Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Investment markets have been remarkably resilient over the course of 2017. Sure, the geopolitical environment has thrown up a few frightening days which saw markets sell-off but on the whole volatility has been muted and most asset classes have generated solid total returns. That said, any horror movie fan will tell you that the scariest part of a horror film happens when things are relatively calm. With that in mind, here are a few charts that shine a light on a number of threats that are lurking just below the surface of the global economy.

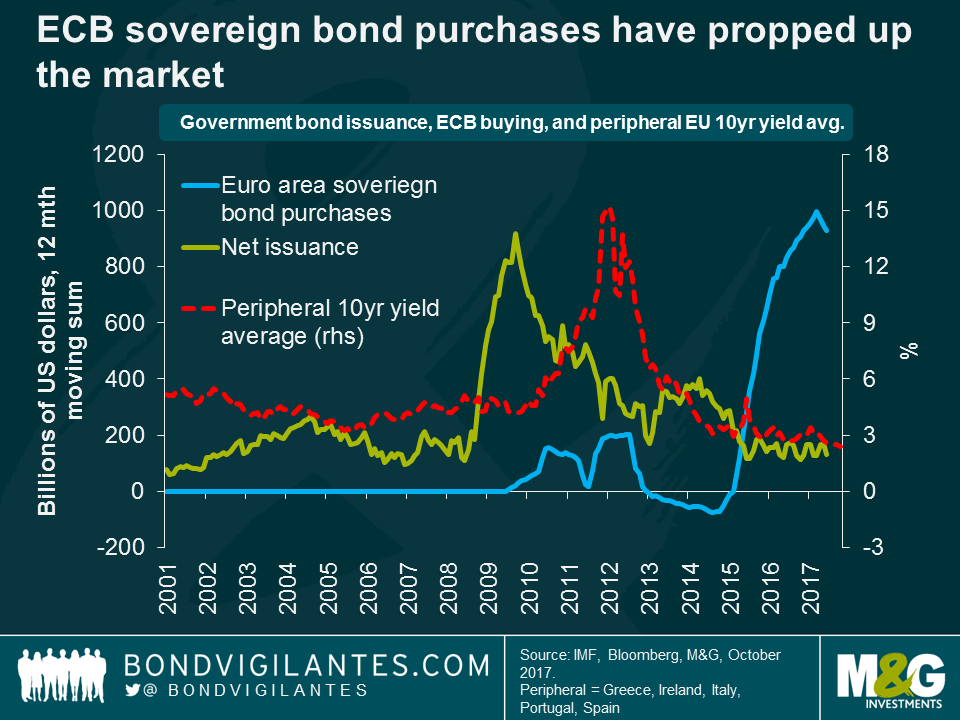

The strength of the European economy, and signs of labour market healing across the euro area, has been the surprise story of 2017. It is undeniable that the ECB, and its quantitative easing programme, has played a huge part in the economic success seen to date. Many point to the fall in yields on peripheral area debt as a sign that the euro sovereign debt crisis is well and truly over. The question is, do falling yields signify increasing confidence in the ability of euro area nations to repay their debt, or do they simply reflect the asset purchases that the ECB has conducted since the QE programme started? The above chart, published in the most recent IMF Global Financial Stability Report, shows that official purchases of euro area debt has eclipsed net issuance since May 2015. Indeed, ECB QE is currently 7 times bigger than net issuance. So is it any wonder why yields have fallen, and what happens when the ECB tries to turn off the easy money tap?

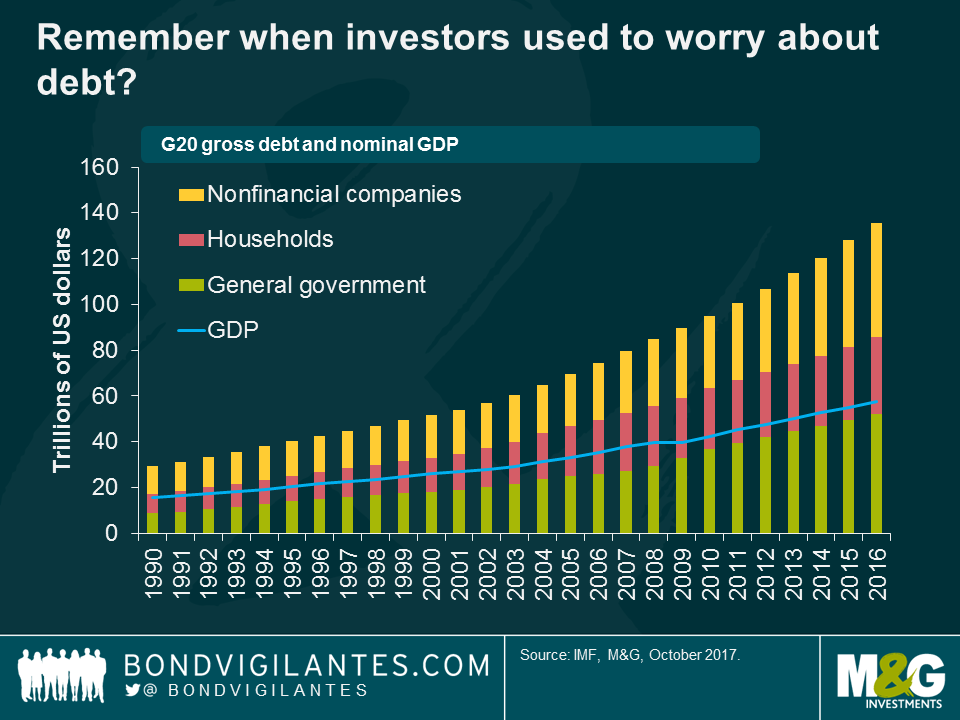

In G20 advanced economies, the debt-to-GDP ratio has grown steadily over the past decade and now stands at over 260% of GDP or 135 trillion US dollars. $135,000,000,000,000.00. It’s a big number, and whilst it is true that this debt represents an asset on another balance sheet, it is undeniable that governments, corporates, and households have never lived beyond their means by so much. It is for this reason that advanced economy interest rates are so low, and are unlikely to return back to levels observed before the 2008 financial crisis. For investors, that means you are going to have to take more risk to generate positive real returns.

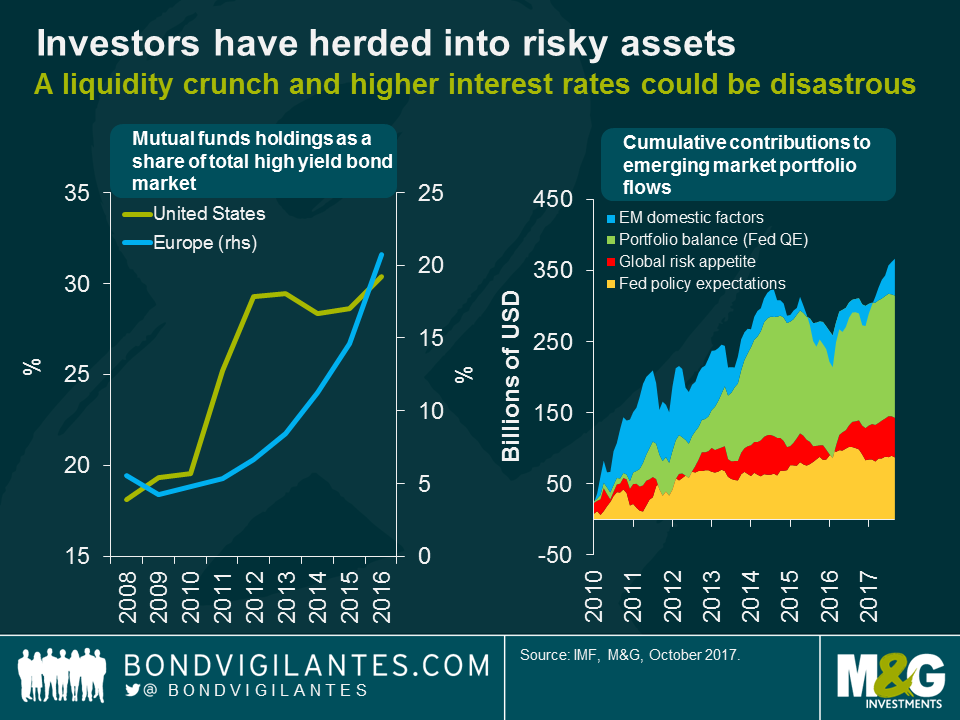

Accommodative central bank policy has encouraged investors to invest in riskier and riskier assets. Whilst this can be described as “portfolio rebalancing” and central banks think that it will help them to generate inflation, it may also pose a significant risk to the global financial system. In the US and Europe, mutual fund holdings of their respective high yield markets have grown considerably. Turning to emerging markets, large-scale monetary accommodation has underpinned a significant portion of portfolio flows to emerging market economies. IMF estimates indicate that around $260bn in portfolio inflows since 2010 can be attributed to the Fed’s QE programme.

A significant issue for the performance of investments in riskier asset classes like high yield and emerging markets would be a spike in investor risk aversion or some form of external shock (like the oil price collapse in 2014). If investors head for the exits, this could trigger sales of riskier and less liquid assets held in open-ended mutual funds, resulting in substantial price declines. The very gradual pace of monetary policy normalisation may be exacerbating these risks, as continued low volatility and low yields encourage investors to further increase credit risk exposure, duration, and financial leverage.

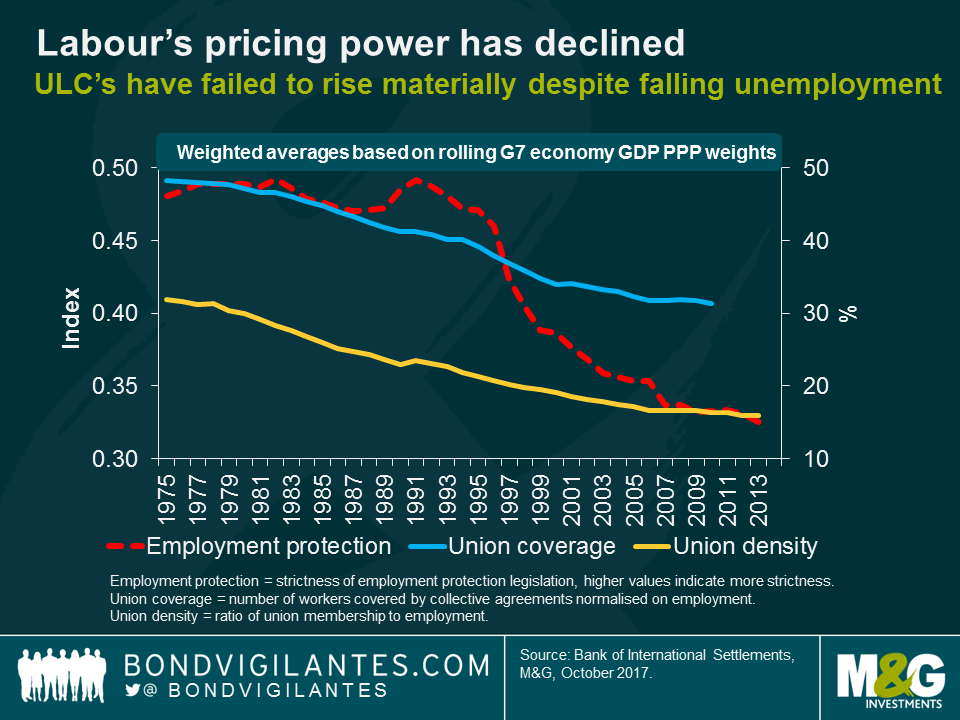

Low wage growth, despite low unemployment rates, is a sign of labour’s declining pricing power as a factor of production. This is a problem, as labour markets have traditionally been regarded as key for inflation as rising wages generally lead to higher production costs, resulting in higher inflation. For the first time, central bankers like Mario Draghi and Haruhiko Kuroda have been calling on unions to increase wage demands, with Draghi stating wages are the “primary driver of inflation”.

The more workers can strengthen their pricing power, the more likely it is that wage demands will be agreed to by businesses. Unfortunately for low and middle-income workers across the G7 economies, pricing power has fallen since the early 1990s. The decline in rates of union density and coverage, combined with a fall in employment protection, has left workers in a weaker position to press for higher wages. Unless workers can start demanding higher rates of pay, it is likely they will continue to suffer real-wage declines. This has been the case in the UK, with unit labour costs and inflation growing by 16% and 25% respectively since 2008.

From what has been reported in the UK press on a daily basis, it doesn’t look like negotiations between the UK and Europe are going well. To highlight the scale of the challenge that the UK faces, this chart shows the share of total UK trade by trade agreement. According to Bruegel, approximately 51% of UK trade today is conducted with the EU, 4% with nations that are in the EEA or have a customs union agreement, and 9% under existing EU preferential trade agreements (PTA). A further 21% of trade is conducted with nations that have a PTA under negotiation.

In March 2019, unless some form of deal is agreed, the UK will have to negotiate trade deals with the majority of its current trading partners. This would be a major challenge as complex trade agreements are not easy to negotiate and often take years to agree to. If the UK finds itself outside the European Union Single market and the EU Customs Union, tariff and non-tariff trade barriers (like quotas, embargoes, and levies) are likely to be implemented between the UK and its main European trading partners. Some sectors and companies may face much more restricted access to the European market, and that will prove to be a significant headwind to UK economic growth in the short-term.

This week on BVTV I am joined by Helen Thomas from blondemoney.co.uk. Helen thinks that the market is underestimating the scenarios around Brexit, and believes that a reversal of Brexit should be on investors’ radars. With many expecting a continuation of the current goldilocks environment (low inflation, solid growth) into 2018, and the Bank of England in-play this week, could an unforeseen development in the Brexit negotiations be a catalyst for the next UK recession?

While the market gears up for the much anticipated European Central Bank meeting on Thursday, there are two other European central banks due to meet earlier in the day; Sweden and Norway.

I was in Washington a couple of weeks ago for the World Bank and IMF conferences, which was a great opportunity to hear from policy makers and economists. It served as a timely reminder that the European central banks are likely to be more patient (i.e. dovish) than market participants expect – especially those with strong trading links to the Euro area. In the case of Sweden, it has taken 6 years for growth to pick up and maintain a convincing upward trend, inflation and expectations also. Policymakers will not be in a rush to tackle rising inflation prematurely.

There’s been much speculation about whether the ECB will tweak or begin preparations to exit its quantitative easing (QE) programme. The Swedish Riksbank has been implementing its own quantitative easing and although the economic fundamentals in Sweden have been improving, indicating for much of this year that normalisation is perhaps warranted, I do not anticipate this being tweaked ahead of the ECB announcement. This is because what’s especially pertinent for Scandinavian nations – particularly Sweden, Norway and Denmark – is that as small open economies with large shares of GDP derived from trade, it is the exchange rate which acts as the key transmission mechanism for monetary policy (Denmark with its currency peg, is obviously more explicit about this).

Given that both Sweden and Norway have strong economic links to their Eurozone trading partner, neither the Swedish Riksbank nor the Norges Bank would want to see their respective currencies appreciate (and their inflation target missed) by implementing hawkish monetary policy. This would only serve as a first-mover disadvantage. They too, will be in wait-and-see mode on Thursday with respect to the ECB, before they embark on their own policy normalisation path.

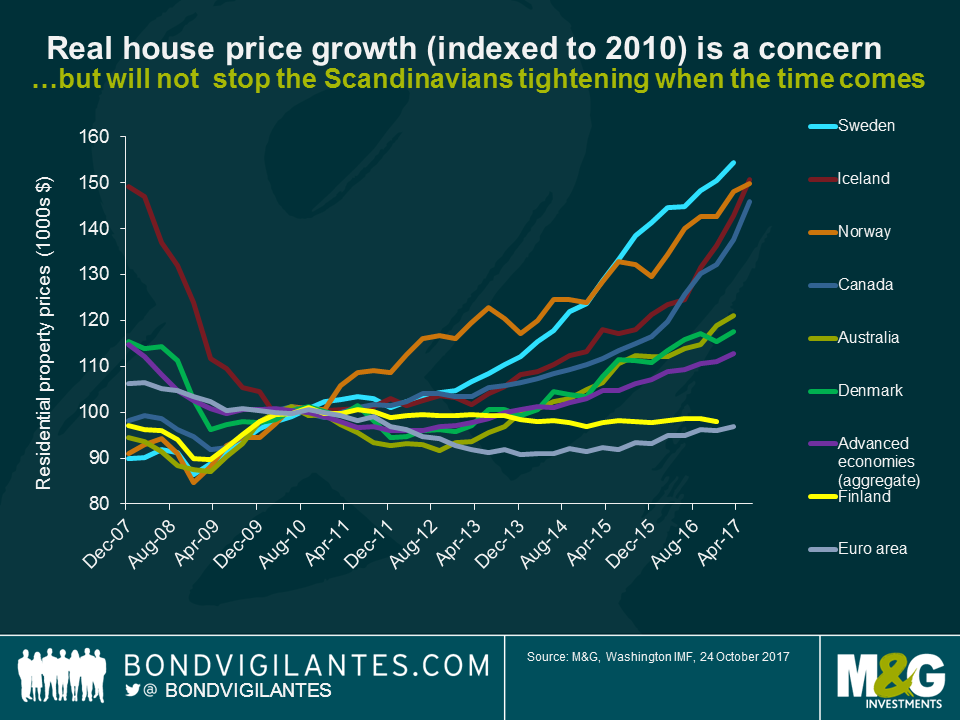

The final point worthy of note is with respect to leverage in the housing sector. The chart below shows how this is a growing problem, not just in Scandinavia, but in countries such as Canada and Australia too. It is difficult to find research which doesn’t cite this as a growing problem in these economies, often pairing this reasoning with arguments why central bankers will not be able to hike rates significantly. Scandinavia essentially needs two interest rates; one (which is much, much higher) to curb the housing market and a second one (to remain low) for corporates to ensure they remain competitive versus the continent.

Since the meetings in Washington however, I have noticed just how many central bankers worldwide have been at pains to stress that financial stability is not their key remit. Household debt is on their radar but it’s a problem for macro-prudential tools or politicians to deal with and not traditional monetary policy. The ball is being shifted to someone else’s court. If and when the Scandinavian central bankers do embark upon their rate hiking cycles, it will not be housing sector concerns that stop them from doing so. Market participants would do well to remember that central bankers may be agnostic towards housing market excesses when the tightening cycles ensue.

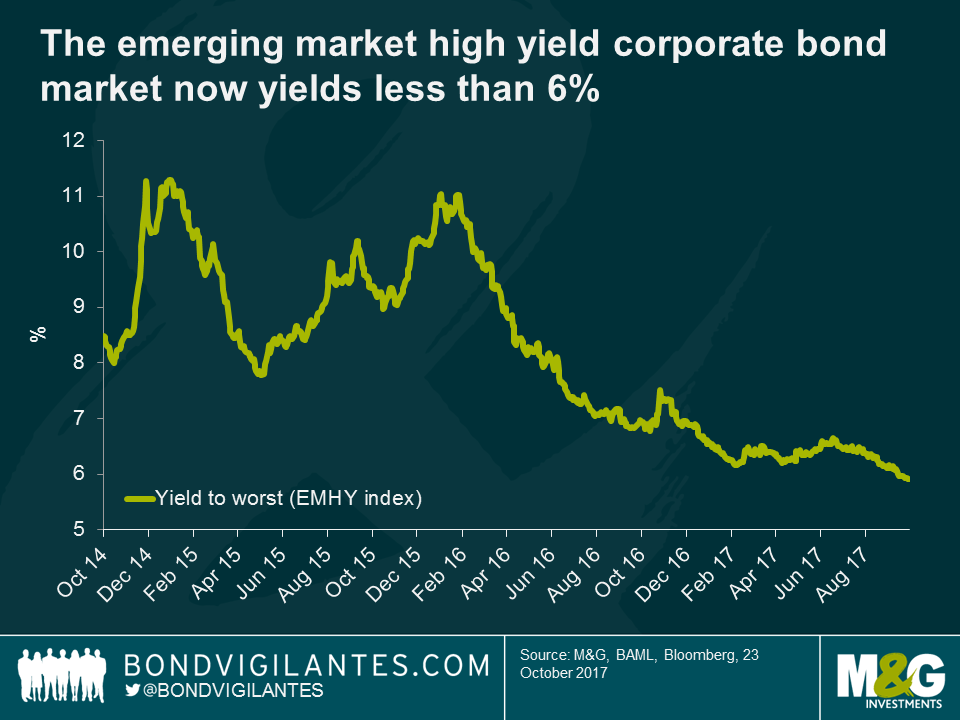

Would you buy a 7-year unsecured bond at 6% yield from a B1/B+ rated Brazilian airline (first time issuer) with well-below-standard credit covenant protection for investors? Many did last week. Few would have a year ago.

This year, many emerging market bond investors have been tempted to lend further down the credit spectrum in search for higher yields. Strong inflows into the asset class combined with the current low default rate environment has helped to encourage this trend. The primary market and in particular debut bond issuance have become key areas of focus, as this is usually where investors find mispricing opportunities and capture new issue spread premium. The flip side of the high demand for EM high yield primary deals has been an erosion of covenant protection. Corporate issuers and their financial advisers have been increasing issuers’ financial flexibility by reducing credit investors’ protection in bond documentation. Long story short, the search for yield in emerging markets has been killing EM high yield covenant standards recently.

I have come across multiple examples in the past six months. The most bizarre one was when a Pan-Asian healthcare provider issued non-rated perpetual bonds with a change of control call, not put! This gave the issuer (not the bondholder) the right, but not the obligation, to buy back their own bonds at 101 in the event that the company changes ownership. This essentially amounts to a blank cheque for an M&A transaction without having to refinance the existing capital structure. I asked my European and US HY fund manager colleagues if they had seen this before, and they too had never heard of such a feature.

Then we had a number of mid-BB bond issuers, in particular from Latin America, coming to market with some standard HY covenants such as a restriction on how much debt they can issue based on meeting a minimum level of fixed charge coverage ratio (EBITDA to interest) and similarly restriction on payments like dividends based on the same ratio. However, none of the restrictions were based on a leverage ratio (debt to EBITDA) which is usually a market standard.

Finally, we had a Brazilian airline last week which successfully issued B+/B1 rated bonds with no restrictions on how much debt they can issue, nor how much in dividends they can pay to shareholders. This means, on paper, that the financial policy might favour shareholders at the expense of the credit profile of the company with no controls from unsecured bondholders. I doubt that any of the lending banks would allow a similar situation on secured debt.

I think EM corporate bond investors have it all wrong. In periods of economic recovery – like EM is currently experiencing – corporates tend to engage more in dividend upstream or transformational projects (M&A, large expansion capex). In periods of economic troubles, financial discipline is usually implemented to preserve cash flows, credit metrics, investor confidence and ultimately access to capital markets. This happens in order to attempt to ensure that refinancing maturities remain at an acceptable yield for issuers. In other words, credit covenants are a protection against the downside and in my view are even more vital when corporate bond spreads are tight. In the current market environment, capital that is chasing higher yielding assets is agnostic to the risks of any possible downturn. This poor security selection will hamper returns in a selloff scenario, with those that have implemented careful credit differentiation in the good times more likely to weather the storm.

Today I am joined in the studio by M&G credit analyst Othman El Iraki and we will be taking a closer look at an area of the fixed income market that has been generating a lot of interest in recent months – Real Estate Investment Trusts (REITs). Othman will talk through some of the characteristics of this asset class and explain what’s been driving the recent surge in new bond issuance, especially in the UK. Also this week – we look ahead to Thursday’s eagerly awaited ECB monetary policy meeting where bond investors are hoping to get more details on the bank’s QE exit strategy. Tune in to find out more.

President Trump is likely to announce his choice for the next Fed Chair by the end of this month. Whilst current Chair Janet Yellen is still in the running, she has been slipping down the betting over the past few weeks. There are three good reasons why (from his perspective) Trump should re-appoint Yellen to the position.

Yet over the weekend “people familiar with the matter” suggested to Bloomberg that Trump “gushed” over Stanford University economist John Taylor, having interviewed him in the past week. Presumably Trump is aware that the famous Taylor Rule would likely result in the Fed hiking rates much more aggressively than the market currently expects (if you assume a neutral rate of 2% the Fed Funds rate might currently be at over 3.5%. Many believe the neutral rate is much, much lower nowadays, but even then a “rules based” Fed seems more inflexible than a businessman like Trump might desire).

Whilst he’s surging, Taylor’s not yet overtaken Powell at the bookies. But at 10-1 Janet Yellen is now a firm outsider. If I were Trump she would be my pick.

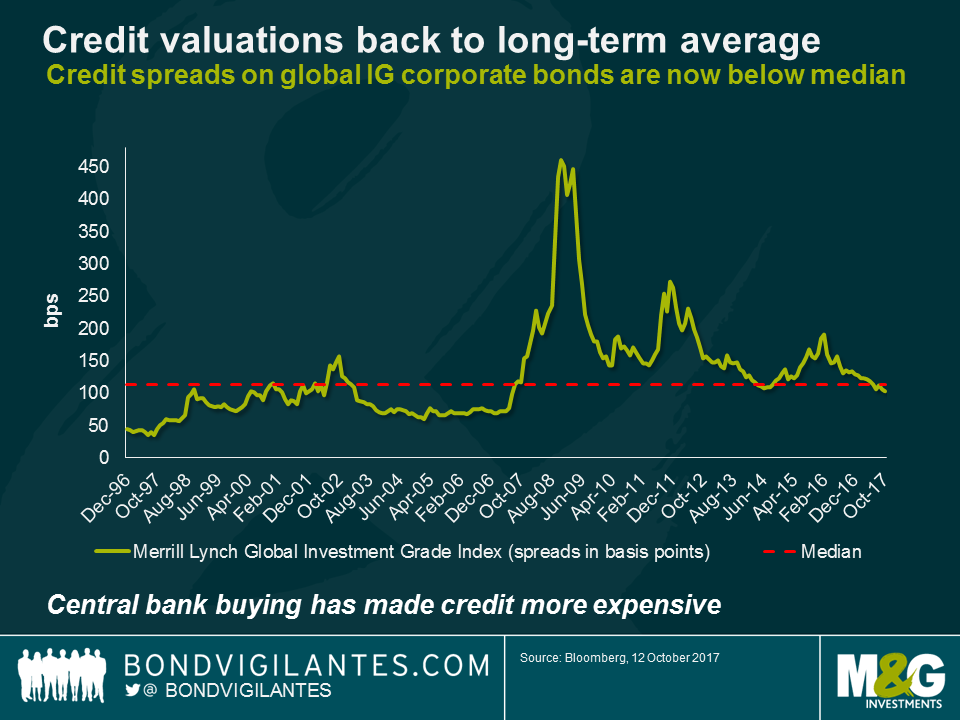

If you just looked at the overall global investment grade universe spread level, you could take comfort that despite the rally in corporate bond prices in the past couple of years (and particularly post the ECB’s decision to buy credit in its QE programme), valuations are simply back to their long term average.

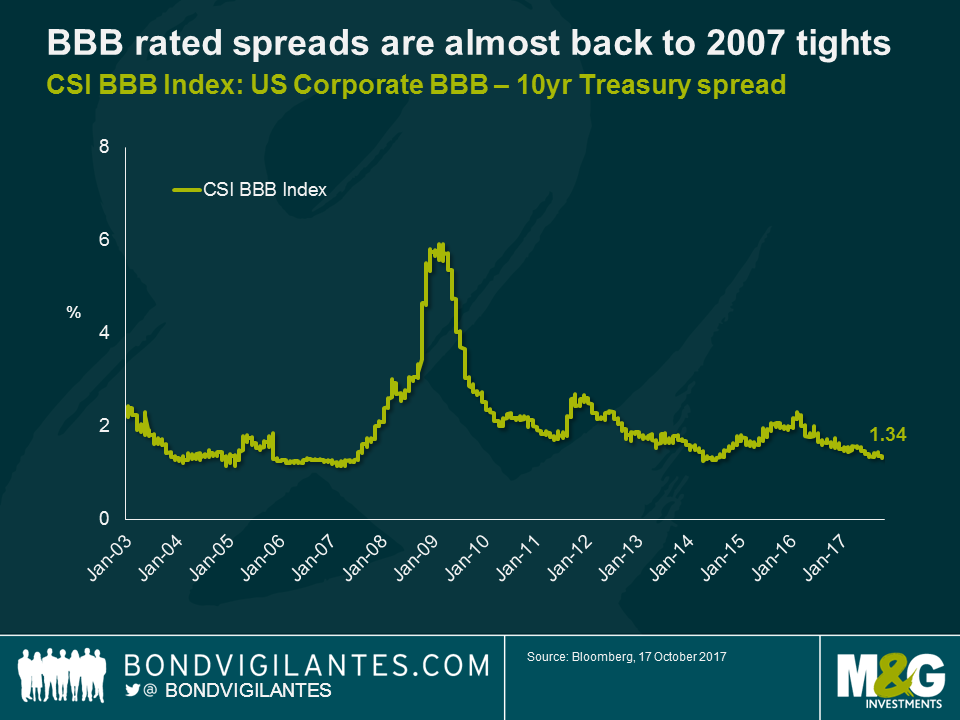

Unfortunately the global investment grade bond universe has changed dramatically since the financial crisis, to an extent that makes this long term average almost meaningless. The quality of investment grade credit has seen significant deterioration in recent years. Partly this has been voluntary, with companies believing that adding leverage to their balance sheets can enhance equity returns (as well as taking advantage of the so-called “tax shield” of interest deductibility), but it also reflects the wide-scale credit downgrades that banks and financial institutions experienced during and after the credit crisis. For example, the issuer rating of Barclays Bank in 2007 was Aa2 with Moody’s, but today it is Baa2. Looking at the market as a whole we can see that in 2000, the nascent Eurozone credit market contained under 10% in BBB rated securities, and the US credit market a little over 30%.

Today, global credit markets are almost 45% exposed to BBB rated issuers, and trending higher. Remember also that credit ratings are not linear, but exponential – as you move closer to the boundary with high yield the risk of default increases significantly. Today’s global credit market has a much riskier credit profile than it did a decade ago.

If we just look at the global BBB credit index spread, it’s clear that at 134 bps we are now near the 120 bps low spread that we saw in 2007, the peak bubble year before the GFC, and well below the average 200 bps spread that BBB rated assets have paid since 2002.

So rather than being “fair” value, global credit has moved into expensive territory. There are some good reasons for this, including the aforementioned QE buying of credit by the ECB, the fact that default rates remain very low (for all credit including high yield the default rate could be 1.5% for 2017, compared with over 2% in 2016), and the ongoing, huge, demand from US investors in particular for income producing assets (look at ETF flows into US$ IG funds). But the plain fact is that this is a market where credit quality has deteriorated, and the rewards for risk taking are much lower than they were.

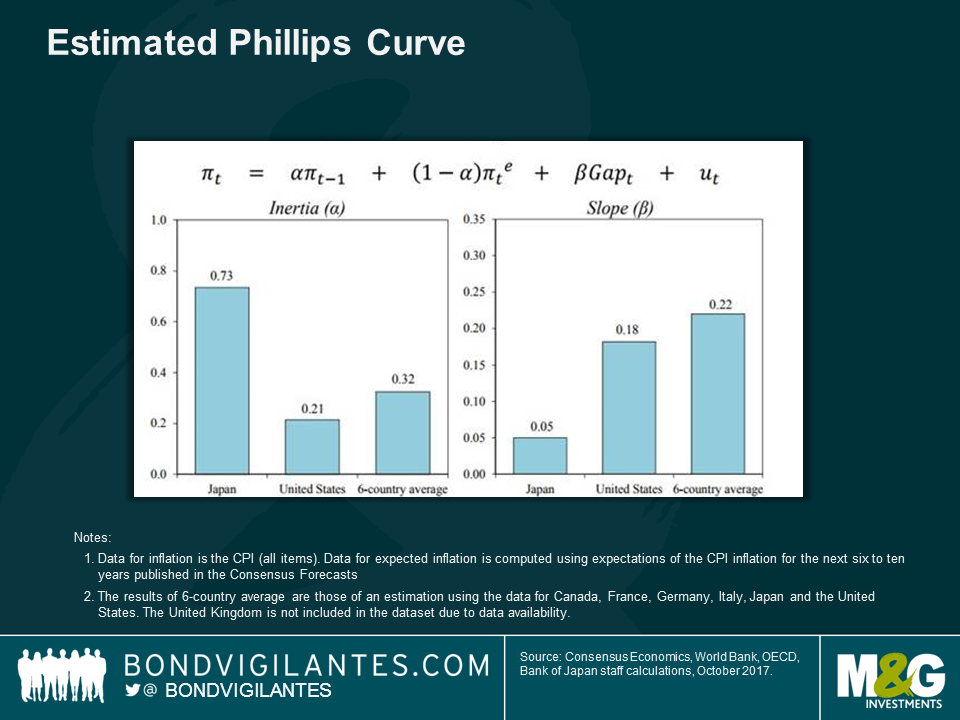

The Deputy Governor of the Bank of Japan, Hiroshi Nakaso, was in London a couple of weeks ago, with an upbeat assessment of the potential growth of the Japanese economy. You can see his slides here. Of Abe’s “3 Arrows” (fiscal policy, monetary policy and structural reform), the speech sensibly seemed to suggest that only the latter would really have any impact on Japan’s growth prospects. In particular Nakaso was bullish on the prospect for labour force growth from the elderly and non-Japanese workers (Japan’s female participation rate is now above that in the UK and US). But on the monetary policy side I thought the below slide was interesting. It shows a Bank of Japan decomposition of Japan’s Philips Curve compared to other nations. Firstly we should note that Japan’s Philips Curve is MUCH flatter than those in the US and elsewhere (right hand chart). Its unemployment rate has fallen to 2.9% from 5.5% with virtually no wage growth. But secondly we should be worried about the left hand chart. The “inertia” shows that low inflation in Japan is largely driven by the fact that inflation was low in past periods. In other words the expectations element of the Philips Curve is much more important in Japan than in the US or elsewhere, and shows how important it is that a) Japan breaks the psychological mind-set of stagnant prices (through wages policies? By hiking rates to show the economy has healed?) and b) that western central banks don’t allow deflationary mind-sets to develop here too.

I really enjoyed this article by Tom Standage in the Economist’s spin-off magazine, 1843. The Blanc brothers, bankers in Bordeaux, bribed operators of a system of mechanical telegraph towers to introduce deliberate errors into messages sent over the network which indicated the previous day’s bond market movements. This allowed them to trade bonds before the news arrived through other means, perhaps days later. The scam worked for a couple of years before the brothers were caught. They were prosecuted, but not convicted as “there was no law against misuse of data networks”. Worth a read.

Whilst we are on the subject of technology, everybody’s favourite car manufacturer (stock up around 66% this year so far) made the news during Hurricane Irma with “an unexpected lesson in modern consumer electronics along the way” (Guardian article here). Cheaper models of Tesla cars were remotely given an extra 30 miles of charge through a software upgrade, to help their drivers get safely away from Irma’s path. These cars have exactly the same battery as the more expensive models, but software limits them to 80% of the range.

“Damaged Goods” is a 1996 MIT paper which showed how tech companies may “intentionally damage a portion of their goods to price discriminate”. In some cases companies may add additional technology to, say, a printer in order to slow it down relative to its more expensive offerings, meaning that the cheap version costs more to produce than the expensive one. Tesla’s gesture was obviously a good thing to have done, but it did bring the concept of “Damaged Goods” back into the public gaze.

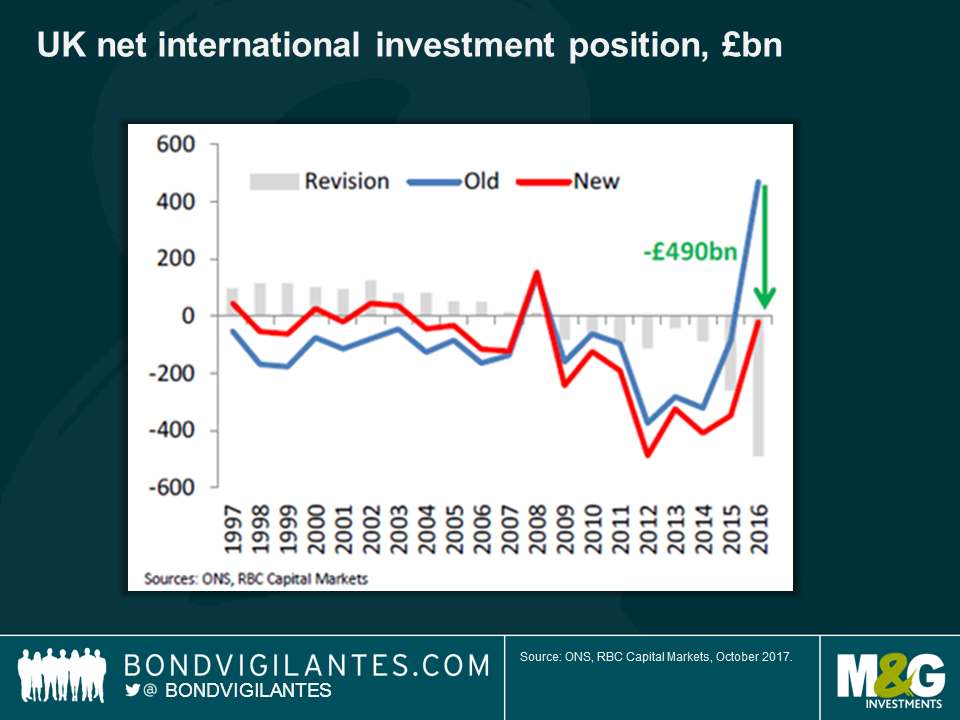

The Daily Telegraph published this article yesterday suggesting that the UK is nearly half a trillion pounds “poorer than previously thought”. Thanks to ONS revisions to the data, a substantial positive position in the UK’s net assets owned overseas has turned into a deficit of £21 billion. In other words the total value of UK investments abroad is worth less than overseas investments in the UK. The chart below, from RBC, shows the extent of this revision, but also that UK investments abroad have jumped in the past year or so. This jump is due to the post-Brexit collapse in the pound making the UK’s overseas assets appear more valuable in sterling terms. As Peter Schaffrik of RBC says “the revision for 2016 doesn’t create a new problem, it serves as a reminder to refocus on an existing one”. As we have a deficit on our international investment position it becomes difficult to generate enough net foreign income to reduce the size of the UK’s large current account deficit. Another sterling depreciation needed?

Art Laffer, the economist who is credited with the idea that cutting taxes would result in higher tax revenues and hence lower government borrowing as stronger economic growth increases the size of the cake is back in the news. Whilst the theory hasn’t necessarily stood the test of time (under Reaganomics debt to GDP increased dramatically as the President cut taxes), the current US President was tweeting approvingly about Laffer yesterday, and Trump wants to see aggressive tax cuts in the US as soon as possible.

Laffer is in the news for another reason, as our colleague Anjulie Rusius discovered in Washington D.C. this weekend at the IMF/World Bank meetings. Bored of Washington, as it’s possible to be after more than an hour or two in the place, she headed to the Smithsonian Museum as she has always wanted to see the famous napkin on which Laffer scribbled his “curve” over dinner back in the day. Literally as she was googling it on her way to the museum, the New York Times ran a story claiming that the Smithsonian’s napkin is a copy, recreated years later. She went anyway (what else is there to do in D.C. once you’ve been to the air and space museum?).

After a couple of months in which central bank policy moves rather than politics have dominated, investors’ attention has recently been pulled back to the political arena. Fund manager Wolfgang Bauer joined me this morning to discuss what Austria’s presidential election result, and Catalonia’s unfolding bid for independence from Spain, mean for government bond and credit markets.

Also –would a decisive Abe victory in Japanese general elections next weekend prolong the country’s monetary policy status quo? Tune in to find out.

Growing awareness of a range of environmental, social and governance (ESG) issues has seen an ever larger number of investors move their focus away from purely financial goals towards an approach that also considers the ESG impact of their investments. Consequently, a pressing question that faces the asset management industry is how to integrate ESG factors into different asset classes and strategies. In this edition of the M&G Panoramic Outlook, fund manager James Tomlins provides an insight into the different ESG approaches from a high yield perspective. We will find out whether the European or the US high yield universe is more affected by ESG rules and what kind of ESG high yield approach is preferred by James to strike the right balance between ESG constraints and the ability to implement investment-driven views.

| View the Panoramic Outlook |

President Trump is expected to announce his pick for next Fed chair imminently, as Janet Yellen’s term expires in February 2018. Trump being Trump, the outcome is particularly hard to predict. Jim Leaviss joined me on BVTV today to talk through the leading candidates and what they would mean for financial markets if selected.

It’s party conference season in the UK, with the Conservative party conference now underway. All eyes will be on Theresa May and her senior cabinet ministers, as investors try to gauge the latest Brexit developments. Anjulie Rusius, our UK-focussed junior fund manager, has joined me this morning to discuss recent signals coming out from the Bank of England and the government, and what these mean for gilt market investors. Should we be preparing for a hiking cycle? Watch this week’s episode for our latest thinking.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.