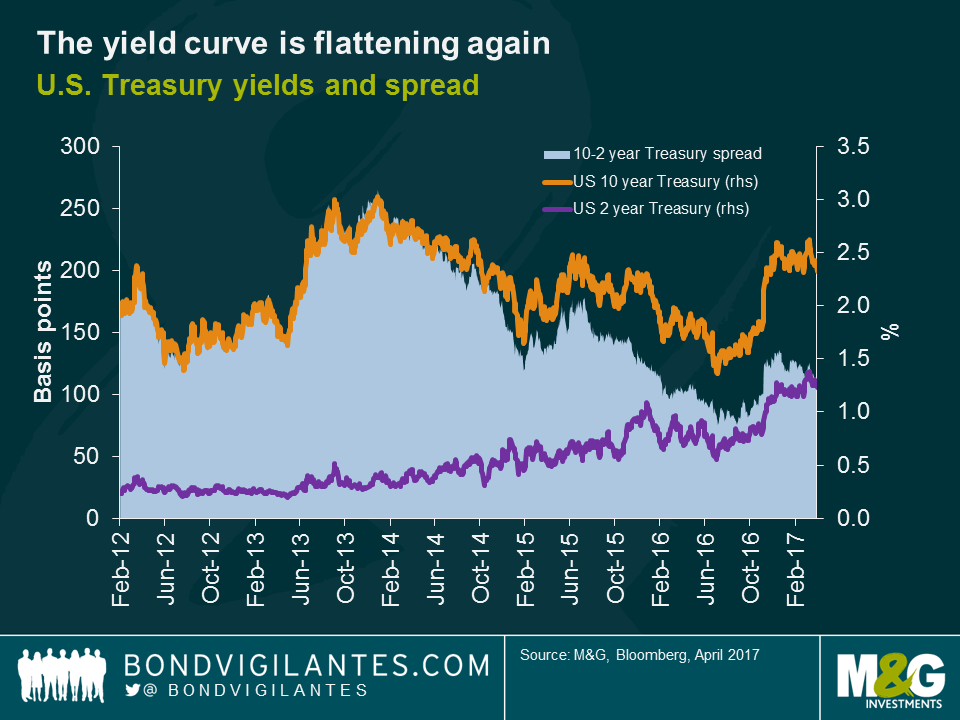

Firstly, the U.S. yield curve has flattened over the course of 2017 with the 10-2 year Treasury spread at a level not seen since the early days after Donald Trump’s election win. At 110 basis points, the yield curve has now been flattening for almost three months. Whilst the move higher in yields at the short-end of the curve largely reflects the FOMC’s interest rate hike and higher inflation, the stubbornness of the 10-year yield to rise from a 2.30-2.60% channel suggests that long-term growth and inflation expectations remain subdued.

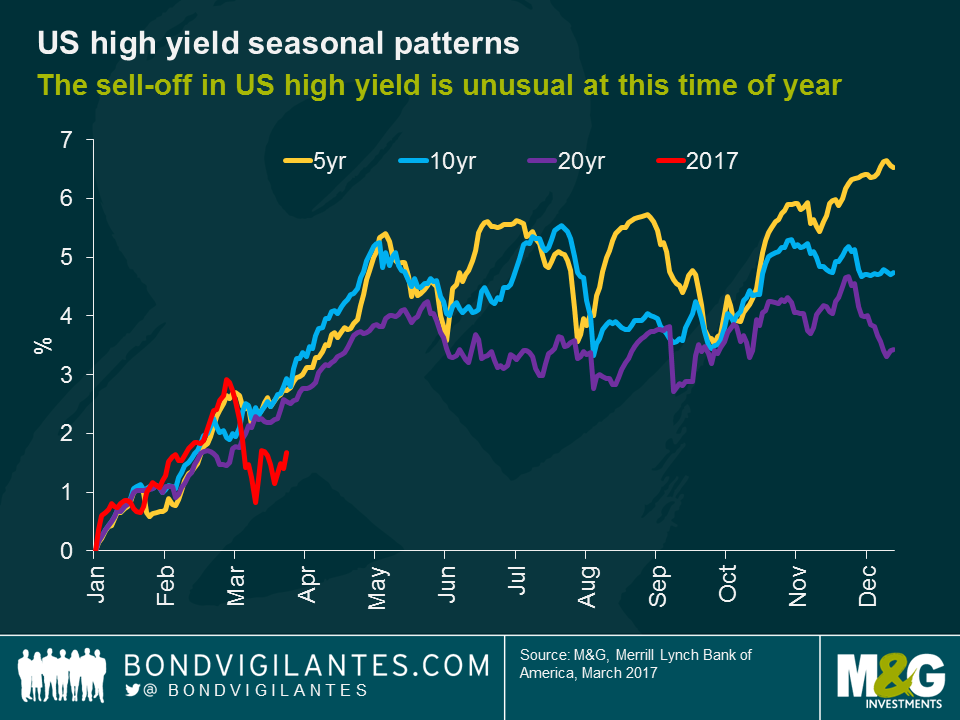

Secondly, the sell-off in US high yield is unusual for this time of year. That 5, 10, and 20 year median seasonal returns show typically the US high yield market does pretty well until around May/June, before returns tend to trend sideways until the end of the year. Looking at the 5 year seasonal pattern, the market tends to bottom out every two months from June until October, before rallying into year end. This is something I’ve previously written about here.

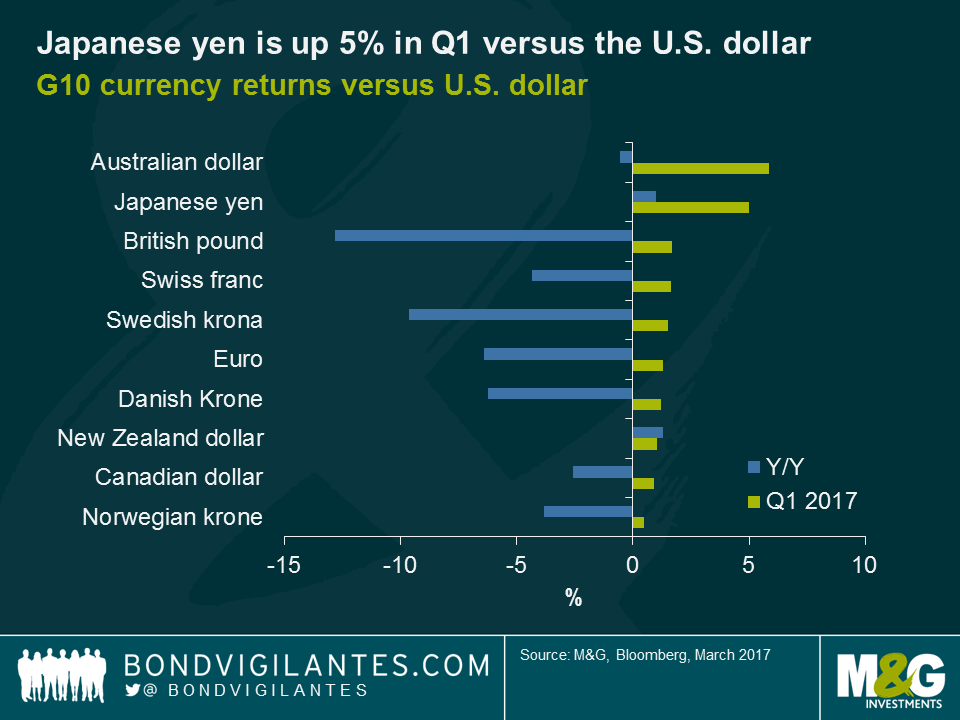

Finally, the yen has been the surprise performer in G10 currency markets so far this year. Over the first quarter of 2017, the yen is up 5% versus the U.S. dollar and 2.5% on a real effective exchange rate basis. The driver of USD/JPY in particular has been U.S. developments, with the failure of the healthcare bill raising questions in currency markets about the ability of Donald Trump to implement his fiscal agenda, resulting in a decline in USD. Japanese investors have also unwound a large amount of foreign bond purchases ahead of fiscal year-end.

Despite the rise in yen in Q1, most professional forecasters continue to expect the yen to weaken versus the dollar as interest rate differentials are expected to grow wider between Japan and the U.S. The Bank of Japan (BoJ) is expected to continue to maintain its policy of yield curve control while the Fed is expected to continue to hike rates. However, there are a number of reasons that these expectations for Japanese monetary policy may be adjusted. Firstly, the Japanese economy is performing well with incoming economic data confirming higher industrial activity. Secondly, the labour market is extremely tight, with an unemployment rate of only 2.8%. This bodes well for both wage and consumption growth going forward, suggesting increased spending on consumer durables. Thirdly, fiscal policy should prove to be mildly expansionary in 2017, with spending measures focused on public investment and cash transfers to households. Finally, Japanese export industries will continue to perform well given the upswing in the global growth cycle and continued strong demand from China and the U.S. The BoJ would most likely react to the improving economic outlook by raising their target for long-term bond yields from 0% to 0.1-0.2% later this year. Should the global upswing remain intact, and if inflation picks up due to increasing wages, then the BoJ could be the surprise central bank in 2017.

Looking ahead, international political risks will likely continue to be a focus for bond markets. French elections and the ability of President Trump to enact his ambitious political agenda are likely to be responsible for short-term swings in bond yields. Despite this, the solid global economic growth outlook suggests a bearish outlook for government bond markets in Q2 in the US and Europe. In the US, the market is under-pricing the possibility of a more hawkish Fed and higher domestic inflation. In Europe, given the improving macroeconomic environment and higher inflation readings, the European Central Bank may look to shift its rhetoric on future action and look to begin more aggressive asset tapering, leading to higher long-end rates and a steepening in yield curves. Throw in to the mix the potential for the BoJ to surprise, suddenly three major central banks are withdrawing stimulus at a faster pace than was previously anticipated. If this type of scenario plays out, it is difficult to see how risk assets like high yield can continue to generate the returns that investors have experienced since the U.S. election result.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox