oil

Not all oil-exporting countries are the cracking winners you think.

By Charles de Quinsonas

4 June 2026

Oil has entered a bear market, despite OPEC’s ongoing supply reduction of 1.8m barrels/day, which started in January 2017 and is set to continue until March 2018. How are fixed income markets reacting? Also, Argentina has been in the news twice this week: successfully tapping the market for the $2.75bn sale of a 2117 bond, but failing to make MSCI’s upgrade from frontier to emerging markets. How does this link to the country’s economic performance? Finally, I’ll review whether there were any market moving updates from last week’s EU Summit in Brussels. Tune in for the latest edition of BVTV!

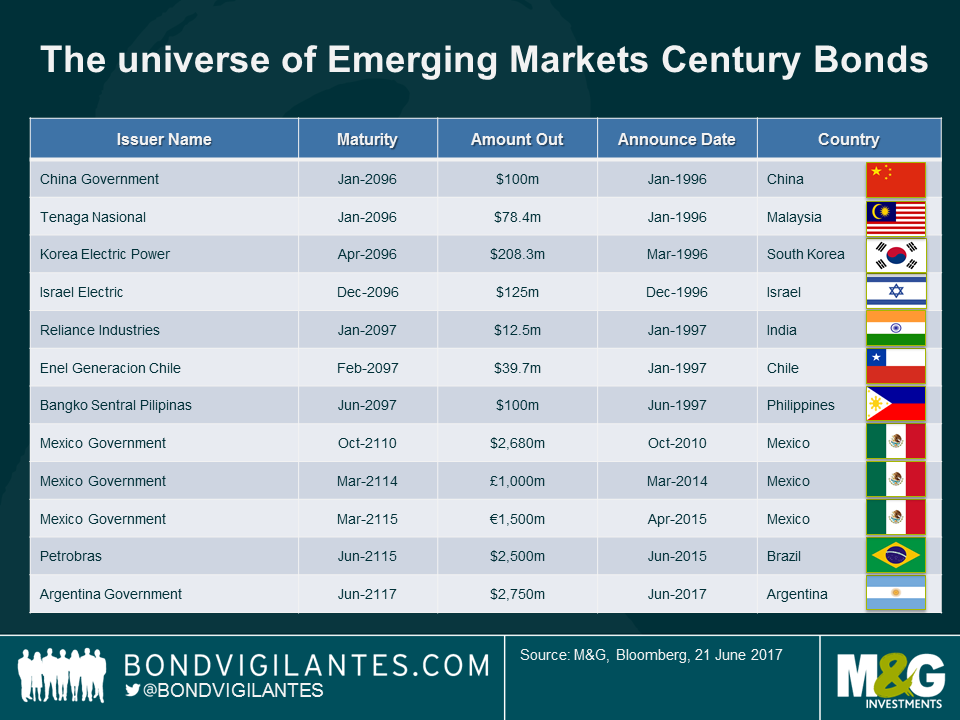

Argentina’s recently issued century bond deal was unexpected in terms of timing and maturity. Century bonds in Emerging Markets (EM) are rare (we think the table below is pretty exhaustive) and they grab the headlines, especially when issued by a credit that has defaulted many (many) times, like Argentina.

Are century bonds that much riskier?

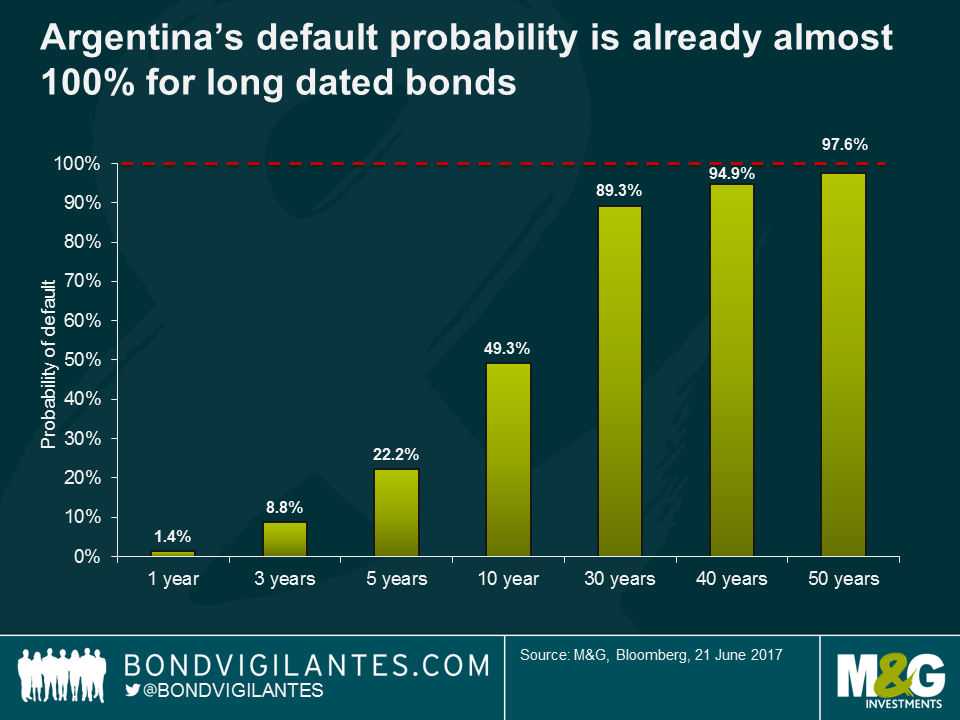

Given the unusual maturity of the bond, the model choked after 50 years. However, we can see that the implied probability of default given these assumptions is already at 97% for a bond maturing in 50 years. Given this, a century bond should not be seen as being much riskier. In other words, the current level of Argentinean spreads is at an unstable equilibrium: either fundamentals will continue improving and credit spreads will continue to fall over the next decades or history will repeat itself, fundamentals will not improve and Argentina will default again. In this latter scenario, it almost does not matter then whether you are holding a 50-year bond or a century bond.

‘In the long run we are all dead’ John Maynard Keynes

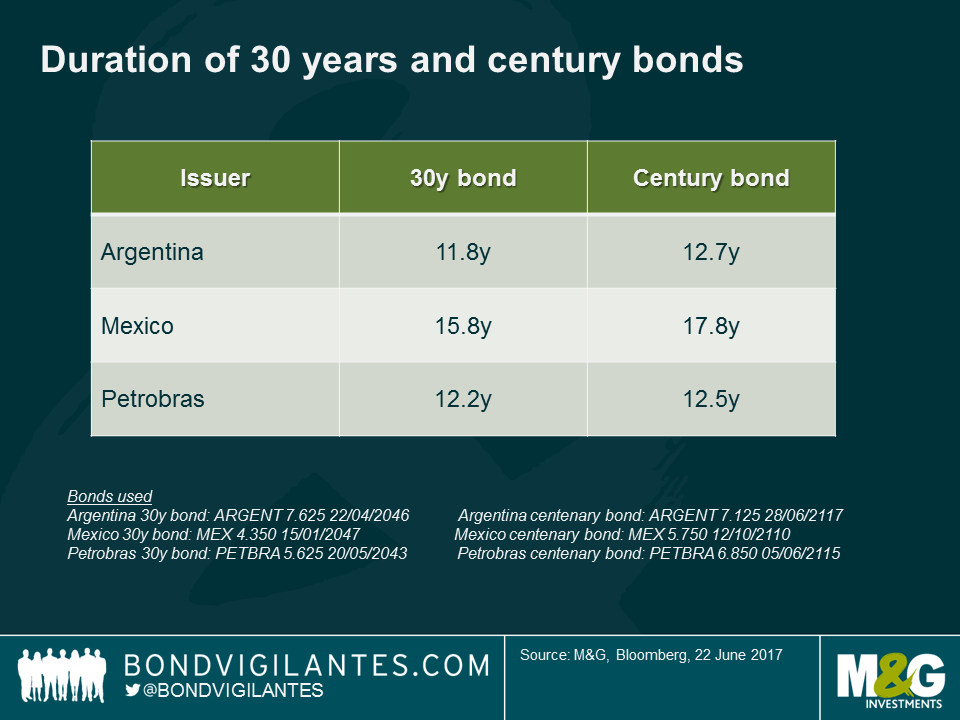

To conclude then, the duration of a 30 year Argentinian bond at 11.8 years is little different to that of a century bond (12.7 years), so spread risk is not significantly higher. The default risk of a 30 year bond is close to 100% anyway given current pricing of long term Argentinian risk – how much worse can it be in a 100 year bond?

| What about the prospects for Argentina’s economy?

In terms of fundamentals, Argentina’s new administration is trying to address deep challenges that were inherited from the prior administration. There has been rapid progress on liberalizing capital controls and they have unified the currency market under a new floating exchange rate regime. Relations with investors have improved markedly and this bond attests to that. On the domestic side, however, the improvements have been more gradual. Inflation (measured by the City of Buenos Aires CPI) is declining as the pass-through the Peso depreciation dissipates but is still hovering above 20%. Growth is picking up, led by investment, and this will be critical in addressing two of Argentina’s medium term risks:

|

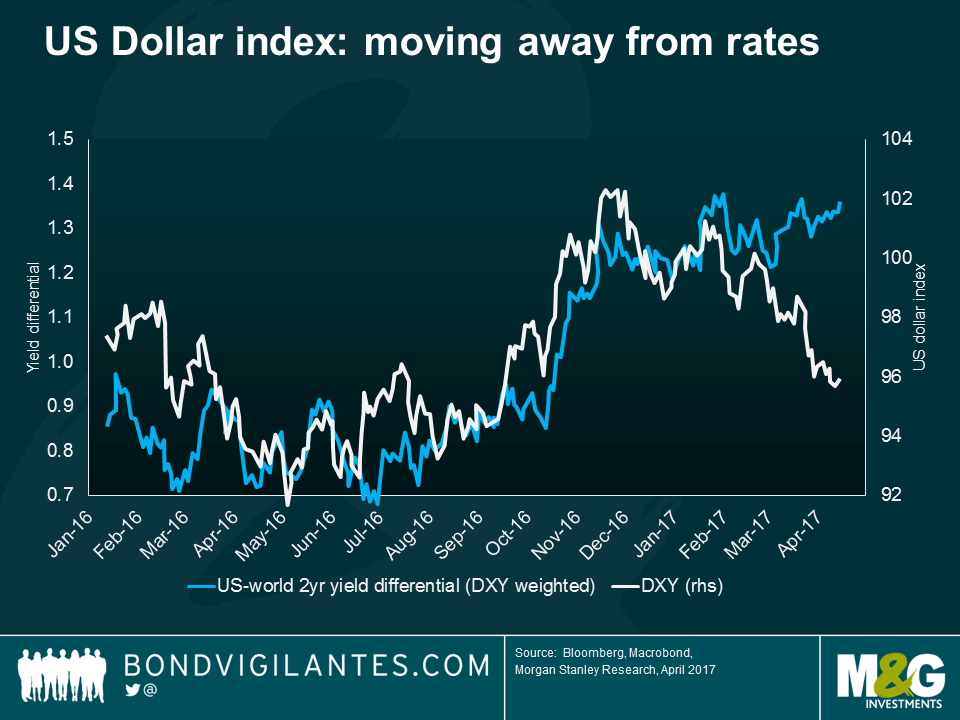

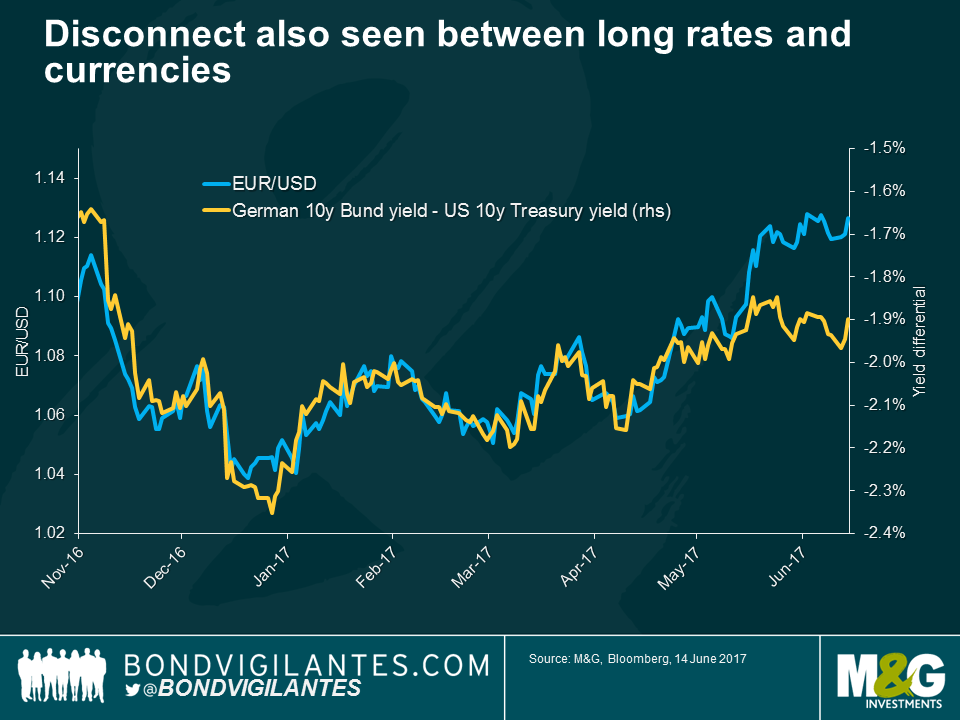

Despite US rate hikes in December, March and another last week, the US dollar has depreciated back to pre-election levels. All of the Trumpflation dollar premium has disappeared. As the Trump dollar trade appears to have run out of steam, the Euro has however been climbing. Optimism around the Euro area growth comeback grew leading up to the ECB meeting earlier this month, with EUR/USD hitting an 8-month high at 1.13, despite Draghi delivering a decidedly dovish statement (with many now questioning their assumed timelines for policy normalisation via tapering and eventual rate hikes).

What’s been interesting about these recent currency moves is that the relative outperformance of the euro has not been driven by rising interest rate expectations for the euro zone’s currency bloc relative to rates in the US. In fact the opposite has been happening. The two charts below show that the recent trend has been for US rate expectations to be stable or rising compared with its major trading partners, and yet the dollar has underperformed sharply despite this rate divergence.

So if rate differentials aren’t driving the dollar and the euro at the moment, what is? Firstly the Citi FX positioning survey suggests that whilst investors had been heavily overweight the US dollar and underweight the euro in 2016, there has been a reversal in this positioning. A large short position amongst investors and speculators can cause significant upwards price corrections on relatively small changes in fundamental outlook, as short covering takes place.

Perhaps most importantly, the fundamental valuation of the euro has also supported its rally. Looking at Purchasing Power Parity (PPP), the euro looks to be almost 20% “cheap” to its fundamental value against the US dollar. Now that the economic data has started to come in stronger, and ahead of expectations in the euro area, and the political uncertainty surrounding elections in France, the Netherlands and elsewhere has diminished substantially, this big undervaluation has suddenly been noticed.

A hiking Fed has caused trouble for Emerging Markets in the past; will history repeat itself? Also, we touch on two things from the Fed meeting that are more interesting than the actual hike itself.

Tune in for the latest edition of BVTV, where Fund Manager Claudia Calich joined me to discuss how she has positioned her EM debt portfolios for the second half of the year.

1. The ECB can act quickly when considering if a bank has reached the point of non-viability (PONV), and enacting a resolution plan. The speed with which regulators acted clearly took the market by surprise. At the same time, how the regulator determines a bank to be non-viable is still a grey area (considering the situation around some of the weaker Italian banks).

2. EU stress tests are not a very good assessment of banks’ medium-term viability. This isn’t new information, but Popular should serve as a reminder of the fact given it had a low but passing adverse-scenario CET1 of 7.0% in the 2016 tests. Similarly, a high liquidity coverage ratio (LCR) may be little comfort in the face of a run on deposits (Popular’s LCR of 146% was well above the 100% regulatory minimum).

3. When it comes to AT1 (Additional Tier 1) conversion triggers, the point of non-viability trigger is the more likely to result in conversion/write-down rather than the breach of capital ratio – making the difference in high trigger to low trigger coco’s less relevant.

4. Valuations of a bank’s assets tends to fall sharply once the bank is deemed non-viable. Whether from signalling effects or regulator incentives to be conservative, losses imposed on investors have historically been considerably larger than market expectations leading up to a resolution or bail-out (Portugal’s Novo Banco is another example).

5. In a stress situation, Tier 2 losses may not be very different from those of AT1s. The swift and full T2 write-down highlights the potentially unenviable position of T2 investors. We’re not suggesting they pose exactly the same risks (unlike T2, AT1s share many features with equity such as discretionary distributions and the possibility to extend into perpetuity), but in a point-of-non-viability case, T2 may not offer much more protection to investors.

6. There is a fine line between PONV and resolution – non-preferred senior bonds are also designed to take losses. While non-preferred senior debt is a resolution instrument, not a PONV instrument, there is a good chance that when a bank reaches PONV it will be put into resolution and trigger the non-preferred senior. There are scenarios where conversion of sub-debt may be sufficient to prevent a bank from being put into resolution, however this depends on the size of the loss at the individual institution. Given the point above re valuations, we think the probability of resolution following PONV is fairly high. There was no non-preferred senior debt outstanding in this case, but if there had been there is a good chance it would have also taken losses.

7. Despite the fact that seniors were spared in this instance, we do not believe this means that regulators will bend over backwards to avoid losses on other bail-in-able seniors in future cases. Regulators are more likely to attempt to protect seniors which are pari-passu with deposits or other senior liabilities, in the name of a “clean” resolution and financial stability, but it is more straightforward for them to bail in liabilities that sit below deposits (e.g. German seniors, HoldCo seniors, non-preferred seniors) and we should not expect these to be protected.

8. Questions remain about the “no creditor worse-off than in liquidation” (NCWO) principle, as it remains unclear how Popular’s subordinated debt holders might have been treated in a liquidation scenario. They may believe the provisions Santander is taking on Popular’s NPLs are too conservative (they result in considerably higher coverage ratios than the average Spanish bank – though the average may not be a reasonable benchmark) and may therefore litigate. The ECB/SRB (Single Resolution Board) made no mention of the NCWO principle in their communications regarding Popular, which raises questions on how they handled this requirement.

While last week ended with British prime minister Theresa May promising to provide ‘certainty’ after yet another shock election result, for markets, the opposite looks likely to be true. And with the renewed uncertainty of a hung parliament likely to prove unhelpful in upcoming Brexit negotiations, what implications can markets draw for UK growth prospects and the likely direction of gilts? Tune in to this morning’s BVTV as I discuss this, plus the key take-aways from the ECB’s latest meeting.

The UK has a hung parliament, with Theresa May’s Conservative Party losing seats and likely ending up 8 short of an overall majority. It looks as if young people voted in large numbers, mainly for Jeremy Corbyn’s Labour Party. The Conservatives remain the single largest party however, and together with the Conservative-leaning DUP on 10 seats, they will likely form the new government. The Prime Minister is holding a press conference at 10am – it is possible that she resigns at that time. This is an extremely poor result for her personally, having gambled that another General Election would significantly boost her majority. For an election designed to deliver a “Strong and Stable” government, we face the possibility of a new Conservative Party leadership battle (perhaps beginning later today) and even another General Election later this year.

This renewed uncertainty seems likely to be unhelpful to the UK’s Brexit negotiations, due to start on 19th June. The Conservatives did especially badly in “Remain” constituencies. Perhaps this result therefore partly reflects a rejection of May’s assertion that “no deal is better than a bad deal”, and increases the chances of a softer Brexit (remaining in the Single Market), or even another referendum on the “deal” (which could be the price of Lib Dem political support in the new government, although pre-announcing a second referendum would perversely incentivise the EU to offer a poor deal to the UK in the hope of it being rejected). Finally, some good news for those fed up with election campaigns: the poor performance of the SNP in Scotland reduces the likelihood of a new Scottish independence referendum in the next few years.

Sterling has weakened overnight, but by only around 2% against the US dollar and euro. There’s been little bond market impact. At the margin there may be less austerity and fiscal tightening in future under a weakened Conservative Party, but there will be no significant rise in gilt issuance and the goal of reducing the UK’s debt/GDP over the next few years is likely to remain in place. Whilst Jeremy Corbyn’s Labour Party did much better than expected, markets don’t need to think about the prospects of nationalisation and significant changes to taxation and spending plans. The gilt market is not yet open, but is expected to start the day down very, very slightly. The US Treasury market was little changed in Asian trading – this is not a global risk off event. Corporate bond markets are a little weaker, with UK banks and insurance companies up to 5 bps wider in spreads. The iTraxx Main investment grade credit index is 0.5 bps wider. These are trivial moves.

The momentum of UK economic growth has been fading as we move through 2017. Retail sales growth, house prices and inflation adjusted incomes are all weakening in what remains a very consumption driven economy. This election result and the continued uncertainty it brings suggests that this trend continues. The Bank of England is not going to tighten policy for the foreseeable future – although there is also no likelihood of an “emergency rate cut/QE” of the sort we saw post the Brexit result last June.

A couple of weeks ago, state-owned International Bank of Azerbaijan (IBA) shocked its bondholders by announcing a surprise restructuring. The bank’s capital ratio turned negative at year-end 2016 due to large currency losses as a result of the depreciation of local-currency Manat (AZN). The International Bank of Azerbaijan bonds (IBAZAZ) 5.625% 2019 bonds were trading above par and dropped by 15 to 20 points on the news.

I watched the investor Q&A session hosted by the company, its restructuring advisor and the Minister of Finance of Azerbaijan himself. Some bond investors seemed surprised that the government of Azerbaijan backed the restructuring of a state-owned entity and did not provide additional support. For background, the government in the past couple of years provided strong support by both injecting a lot of equity in the company and creating a bad bank to clean up a large portion of problem loans. Apparently, it was not enough to fix the balance sheet issues of the largest bank in the country and the company is now proposing to exchange existing bonds into new sovereign debt or newly issued IBA bonds, at a haircut estimated at about 20%.

Sadly it’s not the first time that investors look at a state-owned (also called quasi-sovereign) bond with a view that the government will provide unconditional support (misleadingly called “implicit guarantee”) to the state entity regardless of the standalone corporate fundamentals and despite no legal government guarantee whatsoever. In 2009, the state-controlled Dubai World conglomerate ran into financial trouble and the government of Dubai clearly stated at this time that it had no legal obligation to financially support the company, adding that: “the lenders should bear part of the responsibility”. What was seen as a safe quasi-sovereign investment finally resulted in a painful and lengthy restructuring of the debt for bondholders.

We, bond investors, must make sure we carefully examine bond documentation to assess whether or not we are invested in a bond (“explicitly”) guaranteed at the sovereign level, i.e. with an “unconditional and irrevocable” guarantee in case of defaults. The problem is that the investor community often mixes a guarantee with likelihood of government support. The former is a legal obligation. The latter has nothing to do with a guarantee; it is merely an assessment of the ability and willingness of a government to provide support and how much bond spreads investors are willing to leave on the table when buying these bonds. Either a bond is guaranteed by its sovereign or it is not. There is no such thing as an implicit guarantee, just a likelihood of government support.

According to recent reports, leading foreign football players in the English Premier League are looking to get paid in euro rather than sterling. Since the UK referendum result in June last year, sterling has fallen by 12% against the euro, so it is unsurprising to see that some players have questioned the denomination of their salaries. It is not the first time that global stars have asked to be paid in a particular currency. In 2007, rapper Jay-Z flashed €500 notes in his video clip for “Blue Magic”, hip-hop group Wu-Tang Clan preferred euro to greenbacks in payment for their new album 8 Diagrams, while model Gisele Bünchen asked to be paid in euro rather than US dollars for any promotional deals.

We think there are a number of good reasons to expect euro to strengthen further against sterling from current levels, so this may be a trend that football clubs should get used to as they search for footballing talent in a global marketplace.

The impressive performance of the UK economy post the referendum result has surprised the Bank of England and professional economic forecasters alike. Indeed, the Bank of England was so pessimistic about the prospects for economic growth that it quickly cut the base rate to a record low of 0.25% and embarked upon yet another round of quantitative easing. With the benefit of 20/20 hindsight, this pessimism was misplaced. The key factor in this outperformance was the fact that in the real world, nothing had changed. Businesses retained access to the single market and the depreciation in sterling meant that exports were suddenly much cheaper in the international market. The UK consumer, spurred on by lower interest rates and a robust labour market, felt confident enough to continue to spend freely as evidenced by one of the lowest savings rates in the EU.

Dependent upon the prospect of how Brexit negotiations progress, the UK economy could continue to surprise on the upside in the short-term, as businesses look to stockpile inventories and consumers seek to purchase items before the UK leaves the single market. If it begins to appear increasingly likely that the UK will fall back upon World Trade Organisation rules, then the rational action will be for consumers to bring forward consumption before the imposition of tariffs forces the prices of European imports higher. In this scenario, consumption and inventories generate higher economic growth, despite the impact that a weaker currency has on import price inflation. The better than expected performance of the economy, coupled with and higher inflation and interest rate expectations, has seen sterling rally in recent weeks.

It appears that the confidence in the UK economy is misplaced and the medium term outlook for UK growth and sterling is more challenging. The squeeze on real incomes is likely to intensify given anaemic wage growth, while the propensity to invest amongst the private sector is likely to weaken throughout the Brexit negotiation process.

However, it is extremely difficult to estimate the impact of Brexit on the real economy, given the uncertainties around the UK’s future relationship with the EU If we look beyond the UK there are signs that growth and interest rate differentials are now starting to shift against the UK in favour of Europe and the US respectively.

In Europe, there are signs of a broad based recovery in euro area sentiment. Euro area PMIs and consumer confidence have been marking multi-year highs across the region, and with political risk diminishing after the French election, it appears that Europe is likely to generate a robust economic performance in 2017. The European economy will likely remain in this current goldilocks patch for the next 18 months – growth is solid, inflation is low, and the ECB remains extremely supportive through ultra-easy monetary policy. On this last point, the more solid footing of the European economy will likely give the ECB more confidence to begin tapering quantitative easing and possibly hike the deposit rate later this year. As these expectations become more entrenched in markets, this will provide a tailwind for the euro. This is especially the case against sterling, where the Bank of England remains firmly on-hold.

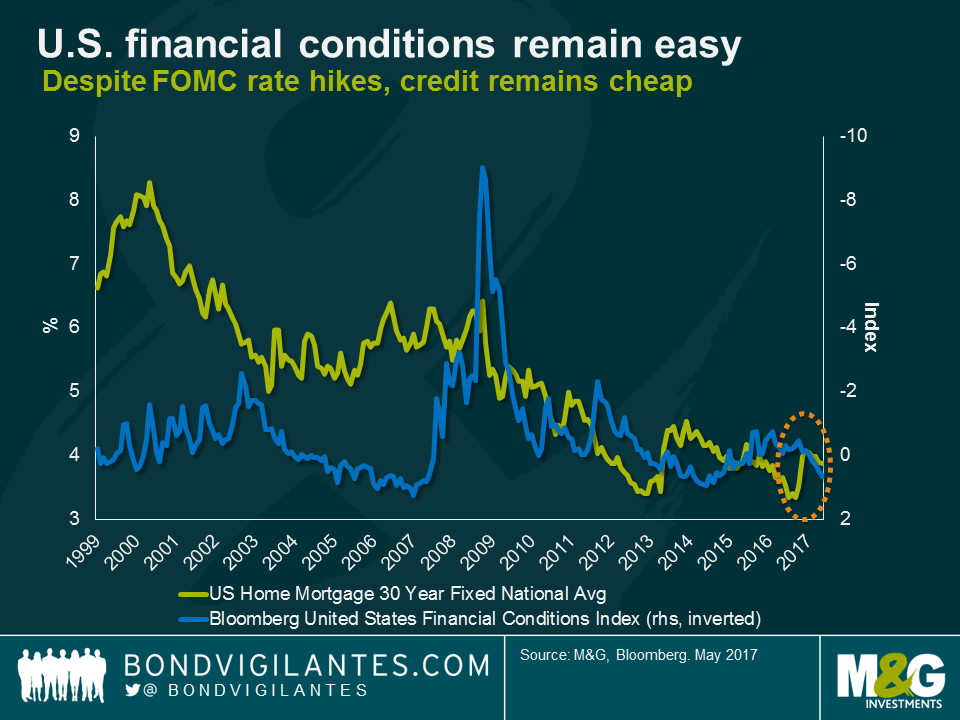

Turning to the U.S., uncertainty abounds around the new administration’s fiscal plans. In recent months, the market has reassessed the prospects of tax reform, leading to a fall in the 10-year treasury yield and dollar. Moving beyond this, it is clear the economy is on a sound footing and important tailwinds support growth. Firstly, the labour market is currently operating at close to full employment, as indicated by a 17-year low unemployment rate of 4.3%. This suggests we are likely to see rising wages (and inflationary pressure) as the demand for workers grows. Secondly, energy prices have firmed, which should support energy-related capital expenditure in the coming 12 months. Thirdly, consumer and business confidence are at robust levels, indicating an expanding economy. Fourthly, financial conditions remain historically easy despite the Fed rate hikes that we have witnessed in the last year. And finally, home builder sentiment is around levels last seen in 2005, indicating that the contribution from construction spending to economic growth will accelerate in year-end. Even before we know the details of the administration’s fiscal plans, it appears that we will see at least two more rate hikes from the FOMC this year, intensifying the decoupling of growth and interest rates relative to the UK.

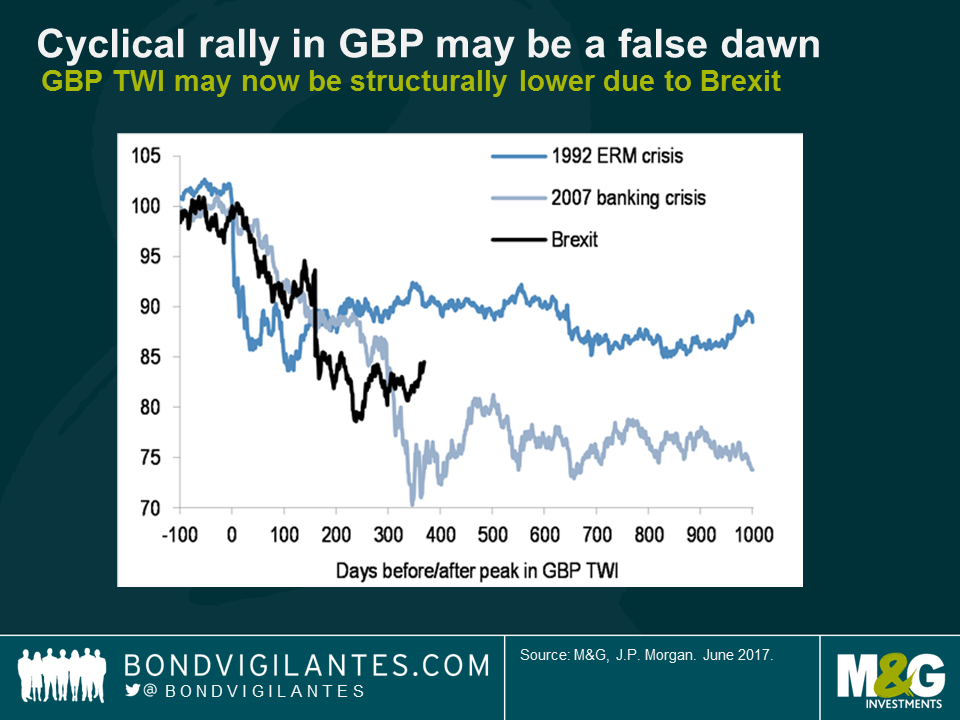

Historically, sterling tends to remain depressed after significant events like the 1992 ERM crisis and 2007 GFC. From this perspective, the recent rally in sterling appears cyclical rather than structural. The currency will likely to continue to be volatile into and after the election, while on a longer-term basis more fundamental factors like interest rate differentials will dominate the direction for sterling. The footballers of the Premier League who are signing 3-5 year contracts may be right in asking to paid in euro rather than sterling.

Are we seeing the end of the Trump trade and, if so, is the Macron trade the new game in town? Join us for this morning’s BVTV, where Stefan Isaacs and I discussed whether the reflation trade has been superseded by Europe’s ever-improving outlook?

Also: what to watch for on the markets this week.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.