Artificial intelligence (AI)

Agentic AI isn’t eating software – it’s feeding market volatility

By David Parsons

19 February 2026

Last week the European Investment Bank (EIB) issued the first public bond based on the reformed SONIA benchmark, marking another step forward in the process of benchmark reform in the U.K. The 5-year, £1bn issue was priced with a coupon of 35bp above overnight SONIA. The deal may very well serve as a benchmark for future issuance in the LIBOR-less world which the Bank of England and other regulators are aiming to create by the start of 2022. It may also help investors get comfortable with the new coupon structure and mechanics.

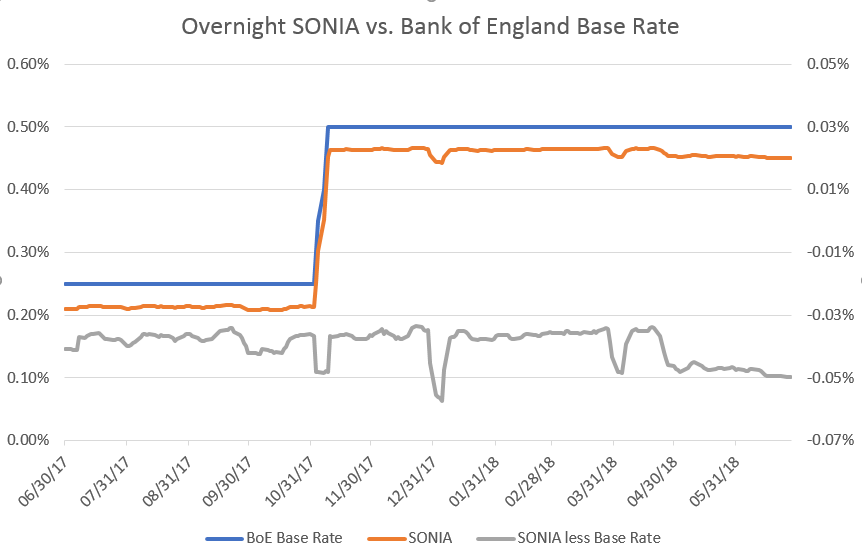

This isn’t the first SONIA-based bond EIB has issued. Their first was in 2010, but the new one is not a simple carbon copy of the first. The new bond references the reformed SONIA benchmark implemented in April, which references a broader range of transactions than the previous rate. The new issue also has a different compounding formula, which could, in our view, become standard: coupons are determined by compounding SONIA daily, then adding on the 35bp margin. The 2010 issue compounded SONIA plus the margin together. Another interesting aspect of the new note is the fallback rate to be used in the event SONIA is unavailable. The fallback rate is set at the Bank of England base rate plus the average spread of SONIA to the base rate over the previous five days for which SONIA was available, excluding the highest and lowest observations (roughly -5bp since April, as shown below). The progress made by the Bank and industry on benchmark reform should, in all likelihood, ensure that this fallback never gets used.

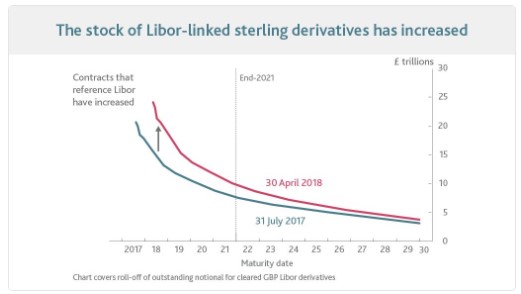

Today’s Bank of England Financial Stability Report discussed the need to transition away from LIBOR to avoid financial stability risks. Since July last year the stock of contracts referencing LIBOR and maturing after 2021 (when LIBOR may not be able to be set reliably) has actually increased. Issuance of benchmark sized public bonds based on SONIA, by a major market participant like the EIB, will therefore be welcomed by the Bank.

German government bonds have gone from strength to strength in recent times; much like the German team at the World Cup – I wish! But is the latest Bund rally sustainable? I think not.

Let’s start with the bull case. In a recent blog, I described how Bunds had provided an efficient hedge against surging political uncertainty in Italy, due to the negative correlation between yields on German and Italian government bonds. With all the political turmoil in the European periphery, Germany looks like a beacon of stability, but what about political risks within Germany? Chancellor Angela Merkel has been in office for nearly thirteen years, her authority however has increasingly been challenged of late. After falling out with her minister of the interior over Germany’s refugee policies, Merkel’s fourth cabinet (which had taken her five and a half months to forge), is facing its biggest crisis yet. An end to her chancellorship suddenly doesn’t seem far-fetched.

But even if Merkel gets ousted – and granted that’s a big if – German government bonds might actually benefit. This may sound counter-intuitive. Typically, political uncertainty around a member state of the Euro area triggers a sharp underperformance of its government bonds, as we have witnessed in the case of Italy. Are Bunds the exception though, due to their ‘safe haven’ status? Further tensions in Europe, even those originating in Germany, would most likely strengthen Bund valuations due to the ‘flight to quality’ reflex of investors. On top of that, in the event of a break-up of the Euro area, Bunds might get re-denominated in a new version of the Deutschmark, which would almost certainly appreciate against most other currencies, thus boosting total returns for Bund investors. Therefore, the higher the political risks in Europe, the higher probability of a Bund re-denomination.

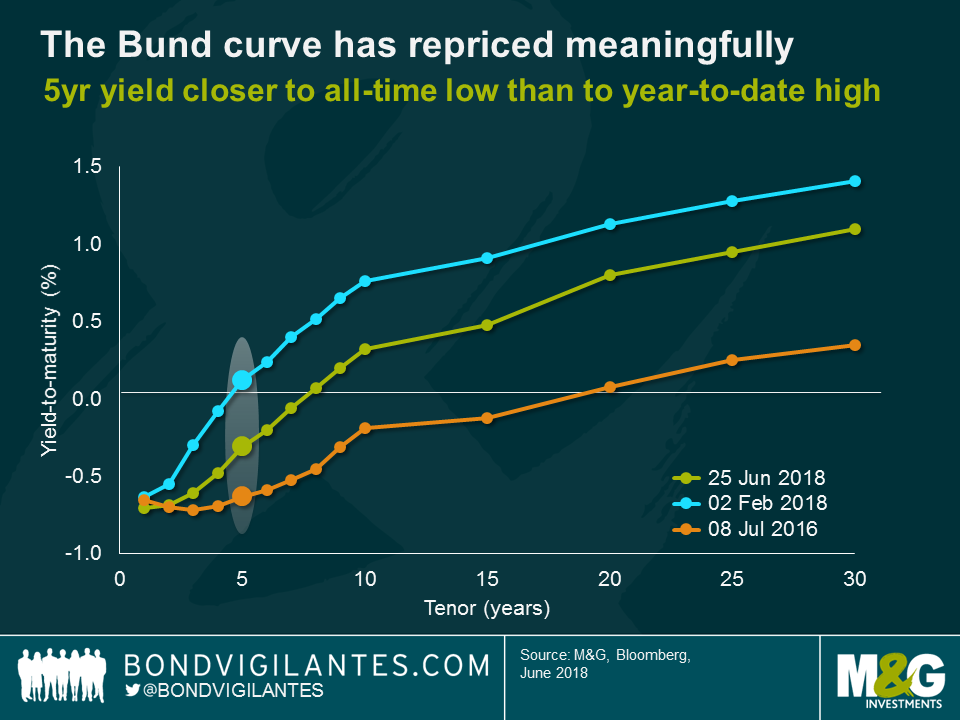

But how much further could Bund yields drop from current levels? It is worth highlighting that Bund yields have already repriced considerably in recent months, particularly at the front-end of the curve. The current five-year yield for instance (-0.3%), is in fact closer to its all-time low reached in early July 2016 (-0.6%) than to its year-to-date high in February this year (+0.1%). The belly of the Bund curve has rallied by around 45 basis points (bps) since February, while the long-end has tightened by more than 30 bps. These are very meaningful moves in the Bund market and I would argue that a fair amount of continued political uncertainty and risk aversion is fully priced in at current levels.

Of course, if ’risk off’ sentiment prevails, in theory Bund yields could drop below the 2016 lows. However, it is important to keep in mind just how extraordinary the situation was back then. In the direct aftermath of the Brexit referendum, doubts about the integrity of the Eurozone were soaring and, consequently, Bunds were benefitting from the aforementioned ‘flight to quality’ impulse and re-denomination speculations. In addition, central banks were flooding the market with liquidity. The European Central Bank (ECB) was buying €80 billion worth of securities per month and Bunds were at the top of their shopping list. Finally, after the dramatic oil price slump below $30 a barrel in early 2016, European inflation was non-existent. In fact, deflation was the concern as the harmonised index of consumer prices (HICP) dropped to -0.2% year-on-year (YoY) in April 2016. In short, all the stars were aligned. It was a unique moment in a time when conditions for Bunds could hardly have been any better.

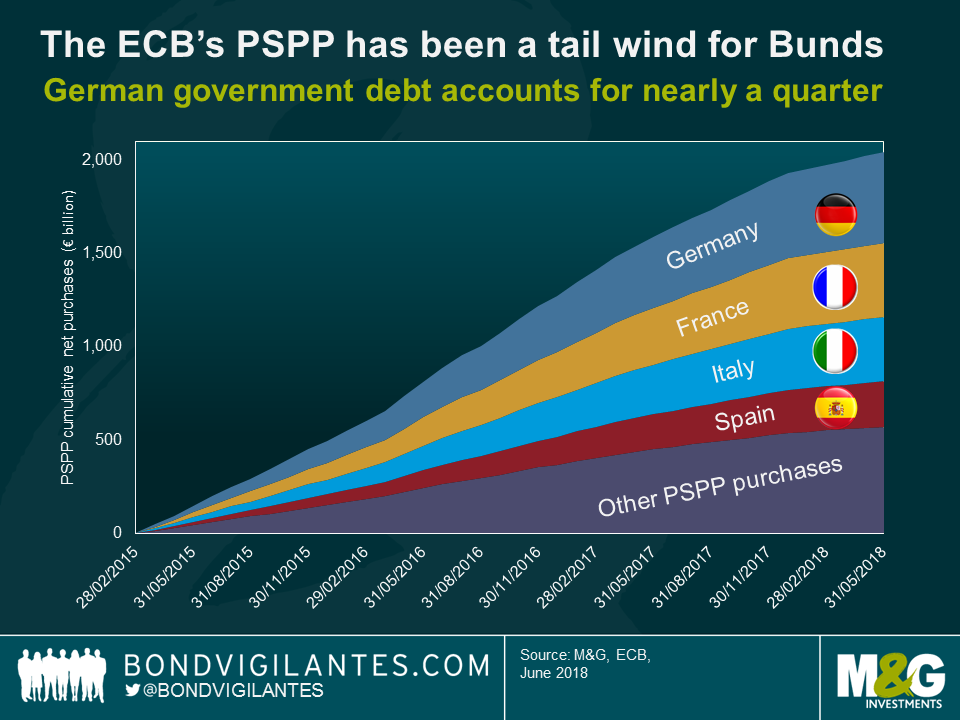

This is why I am sceptical that Bunds will reach mid-2016 levels anytime soon, if ever. European inflation has crept up with the latest HICP reading at 1.9% YoY and is thus in line with the ECB’s definition of price stability, while monetary stimulus is slowly being reduced. Net asset purchases will be phased out over the fourth quarter this year before being stopped altogether at year-end. Bunds have been the main beneficiary of the ECB’s public sector purchase programme (PSPP) (Cumulative monthly net purchases of German debt reached more than €485 billion at the end of May, nearly a quarter of all PSPP net purchases). Although principal payments from maturing securities will be reinvested for the foreseeable future, the ECB tailwind for Bund valuations is going to slow down noticeably going forward.

The market, however, seems to take great comfort from the announcement that the ECB has effectively ruled out any rate hikes at least through the summer of next year. While this measure may well pin down the very front-end of the curve, Bunds with several years to maturity are still vulnerable in my view. Once the general mood in markets becomes less jittery, I believe Bund yields are going to fight an uphill battle over the medium-term. It might thus be a good time to lock-in some profits and dial back Bund exposure.

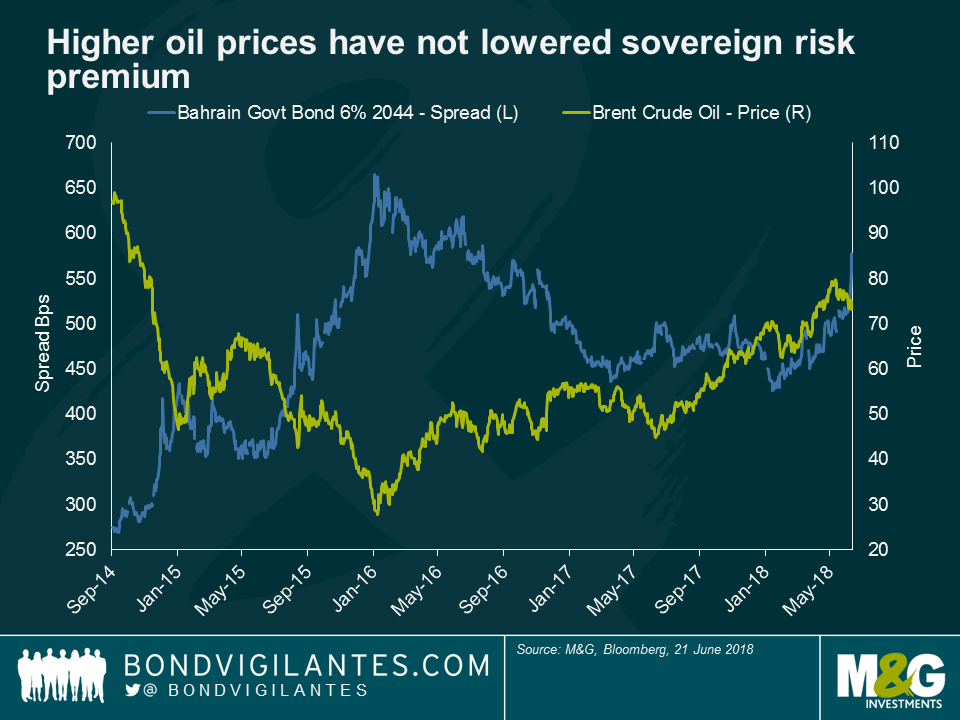

Bahrain spreads have widened in recent months, despite the rise in oil prices. The market is focusing on the $750 million Bahrain Sukuk maturing on November 22, 2018. Given that the country’s international reserves are estimated at around $2.1 billion, the country will need additional funding to repay it. The market consensus is that Bahrain will receive financial support from neighbouring Saudi Arabia and potentially other Gulf Cooperation Countries, who will seek to avoid the economic, financial contagion and pressures on their own economies and currency pegs should a default (and de-peg) ensue. The fact that the Bahrain is a relatively small economy versus its neighbours is another reason why the markets believe that it is a relatively small price to pay in exchange for diffusing the problem into the future. It is not clear, however, what kind of conditions its neighbours would demand in exchange for support. Would they require fiscal tightening, so that Bahrain’s debt dynamics can start stabilizing in a few years? But what if the market consensus is wrong, the support does not materialize and Bahrain cannot pay its sukuk?

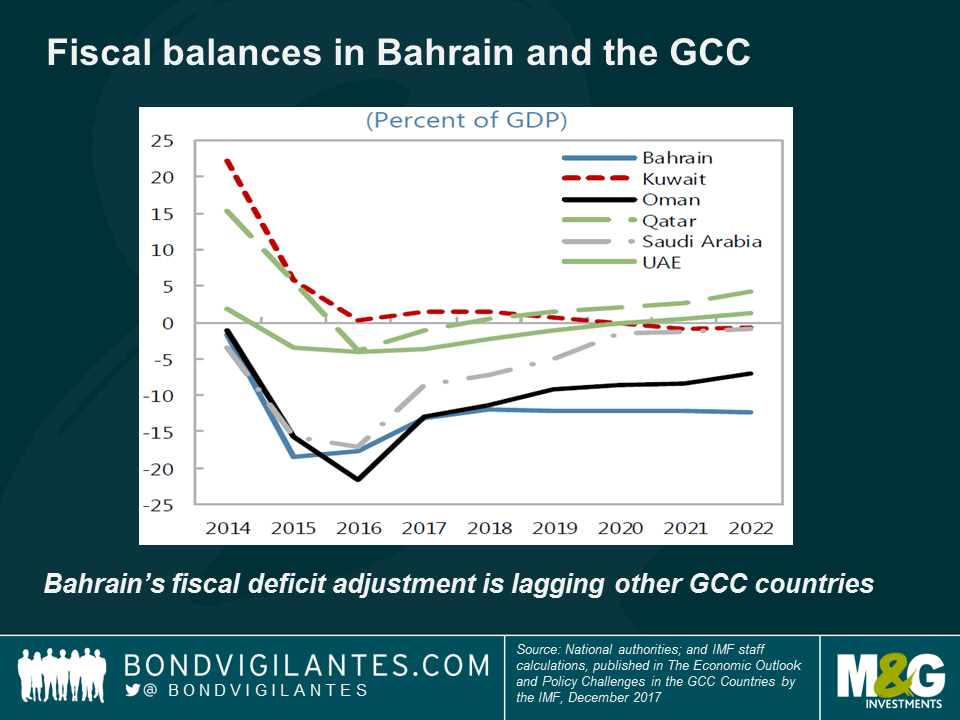

Why are markets starting to worry about a Bahrain default? Debt has doubled in just 3 years, to over 90% of GDP, as the decline in oil prices negatively impacted the fiscal position of the oil exporters in the Middle East. Unlike, most of its neighbours, however, the fiscal adjustment required (i.e. reducing some expenditures such as subsidies and benefits or broadening or increasing non-oil taxes, including VAT) has been very slow.

Given a large debt stock and a sizeable fiscal deficit (flow), it appears that Bahrain’s debt dynamics will continue to deteriorate, especially if borrowing costs, which have been relatively low thus far reflecting debt that had been issued at lower interest rates a few years ago, increase further. Increasing US rates continue to be transmitted very quickly into Bahrain’s financial sector due to its currency peg and this is not helping either. Even with Brent in the mid-70s, Bahrain’s spreads remain elevated, signalling that for risk premia to decline, either much higher levels of oil prices, an explicit statement by neighbouring countries detailing financial support or an announcement of a large fiscal adjustment by the government is required.

The fact that the security maturing in November is a sukuk adds more uncertainty due to there having been some corporate sukuk defaults in recent years (with the exception of Dana Gas ($700 million, Al Mudarabah) and Golden Belt ($650 million, Al Ijara)) which have been relatively small and limited to a handful of bonds. A Bahrain default, if it were to happen, would be the first sovereign sukuk default, comprising of 4 sukuks and 9 conventional bonds, totalling almost $15 billion. Sovereign conventional bond defaults for larger issuers with numerous bonds and a wide investor base can be complex and its resolution time consuming. The Argentina 2001 default and subsequent legal battle with holdouts took over a decade to resolve. Venezuela and PDVSA bonds were issued under different legal structures, are held by a wide array of investors and will likely take many years to be restructured. Bahrain, incidentally, is not part of the JPM emerging market bond indices as the country is classified as high-income (like Saudi Arabia, Qatar and Kuwait). Oman, however, is part of the indices as it is not considered a high-income country.

Sukuk defaults have additional legal layers of uncertainty versus a conventional bond (for discussions on Sukuk defaults and legal considerations, see here and here). The trust agreement is normally governed by English law, while the underlying lease agreements (the asset-based part of the sukuk) are governed by national law, Bahraini law in the case of its own sukuks. Finally, whether or not the structure is Sharia compliant, is subject to a third interpretation. The rating agencies do not seem to explicitly take into account the legal risks when rating the transactions. One of them, has stated that ‘XXX does not express an opinion on whether the relevant transaction documents are enforceable under any applicable law. However, XXX’s rating on the certificates reflects its belief that XXX would stand behind its obligations. When assigning ratings to the sukuk issuance, XXX does not express an opinion on its compliance with sharia principles.’

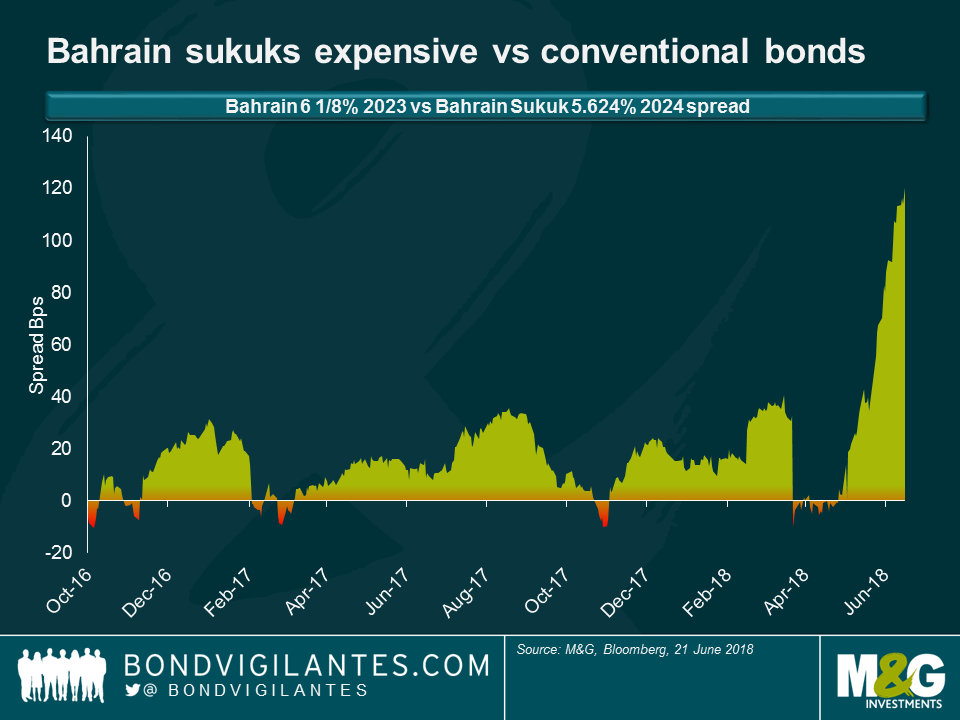

The oddity is that, despite being far more complex from a legal standpoint, spreads on Bahrain sukuks are currently far lower than the spread on its conventional bonds. That is largely because of the strong local support and demands for sukuks vs conventional bonds in recent weeks. Some local investors also cannot sell an instrument below par, as this will require them to account for its market to market loss and may also not be permitted according to Islamic finance. Many international investors have also invested in sukuks, but have the ability to arbitrage between sukuks and conventional bonds as they do not have the same market-to-market considerations or a preference for sharia vs non-sharia compliant instruments.

Given the potential legal complexities should a default occur, not to mention the underlying sovereign credit risk, investors are not being compensated for the risks on Bahrain’s sukuks.

We have already seen several corrections in credit markets so far this year, providing a good opportunity to analyse these episodes from a volatility perspective to see whether they have created good entry points into previously expensive markets. Finding a good entry point is just the first step though. Next, we must consider whether cash bonds, or CDS, look more attractive.

Tune in to this week’s episode as I share three reasons to be constructive on credit right now, and what other factors we need to keep in mind.

I was in Tokyo last week, seeing a mix of economists, JGB experts and clients. I was also awesome at karaoke, dressed as an astronaut.

The last time I was in Japan, over a year ago, I came away thinking there was a decent chance that the Bank of Japan would abandon its zero interest rate policy (ZIRP) as it was damaging banks’ profits, and sending a negative signal to Japanese households and businesses. At the time we were also seeing an uptick in core inflation and positive growth. It doesn’t feel like the BOJ has that view now. There’s no economic despair, but both growth and inflation have weakened, and Abe’s falling popularity raises the prospect of a new LDP leader later this year with less fiscally expansive views. We also have a dreaded consumption tax hike on the horizon – we know from past hikes that it means higher spending now, and a slump thereafter. There’s still plenty of good news too – unemployment rates even lower than the US, and a continuous rise in the female participation rate. In this 4 minute video from the Tachikawa Velodrome (no good reason, sorry) you can hear my views from Japan, and look at a) some cool charts, and b) keirin racers.

Finally, some anecdata. Did you know that post the 2011 tsunami, 43 of Japan’s 54 nuclear power stations remain offline. Before the earthquake they made up 30% of Japan’s electrical power needs. In order to save electricity the government introduced a policy called “Cool Biz”. From the start of June and throughout the summer months, all government and state workers are forbidden to wear jackets and ties to work (and private companies are encouraged to follow this policy too). In government buildings air conditioning is not allowed to kick in until the temperature is above 28 degrees centigrade. Ouch. We are all desperately leafing through health and safety legislation in the hope of being sent home when our ailing aircon here sees temperatures of 24 degrees…

The combination of the US-North Korea summit, crucial Brexit negotiations in the UK, mounting trade tensions, and a raft of central bank activity led some commentators to forecast that this would be the biggest week of the year. In fact, the beginning of the week was rather underwhelming, and it took a dovish ECB to really move markets. See how it all unfolded on today’s episode of Bond Vigilantes TV.

Emerging market currencies have been back in the spotlight in recent weeks after significant repricing – so it seems like a good time to lift the lid on how we think about currency trading. While there are many different aspects to take into consideration, there are three key factors – carry, valuations and fundamentals – that we keep front of mind.

With lower returns from bonds in recent years, currencies may have an increasingly important role to play in future, so watch BVTV to find out more.

Back in 2017, the economic outlook was increasingly rosy for the Eurozone. After years of ultra-loose monetary policy, a synchronised global recovery was in train. The Eurozone economy expanded apace, regularly surprising to the upside, unemployment continued to fall, the banking system had partially recapitalised and funding costs for corporates and sovereigns alike remained low on any measure. Even the inflation picture was showing some signs of a recovery towards the ECB’s definition of price stability. Behind the scenes, the ECB must have been increasingly confident that they had turned a corner and would begin unwinding their emergency monetary policy stance.

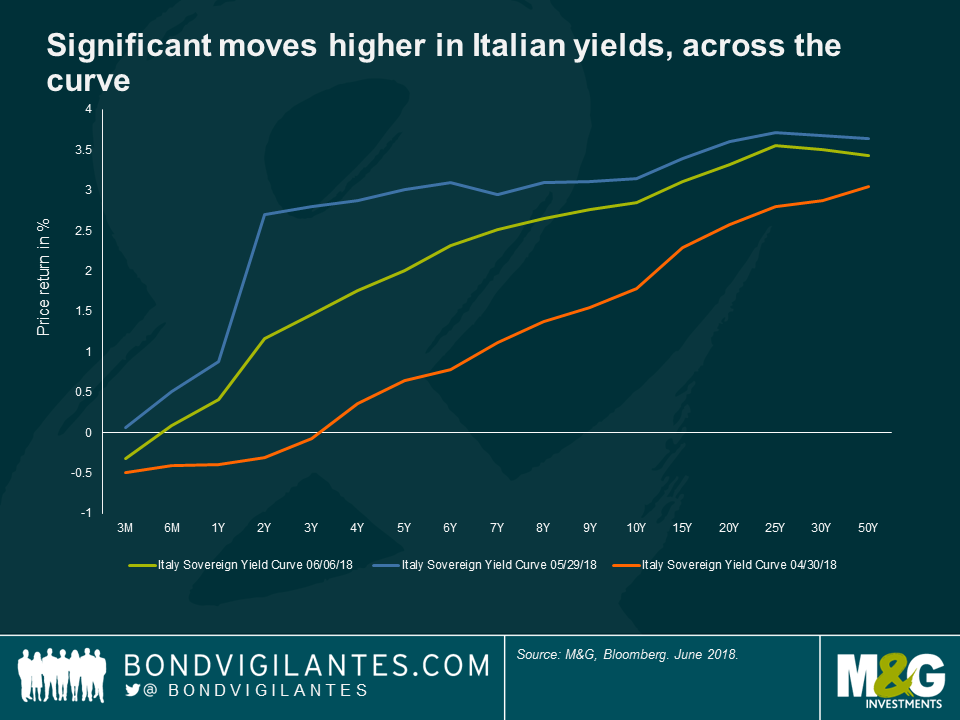

Less than a year later and their plans for normalisation have become more complicated. The economic data has weakened. And recent events in Italy have served to remind of the dangers of discounting populist politics. Whilst Italy is not leaving the Euro any time soon, the notable absence of credit risk priced into Italian assets a mere month ago was foolhardy. At the end of April 2018, ten-year Italian BTPs offered a yield below 2%, and all maturities below 3 years yielded less than 0%. A month later and BTPs yields have climbed dramatically.

The ECB will take comfort from the limited contagion to other peripheral markets thus far. Structural reforms, a stronger economy and better response mechanisms go a long way to explaining this. But dialling back stimulus in the face of increased market volatility and a tightening of financial conditions in Italy will leave the doves on the ECB Council uneasy.

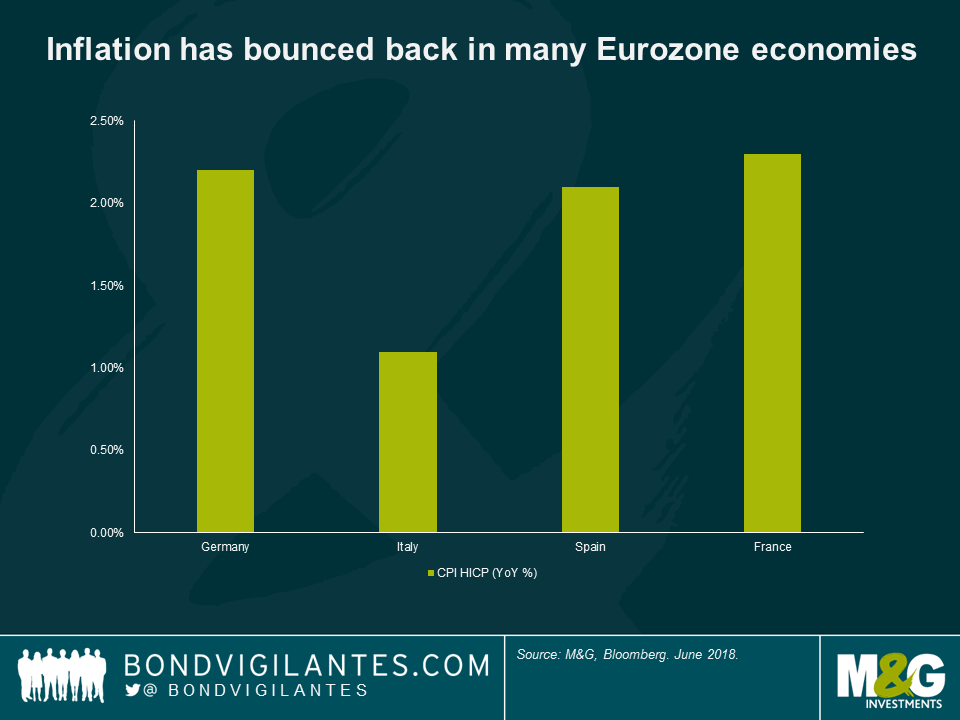

Jens Weidmann, Deutsche Bundesbank President, and other notable hawks will take a different view. They will point to recent German CPI prints of 2.2% and firming labour markets across the Eurozone. Savers continue to be forced to take either considerable term or credit risk to earn a positive real yield and there are some preliminary signs of excesses and imbalances building. Weak or practically non-existent covenant protection have become the norm in many high yield and leverage loan transactions. These concerns are not without merit.

Yet despite these risks, there is danger in tightening policy too early. Arnaud Marés at Citigroup, a former special advisor to Mario Draghi, argues that a central bank requires 300-400 basis points of rate cuts to be confident they can suitably stimulate an economy in the face of a significant economic slowdown. The chances of the ECB getting anywhere close to this watermark before the end of this current cycle are practically zero. Given the lack of fiscal firepower available to Eurozone governments, the ECB finds itself in an unenviable position. The onus remains on easy monetary policy to support economic growth in the Eurozone and the Central Bank is best served by erring on the side of caution. Put another way: they should wait until the they can see the whites of the eyes of inflation before normalising policy. Any tightening should be a gradual affair.

Mario Draghi’s term as ECB President expires in November 2019. He will want to be remembered for playing his part in pulling the Eurozone back from the abyss in 2012. He certainly will not want to be the ECB President who helped cause the very slow down his successor will face, with a largely empty box of tricks.

We interview the academic and TV presenter about her choices of history’s most important economists, and ask what we can learn from them in solving our current problems. Also, win a copy of Linda’s book in our competition.

From Adam Smith, to Robert Solow, Linda Yueh’s latest book examines twelve important economists and suggests how we might use their thinking as we tackle modern society’s economic problems. How do we explain low wages? Is the west likely to experience 1930s style debt deflation? Who wins in a trade war? In this short video I ask Linda about her choices and go on to get her thoughts on the state of modern economics. We’ve got another competition too – I think you’ll love this book and we have five copies of it to give away. You’ll find the question and how to enter below.

Competition question

Who are these two economists?

[This competition has ended]

Political turmoil in Italy and Spain, escalating trade tensions and, for good measure, unexpectedly strong US employment data – to say that markets had a turbulent few days would be an understatement. Taking a step back, here are three lessons I took away from last week.

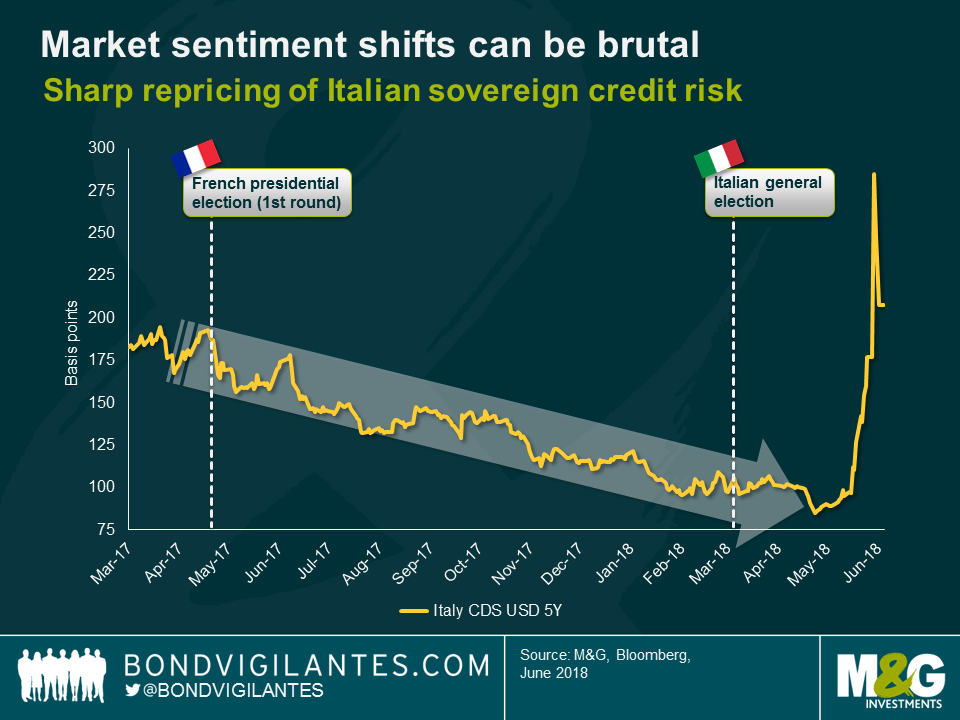

(1) Market sentiment shifts can be brutal

Political risks in the European periphery are real – a statement that might sound trivial now, but let’s not forget how much optimism there had been until very recently. After the first round of the French presidential elections in late April last year, Italy’s 5-year credit default swap (CDS) levels had moved essentially only in one direction (from close to 200 bps to around 100 bps), indicating that the market perceived Italian sovereign credit risk to have subsided substantially. Even the uncertainty created by the result of the Italian general election in early March this year didn’t change the constructive market sentiment. In fact, in late April and early May when credit spreads of corporate bonds were already drifting wider, Italian CDS contracts kept rallying to around 85 bps.

Only when the 5-Star/Lega coalition took shape and anti-Euro rhetoric dialled up, market sentiment made a sharp U-turn and switched into ‘risk off’ mode, pushing Italian CDS levels to around 290 bps. To put this into context, based on CDS levels, mid last week the market assigned higher sovereign credit risk to Italy than many emerging market countries, such as Turkey and Brazil, demonstrating just how violent market moves can be when sentiment changes abruptly.

For active investors these episodes of heightened volatility can present interesting opportunities though. The bearish tone last week quickly spread from Italian assets to other parts of the market due to indiscriminate shunning of risk. European financials and higher-beta securities, such as corporate hybrids, came under pressure, presenting appealing entry points to add exposure.

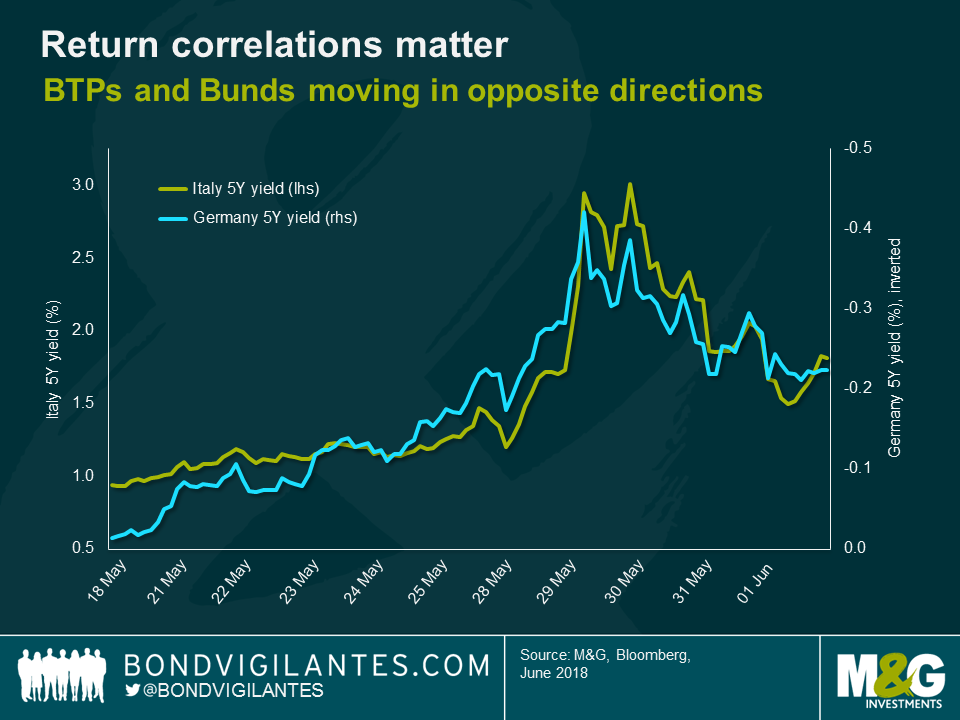

(2) Return correlations matter

The last couple of days have been a textbook example of asset class return correlations at work. Most noticeably, Italian government bonds (BTPs) and German Bunds have behaved pretty much like polar opposites. When Italian BTP yields soared last week, driven by fears of new elections and further gains for anti-Euro Lega, German Bunds lived up to their ‘safe haven’ image. Their yields plummeted, benefitting from the market’s ‘flight to quality’ impulse. Subsequently, when the Italian government finally formed, the BTP relief rally was met by rising Bund yields.

For any investor concerned about portfolio volatility and drawdowns, these correlation patterns matter. As unattractive as Bunds – and other core government bonds for that matter – may look from an outright yield perspective, they can be valuable portfolio stabilisers in times of violent ‘risk off’ market moves.

Against the backdrop of continued robust (enough) economic fundamentals and corporate default rates close to zero, I still see value in risk assets such as investment grade credit. However, considering that political risk in the European periphery is likely to remain elevated with the potential for further escalation of global trade tensions, it doesn’t strike me as unreasonable to maintain some exposure to Bunds and other safe haven assets such as the Japanese Yen, for diversification purposes.

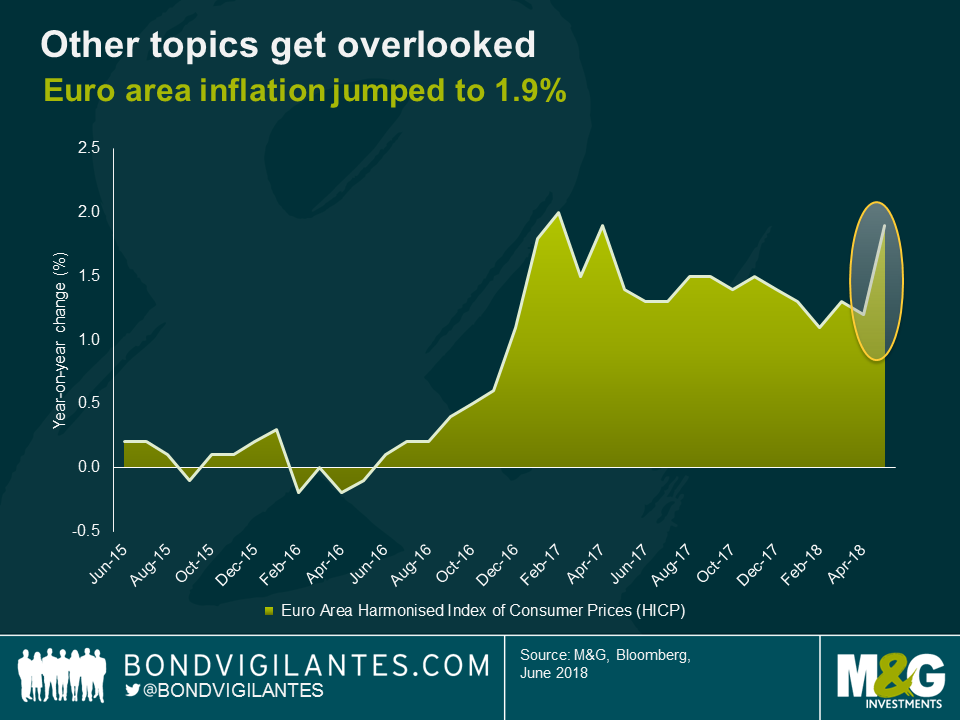

(3) Other topics are overlooked

When specific topics dominate conversations and market sentiment, it is very easy to be sucked into the relentless news flow. Every minute detail suddenly seems relevant and has the potential to move markets in either direction. In some sense, the recent fixation of the market on Italian politics gave me flashbacks of February 2016, when falling oil prices had been a similarly omnipresent and market-moving topic.

However, when preoccupied with a certain subject matter, the obvious risk is that other potentially significant developments might be overlooked. For instance, the release of the latest Euro area inflation data last Thursday barely made headlines, despite the big jump from 1.2% to 1.9% per year. Admittedly, surging energy prices and other transitory effects were the main drivers, while annual core inflation remained subdued at 1.1%. Nonetheless, an inflation print that perfectly meets the ECB’s price stability target of below, but close to 2% should at least raise a few eyebrows, considering the uncertainty around the future path of the ECB’s monetary policy stance.

Sign up to the Bond Vigilantes mailing list to ensure you never miss a great article from our expert Bloggers. We will email all new articles to your inbox, meaning you can stay on top of the world of Bonds.

I confirm that I would like to receive information about Bond Vigilantes and products and services from M&G Securities Limited.

We will use the email address and personal data you have shared with us to send you this information. For existing customers, submitting your contact details and requesting to receive this information from us, will replace any earlier choices you have made in respect of marketing information.

You can unsubscribe from marketing at any time, at which point we will not send any further marketing information to you, by selecting the unsubscribe link in all communications.