Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

With the UK’s vote for Brexit, Trump’s election, and the rise of Le Pen in France, it feels as if there is a backlash against the “Washington Consensus” and globalisation. Stephen King, economic adviser at HSBC has made this the topic of his latest book, “Grave New World: the end of globalisation, the return of history”.

In this short video, the latest in our series of interviews with authors of interesting books on economic themes, we discuss the reversal of trends that we’d started to take for granted, and ask what fills the vacuum if western institutions fall away.

You can also win one of five copies of Stephen King’s book by answering this question: in which year did China become a member of the World Trade Organisation (WTO)?

Enter via this link please bondteam@bondvigilantes.co.uk. (This competition is now closed to entries)

Entries closed at noon UK time on Wednesday 31 May 2017.

The results are in

The answer to the recent Bond Vigilantes competition question:

In which year did China become a member of the World Trade Organisation (WTO)? was 2001.

Congratulations to our five winners:

John McLaughlin – Brewin Dolphin

Adam McCormack – The Shaw Sheet

Niall Clifford – Mercer

Paul Boland – BCA Research

Neil Berry – East Riding of Yorkshire Pension Fund

Your prize of a copy of Stephen King’s book “Grave New World: the end of globalisation, the return of history” is on its way out to you.

Join me, Laura Frost, on BVTV to discuss the political uncertainty surrounding the Trump presidency and Brazilian leader Michel Temer.

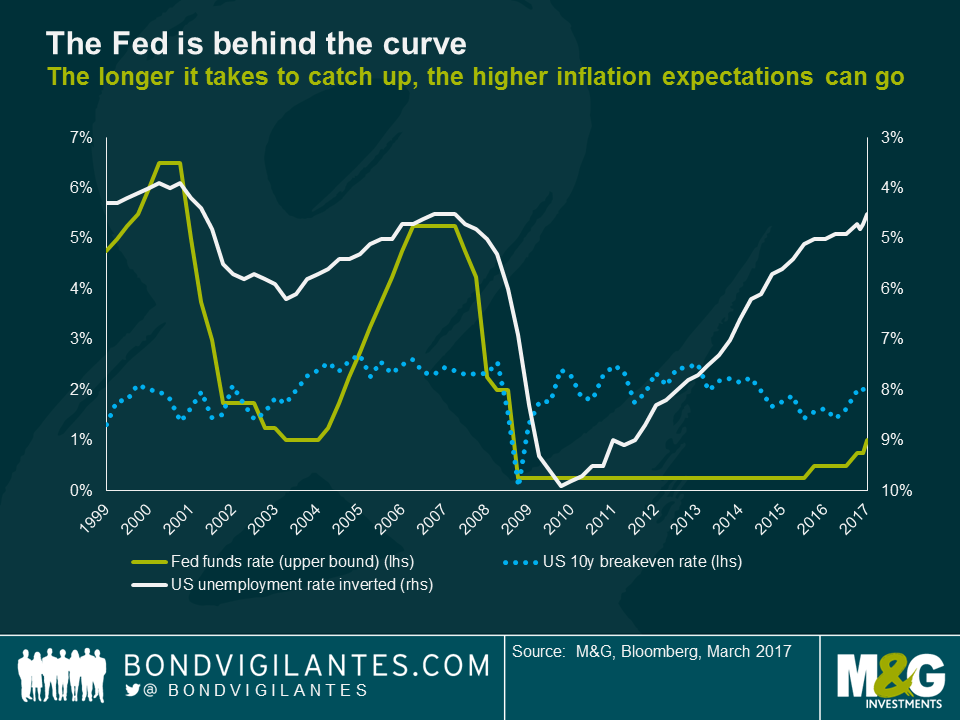

The last time the US had an unemployment rate below 5% and inflation expectations around 2%, the Fed funds rate was above 5% and had been aggressively hiked in the preceding period. Yellen’s Fed has been happy to let rates stay low amongst a tight and tightening labour market because wage growth has been lower than one would expect for a jobs market as healthy as this one. So, slow growth of wages must illustrate some underappreciated slack at work.

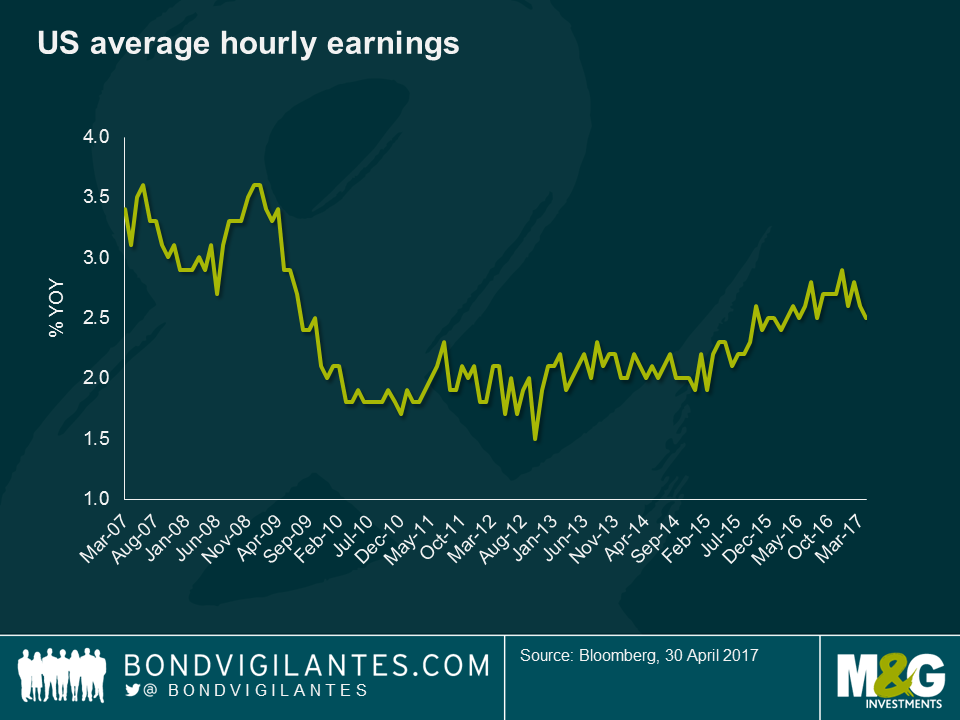

The monthly bell-weather of wages in the U.S. is average hourly earnings (AHE). This takes the aggregate wage growth of the US labour force and as the chart below shows has been curiously and worryingly (for central bankers) flat-lining in the years since the Great Financial Crisis. However, this measure does have a flaw that might lessen its signalling strength of labour market tightness: because it is an average of the aggregate wages of the US, it over-weights the higher paid minority of the population. Further, as younger people enter the workforce and older people retire from it, AHE would be biased lower, for example.

We have been watching the Atlanta Fed wage tracker recently, as a potentially better measure of wage growth given AHE’s biases. This measure is based on a matched micro sample of workers, whereby their wage growth is only measured if they were recorded in the same month a year ago. Thus, it avoids many of the compositional flaws of AHE. Furthermore, it is a median, rather than a mean, measure, which means that it will not over-weight the highest paid to the same extent as AHE. On top of this, the Atlanta Fed wage measure excludes the highest paid cohort from the measure. This is key today, because the highest paid have not been getting pay rises to anything like the same extent as the lower earners. Workers at Walmart, Home Depot, MacDonald’s and those citizens on minimum wages are those that are seeing the most significant wage increases. The Atlanta wage measure stands at a much healthier 3.4% today, having started 2016 at 2.2%, and shows clear signs of heading in an upward trajectory. For job movers, wages are rising at 4.1%. For workers of prime age, wages are rising at 3.8%, and for workers with a college degree, they are rising at 3.7%.

What growth rate of AHE would give the Fed confidence that the labour market is strong enough, and the outlook for consumption is strong enough, for the next series of hikes? We now know from experience that c.2.5% is not enough. But surely wage growth of more than 3% is? At 3.5% I would expect that the Fed has the confidence to signal an upward path of rate hikes. The point is, we are already there on one measure of wage growth, and we are probably only a few months away on the other, flawed but broader, one. Couple these tentative positive signs in wages with the fact that so much household debt is fixed, and the vast majority of it being fixed for more than 23 years (see this blog from earlier this year), and you can see why the Fed is content to press on with its hiking cycle.

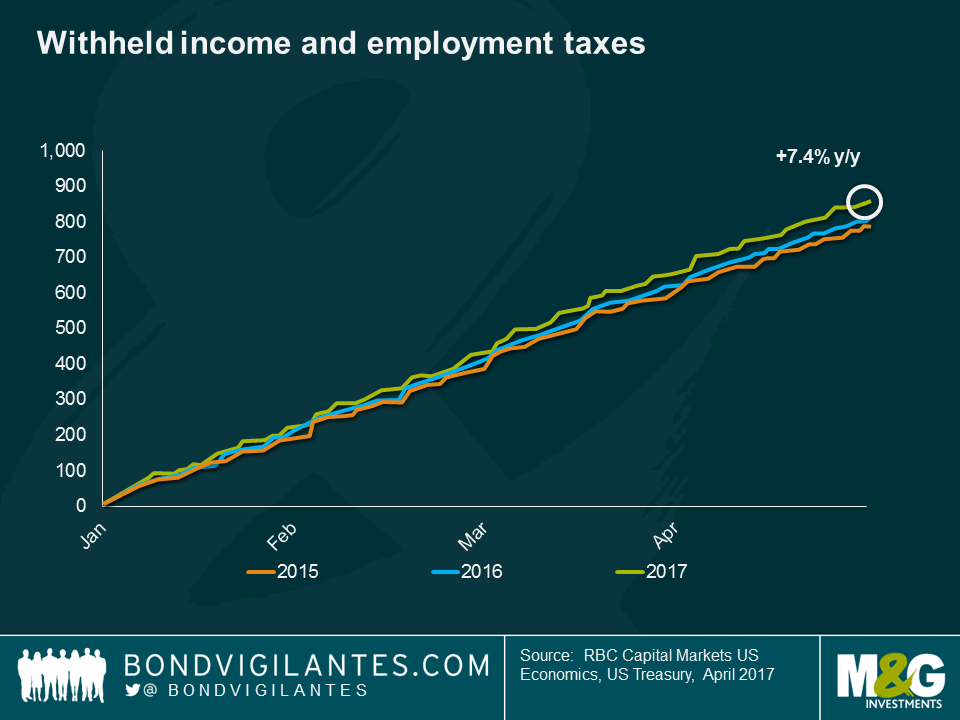

We need to acknowledge that both of these wage measures have flaws and biases. One data point that is being closely monitored by economists at Deutsche Bank and Royal Bank of Canada is withheld income and employment taxes. These are the amounts of tax taxed at source where employers send cash salaries net of taxes to staff and send the tax amounts to the authorities. This happens every day of the year, and so it does need smoothing to be applied. But Joe La Vorgna at Deutsche has long followed this data as it does not get revised and is obviously very timely. We have borrowed this last chart from Tom Porcelli at RBC, who came in to the office last week to give us his views. Currently withheld tax receipts are up 7.4% on the same point of 2016. Either more people are getting jobs, or people are being paid more. Or both.

The Eurovision song contest may be over for another year, but Europe’s capacity to surprise could well continue. Tune in to the latest edition of BVTV, where Anjulie Rusius joined me to discuss:

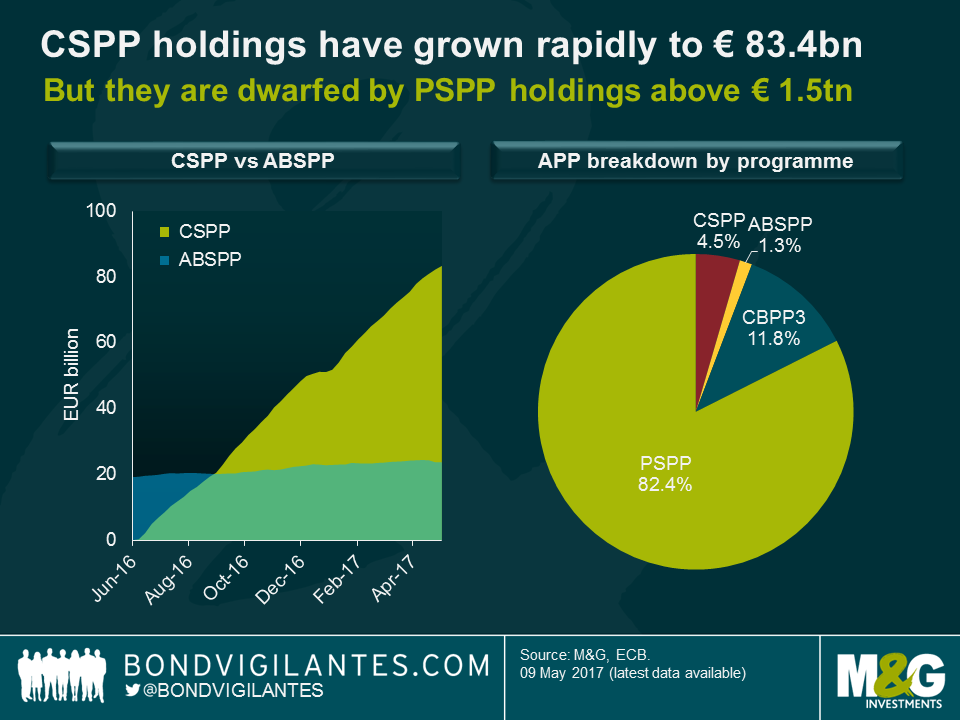

European investment grade (IG) corporate bond spreads are now more than 40 basis points tighter than in early March 2016, before the European Central Bank (ECB) announced the expansion of its quantitative easing programme into the € IG corporate bond space. The technical tailwind provided by monthly bond purchases to the tune of around €7.5 billion from June onwards under the ECB’s corporate sector purchase programme (CSPP) has certainly been a key contributor to the strong performance of the asset class.

The ECB – through six national central banks within the Eurosystem, to be precise – has built up a CSPP balance sheet of around €83.4 billion worth of corporate bond holdings. As impressive as this number may sound, one has to recognise that the CSPP is only one of four programmes within the ECB’s expanded asset purchase programme (APP). While the CSPP has easily overtaken the asset-backed securities purchase programme (ABSPP) in terms of volumes, it is dwarfed by the third covered bond purchase programme (CBPP3) and particularly by the public sector purchase programme (PSPP). The €1.5 trillion of PSPP holdings account for more than 80% of total APP holdings, the CSPP makes up less than 5%.

In December last year the ECB announced an extension of the APP but a reduction of total monthly purchase volumes from €80 billion to €60 billion from April 2017 onwards. The big question for corporate bond investors like us was whether the ECB would trim CSPP purchases in line with overall APP purchases or not. Based on the ECB’s weekly financial statements, we calculated rolling four-week purchase volumes – a proxy for monthly purchases – from June 2016 onwards. The chart below reveals a pronounced seasonal pattern. Purchases were dialled back significantly in August and, even more so, in December. This is not particularly surprising, considering how bond market liquidity tends to dry up at the height of summer and between Christmas and New Year. More interesting is the recent decline in purchase volumes from January to April 2017. APP purchases are now at around €60 billion per month, and thus consistent with the ECB’s earlier announcement. Importantly, the tightening in monthly CSPP purchases to currently €5.6 billion seems to be happening in a proportional fashion with overall APP tapering.

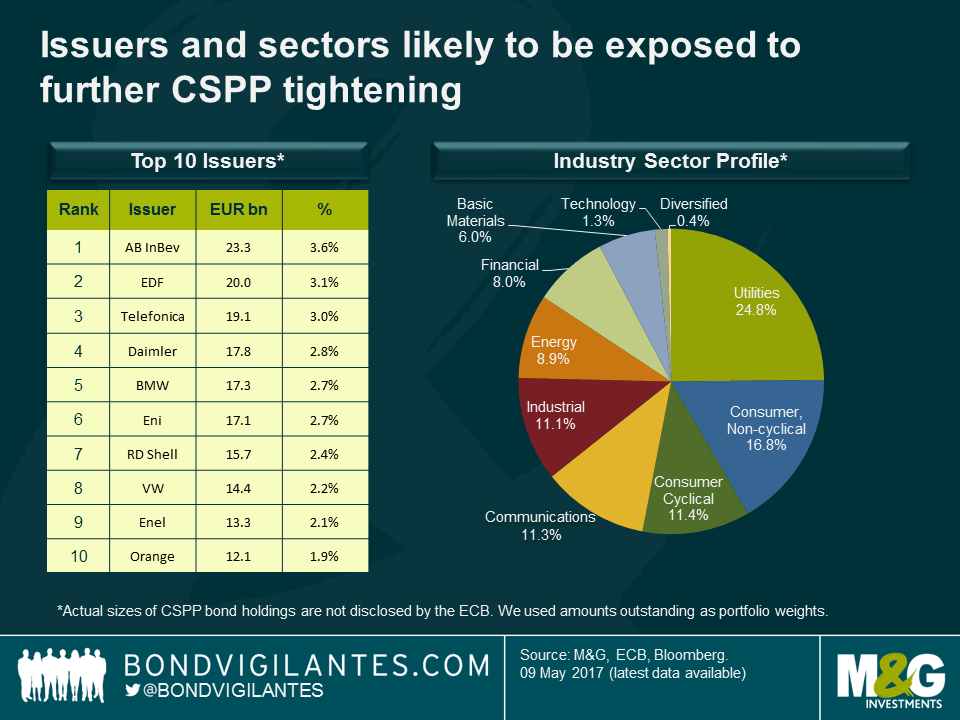

Taking it one step further, we had a look at individual corporate bond issuers and industry sectors whose valuations have so far benefitted from the CSPP but might become vulnerable when purchases get curtailed further or phased out entirely. This analysis is less straightforward than one might think, though. While the total volume of purchases and the identity of the 912 corporate bonds bought under the CSPP are disclosed by the ECB and national central banks, respectively, the holding sizes are not. We are therefore unable to calculate accurate portfolio weights for individual bonds, issuers or sectors. In our analysis we assumed that the ECB bought corporate bonds in proportion to their amounts outstanding – not particularly likely but nonetheless our best guess.

According to our analysis, the main beneficiaries of the CSPP amongst corporate bond issuers have been Anheuser-Busch InBev, EDF and Telefonica, followed by Daimler and BMW. For example, all 18 AB InBev bonds on the list of CSPP holdings have a combined amount outstanding of €23.3 billion, which is 3.6% of the total amount outstanding of all corporate bonds held by the ECB. With regards to industry sectors, utilities, consumer non-cyclicals and consumer cyclicals have attracted most CSPP demand. All else being equal, with falling and eventually disappearing CSPP purchases, the demand and supply dynamics for these issuers and sectors are likely to deteriorate, which could potentially lead to underperformance against the wider € IG corporate bond universe. However, it is important to point out that these technical considerations are one factor influencing bond valuations. The credit and sector fundamentals are at least as important, particularly for investors with longer investment horizons.

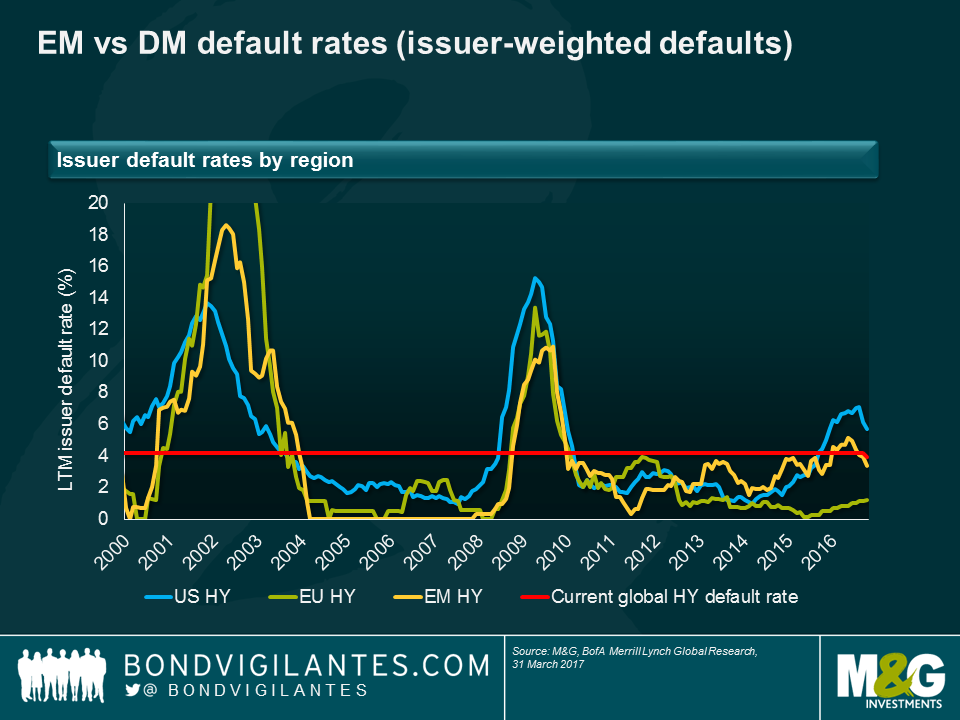

There are a lot of misconceptions about defaults in emerging market (EM) debt. Too often, EM corporates are either considered ‘serial defaulters’ compared with their developed market peers, or seen as a single and homogeneous geography. In reality, default rates follow economic cycles, and having a regional, if not country, approach to default risk remains paramount due to different jurisdictions and various recovery values between regions and countries. Another common misconception is that high yield default risk is higher in EM than in Europe or the US. Looking at the chart below, EM high yield corporate defaults are very much in line with those of European high yield or US high yield. During the last global financial crisis in 2008-09, the EM high yield segment had a lower peak in the default rate than its developed market counterparts.

In this edition of the M&G Panoramic Outlook, Charles De Quinsonas provides an insight into EM corporate default risk within the ever-expanding EM corporate bond universe. In his view, improving EM macroeconomic fundamentals and an expected benign default rate environment continue to offer opportunities to find attractive yields in emerging market debt markets.

I have to be honest here. Even though we sponsor it, whenever I go to the Chelsea Flower Show I am reminded of bleak Sundays being dragged around garden centres as a child, hoping there is at least a pets section with some rabbits or something in it. Or some swings. Nevertheless, many people love flowers and plants.

So, in support of CASCAID, the UK asset management industry’s effort to raise over a million pounds for Cancer Research UK, I’ve got hold of two gold dust tickets for the RHS Chelsea Flower Show on Wednesday 24th May 2017. These are especially rare and valuable as they are only available for members of the RHS on this date, and in any case sell out quickly.

It’s difficult to work out how to maximise the amount of cash we raise for Cancer Research UK. We could run a raffle or auction for the tickets, but that makes it tricky if we want people to increase the value of their giving through Gift Aid. So I’m going to simply rely on people’s goodwill and ask that if you enter the competition you might consider making a donation (a fiver? Tenner?) to the fantastic cause through my existing Cancer Research UK fund raising page. Whether you donate or not will honestly make no difference to your chances of winning. But karma.

To win the two tickets, valid from 8am to 8pm on Wednesday 24th May, please name the plant shown in the photo (chosen by our emerging market bond fund manager Claudia Calich who will be volunteering at the M&G garden at times during the show, so please go and say “hi”) and send the correct answer to bondteam@bondvigilantes.co.uk by midday UK time on Wednesday 17th May 2017. Good luck!

This competition is now closed.

EU officials are breathing their latest sigh of relief this morning, after French voters opted for centrist candidate Emmanuel Macron over far-right rival Marine Le Pen in yesterday’s second round presidential elections. Markets will now turn their attention to whether the incoming president can assemble a parliamentary majority without the benefit of an established party behind him.

Tune in to our latest edition of BVTV as I discuss market reaction to Macron’s victory, and implications of president Trump’s second time lucky attempt at repealing Obamacare.

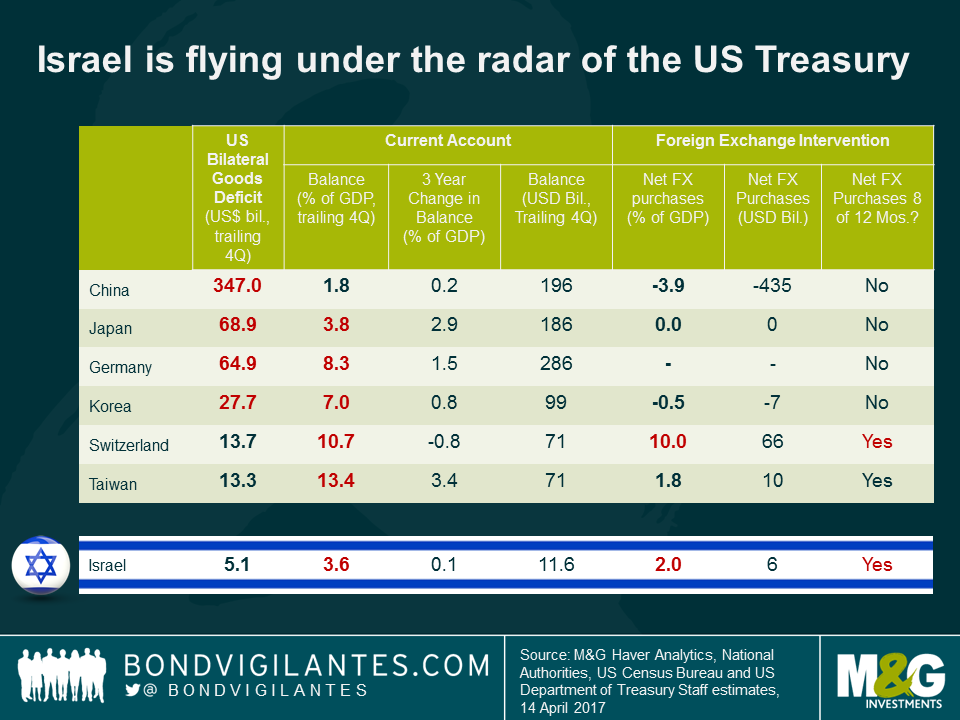

Though the recent US Treasury report did not name any country as a currency manipulator (see more details on this in Mario’s blog), the monitoring list centres on larger economies that meet the following criteria:

Because Israel is a much smaller economy (estimated $318 billion at the end of 2016) and not a major trading partner with the US (bilateral trade surplus is far less than $20 billion), it is not included on the monitoring list. Anecdotally however, if one were to examine the other factors that are part of the monitoring criteria, Israel would likely have joined the club.

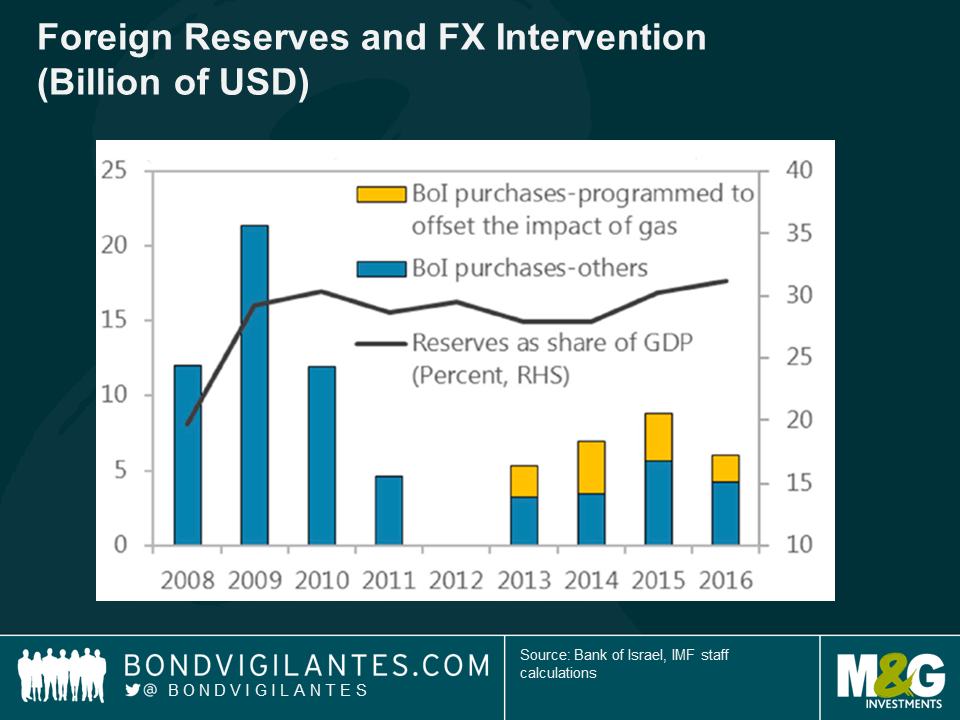

The Bank of Israel conducts monetary policy using a combination of interest rate and currency interventions. Inflation and inflation expectations are now approaching the lower end of the 1-3% target (after a two year deflationary period) and the economy is growing at a solid pace. There is room for monetary policy to remain accommodative, but I think it unlikely that interest rates will be reduced into negative territory from the current 0.1% base rate, now that inflation is heading in the right direction.

The Bank of Israel perceives the Shekel to be moderately overvalued and has been intervening in the currency markets to smooth the appreciation and in more recent years, to neutralize the flows coming from gas exports, in others to mitigate the risk of Dutch disease. The IMF, on the other hand, believes that the currency is roughly in line with fundamentals. There are, however, conflicting results depending on the FX model methodology used, as it is often the case when attempting to model currencies. Some models suggest a 15% undervaluation, while others suggest a modest 4% overvaluation. See page 50 here for more details.

The Shekel could be an interesting opportunity for currency investors (not concerned over additional USD strength) that believe that the favourable trends in the balance of payments remain intact, that the Bank of Israel will not increase the pace of currency interventions and that there is no scope for additional monetary easing.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.