Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

And they say German elections are boring… As the preliminary results are in, here are our three key takeaways.

(1) Merkel goes fourth

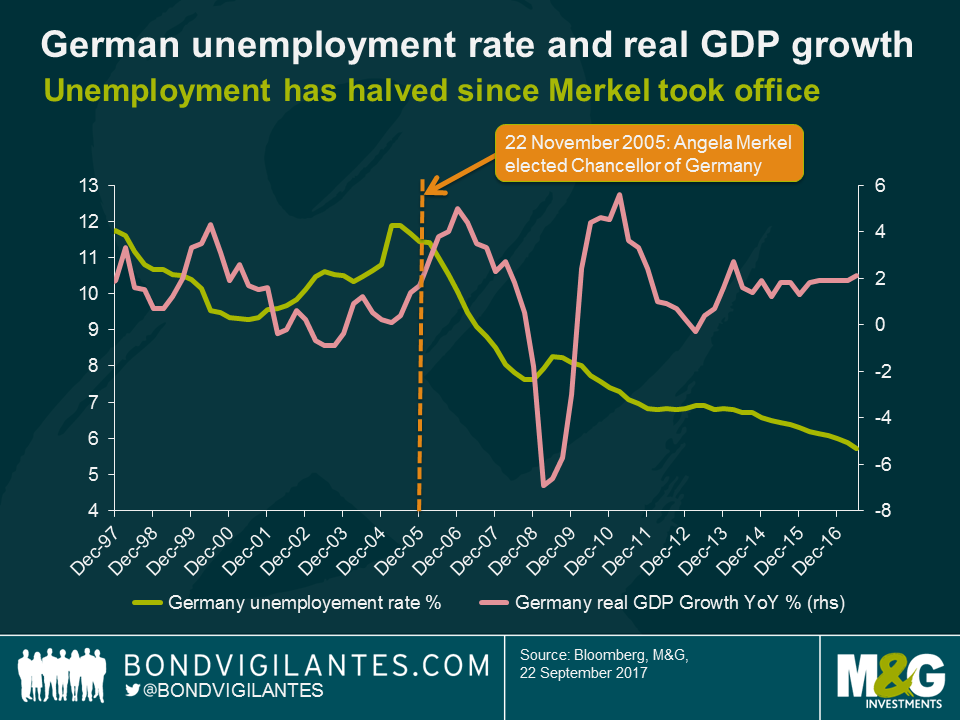

First things first, as expected Angela Merkel has won the election. Her CDU, in combination with its Bavarian sister party CSU, is going to remain the largest faction in parliament (33.0% of votes combined). All roads lead to a fourth term for her as chancellor. This didn’t come as a surprise, of course, particularly considering the strength of the German economy. The unemployment rate has halved since Merkel first took office in November 2005 and GDP growth is above 2%.

However, this is not the main story. The CDU/CSU experienced severe losses, dropping by 8.5% compared to the 2013 elections, which is all the more significant considering the strong economic backdrop, which should actually have been a tailwind for Merkel as the incumbent chancellor. Two factors might have played a key role: “Merkel fatigue” – after twelve years in office many voters probably thought it was time for a change of management. Furthermore, her handling of the refugee / immigration crisis has alienated voters at the conservative end of the political spectrum.

(2) Game of coalitions

Merkel’s current coalition partner had a pretty rough night, too. The SPD only got 20.5% in the election, a new record low. They were quick to rule out a continuation of the so-called grand coalition with Merkel’s CDU/CSU. This would follow some logic, of course. Both ruling blocs – CDU/CSU and SPD – are facing significant losses, which doesn’t seem like a particularly strong mandate for “business as usual”. Establishing themselves as a strong opposition leader might also help the SPD position themselves as a credible alternative to the CDU/CSU in the next elections. Time will tell whether they are genuinely willing to give up power and leave the coalition or whether they are merely playing hardball to improve their bargaining position in coalition negotiations.

Apart from a grand coalition, the only other realistic option would be a “Jamaica coalition” between CDU/CSU, FDP and Green Party – it’s called this because the combined black, yellow and green party colours match those of the Caribbean island’s flag. This coalition has happened before in German state parliaments, for example currently in Schleswig-Holstein, but there are certainly major obstacles on a federal level. The Green Party has ideological differences with the liberal FDP (economic policy, tax reform, etc.) and the conservative wing of the CDU/CSU (immigration policy, social issues, etc.). This could make a Jamaica coalition rather instable and pre-occupied with infighting.

Whether we end up with a grand or a Jamaica coalition in the end, negotiations are going to be tough either way and might drag on for a while. This clearly weakens Merkel’s position both inside Germany and abroad. She might get challenged by French president Emmanuel Macron for the unofficial leadership role within the EU. If he is able to seize the moment, this would make Eurozone debt mutualisation and the creation of a European finance minister more likely, at least in the medium term. Merkel’s rumoured plan to install Jens Weidmann, the current President of the Bundesbank, as new ECB President after Draghi’s term ends in 2019, seems less realistic today. This increases the odds of a continuation of the ECB’s expansive policy stance.

(3) Populism is back with a vengeance

One of the most striking election results is certainly the strong performance of the right-wing nationalist AfD (12.6%). Not only is the party entering the German Bundestag for the first time but the AfD is going to become the third largest faction in parliament. If the grand coalition is continued – which can’t be ruled out entirely at this point – the AfD would de facto become the opposition leader. While this is certainly noteworthy, to say the least, the direct political implications are likely to be minimal. None of the other parties is going to form a coalition with them and AfD members of parliament are likely to be treated as political pariahs. We have seen this happening in German state parliaments many times before.

However, I think there might be two important indirect consequences of the AfD’s electoral success. First, within Germany the pressure on Merkel, not least from her own party, with regards to policy changes is going to build up. For obvious reasons, preventing the rise of a right-wing nationalist movement has been a central dogma in German politics. That’s out of the window now after the AfD’s double digits score last night – on Merkel’s watch. In the past, she has been willing to revise long-held positions (on nuclear power, the minimum wage, same sex marriage etc.) when she felt that sentiment amongst voters was shifting. In order to prise back votes from the AfD she might change tack again, possibly turning more conservative, with a stricter stance on migration, EU centralisation and so on.

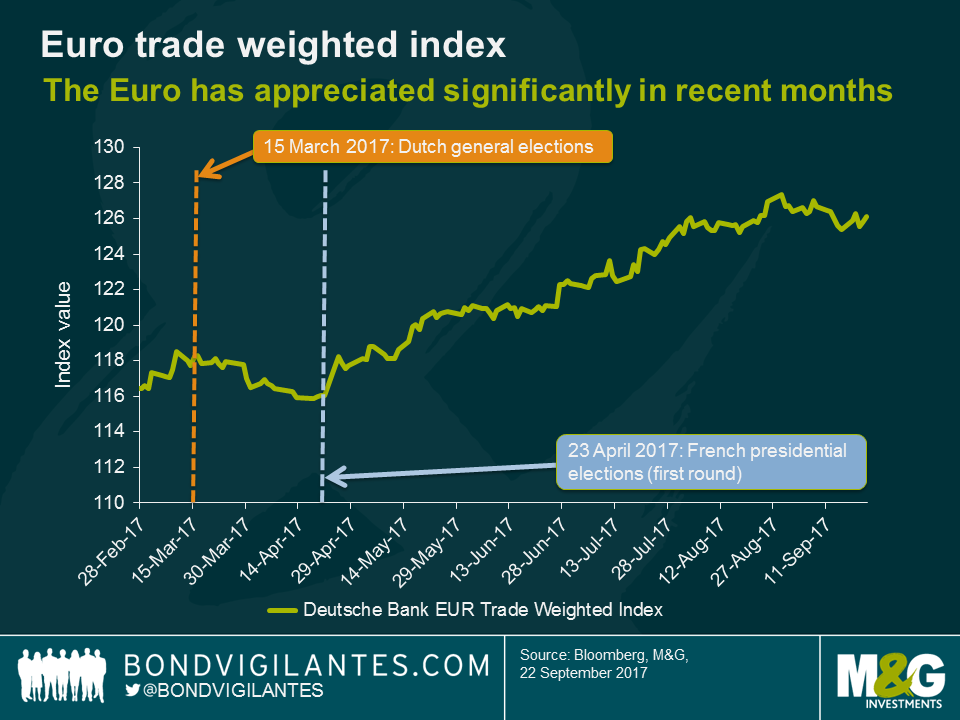

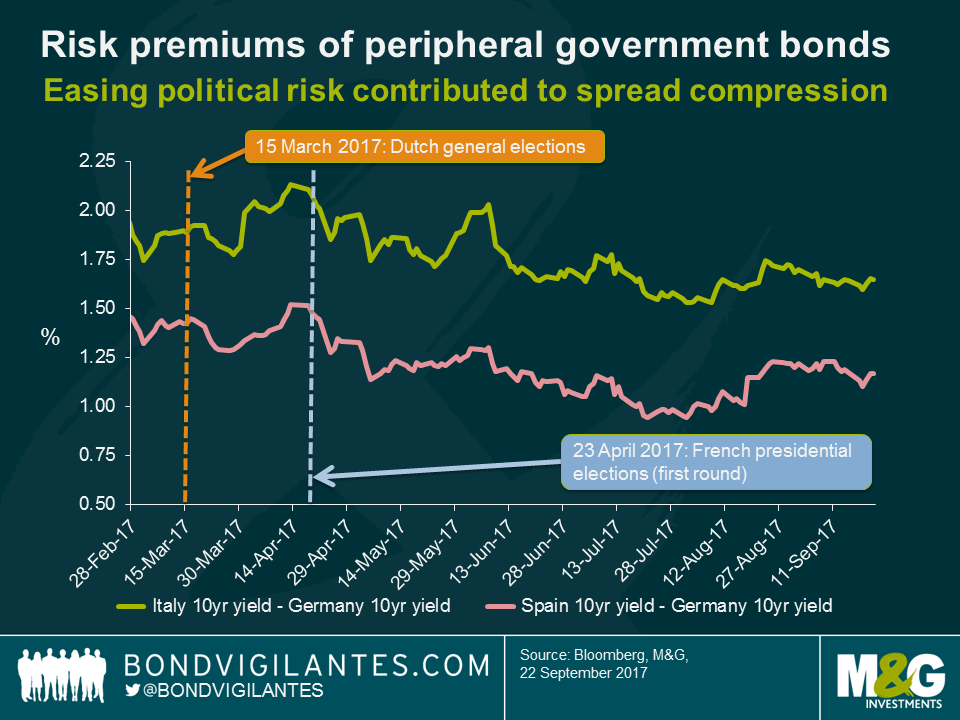

Secondly, the success of the AfD at the ballot box might challenge the prevailing narrative, particularly since the Dutch and French elections, that anti-EU populism is on the decline. This could have implications for markets, which arguably have become somewhat complacent in this regard. The Euro, which has been going from strength to strength in recent months, might get under pressure. Compressed peripheral risk premiums for government and corporate bonds might widen again, considering that there are more political events on the horizon, namely the Catalan independence referendum as well as elections in Austria and Italy.

In today’s environment of solid, synchronised economic growth and low volatility, it is easy to believe such conditions are well set to continue. Did you know that we are now in the third longest bull run in the history of financial markets?

This week on BVTV I look back at the run-up to previous market bubbles and discuss what the Fed’s long-awaited balance sheet reduction announcement could mean for today’s investors. Tune in for the latest!

In December 2012, the then Governor of the Bank of Canada, Mark Carney, gave a speech entitled “Guidance” to the CFA Society of Toronto. Less than two weeks earlier, the UK Chancellor of the Exchequer, George Osborne, had announced that Carney would be the 120th Governor of the Bank of England (BoE). As this was Carney’s first public engagement since the announcement, traders and market economists waited in anticipation to hear from the new Governor (you can read our initial analysis of the speech here).

The speech will be remembered for the radical measures that Carney said central banks should take when interest rates are near zero. These included commitments to keep rates on hold for an extended period of time and setting numerical targets for unemployment. It is interesting that some of the proposals that Carney mused upon in the speech were subsequently incorporated into the BoE’s monetary policy framework. In August 2013, Carney broke with tradition and introduced forward guidance which was contingent on three “knockouts” events that incorporated the BoE’s forecast of inflation, inflation expectations, and financial stability. The forward guidance also hinged on an unemployment threshold, with the Monetary Policy Committee (MPC) stating that it would not hike interest rates until the unemployment rate fell below a threshold of 7%. Incorporating numerical thresholds for inflation and unemployment into forward guidance was precisely what Carney had stated in his speech in Toronto nine months earlier.

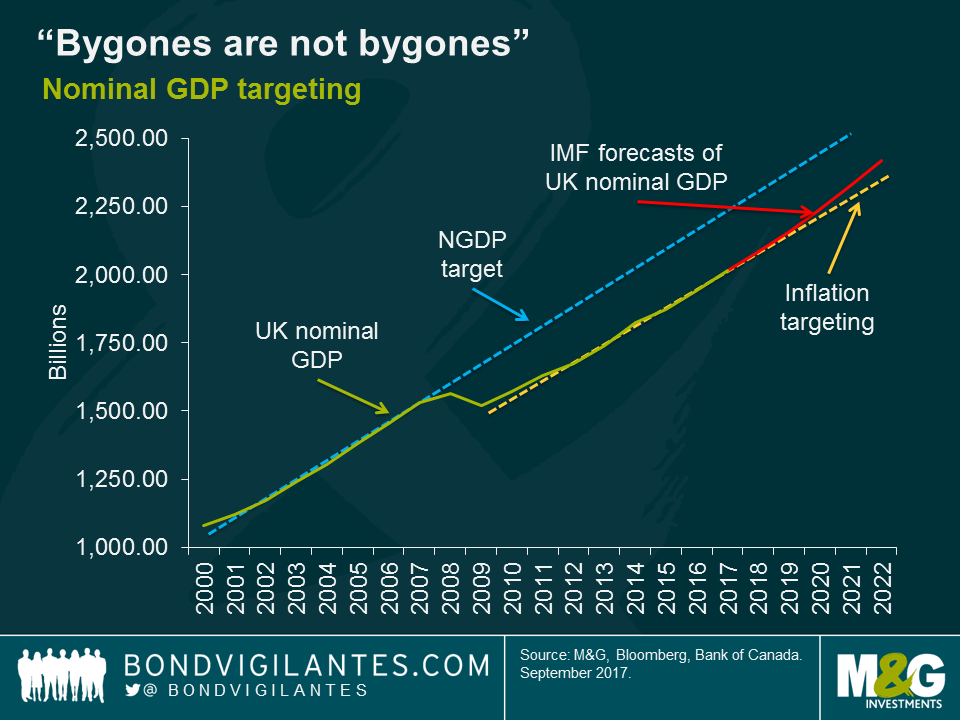

Carney included another important option that central bankers could use to guide economic agents in his speech that day. The Governor discussed the potential adoption of nominal GDP (NGDP) target, stating that

“…adopting a nominal GDP (NGDP)-level target could in many respects be more powerful than employing thresholds under flexible inflation targeting. This is because doing so would add “history dependence” to monetary policy. Under NGDP targeting, bygones are not bygones and the central bank is compelled to make up for past misses on the path of nominal GDP.”

He went on to say

“…when policy rates are stuck at the zero lower bound, there could be a more favourable case for NGDP targeting. The exceptional nature of the situation, and the magnitude of the gaps involved, could make such a policy more credible and easier to understand.”

Under NGDP targeting, Carney said that “bygones are not bygones”. The central bank is compelled to make up for past misses by targeting higher rates of NGDP growth to return the economy to its previous trend. In the short-term, targeting NGDP would allow the MPC to retain an easy monetary policy stance, even if inflation is above the Bank’s target for a sustained period of time.

It appears that many of the conditions that Carney stated in his speech could be applied to the UK economy today. The Bank Rate is only 0.25%, close to what economists call the zero lower bound on nominal interest rates. The UK is committed to leaving the European Union, which is clearly an exceptional situation and will likely have a large impact on the UK economy. The rate of inflation is above the BoE’s target, at 2.9%. And finally, the UK’s NGDP level has not returned to its pre-crisis trend and, according to IMF forecasts, is unlikely to do so for the foreseeable future.

With market expectations for an interest rate hike in December rising from around 20% to 72% over the past week despite the Brexit induced clouds that hang over the economy, is now the time for the BoE to consider a shift toward NGDP targeting? Central bank regimes have come and gone throughout history (such as fixing the price of gold, money supply targets, and exchange rate targets), and inflation targeting has only been the main goal of the BoE’s Monetary Policy Committee since 1998.

The advantage of a NGDP target is its robustness. For example, if productivity rises and inflation falls, an inflation-targeting central bank would likely ease policy, potentially generating asset bubbles. Under a NGDP target regime, prices would be allowed to fall. Alternatively, if prices rise due to an external event (such as higher oil prices), an inflation-targeting is compelled to hike interest rates, thereby reducing growth. One wonders if the ECB could have avoided hiking interest rates in July 2008, just as the European economy entered into recession, if it had been targeting NGDP instead of price stability.

Today, the MPC faces a difficult decision. There are signs that the economy is slowing, inflation is likely to peak in the next few months as the large depreciation in sterling and its impact on import prices falls out of annual calculations, and the political landscape both domestically and in the context of Brexit is challenged. The market is pricing in higher rates given the hawkish tone of the minutes of the MPC’s September meeting, which reflects the view of some members that an interest rate hike could mitigate the risks of a sustained period of above-target inflationary pressure. The question is, are these inflationary concerns justified, or could the MPC be about to repeat the mistake of the ECB’s governing council in 2008?

Next week, the Bank of England will be holding a conference celebrating 20 years of independence. Speakers include Gordon Brown, Fed vice-chair Stanley Fischer, ECB President Mario Draghi and IMF Managing Director Christine Lagarde. It will be interesting to see if Carney revisits his old speech from 2012 in his remarks. He has shown that he is willing to alter the BoE’s policy framework before and altering it again to incorporate a NGDP target may be his parting gift to the Bank and the central banking community before he leaves in June 2019. It would give the MPC some breathing space, and assist them in making the right decision at a very uncertain time.

Ben Lord, corporate bond fund manager and inflation specialist, joined me in the studio this morning, after a week in which we saw both the UK and US CPI prints surprise to the upside. With some central banks ramping up their hawkish rhetoric in recent weeks, what likelihood of rate hikes are markets now pricing in, and what impact is this having on bond markets? Watch BVTV for Ben’s latest thinking.

I’m just back from a fascinating research trip to Mexico City, to meet with policymakers, bankers, politicians, analysts, pension funds and regulators. Like many emerging market economies, the Mexican economy has suffered over the past couple of years due to lower commodity prices and weak global demand for goods. Of course, Mexico has had its own unique challenge with Donald Trump’s election and the potential impact that might have on trade and remittances from Mexican migrants to the US.

In this quick primer on the Mexican economy I look at the five areas that I found especially interesting. In particular there could be significant changes to Mexico’s political landscape.

Thanks go to HSBC for organising some extremely interesting meetings.

Just as the UK, US and Europe have seen their electorates support populist parties and policies in the last couple of years, so too has Mexico. The Morena party is just three years old, but with the experienced anti-system left-winger Andres Manuel Lopez Obrador (“AMLO”) as its presidential candidate it could pull off a big shock in the 2018 Presidential election. AMLO has stood in previous presidential elections for the established PRD party, and is well-known to the electorate. AMLO’s campaign focuses on corruption, and in particular on an assertion that the ruling PRI party, which has had an effective 80-year hegemony in Mexican politics, is rotten. In an August poll, AMLO had the highest voting intention percentage of all the potential presidential candidates, and momentum is currently on his side.

Whilst no-one expects AMLO to win control of Congress as well as the Presidency, he would still be well placed to delay planned reforms to the energy and education sectors, halt some private sector-led infrastructure developments (for example the expansion of Mexico City airport), and tighten Mexico’s NAFTA negotiating stance with the US. AMLO may also reintroduce the gasoline subsidies which have only recently been eliminated. Comparisons with Venezuela’s Chaves are unfair though; AMLO was the mayor of the vast City of Mexico region and ran it responsibly. Nevertheless, comparisons will be made, and investors could start to get nervous as the election approaches. One analyst I met was worried about the potential impact of an election loss given AMLO’s belief that elections are rigged against him: “there won’t be a revolution, but…”.

In 2012 the IMF made recommendations that the Mexican inflation and national income statistics needed to be brought up to international standards. Data had traditionally been collected from larger towns and cities, but smaller, rural settlements were not surveyed. As these tend to be poorer areas, the household spending patterns which were used for the inflation component weights had been skewed to the spending patterns of relatively richer Mexicans. This meant that services have had a relatively high weight in CPI.

From July next year the weights in the inflation data will include far more rural communities: as a result the goods weight in the inflation basket rises from 34% to 41%, and within this, food rises from 15% to 21%. The implication for monetary policy, and holders of inflation linked bonds, is that inflation will become even more volatile as food prices are erratic (onion and tomato prices have skyrocketed in Mexico lately), and because goods prices are very sensitive to the level of the Mexican peso. It seems politically impossible for the Bank of Mexico to target only “core” inflation rates – the headline number is everything.

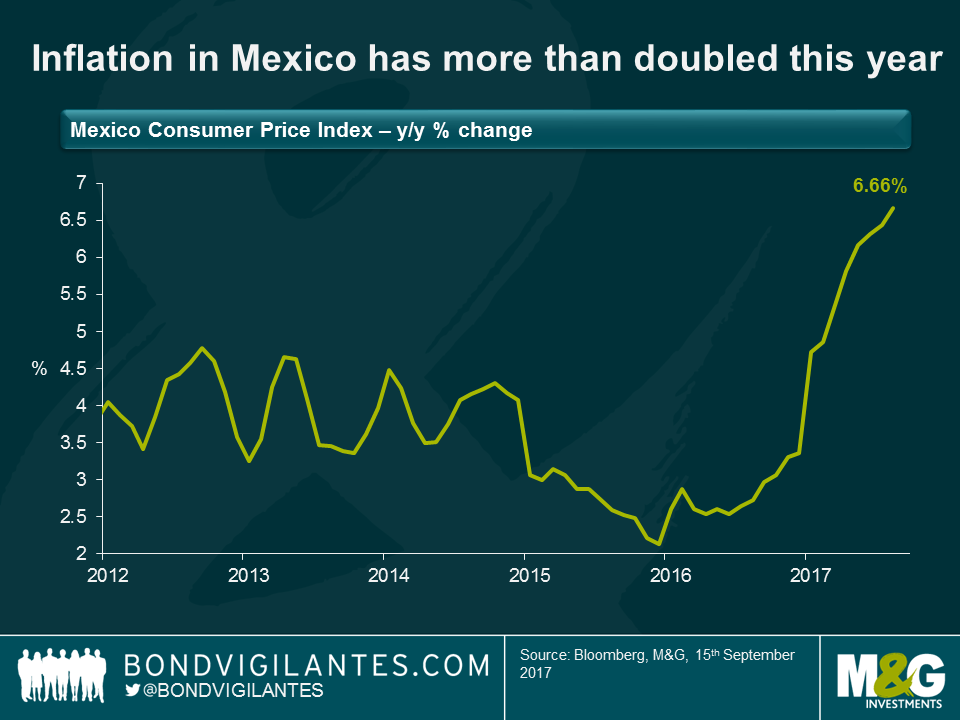

Mexico’s inflation rate has more than doubled this year, to the devilishly high level of 6.66%. Part of this move is as a lagged result of higher import prices following the peso’s depreciation to MXN 22, partly it’s due to those tomatoes (red AND green) and onions, and the rest is explained by the liberalisation of gasoline prices in January (itself adding 1.3% to inflation). The Bank of Mexico’s target is 3%. Whilst breakeven inflation rates derived from linker prices don’t suggest the Bank will quite achieve that target over the medium term, 2018 will see a significant fall in inflation, simply reflecting the base effects of 2017’s price rises falling away, and a stronger peso. Whether this will allow the central bank to cut rates is another question…

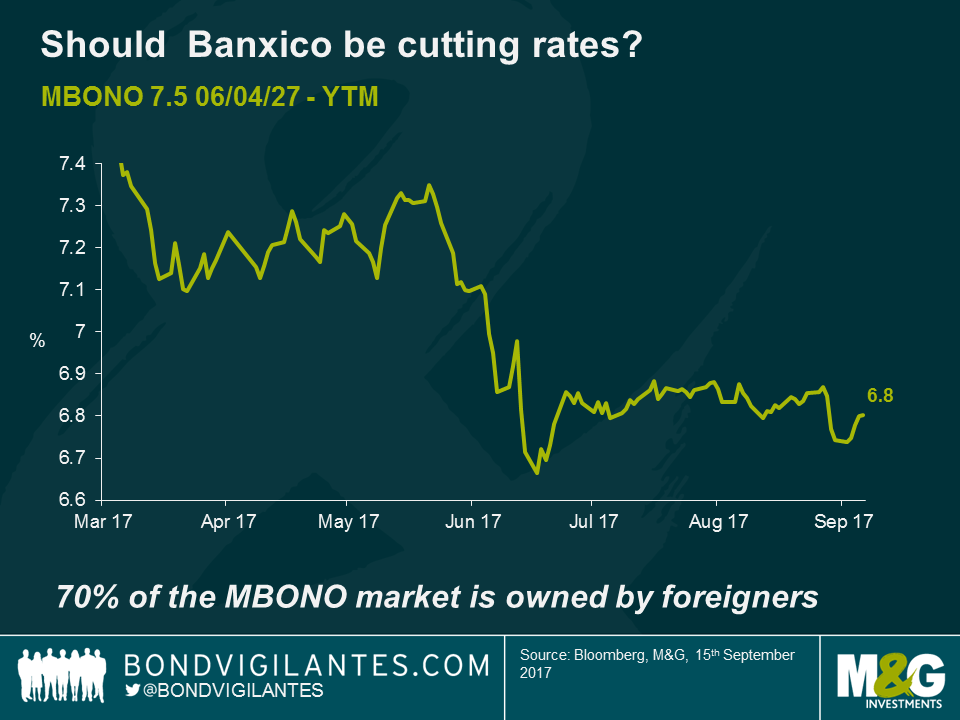

Emerging markets central banks have a different approach to managing monetary policy compared to their developed market counterparts. Whilst both set rates to manage consumer, business and market inflation expectations, the Fed for example will hike rates to influence demand, whilst the Mexican central bank knows that the penetration of variable rate loans, especially amongst consumers, is extremely low and that a rate hike (or cut) will thus have little impact on economic activity.

The transmission mechanism for EM central bankers works disproportionately through the exchange rate. Cutting rates will cause the exchange rate to weaken, which will result in more expensive imported goods prices (and significant second round effects – for example taxi drivers in Mexico put their peso fares up to keep the dollar value of those fares constant, above and beyond what might be the direct rise in imported fuel costs). A rate cut might therefore result in a drag on economic growth, rather than a stimulus. The Bank of Mexico, unlike the Fed, has just one policy target, which is inflation (not inflation and employment, and as mentioned, it is headline inflation, not core). With inflation almost certain to fall sharply in 2018, should the Bank be cutting rates already? And does this make the bond market look cheap (the 10 year MBONO yields 6.75% at the moment)? In theory yes, but the policymakers have two potentially peso-negative shocks to worry about; firstly the aforementioned presidential election volatility, and secondly a possible failure of the NAFTA negotiations. 70% of the MBONO market is owned by foreigners – a huge percentage, and most do not hedge the currency risk. Falls in the peso due to these factors and rate cuts could see the peso retest or exceed the “Trump-fear” lows, and selling could threaten financial stability. So the Bank of Mexico is yet to cut, and may be more cautious than the pure inflation forecast would predict. Perhaps they pay more attention to the level of foreign participation in their asset markets than I previously imagined.

Elsewhere, the Bank is puzzled over the same issues as developed market policy makers – why is there no wage pressure, despite falling unemployment rates? And is their neutral real rate estimate (r*) for Mexico too high at, say, 2.5% if the US’s r* is actually zero rather than an assumption that it’s 1%?

With the Trans-Pacific Partnership (TPP) scrapped by Donald Trump immediately upon taking office, attention now turns to his pledge to renegotiate the NAFTA agreement between the US, Canada and Mexico. Trump has three main areas of contention. Firstly, that the trade deficit that the US runs with Mexico must fall. Secondly, that Mexico should increase workers’ wages towards those in the US. Thirdly, that the “Rules of Origin” must be tightened such that more of the regional content in manufactured goods comes from within the NAFTA area (and preferably from within the US).

All three goals are contentious, and difficult to deliver without damaging the Mexican (and probably the US) economy. The third (of seven) round of NAFTA renegotiation talks begins in October. One trade expert we talked to suggested that the subsequent 4th and 5th rounds later this year would be the most precarious, and that Trump might be minded to withdraw from NAFTA then.

The good news is that most experts suggest that Mexico’s “Plan B” would mitigate much of the damage that NAFTA’s scrapping would cause. It would still trade under WTO’s Most Favoured Nation status with the US, with generally moderate tariffs; it’s possible that those WTO tariffs would not deter trade if a likely peso depreciation made Mexico’s goods cheaper to US dollar buyers; and it is negotiating other trade deals around the world to open up new markets (the EU, Brazil).

It’s difficult to imagine that a Trump tweet in November announcing the end of NAFTA wouldn’t send Mexican assets lower however, at least in the short term.

Historically many emerging market governments have subsidised the price of fuel for their populations, and especially those with ample reserves of oil. It’s a popular policy with voters, and helps to insulate a low income economy from volatility in global energy markets. However, it became very expensive for Mexico when oil prices were $100 per barrel a few years ago while its “cash cow”, the Cantarell Oil Field (named after the fisherman who discovered it), saw production collapse (from 2.1 million barrels per day to 400,000) causing its gasoline imports to increase.

In recent years then, government policy has been to liberalise gasoline prices, and allow them to move higher towards market levels. As we saw, this has been a big upwards influence on Mexican inflation, especially in January 2017.

Additionally, the government is trying to reduce the influence that the state owned oil giant Pemex has on the nation’s energy supply. Over the years Pemex has provided revenues to finance a huge chunk of Mexico’s fiscal needs, but by prioritising crude oil production at all costs, it neglected investing in maintenance (resulting in unplanned shutdowns 10 times higher than the industry standard), refining capability (resulting in Mexico importing gasoline from the US), and a nation where 40% of towns have no petrol station. In the US there’s one gas station per 2500 people, in Brazil it’s 1 per 5000, in Mexico 1 per 10000.

So on top of a move to end gasoline subsidies, Mexico is now open to competition all across the supply chain. Companies can bid for exploration blocks in the Gulf of Mexico, to build new pipelines, to import fuel by truck from the US, and to run and build gas stations. More competition should result in lower prices for consumers, higher efficiencies in the oil supply chain, and an end to the drag on Mexico’s growth rate that the energy sector has delivered in recent years.

I ate one of these. I’d like to say it tasted of chicken, but it tasted of worm.

Further reading

Claudia wrote about Trump and Latin American remittances here: https://bondvigilantes.com/blog/2021/12/14/the-central-american-remittance-crunch-who-would-lose-most-from-a-trump-presidency/

Charles wrote about NAFTA here: https://bondvigilantes.com/blog/2021/12/26/research-trip-mexico-trump-key-call-emerging-markets/

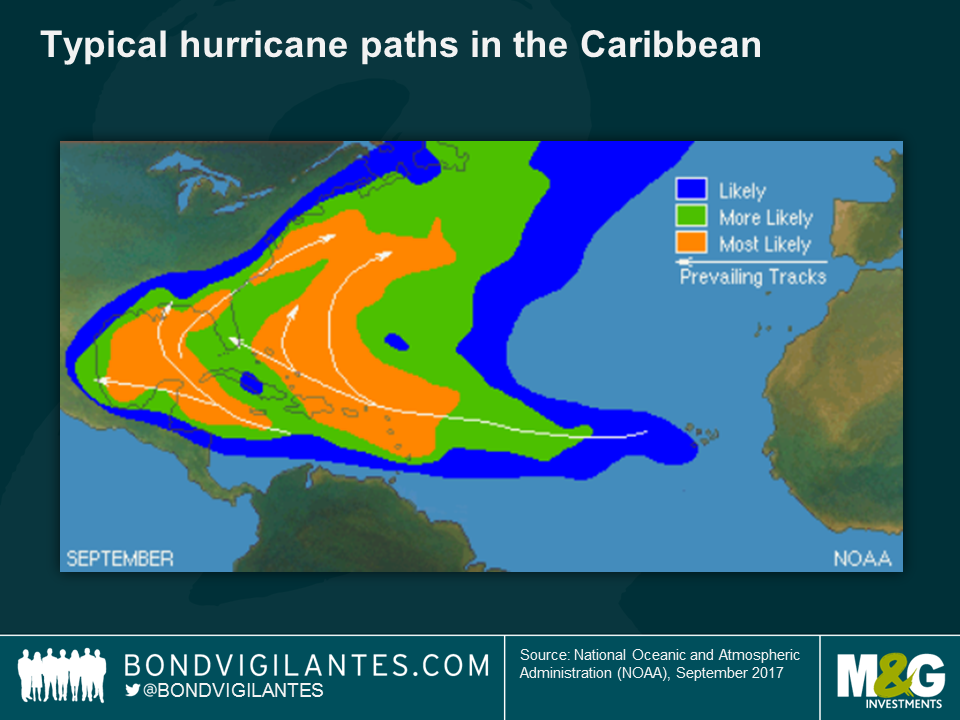

First of all, our thoughts are with those impacted by Hurricane Irma and other recent weather-related disasters.

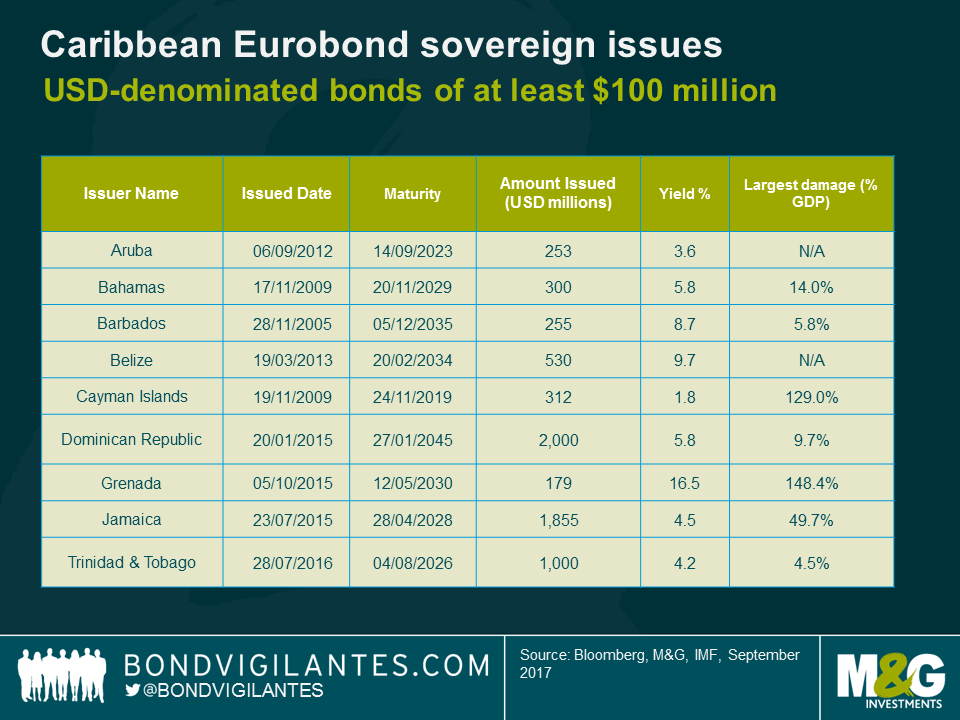

Beyond the human tragedy and economic costs, these are typically low-probability, but potentially high-impact, events that can ultimately impact an issuer’s ability to service its debt obligations. As bond investors, we aim to assess the various risk factors related to the companies we invest in and, ultimately, decide whether we are being well enough compensated for taking those risks.

The chart above lists a sample of USD-denominated bonds of at least USD 100 million issued by various Caribbean countries, where Grenada provides one interesting case study. Grenada, a small and largely tourism-based economy, was hit by Hurricane Ivan in 2004, only two years after its international bond market debut with a sovereign issue maturing in 2012. The damage was widespread, estimated at almost 150% of GDP, impacting physical infrastructure, housing (where only a small portion of the housing stock was insured), agriculture and tourism. The country ended up defaulting and restructuring its bonds with a haircut of approximately 40%.

Delving into the detail of Grenada’s prospectus for that particular bond, we find that it did state that ‘Grenada lies south of the usual track of hurricanes, but when storms do occur, as in 1955, 1979 and 1980, they often cause extensive damage. A major hurricane or other climatic or geological occurrence could have a material adverse effect on Grenada and, as a result, the Government’s financial condition and its ability to meet its debt service and other obligations, including with respect to the note’. For a prospectus that was 94 pages long, with an extensive assessment of Grenada’s economic, geographic and environmental conditions, one may be surprised to see the word ‘hurricane’ appear only twice and the broader word ‘disaster’ just get 15 mentions.

The IMF has recently published a very comprehensive study around the associated costs of hurricane impacts in the Caribbean region. Surprisingly it states that economic damages could be underestimated by material amounts, with the average damage per island potentially being as large as 82% of GDP .

Furthermore, this map comes to show how hurricanes can indeed affect most Caribbean countries, with only very few (i.e. Aruba or Belize) falling outside the main hurricane belt. With this in mind, I would argue that prevailing sovereign bond yields for many of these economies are currently not pricing in a worst-case scenario of being hit by a large-scale weather-related disaster. As in the case of any fat-tail event, caveat emptor.

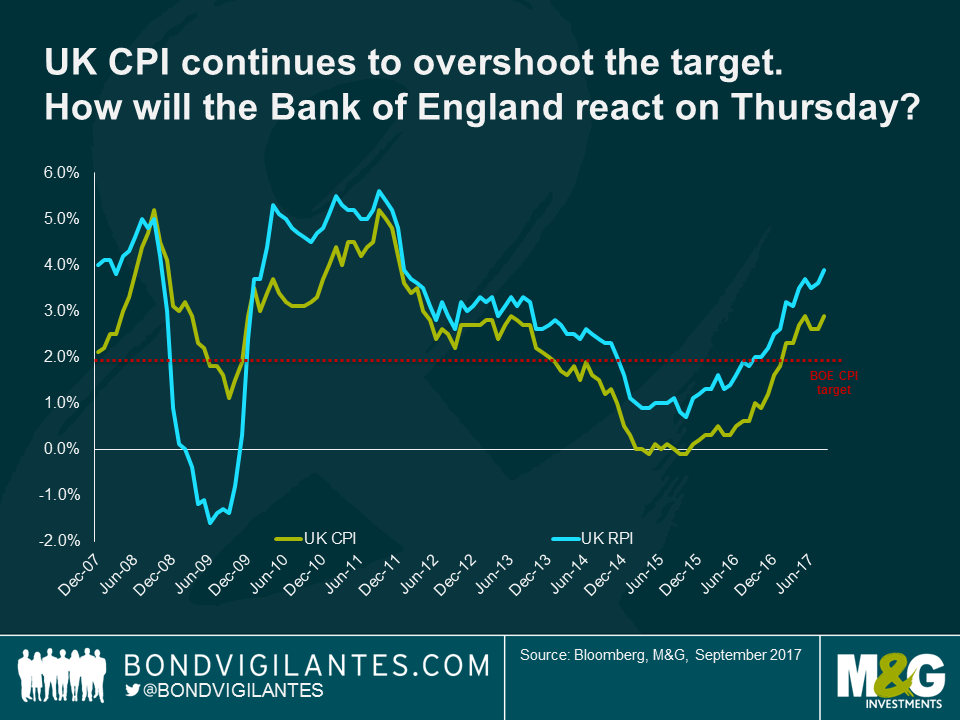

UK CPI is now within a hair’s breadth of requiring a letter to the Chancellor. RPI increased to 3.9% from 3.6%, which was also above expectations. The increased fuel prices were expected this month, but August is also a high inflation month given transport price hikes that take place as people head away for their holidays, and as clothing and footwear prices are hiked with the new season’s collections coming to shop shelves.

But it seems likely that we are close, now, to peak inflation in the UK. Given this, I feel that the MPC should look through any headlines this week and stay their course, given concerns around the outlook for the consumer, and enormous uncertainty about the post March 2019 economy. That being said, I believe that the risks of a 6-3 vote have risen materially on the back of this number, as Andy Haldane has been pretty explicit on his discomfort with present levels of inflation, even if they are due to currency weakness and imports.

Increased disagreement on the MPC will likely lead to some sterling strength, in the short term at least, and it could see some downward reaction in short dated breakevens. But if we are a month or so away from peak inflation, to hike rates, strengthen the pound and reduce breakevens would be overly myopic and pro-cyclical in my view. It seems likely to me that inflation and breakevens are going to start to slide back from here gradually anyway: why accelerate and exaggerate those moves by acting a month or two early?

Perhaps heightened disagreement and debate though is the right policy, especially when combined with at least a cursory discussion on the potential need to raise rates more aggressively than the market is pricing in? If you think inflation does fall back from here, then perhaps you remain bullish on rates and don’t expect the first hike to come in the middle of 2018 and the second hike to come at some point in the second half of 2019. If inflation doesn’t fall back for whatever reason (likely to be sterling weakness on account of Brexit debates), then you probably need to start bringing forward rate hikes and increasing their number. With 10 year gilt yields at 1%, though, the bond market remains firmly nervous on the economy and unconcerned about the risk of hikes at this highly uncertain moment in time.

Dr. Wolfgang Bauer, M&G fund manager, helps manage corporate bond and absolute return portfolios. This week on BVTV I ask him:

Hear Wolfgang’s views as well as a look at the week ahead.

The Slavery Abolition Act of 1833 formally freed 800,000 Africans who were then the legal property of Britain’s slave owners. What is less well known is that the same act contained a provision for the financial compensation of the owners of those slaves, by the British taxpayer, for the loss of their “property”. The compensation commission was the government body established to evaluate the claims of the slave owners and administer the distribution of the £20m the government had set aside to pay them off. That sum represented 40% of the total government expenditure for 1834. It is the modern equivalent of around £23bn.

The distribution of the £20m was entrusted to a Slave Compensation Commission which began to meet in October 1833 and included representatives of the Colonial Office and the slave registry. It worked on data collected by assistant colonial boards of compensation nominated by the governor in each colony, and compensation was allowed on slaves appearing on the books of the slave registry on 1 July 1835. Actual payment of the claims was made by the National Debt Office and began in 1835. The commission was terminated at the end of 1842, but one of the commissioners was appointed as an arbitrator to adjudicate upon outstanding claims. At the end of 1845 all money unappropriated reverted to the public purse. The registry continued in existence until 1848. Enslaved Africans received nothing.

Director of the Centre for the Study of the Legacies of British Slave-ownership at University College London, Dr Nicholas Draper, in his book The Price of Emancipation suggests that approximately half of the £20 million the British taxpayers paid in compensation to slave owners stayed in Britain. According to the BBC, slave-ownership wasn’t confined to the upper classes: an enslaved person was considered a sound investment. In 1833, middle class people including clergymen, naval personnel and people who had returned from the colonies were all slave-owners. Some purchased enslaved people, others acquired them through inheritance or marriage. Their value was based on skills, gender, age, health and the profitability of the plantation where they worked.

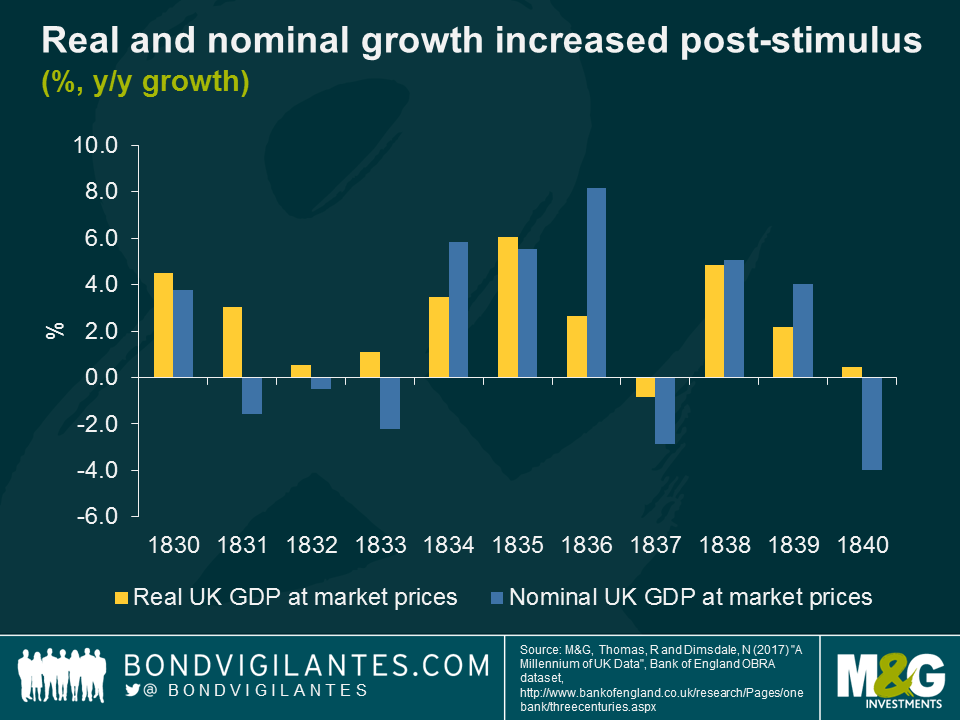

The compensation of Britain’s 46,000 slave owners was the largest bailout in British history until the bailout of the banks in 2009. Using data sourced from the Bank of England, it is possible to gain an understanding of the impact that this large monetary stimulus had on the UK economy. The payments to British slave owners represent a helicopter drop of money into a fairly closed economy, and the impact on growth, inflation, and asset prices should be directly observable.

According to government finances, the bailout was largely funded by government borrowing. In 1835, the public sector registered a deficit of -£15.2m, the equivalent of -2.8% of nominal GDP.

In the basic IS-LM model, the behaviour of the economic agents – consumers, firms, and the government – is reconciled by the product and money markets. The product market balances the demand for product by consumers, firms, and the government with national income. The money market balances the demand for money by consumers and firms with the supply of money provided by the government and the banks. The equilibrium the IS-LM model obtains is the demand equilibrium for the economy.

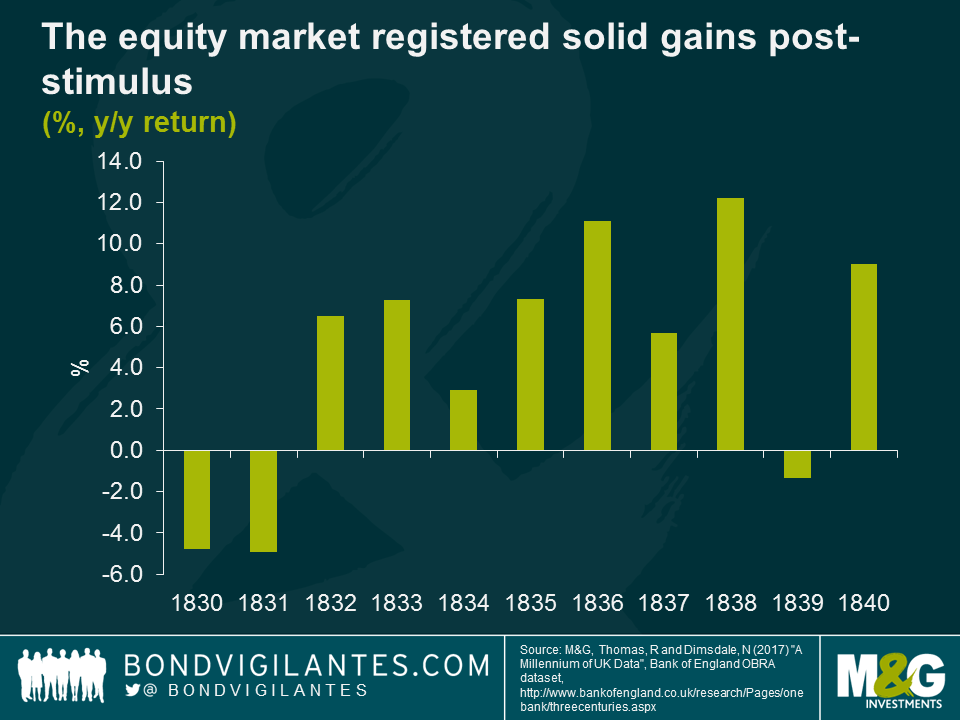

As the economic theory would suggest, the effect of a large cash stimulus was a spike in inflation. This is because the cash stimulus resulted in an increase in aggregate demand due to an excess demand for goods and services. After a four year period of deflation between 1832-35, inflation skyrocketed by almost 10% in 1836.

The increase in aggregate demand resulted in a short-term boost in output. Since in the long-run output is determined by supply factors, a fiscal expansion cannot permanently increase output above its long-run full employment level. Nominal GDP grew by over 8% in 1836, with real GDP rising by 2.6%. In 1837 the economy contracted in both real and nominal terms before returning to positive growth in 1838.

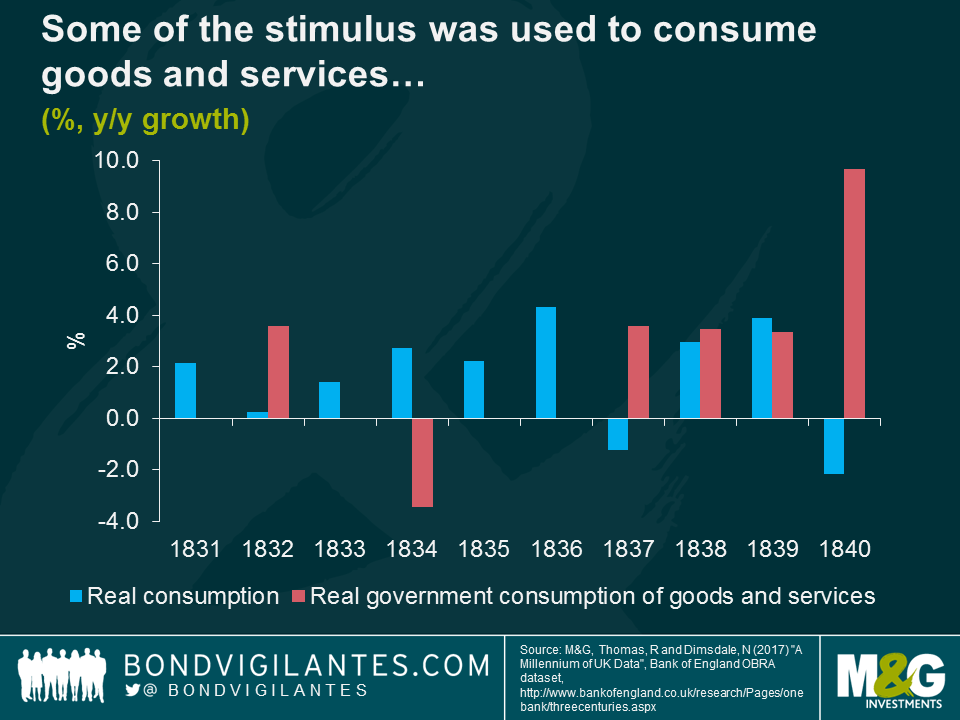

Looking at the drivers of economic growth during the period following the payments, consumption growth almost doubled to 4.3% in 1836. Government spending on goods and services was flat as it had been for most of the preceding years. This is unsurprising given the lack of any social net. Government expenditure was almost entirely spent on defence or spent on servicing the national debt (UK debt to nominal GDP was 155.1% in 1835 and 50% of government expenditure was used to service the debt).

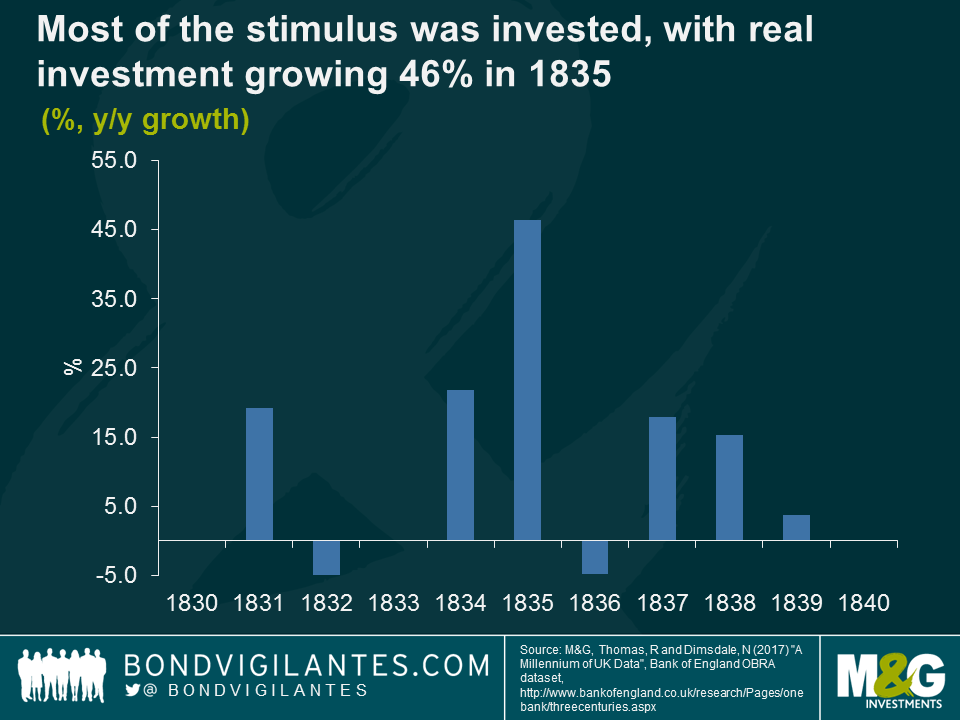

The main impact of the cash stimulus into the UK economy was on private investment which grew by over 46% in 1835. Proceeds of the government bailout were invested in a number of industries including railways, construction, banks, insurance and shipping.

The equity market registered strong gains for most of the 1830s, including an 11% rise in 1836, 6% in 1837 and 12% in 1838. Share prices may have risen as investors recycled cash into shares in corporations. Dr Draper claims that as many as one fifth of wealthy Victorian Britons derived all or part of their fortunes from the slave economy and that up to 10 per cent of Britons who died in the 18th century had benefited.

The amount of money available to the compensation fund reflects how much influence elite Victorians had on the UK government of the day. The fiscal injection of cash into the economy had textbook consequences including an increase in GDP, high inflation and rising asset prices. It is an interesting economic event from Great Britain’s distant past, albeit one generated from the horrors of slavery.

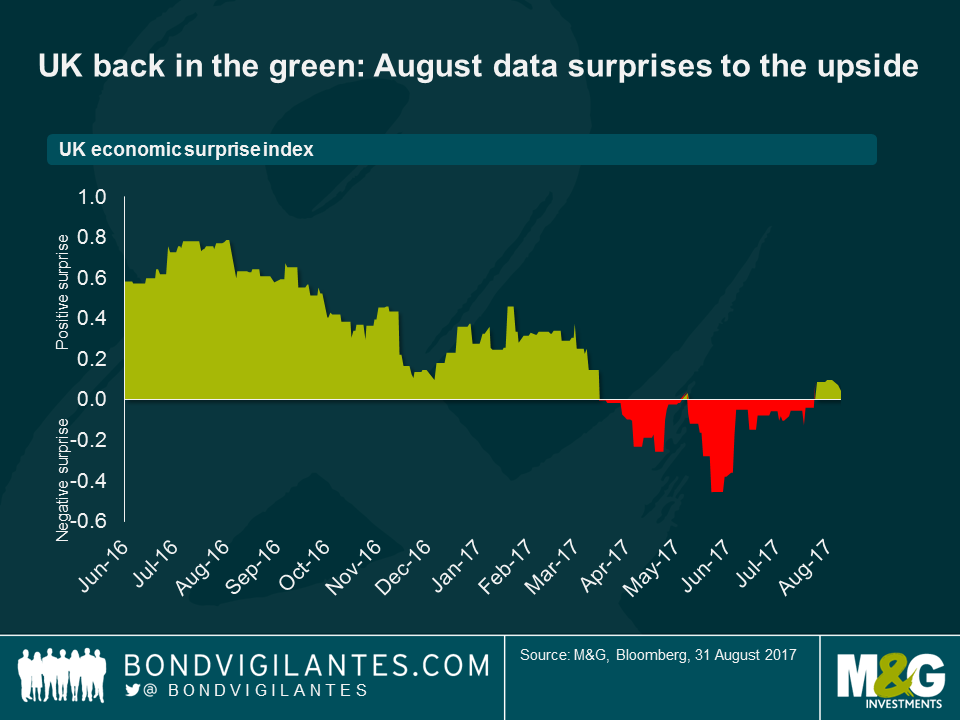

Another month has drawn to an end, which presents a good opportunity to take stock and review recent events and Bloomberg’s surprise monitors – true to their name – have provided some unexpected results in August.

Economic analysts appear to have been too pessimistic in August, suggesting that perhaps too much doom and gloom has been priced into the UK rates market.

Given the Brexit backdrop, I’ve been pessimistic on the economic outlook for the UK, which is in-line with many economists’ thinking (in fact, since the EU Referendum, I’ve not met with a single research house that is bullish or in the least bit optimistic). Although the economic data for the UK held up well into the 2016 year end, this has since rolled over with consumer readings a particular concern. Earnings growth remains subdued, retail sales are trending downwards and the YouGov/Cebr consumer confidence survey recently indicated that consumer perceptions of household finances deteriorated for the fifth consecutive month (the longest negative trend since records began 8 years ago).

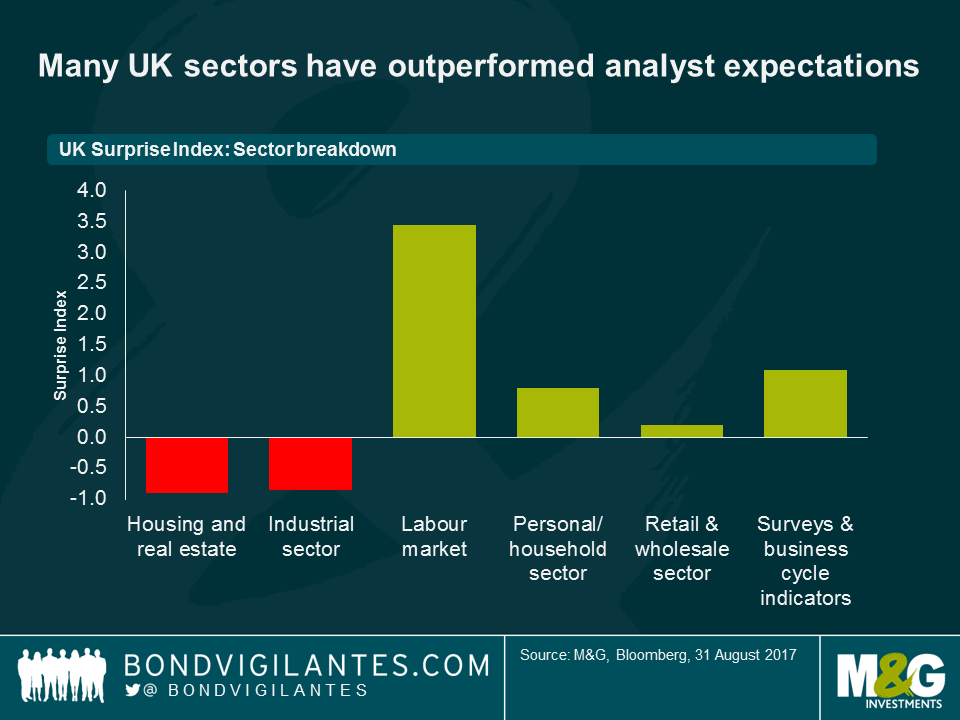

Despite these outcomes, the ingrained low expectations mean that the UK economic data has managed to outperform the low base of expectations. Bloomberg’s surprise indices monitor economic analysts’ expectations and indicate where the underlying business cycle under or overshoots their forecasts. As you can see below, many sectors – particularly the labour market – surprised to the upside in August.

What’s interesting is the effect that this has had on the overall index, where the aggregate UK surprise index moved back into the green in August. This indicates that the economy has outperformed economist expectations, after a run of data surprises to the downside since April of this year. If this trend continues with economic forecasts continuing to underestimate the UK, we could see rates sell off on individual data releases, as market participants start to price in the surprisingly robust fundamentals.

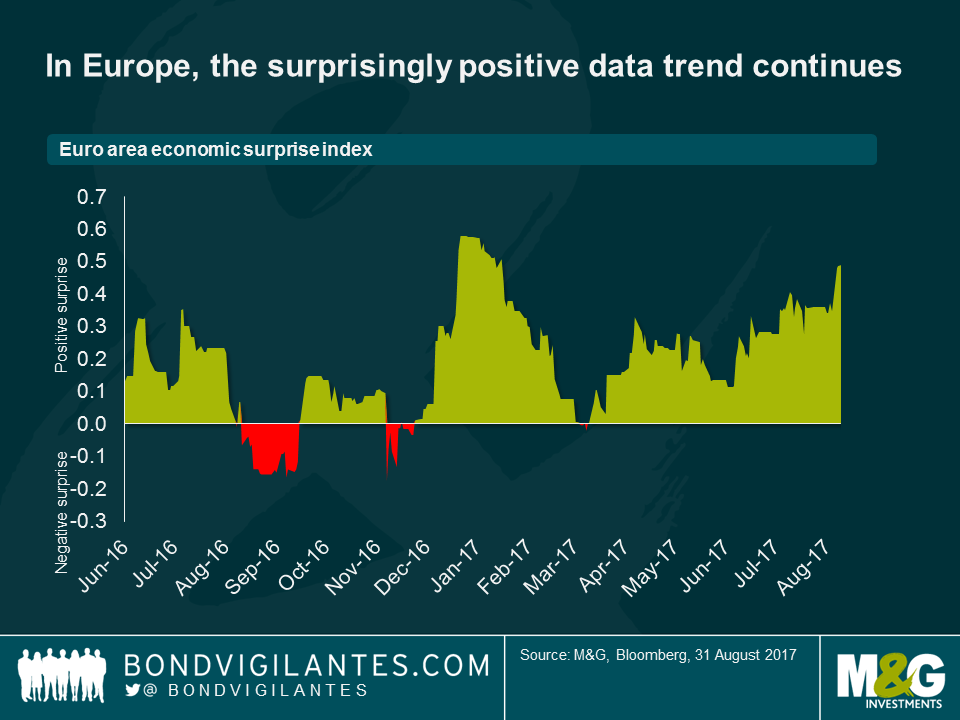

In contrast to the UK, Europe has exhibited an upward trend of positive data surprises over the same time period (i.e. post the EU referendum), with the retail sector and business surveys the main drivers of late. The consistency in positive surprises indicates that economists have perhaps been too cautious in forecasting the Euro area recovery, in line with Draghi’s careful dovish messaging. After this strong run of data releases, if economists were to turn more bullish from here, I would expect to see core Euro area rates sell off, reflecting the improvement in the underlying economy and expectation of more imminent policy normalisation from the ECB.

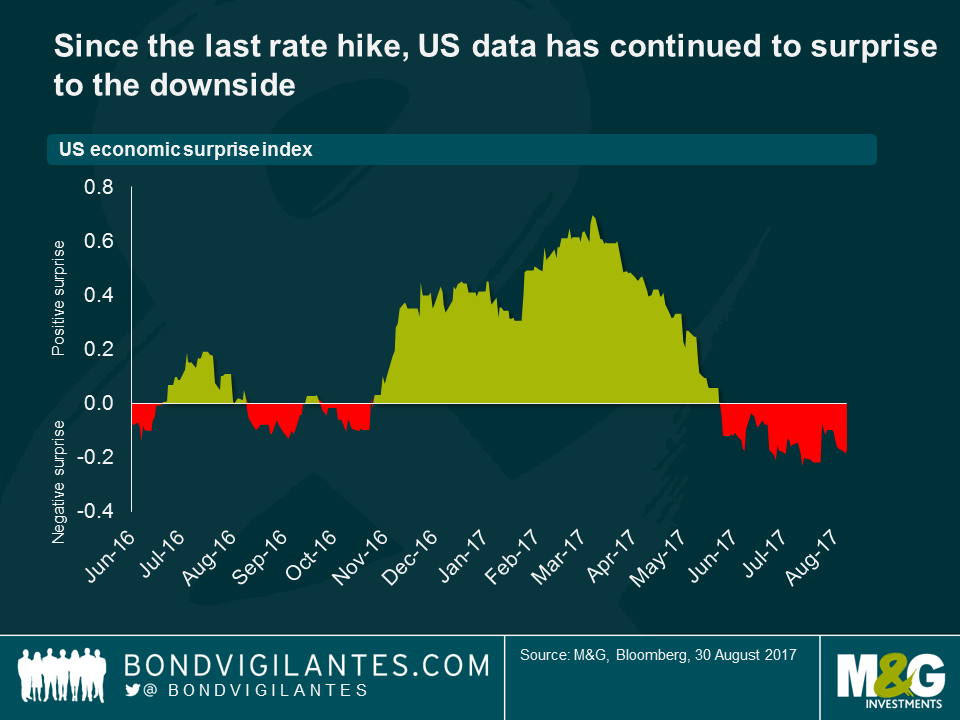

What’s surprising about the US, is that since the FOMC’s last rate hike in mid-June, the data from the underlying economy has constantly undershot analysts’ bullish forecasts. This is in contrast to the previous two hikes in December 2016 and March 2017 where data continued to surprise to the upside for months afterwards. That’s not to say that the underlying economy is slowing down (Q2 GDP was revised up from 2.6% to 3% at the end of August, driven by solid momentum in domestic demand with both the consumption and investment contributions increasing. Retail sales also surprised to the upside etc.), but rather that analysts have been supremely optimistic on the data front.

What’s clear from these charts is that most recently, economists have been too bearish on the UK and Euro area, but too bullish on the US. This does not bode particularly well for those advocating an aggressive rate hiking path from the FOMC. Indeed, the underwhelming data in the US has been reflected in market expectations for Fed rate hikes, with 60 basis points of rate hikes priced out from the Fed Funds curve (over the next 3 years). The pessimistic view on the Euro area, however, arguably makes it a tad easier for the ECB to follow its slow and gentle plan towards policy normalisation, as forecasters are similarly reticent about being too bullish too soon. In the UK, this has made me ponder the Bank of England’s policy rate. The “emergency rate cut” of August 2016 to 0.25% could be reversed should this trend continue (there already are a couple of hawks in the MPC), though this is certainly not what most economists are expecting.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.