Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Guest contributor – Chris Mansfield (Investment Graduate, M&G)

The sustained demand for high yield bonds and European leveraged loans over the past few years, combined with improving corporate fundamentals, has led to strong performance from both asset classes. The large amount of capital available for issuers of higher yielding assets has placed the bargaining power squarely in the hands of the borrowers, and they’ve exercised this power unreservedly on the covenants offered with new deals. In 2014, James wrote about the deterioration in high yield bond covenants. Since then, little has changed in this market; spreads have just grown tighter. The European loan market, by contrast, has seen some dramatic changes to standard covenant packages over the last five years.

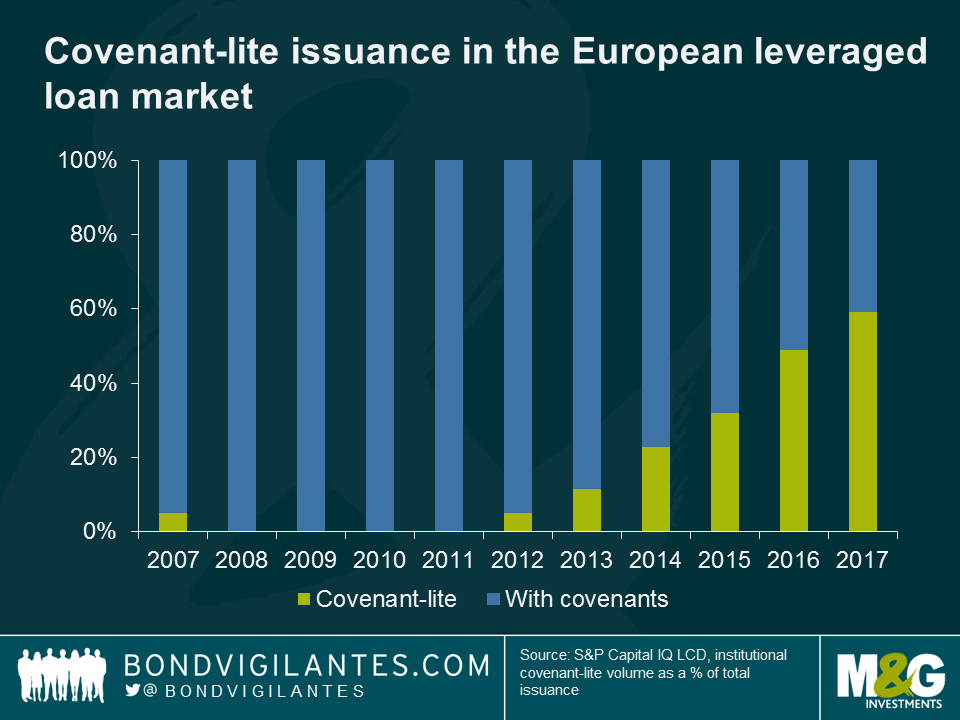

Back in the aftermath of the crisis, the average European leveraged loan deal came with four maintenance covenants. In rough descending order of importance, these were: leverage, interest cover, debt service cover, and capital expenditure. Respectively, these covenants: limited the ratio of net debt to EBITDA (and often enforced a reduction over time); imposed a maximum ratio of interest costs to operating income; enacted a maximum ratio of current debt obligations to cash flow; and limited capital expenditure as a proportion of cash flow or cash-like earnings.

Since then, and over the last five years in particular, the maintenance covenant package initially dropped to typically just leverage, and now ‘cov-lite’ is a common term used to describe loan deals with no maintenance covenants at all (NB incurrence covenants still remain present). As shown below, the proportion of leverage loan deals that are cov-lite has been growing steadily.

Of the deals that aren’t cov-lite, there is almost always only one maintenance covenant – leverage. And whilst it’s still present, its power has depleted. Historically, the headroom (distance between current pro forma leverage and the leverage ratio in the covenant) was around 25%; this is now more like 40%. The leverage ratio used to ratchet down over time, forcing the company to de-lever; today the ratio profile typically remains flat. Lastly, the documentation typically allows ‘adjusted EBITDA’ and even ‘net debt’ to be redefined, all combining to mean that the typical leverage covenant today is a weak shadow of its former self.

In the loans market the demise of maintenance covenants limits the power lenders have to stop the issuer aggressively reducing its creditworthiness whilst pursuing some (presumably shareholder-value-enhancing) strategy, raising downside risk. The result is that any macro factors that impact corporate fundamentals could see a sharper sell-off, hurting investor wealth, and potentially a corresponding decrease in recovery rates, compared with a European loans market where maintenance covenants remained unwavering. The corollary is that full due diligence and credit research is more important now than ever.

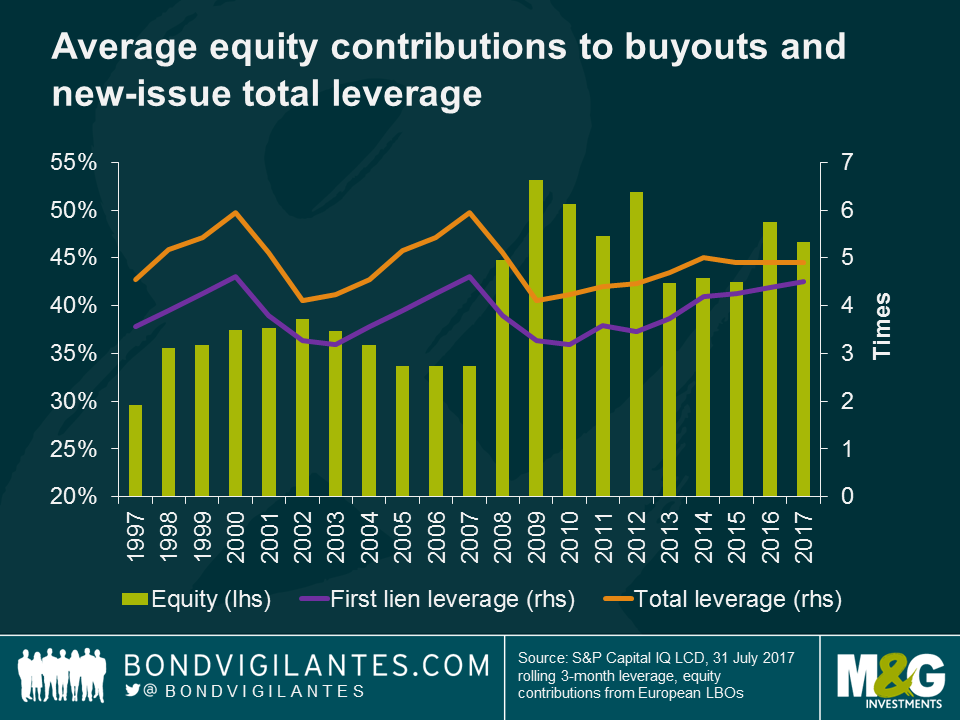

That said, there have been some more positive trends. The average leverage on new leveraged loan deals remains below the pre-crisis peak and is expected to stabilise at the current levels, and the average equity contribution in buyouts is now closer to 50% (and growing) than the c.40% seen in 2013-2015. These act as positive forces on recovery rates, possibly counteracting the above comment.

A question for investors is whether the overall terms on offer provide adequate compensation for the heightened risk resultant from covenant demise. They may well do given the context of other asset classes, but it’s unarguable that this decline in lender protection is unwelcome. So what should investors make of it?

Demanding a higher risk premium as compensation seems an obvious solution, notwithstanding the fact that spreads in the loan market have remained broadly flat in recent years amidst tightening in other markets. However, given the need of investors to deploy cash when inflows are strong, voicing disdain in either market – by declining to participate – is a difficult game to win. Some sort of unionisation of investors to ignite pushback would likely be the most effective solution.

The issue that stops investors from pursuing this strategy is that each individual would rather everyone else bore the effort. Additionally, investors may miss out on investment opportunities during such a pushback. Aggregate this desire across all investors and combine with the need to invest inflows, and you have one tricky problem to solve. Perhaps only a downturn will empower investors to demand the protection of the past.

Heated debates about proposals to repeal and replace Obamacare, generic pharmaceuticals feeling the pain of pressures on drug prices and lingering event risk around potential mergers and acquisitions – there are many reasons to take a closer look at the US healthcare sector right now. On my recent research trip to Chicago I discussed these and other topics with Laura Reepmeyer, Managing Director – Credit Analysis at PPM America. Here is the video.

James Tomlins, M&G fund manger, helps manage over £5bn in high yield assets. This week on BVTV I ask him:

Click on the link to hear James’ views and have a look at some of the cracking charts we’ve put together.

This week on BVTV Fund Manager Matt Russell joins in to discuss:

1) Why an interest rate shock could cause carnage in bond markets

2) The duration impact on a credit portfolio

3) Best strategies to hedge against interest rate risk going forward

Tune in for the charts and articles that are making headlines in bond markets.

Guest contributor – Simon Duff (Credit Analyst, M&G Credit Analysis team)

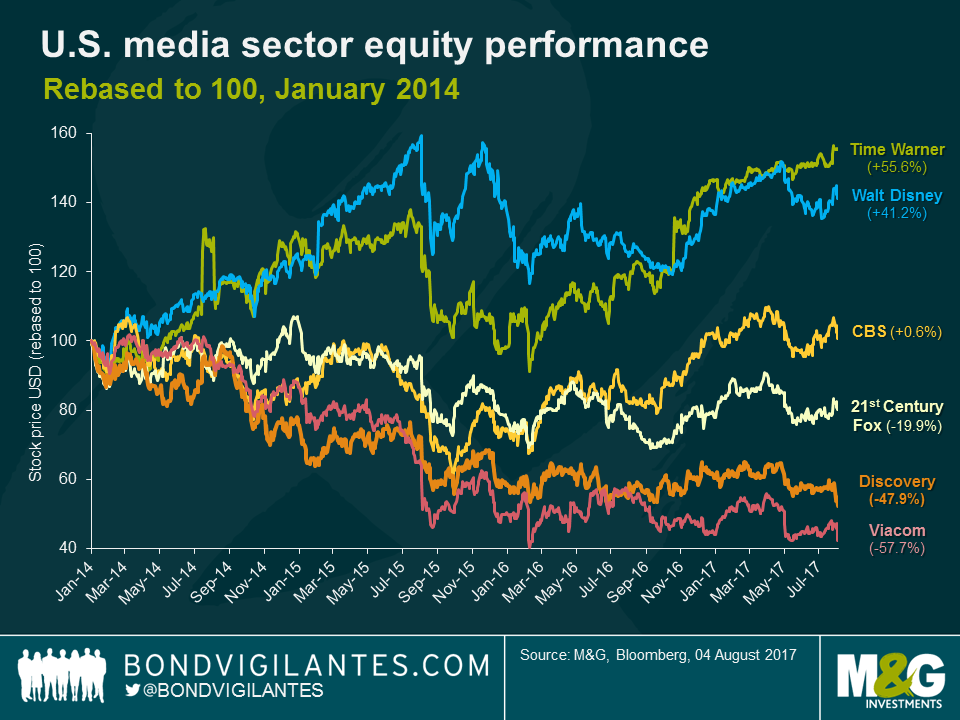

Last week, International TV network operator Discovery Communications announced the US$15bn acquisition of Scripps Networks. Scripps owns TV networks focused on food, home and travel, so it fits with the factual or “non-scripted” focus of Discovery’s core networks (Discovery, TLC, Animal Planet). It also offers an opportunity for Discovery to further diversify beyond its core male orientated demographic as well as boost US-centric Scripps’ efforts to expand into international markets by using Discovery’s global reach. So what’s not to like about the deal? Apparently a lot if you are a Discovery shareholder, with the stock falling 9% on the announcement of the deal. This is on the back of a stock that had already fallen over 40% since January 2014.

The decline in the share price was driven by concerns over the wisdom of a transaction that doubles down on the bundled pay-TV network business model. This is being caused by increasing structural pressure from the shift in consumer viewing habits to cheaper “skinny bundles” that exclude less popular networks, “over-the-top” on-demand viewing, and “short-form” mobile device viewing via platforms like Snapchat or Facebook. To illustrate this point, on the same day that the deal was announced Discovery disclosed that the pace of subscriber decline in its core US subscriber base accelerated to 4% in 2017 vs 3% in the prior quarter and 2% in the prior year. Scripps reported continued subscriber declines and guided down on forecast 2017 revenue and profits on weaker ratings. The concerns of shareholders were exacerbated by the knowledge that they cannot realistically block the transaction due to the dominant position of co-controlling shareholders John Malone and the Advance-Newhouse family.

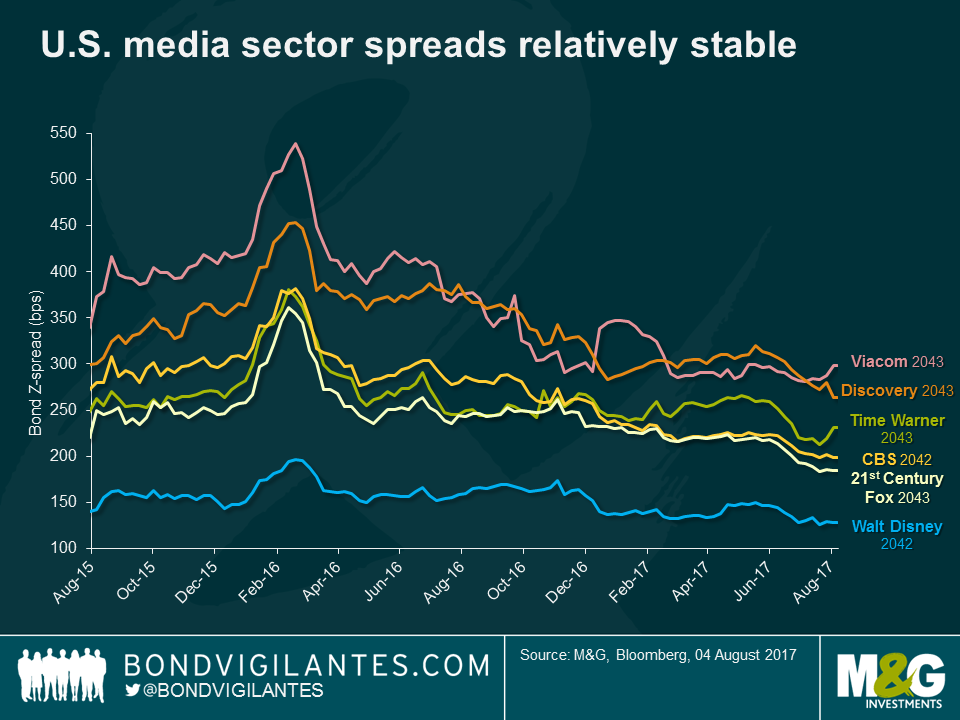

What surprised me most was the reaction of credit markets. The transaction is structured in an equity friendly manner with Scripps shares acquired with 70% cash (funded via incremental Discovery debt) and only 30% by Discovery equity issuance. Combined with around US$3bn of Scripps debt that Discovery will also be assuming, this will increase Discovery’s pro-forma leverage from 3.3x to 4.8x. This will more than double Discovery’s pre-transaction debt load with almost US$11bn incremental debt on the balance sheet. Of course, Discovery points to US$350m cost synergies and suspension of the stock buyback programme to support post-deal debt reduction towards a new 3.0-3.5x target. This is little comfort in a market suffering the aforementioned structural pressures with an issuer with an itchy M&A trigger finger. So what’s not to concern you as a creditor? Apparently not a lot if you are a rating agency, with both S&P and Moody’s affirming Discovery’s weak investment grade ratings at low-BBB. And it’s a similar story for bondholders who saw risk spreads barely move on the news.

So which reaction better reflects the news of Discovery’s acquisition of Scripps? In our view, the wisdom of equity market caution could, in this instance, stand in stark contrast to credit market and rating agency insouciance. For corporates, the lesson is clear: acquire assets and growth by exploiting cheap credit in a yield hungry environment underpinned by rating agency leeway on leveraging transactions. For credit investors, the message is equally clear: beware of M&A driving up leverage with limited incremental spread reward on new issuance to reflect a rising risk profile and potentially false comfort on the lack of spread widening on existing bonds in your portfolio.

This week, Ritu Vohora, investment director in M&G’s equities team, joined me on the BVTV sofa to discuss the curious case of the de-correlation between equities and bond yields. Why are stocks and bonds both rising at the same time, and which market is giving the true outlook for the global economy?

Also this week: is Venezuelan debt in a death spiral? And what to watch out for in the markets.

Guest contributor – Jean-Paul Jaegers, CFA, CQF (Senior Investment Strategist, Prudential Portfolio Management Group)

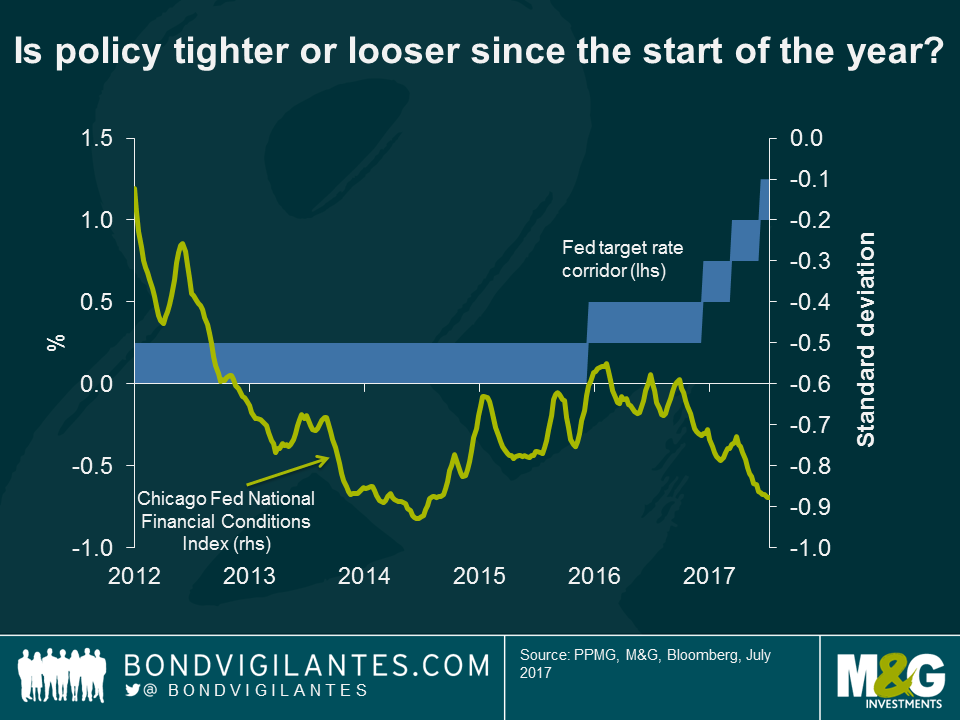

A lot has been written on the recent softness in US inflation data, as headline inflation pulled back, with a similar trend in core inflation. Admittedly, a number of unusual factors have partly been a driver behind this, although more importantly there is quite some persistence in the broad-based softness in inflation. In recent communications by the Federal Open Market Committee (FOMC) members (more specifically by Chair Yellen) the uncertainty in the outlook for inflation has been highlighted and only part of the recent softness in inflation was deemed transitory. Interestingly, in Fed communications there is more and more reference to “financial conditions”. This is important.

The policy rate set by the central bank indirectly impacts the economy, not directly. It is therefore important to assess financial conditions in order to assess the impact that a central bank’s monetary policy stance is having on the real economy. The chart below illustrates that although the policy rate corridor has been raised, financial conditions have eased over that same period. Thus for the real economy, one could possibly argue that Fed policy has so far had limited direct impact.

The Fed has been referring in minutes that “a few” members of the FOMC are more worried about the risk of financial stability than Chair Yellen. And potentially, easier financial conditions may at the margin encourage the Fed to lean a bit against asset price bubbles.

Central bankers have made relatively explicit statements that as financial conditions have become easier, policy needs to be tightened in order to have the appropriate effect on the economy. This would be an important nuance as a continuation in easing of financial conditions (i.e. lower USD, higher equity prices, lower interest rates, etc.) could potentially strengthen the case for a continuation in tightening either via the policy rate or through balance sheet adjustment. Thus if the Fed were to start focussing more on financial conditions and financial stability, it may potentially sound more hawkish than inflation data and dynamics would currently suggest. Central banks want this tightening to come about gradually, but the brief history of unconventional monetary policy suggests that asset re-pricing tends to occur abruptly.

How could this potentially impact the investment landscape? For fixed income investors, the narrow spreads for high yield bonds might be something to shy away from as the volatility may pick up for risk assets. More focus on the risk of financial instability, in the absence of inflation picking up will likely result in a flatter yield curve (due to a flatter term premium and absence of an inflation risk premium). For equity investors that have so far enjoyed a ‘Goldilocks’ environment of stable growth, monetary accommodation and low inflation, this may be something to monitor. Looking at history, the track record of central banks addressing worries about potential financial instability has often been less impressive, as the transmission mechanism and policy dynamics are extremely hard to control and assess. Now is the time to keep an eye on the developments in financial conditions, as year-to-date the market has experienced quite an easing, and this has sparked enough interest in the Fed that it has featured as an important undercurrent of recent communications.

This content is prepared for information and does not contain or constitute investment advice. Neither PPMG, nor any of its associates, nor any director, or employee accepts any liability for any loss arising directly or indirectly from any use of this material.

On August 4th last year, the Bank of England announced a series of easing measures in response to the Brexit referendum results. They were very concerned regarding a potential slowdown and collapse in both the economy and corporate confidence and so implemented a variety of measures; reducing interest rates, increasing liquidity lines for banks, and reintroducing their gilt and corporate bond purchase programmes. Since then, growth has remained positive, and unemployment has continued to be low. The measures appear to have helped.

These ‘crisis response’ measures are however not new, having previously been implemented in 2008 to similar effect, in response to the far larger financial crisis. Though this time around, being near the limit of zero rates in 2016 meant the Bank leaned more heavily on non-conventional monetary policy measures, as illustrated in the table below.

| Post-Lehman | Post-Brexit | |

| Rate cuts | 4.50% | 0.25% |

| Gilt purchases | £375bn | £60bn |

| Corporate bond purchases | £2.3bn | £10.0bn |

| Term Funding Scheme Loans | £41,836m | £33,828m |

| Change in unemployment | + 2.17% * | – 0.26% ** |

| Change in inflation (CPI, yoy) | – 2.2% * | +2.1% ** |

* November 2008 – November 2009

** June 2016 – August 2017

The scorecard above illustrates the differences economically and in terms of policy response. The Bank used the same policy tools, though more unconventionally weighted, when faced with a smaller crisis. The most notable feature is the disproportional purchase of corporate bonds this time around versus other measures; four times as much corporate quantitative easing has been undertaken compared to the Great Financial Crisis. This was due to fears that companies would not be able to fund themselves and financial dislocation would occur. Partly as a result of the Bank’s emergency actions, markets fortunately remained firmly open – here and abroad – for U.K. companies.

Glancing back to the scorecard which demonstrates the stability of markets over the last year (i.e. with unemployment continuing to fall), the need for aggressive monetary policy and emergency measures has lessened. The chart below shows corporate bond spreads in the U.K. Although they did widen on the shock Brexit vote, they have since returned to new post financial crisis tights. The Bank is in agreement that aggressive emergency measures are no longer necessary; it has completed and ceased its corporate bond buying programme, and recently committee members at the Bank have been advocating the reversal of the ‘emergency’ rate cut of 2016. This is in stark contrast to this time last year when the Bank had a bias towards easing. A reversal of policy appears to be on the cards.

From a rate perspective, removing the quarter point cut is not that dramatic as the conventional policy response was limited last year. From a corporate bond perspective however, selling the corporates back to the market could potentially weigh on the performance of sterling corporate bonds held by the Bank.

During the Great Financial Crisis the Bank bought bonds from March 2009 and completed selling them back to the market by April 2013, this time round they bought them in a seven month window from September 2016 to April 2017. Will the Bank now sell these holdings and if so, when?

In answer to the first question, I think they will. The one major unwind of emergency policy of the Great Financial Crisis was the selling back of the non-gilts purchased, to the market; I do not see why it should be different this time. Indeed we have a situation where the Bank wants to potentially tighten policy, the need for emergency funding appears low, and in fact the Bank has been arguing recently that lending conditions are getting too lax from a prudential perspective. One way to solve this is to let the private sector fund corporate debt, having been potentially crowded out of that option by the Bank’s significant corporate bond buying programme.

Going forward there are still Brexit uncertainties, but one aspect perhaps less so: the Bank of England meetings will at some point not only be discussing the direction of interest rates, but when to sell its corporate bond holdings.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.