Rolldown

A dispatch from the number crunchers – Yield curve rolldown

By Matthew Russell

15 April 2026

Former Bank of England Deputy Governor Paul Tucker has written a book about accountability and central banking. Have central banks become “overmighty citizens”, with too much power and insufficient democratic input? If so, does it matter and what can we do about it? In an era of QE, and bailouts of commercial banks, wealth inequality has widened in most developed economies. Did society agree that this outcome was what it wanted when central bankers “saved the world” in the Great Financial Crisis? I think this is an incredibly important book.

In this short video I ask Paul about these important dilemmas and what democracies should do about this “unelected power”. We’re also running a competition to win one of five copies of the book. You’ll find the question and how to enter below.

[This competition has ended]

After a significant policy error at the end of last year, Argentina has once again found itself in trouble – and back in the headlines – in recent months, suffering from dented credibility and a fast depreciating peso. This morning on BVTV, I look at whether current levels now offer a buying opportunity.

Also this morning: what’s behind EM FX market weakness, and is it actually a US dollar story, rather than one of EM woes? And, with the oil price still climbing, are Russian credit spread levels too pessimistic?

Tune in for our latest thoughts!

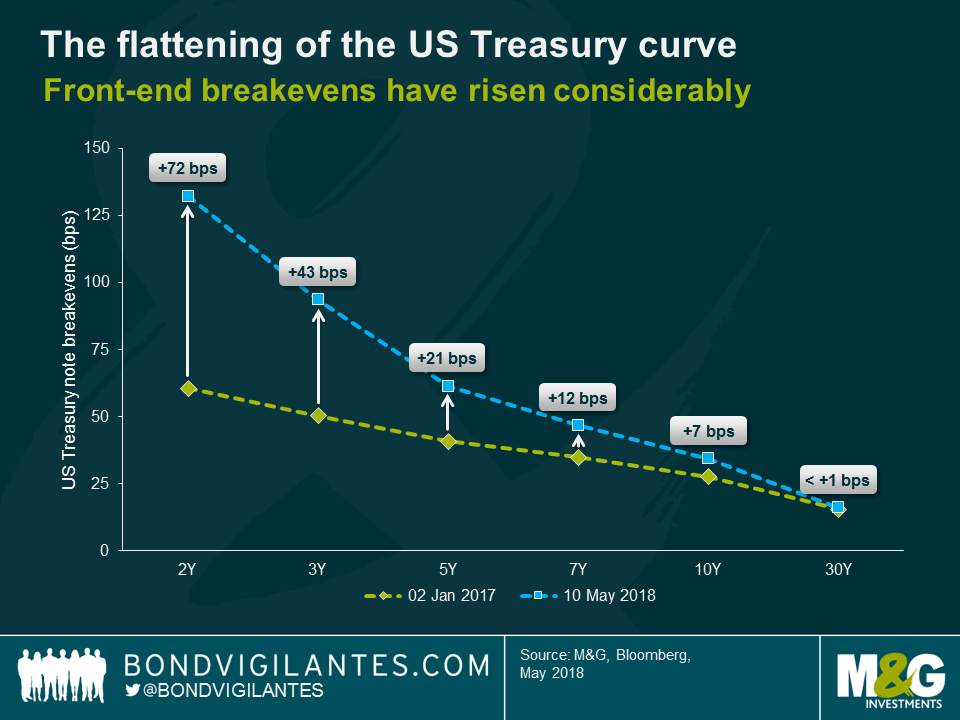

With the notable exception of the upcoming royal wedding, it would be pretty difficult to find a topic that is currently more over-analysed than the flattening of the US Treasury yield curve. On this blog as well we have pondered potential implications for credit valuations and possible counter-measures the Fed might employ. Still, one aspect that has arguably not received enough attention in the ongoing debate is the way the curve flattening impacts risk-reward profiles for US Treasury investors.

Should investors be buying Treasuries? The combination of virtually no default risk, superb liquidity and “safe haven” status is appealing. However, there are plenty of reasons to be bearish and shun Treasury exposure at the moment. Interest rate risk remains elevated in the US as it is entirely possible that the Fed decides to hike rates more forcefully than currently anticipated, should for example the diminishing slack in the US economy – in combination with a potential consumption boost due to tax reform – translate into inflationary pressures. Furthermore, Treasury supply dynamics have taken a turn for the worse due to the expanding US budget deficit and the unwinding of the Fed’s balance sheet.

Even if investors expect further pressure on valuations, from a total return perspective we cannot ignore the running yield of Treasury securities. One way of looking at the issue is a simple breakeven analysis, in which we approximate by how many basis points (bps) Treasury yields would need to rise within one year before the decline in the cash price of the bond exactly offsets the annual yield, leading to an annual total return of zero. Essentially, the breakeven quantifies the buffer capacity of a bond towards further yield rises. It is a function of the bond’s yield-to-maturity and its interest rate duration: Higher yields and lower duration numbers lead to higher breakevens and vice versa. For example, with a duration of 8.6 years and a yield of 2.96%, the breakeven for the on-the-run 10-year Treasury note (T 2.875 05/15/28) is c. 2.96% / 8.6 = 34 bps.

Breakevens are not static, of course, and the strong underperformance of short-dated vs long-dated US Treasury notes – i.e., the flattening of the curve – has had a tremendous impact. Surging yields at the front-end have pushed breakevens for 2Y and 3Y Treasuries up by 72 bps and 43 bps, respectively, since the beginning of 2017. In contrast, the 30Y Treasury yield has stayed more or less flat over the same period, and consequently the 30Y breakeven has hardly moved at all.

This has profound implications for investors. With a breakeven of only 16 bps, 30Y Treasury notes don’t seem to offer a particularly appealing risk-reward profile as they remain vulnerable to further yield rises. Considering the potential impact of the continuing oil price rally and the increasingly tight labour market on the US inflation outlook, a >16 bps sell-off at the long-end of the Treasury curve doesn’t strike me as implausible, to say the least. I would argue, the bear flattening of the yield curve has created a much more attractive risk-reward opportunity at the front-end. The current breakeven of 132 bps for 2Y Treasury notes, which is more than eight times higher than for 30Y Treasuries, provides a comfortable cushion to absorb even harsh yield rises, going forward.

There are a few caveats, though. The obvious risk of favouring the front-end over the long-end is of course that the US Treasury curve continues to flatten or even fully inverts. History tells us that this would be a likely scenario if the US economy was approaching a recession, which however I do not consider an immediate concern. Furthermore, the breakeven analysis does not take opportunity costs into account. The high breakeven of 2Y Treasury notes may well help investors avoid negative total returns even if yields continue to rise, but it is entirely possible that other asset classes still offer superior return opportunities. Finally, the risk-reward analysis gets more complicated for non-US Dollar investors. The costs of hedging the currency risk of US dollar positions can be material, which may reduce the relative attractiveness of US Treasury notes, particularly for Euro-investors.

Having lagged the broader market somewhat last year, US banks are expected to see revenue gains in 2018 as interest rates continue their rise. By contrast, the picture in Europe is less rosy, and earnings catalysts remain hard to find.

Stephanie Betts, an investment specialist in M&G’s equities team, joined me this morning to discuss prospects for bond and equity investors. Tune in to hear us discuss the diverging outlooks.

If you looked at the post-referendum changes in sterling versus the dollar, or the movement in gilts, you’d be forgiven for thinking that Brexit was done and dusted. The 10 year gilt yield has bounced back to around pre-referendum levels hovering around the 1.4% mark (in August 2016, 10 year gilts rallied to historical lows of 0.5%), while the front end of the yield curve has moved higher. Similarly, from a currency perspective, GBP real effective exchange rates have bounced considerably from their post-referendum lows.

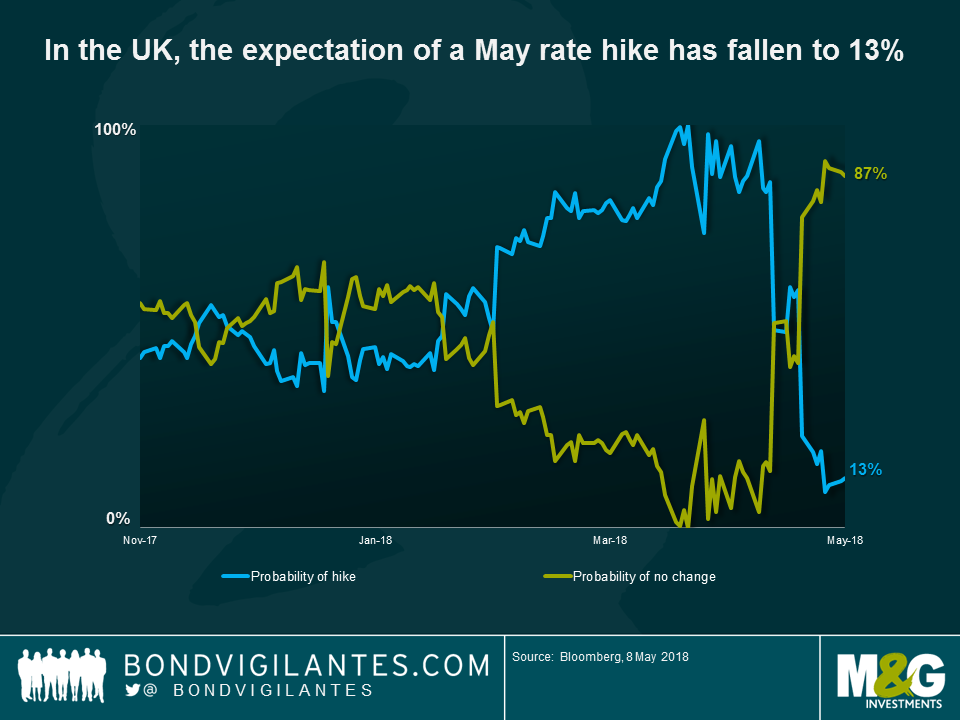

On the surface, this perhaps suggests that Brexit concerns have abated. Indeed, up until last month, the market was pricing over a 90% probability of a rate hike at tomorrow’s meeting (which would be the first time rates have been above 0.5% since March 2009). Scratch a little deeper however and there are still signs that there’s a raincloud hanging over the UK, which is why the Bank of England (BoE) may pause tomorrow, explaining why the market’s rate hike expectations have fallen off a cliff.

Initially economists and the market priced in a doom and gloom Brexit scenario, but after the currency depreciation and big gilt curve moves, the economic data held up into the end of 2016. As the political discussions have dragged on with definite details sparse, ‘Brexit boredom’ has perhaps been the result. Through 2017, front end gilts traded sideways in a 40 basis points range, with this range limited to just 15 basis points from September (the market priced in a reversal of the BoE’s post-referendum ‘emergency’ rate cut, which was indeed reversed in November) through to the year end.

For the best part of this year, with rate hike expectations growing, it has paid to be short duration in the front end. But the trajectory has recently changed. Just as the market had decided to underweight the politics and the gilt curve had become sensitive to central bank rhetoric once again, more of the economic hard data has started to turn. The near-certainty of a May rate hike was first called into question, when during an April interview with the BBC, Mark Carney explicitly stated that he was “conscious that there are other meetings over the course of this year.” Since this warning, the economic data has followed suit. CPI at 2.5%, retail sales of -1.2% and Q1 GDP at 0.1% have all been below expectations. Last week, in the final run up to this week’s meeting, all of the UK’s PMIs (manufacturing, services and composite) fell below expectations.

If the May hike is off the table, then when do the BoE move next? Central banks remain data dependent, but are increasingly intent on hand-holding, providing signals and guidance to the market. What this has meant in recent practice is that both the FOMC and BoE have tended to move rates at meetings which are followed by press conferences, where they can verbally articulate their changes. This is why the market is pricing in a low probability of a move by the BoE in June, but a greater chance of a hike at the quarterly meeting in August. To my mind, even August may prove too soon, if the consumer squeeze and hesitant investment environment continues.

Brexit uncertainly is still an issue. It’s very much on the political radar and is on the economic map now too; the market had just been temporarily lulled into a false sense of security. Without supportive economic data or political clarity, any move upwards in rates could easily prove to be a ‘bad’ hike.

Argentinian assets have been under material pressure in recent days. I thought it would be useful to write my thoughts on the recent moves and implications for markets going forward.

Over the past two months, the Argentinian peso had become overvalued in real terms following large inflows from foreign investors in 2017. These capital flows caused the nominal exchange rate to depreciate by much less than inflation. Those investing in Argentinian assets cited the carry trade theme, relatively low volatility, and the entering of Argentinian local currency sovereign bonds into the JP Morgan Government Bond Indices as investment rationales. However, the tide started to turn late last year when the Central Bank of Argentina (BCRA) made a policy mistake by raising the 2018 inflation target from 10 to 15%. The adjustment of the inflation target subsequently allowed the BCRA to cut interest rates in early January this year.

The cut in interest rates dented the BCRA’s credibility, and concerns grew about whether monetary policy was free of interference from the government. Another policy mistake was the announcement of a 5% tax on Argentinian peso Treasury bill investments, which impacted both locals and foreigners and led to a reduction in holdings of Argentinian peso Treasury bills by investors. Higher than expected inflation readings, and a strengthening of the US dollar finally generated large pressures on the Argentinian peso. After attempting to support the local currency by buying over USD 5 billion worth of pesos in the currency market, the BCRA finally realised that its monetary stance had to be tightened. We have now witnessed three emergency hikes (a combined 12%), bringing the policy rate to an eye-watering 40%. I believe the monetary authorities will now be successful in slowing the depreciation of the currency going forward.

The overvalued peso also contributed to Argentina’s current account deficit widening 5%. I expect the current account deficit to begin to start narrowing again as the currency moves into equilibrium (say, to 24-26 against the US dollar by year-end) and the economy slows as a result of the monetary and fiscal tightening (a 0.5% tightening of the fiscal deficit was also announced). The implications of this will be higher inflation this year and possibly next, lower growth and a further decline in Macri’s popularity.

If this a default situation? Not yet. I see this as a re-pricing of Argentinean risk which had started earlier in the year, coupled with an already ongoing emerging market sell-off in the local and hard currency space.

On the positive side, I believe that there are two silver linings for the time being.

Firstly, the next election is not until late 2019, so there is some time for the authorities to take its bitter medicine this year – including more utility tariff hikes, a depreciation of the peso, and attempt to control the next public wage negotiations in September. Accepting these tough measures will allow the economy to readjust over the course of 2018. The opposition and Peronists are still divided, so while Macri’s re-election chances and policy continuity look much more complicated now, it is still not a given that Argentineans will choose another populist government.

Secondly, the IMF may be prompted to get involved. Unlike other countries which would ideologically be opposed to an IMF program (Venezuela for sure, potentially Turkey, while Ecuador is uncertain as always), the authorities may end up under a program if they lose access to the markets and/or Argentina experiences a balance of payment crisis fuelled by capital flight. Argentina and the IMF have had a tumultuous relationship in the past, but under different administrations (Menem, Nestor and Cristina). The goal in this case, for both sides, would be to ensure stability so that Argentina does not return to its failed populist policies under a new administration. The current government is full of technocrats that understand this and, if push comes to shove, would convince Macri that this is his least worst option. Such an event would provide sufficient funding sources until at least the end of next year.

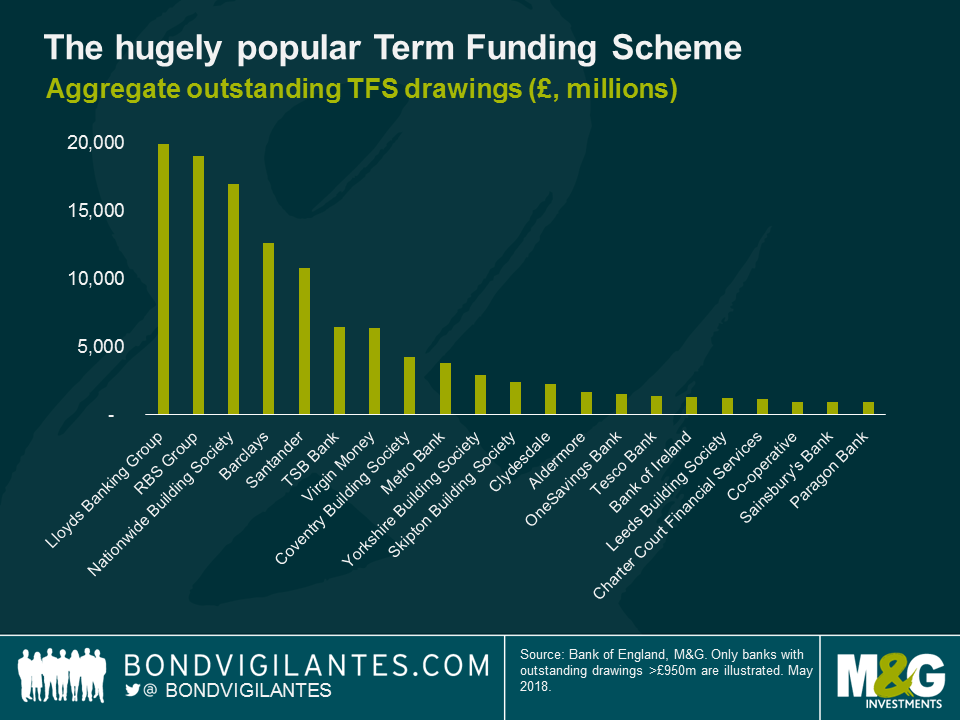

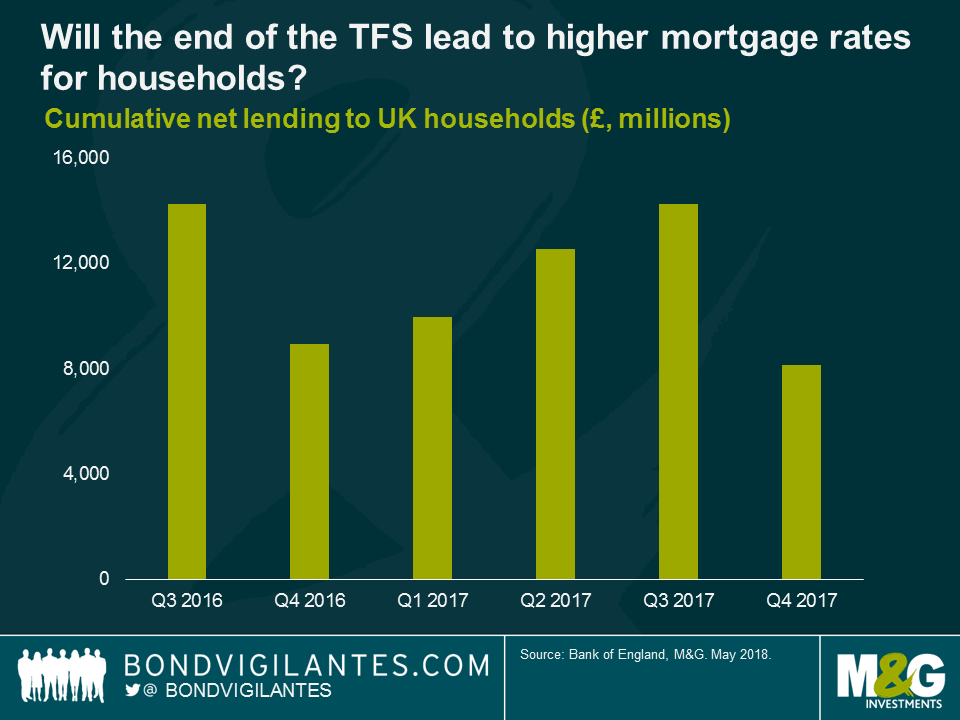

The Bank of England’s (BoE) Term Funding Scheme (TFS) came to an end earlier this year. As a brief recap, the scheme offered four year funding at the BoE Base Rate plus a fee to the banks and in turn, the banks were required to lend into the real economy (the fee was dependent upon the net lending of the bank). We previously wrote about the scheme here and here.

The borrowing scheme has been hugely popular and as of April 2018, aggregate outstanding TFS drawings (cheap loans) made available to banks was £127bn. Net lending as a result of the TFS reached £68bn between September 2016 and December 2017. The largest users of the scheme were Lloyds, RBS, Nationwide and Barclays. Consequently, it wasn’t a surprise that because banks were funding via the TFS, ABS issuance experienced a significant decrease over the last two years, with lenders paying a relatively expensive 35-60 basis points for issuing 3-5 year RMBS senior AAA notes.

With drawdowns for the scheme closing earlier this year and ahead of upcoming TFS maturities, UK domiciled banks have been planning to diversify their funding channels and tap the securitisation markets again. The tenor of the borrowings under the scheme is four years from the drawdown date, and we expect significant re-financing walls in late 2020 and in 2021. Lenders are now trying to get ahead of these walls and have been looking to issue longer maturity RMBS paper. For example, Nationwide had not funded via RMBS markets since 2016 and issued its first RMBS in February, and after a two year hiatus Paragon Bank issued its first Buy-to-Let RMBS in April.

We have seen strong UK RMBS issuance this year to date (circa €4bn) with some forecasts of €13-18bn of further issuance for the year (in both prime and non-prime space). The issuance level is still low compared to pre-scheme days of €30bn issuance annually but we expect the continued re-emergence of lenders back to the market as this dynamic should also contain funding spreads for them.

What are the likely impacts on households and consumers in the near future? Weaning banks off TFS borrowings will likely translate into higher mortgage rates for customers (but on the flip side, higher savings rates). However, funding via covered bond markets remain an alternative wholesale funding channel for banks and building societies where funding costs remain more competitive. This may help to alleviate rising cost pressures.

From an investor standpoint, despite the spread pressures, we continue to like and invest in the asset class. UK RMBS credit performance has been stable in the last few years and there have been zero losses to date on outstanding notes.

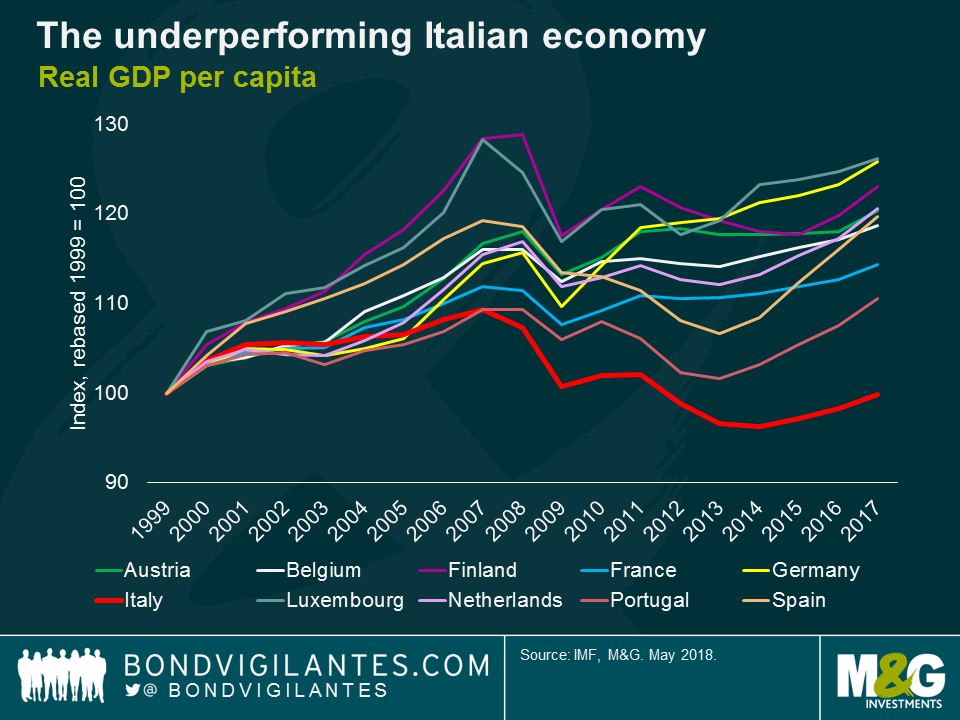

Persistent structural weaknesses, imbalances, and financial fragilities. These were some of the ways in which the International Monetary Fund (IMF) described the Italian economy in its most recent country report. Almost a decade after the great financial crisis, Italy’s economic prospects remain dim, with the costs borne disproportionately by the working age and younger population. With no government in place, a deeply divided electorate has complicated the prospects for much needed reforms and adjustments. Real disposable incomes per capita are below pre-euro accession levels, while Italy’s euro area partners are likely to pull even further ahead in terms of GDP per capita growth and incomes in the coming decade.

Italy’s economy is the third largest in the euro area, accounting for 16% of the area’s GDP. Because of its size, the EU Commission has already warned markets that Italy’s economy is potentially a major source of economic and financial risk for the euro area. The Public debt-to-GDP levels are around 133 percent, the second highest in the European Union (EU) behind Greece. Non-performing loans of banks are around 21 percent of GDP, amongst the highest in the EU. With ultra-easy monetary policy providing ample liquidity to prevent a short-term crisis, the European Central Bank (ECB) and President Mario Draghi have been able to prevent a scenario of a member nation leaving the single currency bloc.

Longer term, there remain significant issues with the Italian economy that will have to be addressed in order to withstand a tougher economic environment. Given the structural weaknesses that exist in the Italian economy (like high unit labour costs, high taxation, barriers to competition, an inefficient public sector), will Italy ask to leave the Economic and Monetary Union of the European Union (EMU)?

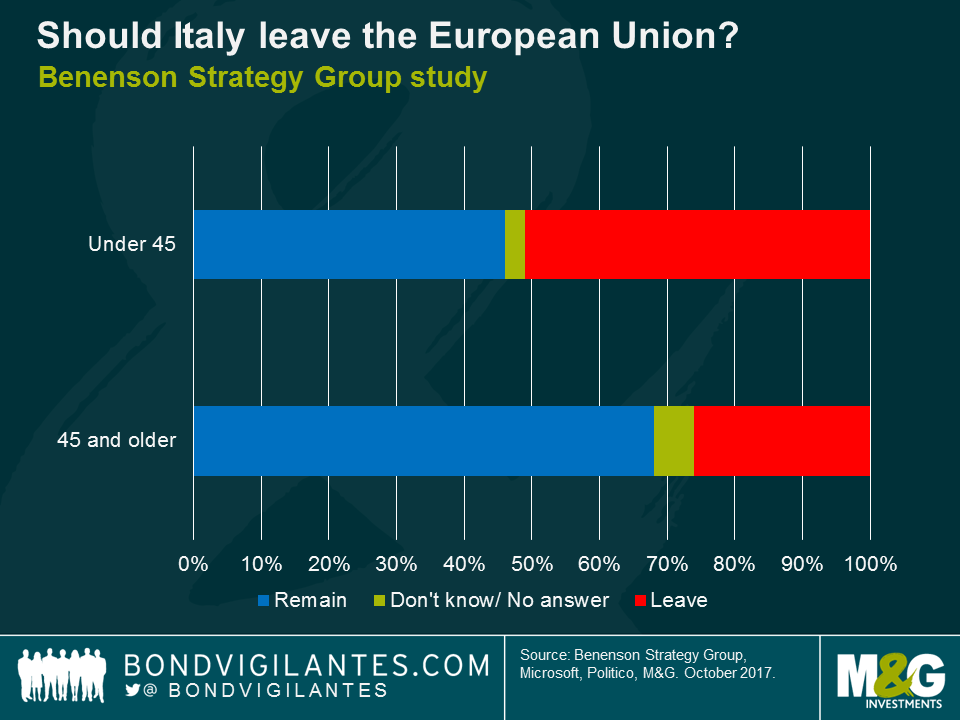

Given the political and economic backdrop, it is unsurprising that recent survey results suggested that if Italy were to hold a referendum on EU membership, 51 percent of voters under 45 would vote to leave, while 46 percent would vote to remain (voters aged over 45 supported staying in the EU by 68 percent to 26 percent). Younger Italian voters are unhappy with the EU, believing that economic convergence amongst EU member nations has come at the expense of Italy. However, with nearly half the Italian population over 45, the young of voting age are vastly outnumbered, suggesting the probability of Italy triggering Article 50 is low.

Would Italy be better off outside the EU and the EMU? Unlikely. An EMU exit by a member state would likely result in capital outflows and bank runs, leaving the banking system in ruins. A devaluation of the new currency would instantly result in high inflation and sharply cut wages. There would be a huge number of legal ramifications on a range of complex issues, not least the validity and enforceability of outstanding re-denominated contracts and obligations with creditors. It is for these reasons and many more that several Greek governments have turned away from Grexit in in favour of bailout programmes.

The outlook for the Italian economy is not particularly bright within the EMU, with soft economic growth forecast by the IMF over the medium term. Italy also faces the prospect of a decade or more of painful internal devaluation. For example, it is estimated that Italian nominal wages should be devalued by 20%, and more than 30% in manufacturing, to regain competitiveness with Germany. In the absence of a Greek-style internal devaluation, it appears that Italy will continue to muddle through, but the lack of Government is preventing the country from implementing the necessary changes for the economy to overcome its structural issues.

For bond investors, the lack of structural reform, high debt-to-GDP levels, the slow withdrawal of quantitative easing and a potential regime change at the ECB (which will be led by a new President from November 2019) suggests caution is warranted when lending to Italy at longer maturities. A 10-year spread of 119 basis points over Germany is below the 5 year average of 159 basis points, suggesting some discounting of the challenges the Italian economy faces. In addition, Italian yields are distorted by quantitative easing and the ECB is estimated to own 28 percent of Italian government bonds. Their current low spread over Bunds is also symptomatic of a market reaching for yield, encouraged by low yields in “core” European government bond markets. On a relative basis, BBB-rated Italian 10 year bonds are trading wider than their major EMU partners, including those located on the periphery that were responsible for the Eurozone debt crisis.

The current favourable macroeconomic and monetary environment will not continue indefinitely. It is important that the authorities in Italy and Europe acknowledge the IMF’s warnings in order to address the fragilities that exist within the Italian economy. If not, one may wonder if Italy could become the source of another European economic crisis.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.