Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Last week was a particularly busy week in the earnings season calendar, but has sentiment for the auto sector been dampened by the latest revelations in Germany’s Der Spiegel magazine of how car manufacturers colluded over diesel emissions treatment systems?

Wolfgang Bauer joins me for an auto sector special this week on BVTV, where we discuss the latest scandal, plus the impact of the further government moves to ban all petrol and diesel cars by 2040 (or earlier). How have credit markets reacted so far and what more can we expect? Tune in to hear our latest thinking.

Today marks five years on from Mario Draghi’s now famous ‘whatever it takes’ remarks, widely credited with sparking a reversal in the Eurozone’s fortunes.

Below are five charts offering some insights into the European Central Bank’s successes and failures in the ensuing period, as well as some of the challenges that remain.

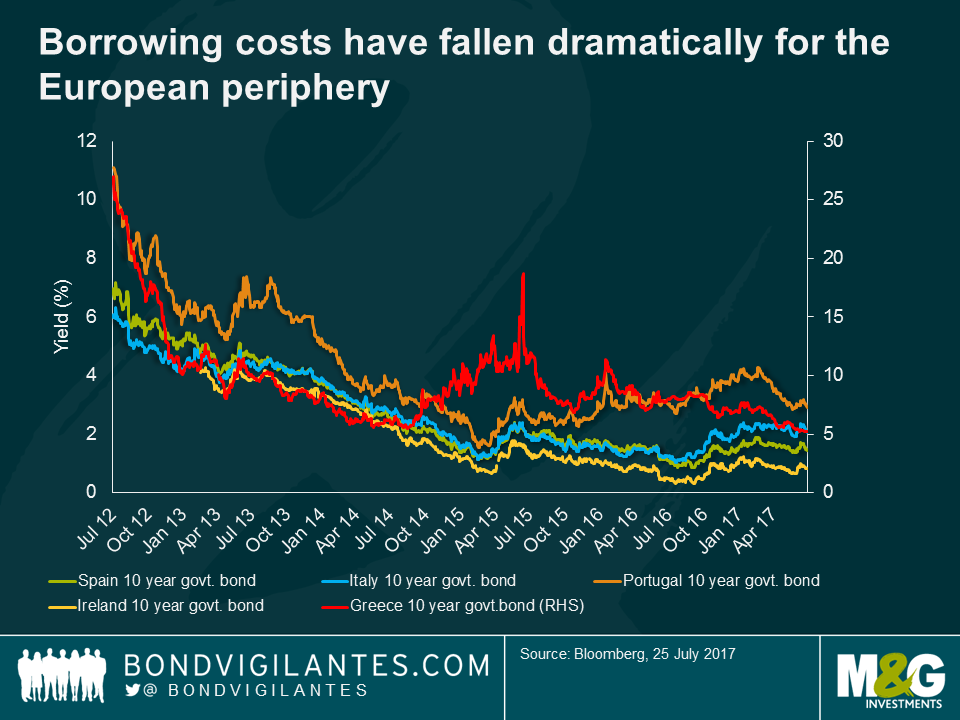

Five years ago, funding costs for the periphery had climbed to unsustainable levels. Spanish ten year debt traded at 7.5%, Italy at 7%, Portugal at 11% and Greece a whopping 27%. In part this reflected the redenomination risk into local currency. Finally acting as the lender of last resort, the ECB significantly decreased this risk, reopened market access for the likes of Spain and Italy and with it lowered their implied cost of funding. Over time (some) structural reforms, further monetary easing and improved growth has seen funding costs fall towards, and in some cases below current growth rates, offering a real prospect of debt sustainability for these economies. Greece’s return to market completes an astonishing recovery in fortunes.

Ultra-loose monetary policy penalised saving, reduced debt servicing costs and encouraged investors to take on risks. This has served as a backdrop for improved consumer sentiment, higher asset prices and a pick-up in consumption. The Eurozone has surprised recently as the global outperformer growing well above potential. Yesterday’s record print for the German IFO suggests growth may be tracking around 3% in H2 2017.

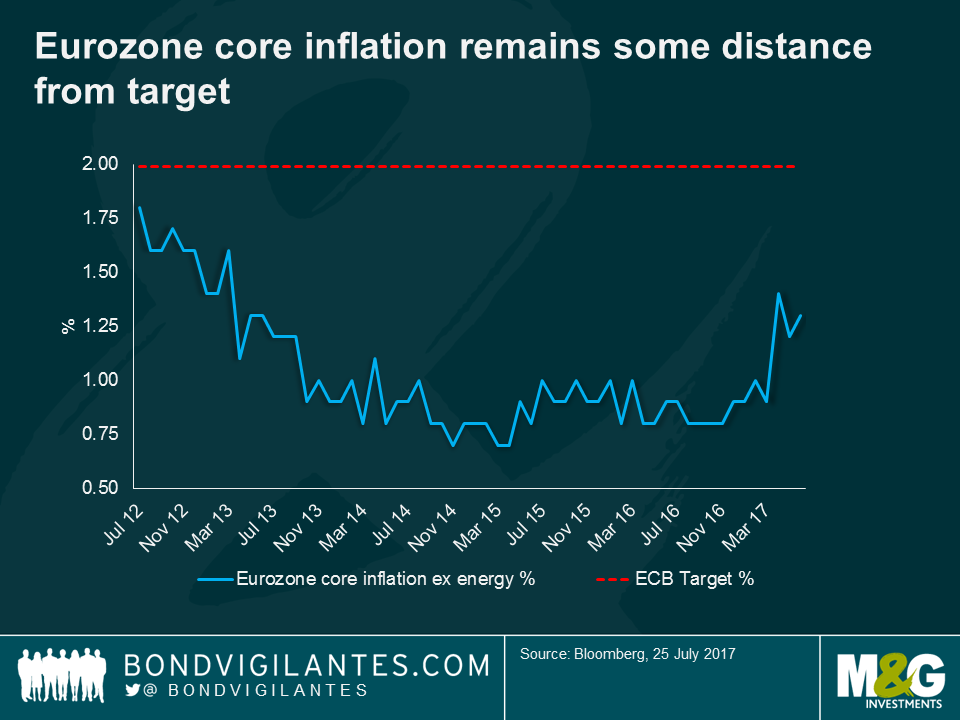

Despite the stabilisation seen in the Eurozone, lower borrowing costs and a generally improved economic outlook, the ECB continues to miss its inflation target. This has proven problematic given the ECB’s sole target is to deliver inflation of close to but below 2%. Whilst there are signs that inflation is trending back towards the Bank’s definition of price stability it has been very slow in the making. Any tightening of policy will likely be a protracted affair.

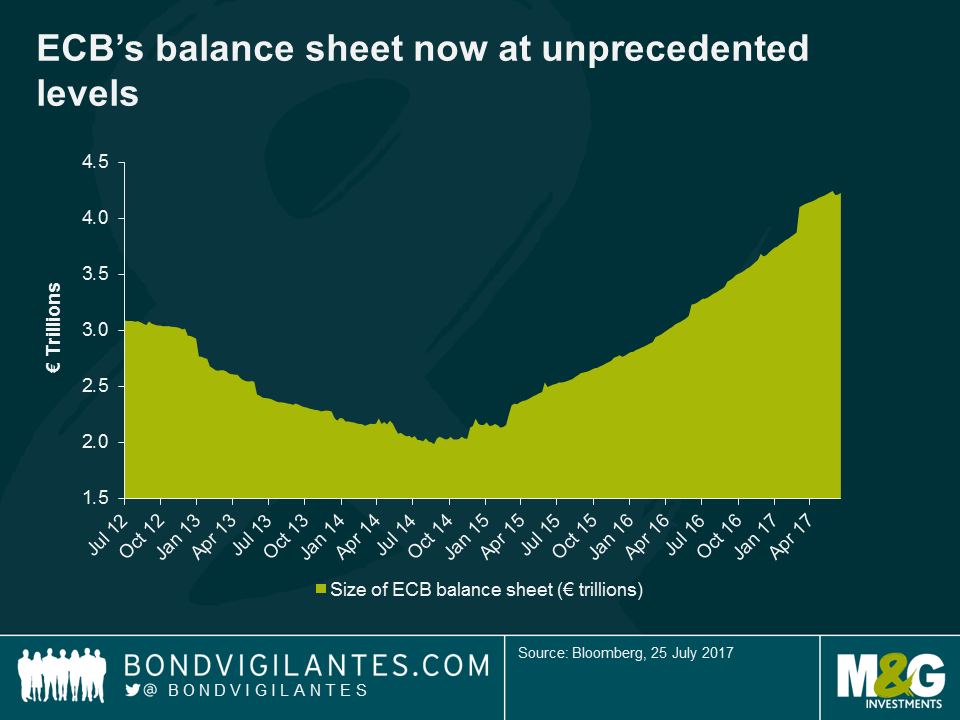

Having taken the refi-rate below the ‘zero-bound’ in 2014 the ECB still found itself facing the risk of a self-reinforcing deflationary spiral. Ultimately the Bank followed other central banks announcing in Jan 2015 that it would inject €1.1 trillion via bond purchases through to September 2016. The problem? Despite the significant expansion of its balance sheet the ECB was forced to extend its quantitative easing programme both in terms of length and to include corporate bonds. It now sits above a whopping €4 trillion. Draghi has since gone to lengths to stress that any tightening of monetary policy will be done in a gradual fashion. But there are clearly some on the Governing Council who worry about the negative consequences of an ever expanding balance sheet, the implications for the banking system, the Eurozone’s ‘addiction’ to debt and consequently the ECB’s ability to exit its ultra-loose stance.

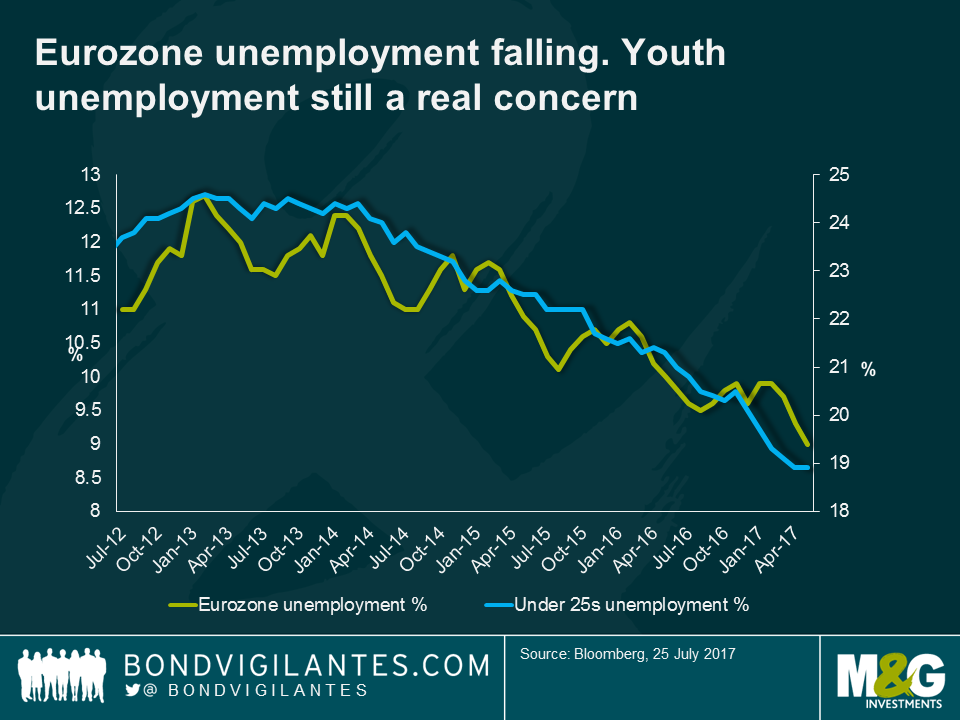

Whilst populism appeared to be sweeping across the developed world, the outcomes in the Dutch and French elections suggest that the Eurozone may have taken a different approach. However Italy’s lagging economic performance and a general election in 2018 offer the potential for an upset. Although levels of unemployment in the Eurozone have come down somewhat they remain elevated, especially amongst the younger cohorts.

Doomsday predictions claiming the beginning of the end for the Eurozone were two a penny back in 2012. Investors and economists queued up to argue that the single currency would not hold. Either peripheral countries would be forced out or the core would walk away so went the argument. Despite all the speculation, no country has left the Eurozone and markets currently appear much less concerned. This is perhaps the single most important measure upon which to judge the effectiveness of ECB policy over the past five years.

The United States is fast approaching the point at which its indebtedness reaches its debt limit, which generally is approved by Congress without debate. Routinely in the past the debt ceiling would be raised, reflecting that it does not affect the amount of spending, but only makes sure the U.S. can pay for spending it is committed to whether by tax receipts or by borrowing. It is about ensuring the U.S. can pay its bills.

Well, by most estimates we are now three months or so away from the U.S. once again hitting its debt ceiling. In the event that Congress does not raise the limit, then the U.S. Treasury would have to default on its bond obligations, or immediately curtail payments to public programmes or employees, known as a partial government shut down. In the Summer of 2011, Republicans demanded that in order for the debt ceiling to be raised, spending would have to be cut and taxes rise no further. Democrats wanted to see higher spending funded by higher taxation, and so Congress could not agree to raise the debt ceiling.

The U.S. entered a debt issuance suspension period in May, and would have run out of funds on 2nd August 2011, at which point either the U.S. Treasury would default, or it would have had to cut spending drastically overnight seeing government employees and programmes losing funding with clearly disastrous impacts on aggregate demand. The debt ceiling passed votes at both houses at the eleventh hour, on 1st August, and the default was avoided.

Given how little appears to be being done by the present administration at the moment, one can be forgiven for thinking ‘here we go again’. The chart below shows that in recent sessions the cost of 3 month money to the Treasury has surpassed that of 6 month money, so the curve has inverted for the first time in a long time. The bond market is starting to worry about a partial and temporary shut-down once more.

What should investors do then, if they are concerned about the debt ceiling not being raised and the U.S. is to find itself unable to pay its bills? Selling Treasuries might seem like the obvious trade, but it’s worth remembering that in the suspension period between April and August 2011, Treasury yields actually rallied. There was a period in late June and early July when default fears escalated and yields rose by approximately 40 basis points (c.4 point fall on the 10 year Treasury bond). This was soon reversed though, as concerns around a U.S. default brought a healthy dose of risk off to global markets, which saw Treasury yields continue to fall. A partial shutdown can’t be viewed positively for the U.S. economy, though, and if programmes are shut down and employees aren’t paid, then unemployment will rise, wages will fall, and aggregate demand will fall, which will put to bed fears of the U.S. economy overheating and further rate hikes being expected. So it’s a big issue. But the direction of Treasury yields and bond yields priced over them is highly uncertain, and indeed counterintuitive. Be careful.

It was just about 3 years ago the market was getting very relaxed about the global economy, asset prices were rich and volatility was very low…then the market sold off. Today it feels like we are back to that situation: a recession seems very unlikely, but can we experience another market correction? In this episode of BVTV we highlight 3 things that could potentially lead to a correction in the market

In this episode of BVTV, I take a look at how the global economy is expected to perform in the second half of 2017. Is it a Goldilocks scenario of solid growth, low inflation and gradual monetary policy tightening, or is something more sinister lurking beneath the surface?

I’m now more than three quarters of the way through my attempt to climb 100 iconic hills, bergs, kops and mountains on my bike in 2017. It’s been amazing fun so far, and I’ve ridden a huge variety of different types of hill and mountain with some great people. The hardest? Well it took me six tries to get up Bristol’s Vale Street, the steepest residential road in the UK – but I was on a station hire bike and my leather shoes kept slipping off the pedals. I guess Corkscrew Hill outside Manchester should also qualify. Wet and roughly cobbled, none of our group made it more than a couple of metres up the 45 degree slope before falling off. It is not included in the honour roll below. As a region, I found that the hills of the Lake District were both consistently brutal, and the most beautiful I’ve ever seen. I can’t believe I made it to my mid 40s without ever properly visiting this area of the UK – go!

By now you probably know why I’m doing these climbs. Unbelievably, after only six months, Cascaid has already raised over £1.37 million for Cancer Research UK (CRUK), and has doubled its target to £2 million for 2017. This now seems very achievable. You can read about some of these efforts and the work of CASCAID and Cancer Research UK on the link below. I’m especially blown away by former M&G marketing guru Anne-Marie McConnon and team’s effort to row the Irish Sea from Wales to Dublin, which they did in heavy seas a couple of weeks ago. That’s the good news. The bad news is that even £2 million doesn’t go far – research is incredibly expensive. But survival rates from cancer have doubled from the 1970s, and Cancer Research UK is targeting a 75% survival rate by 2034, in particular by trying to improve the chances of those with pancreatic and lung cancer where the outlook is currently poor. Just two weeks ago CRUK announced the results of a large scale trial in prostate cancer, which showed a 37% improvement in survival rates. The money that you have kindly donated so far will make a difference.

http://www.cascaidcharity.com/

Cascaid’s fundraising page is now the most successful ever on the Virgin Giving platform, earning a “thumbs up” from Richard Branson himself last week. My fundraising page is linked below. Many thanks to all of you who have already donated.

I promised that if I raised an extra £500 then I’d shave my legs. You donated, and I am now silky smooth. I thought it might help me to a PB on Dark Hill in Richmond Park this weekend, but it turns out the aero impact is not as significant as I had hoped. Silky though.

A few thank yous. So as a reminder, I’m cycling up famous climbs featured mainly in Simon Warren’s excellent series of books called things like “100 Greatest Cycling Climbs” and “Another 100 Greatest Cycling Climbs”. Simon has very kindly helped me to plan some routes. The books are ace, buy them! Thanks to everybody who has ridden with me so far this year – I’ll do a full rollcall when I’m finished, but the company has been invaluable. Thanks also to Will Masi at Nuffield gym, and Athlete Lab at Monument for getting me in a state to get up the hills. Finally thanks to my family for support car services, and for tolerating me disappearing for a morning or two when on holiday. I promise it was coincidence that our trip to Bruges took place at the same time as Paris-Roubaix.

You’ll find the evidence of climbs on my Strava feed.

Here’s the list of all the climbs that I’ve done so far:

What’s next? Kent and East Sussex still have a few hills left for me, but before I finish I want to get up to the Derbyshire Peak District, I want to ride up a hill in Calverton which I could never get up on my Raleigh Grifter as a schoolboy in Nottinghamshire, and I think I should tick off some of the Yorkshire hills that featured in the Tour de France a couple of years ago. Thanks for all of your support. Here’s a picture of The Struggle near Windermere. An awful hill.

As we enter the second half of 2017, one of the biggest themes to emerge recently has been renewed oil price weakness. M&G credit analyst Vladimir Jovkovic joins me this morning on BVTV to discuss what’s driving the latest price falls and what the possible implications may be for the next US high yield investment cycle. Also this morning: a quick recap of how bond markets have performed in the first half of the year. Tune in to hear more!

Join us on BVTV, where this week we discuss:

Tune in for our thoughts on the stories making headlines this week.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.