Panoramic Weekly – Trade war survivors: High Yield, FRNs

Despite a battery of central bank meetings, which left things more or less where they were – read: supportive of economic growth – global bond markets suffered from the ongoing trade wars, from rising oil prices and also as US data remained unconvincing, dragging down inflation expectations. Only about one quarter of the 100 fixed income asset classes followed by Panoramic Weekly posted positive returns over the past 5 trading days, mostly led by US High Yield (HY), which benefited from a strong earnings season and its traditional domestic focus. The asset class shrugged off US President Trump’s renewed threats to impose higher tariffs on Chinese imports, a move that continued to drag the renminbi lower, until China made it more expensive for investors to short its currency, partially containing the drop.

The renewed tensions lifted the US dollar, hitting Emerging Markets (EMs) and their currencies, especially those of countries that export to China, such as Chile, a leading copper producer. US foreign policy also impacted other nations, such as Russia, whose currency plunged 3.6% against the dollar after a group of US senators introduced new sanctions amid the country’s alleged interfering in US elections. Other EMs suffered on their own account: The Turkish lira sank 7% against the greenback and its 10-year sovereign yield spiked to 18% as, adding to recent political upheaval, the central bank said it will not meet its 5% inflation target for three more years. Some EMs fared better: Mexican government bonds were the five-day top-performing asset class, out of 100, up 1.5% and taking their 1-month return to 4%. Investors are favouring bonos on hopes that a new North American Free Trade Agreement (NAFTA) will be reached soon.

Sterling plunged almost 2% against the dollar, reaching a one-year low, on concerns the country will not strike a deal with the European Union (EU) to have an orderly exit next year. Despite Prime Minister Theresa May’s recent diplomatic efforts in the French president’s holiday villa, speculation is that Brussels-centred officials will have as much say in the final decision as Europe’s heads of state. She may have to swap the Cote d’Azur for Brussels next time.

Heading up:

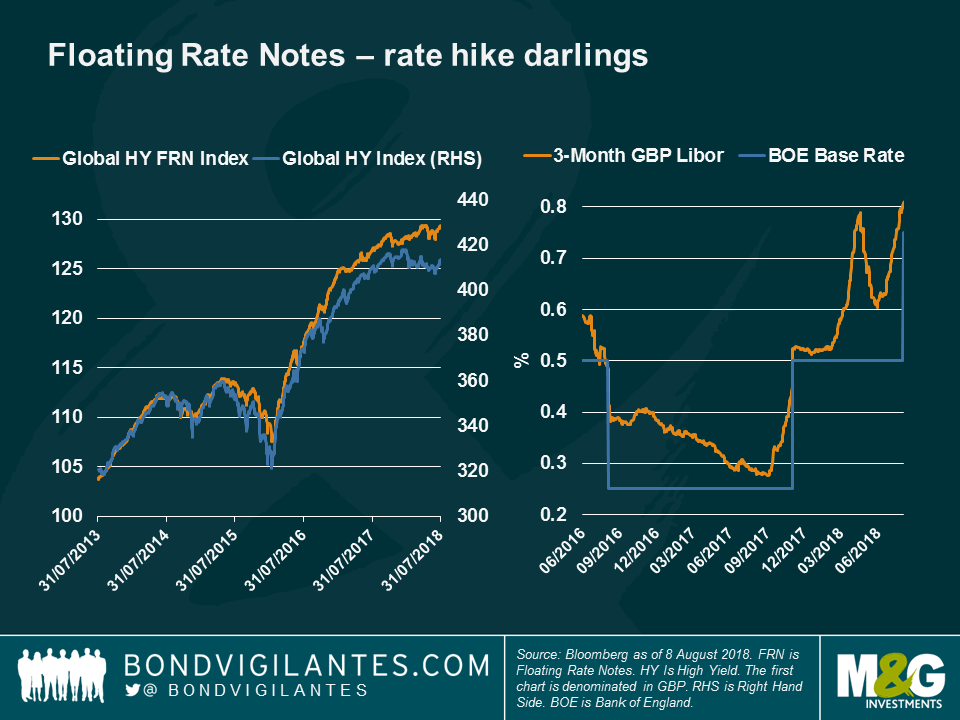

High Yield Floating Rate Notes (FRNs) – going for a hike? After years of trailing behind, HY FRN’s have now caught up and surpassed their fixed-interest paying HY pals: so far this year, Global HY FRNs have returned 1.3% to investors, compared with the 0.1% drop offered by Global High Yield names (both denominated in sterling). As seen on the chart, the decoupling between the two intensified towards the end of last year, when more central banks, other than the US Federal Reserve (Fed), started signalling that future rate hikes were on the table: the European Central Bank (ECB) unveiled plans to rein in its monetary stimulus, while the Bank of Japan (BOJ) has slightly widened the target trading range for the 10-year sovereign yield. FRNs are popular in a rising rate environment as their coupon is linked to a rate benchmark, such as Libor, which tends to shadow the central bank’s base rate. As seen on the chart, GBP-Libor rose following the Bank of England’s rate hike last week. Because coupons are reset periodically to match Libor, FRNs also have lower interest rate risk, reducing potential price losses when interest rates rise. A bigger coupon is also more likely to absorb any price drop derived from rising rates. To learn more about FRNs and the consequences of the BOE’s latest hike, watch M&G fund manager Matthew Russell’s recent video and read his blog.

Trump’s enemies – booming exports: Despite Trump’s loud and direct attempts to reduce the US trade deficit with leading exporters such as Germany and China, the fact is that the two countries’ exports continue to boom: Chinese exports rose at an annualised 6% in July, more than expected, while imports surged 21%, also more than forecasted. At the same time, Germany’s Current Account surplus rose for a third consecutive quarter, reaching 8.1% of Gross Domestic Product, one of the highest in the world. Germany and China’s export resilience raises questions about the true effect of the new US tariffs, which have so far hit China’s currency and the EM asset class, in general.

Heading down:

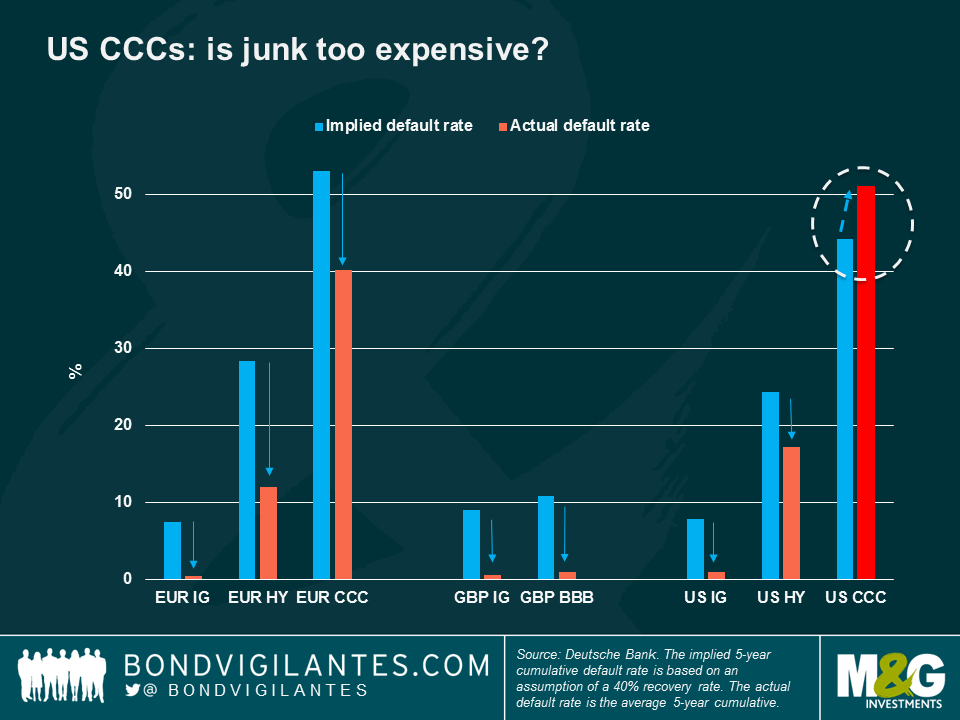

US CCCs – paying for junk: The lowest rated HY category has outperformed other HY rating brackets so far this year, as yield-hungry investors bought into the asset class encouraged by an improving US economy, a relentlessly increasing stock market and rising corporate profits – perhaps paying less attention to the usual red flags: Moody’s Investors Service defines Caa-rated debt as “very high credit risk, poor standing.” Still, investors have continued to buy the lowest US junk-rated debt, attracted by its high coupons, strong correlation to economic growth and traditional domestic focus, which makes it less exposed to international trade wars. The interest, however, has lifted valuations to a level that implies a 5-year cumulative default rate that is below the actual 5-year cumulative default rate: as seen on the chart, current prices imply that US CCC-rated bonds will default less than in the past. According to some market observers, such optimism is backed by a strong US economy; according to others, such positive view is unfounded, especially as US data has failed to show full traction; hence, they favour other, more pessimistically-priced asset classes, including some higher-rated HY brackets, as they offer higher credit quality and are also cheaper, on a relative basis. How much can investors pay for junk?

Italy – budget drama: Italian sovereign bonds lost almost 2% over the past five trading days, lifting the 10-year yield to 2.8%, the highest in Europe and about 1.5% above Spain’s. Investors have sold the country’s debt on concerns that the populist coalition government may increase spending in next month’s budget, widening its current 2.3% (of GDP) deficit. The country’s debt plunged after May, when some members of the ruling coalition questioned Italy’s presence in the Eurozone. Prime minister Giuseppe Conte reassured investors on Wednesday the budget will be serious and rigorous. Italian bond yields continued to rise.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

18 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox