Panoramic Weekly – World to US, China: Let them eat trade

While the US and China continued their ongoing mutual trade threats and stand-offs, other nations’ assets rallied on hopes that the trade wars will open opportunity for third parties. Indeed, and as seen below, Asian, African and European exports to China are on the rise, while those from the US are increasing at a slower pace. The potential negative effects of the trade wars, as well as protracted lukewarm data, continue to weigh on the US dollar, which fell against most world and Emerging Market (EM) currencies over the past five trading days. Not even Wednesday’s widely expected US interest rate hike and the Federal Reserve’s (Fed) signals that another hike may come this year, were able to lift the US currency.

European peripheral bonds performed best, fuelled by hopes that Italy will deliver a fiscally responsible budget and after European Central Bank (ECB) head Mario Draghi said inflation is building up. But it was Russian sovereign debt that performed best among a list of 100 Fixed Income sectors tracked by Panoramic Weekly: they gained 3.7% over the past 5 trading days on the back of surging oil prices – WTI oil surpassed the US$70 per barrel level for the first time since July after the OPEC decided not to increase output to offset Iran’s falling exports. The Argentinean peso, the Turkish lira and the South African rand all rallied more than 3% against the US dollar as the summer fears that triggered their sell-off continued to abate – and the greenback remained weak. Traditional safe-havens, such as long-maturity Treasuries, and German and Swiss government bonds, fell.

Heading up:

Global rates – all together now: The Czech and Norwegian central banks lifted their base interest rate over the past five trading days, a move that should not raise too many eyebrows among investors: as seen on the chart, and out of a list of 19 major countries or monetary unions, all but one are expected to have higher rates in three years’ time. The only exception is Mexico, which has been matching the Fed’s rate-rising path, pushing core inflation down to 3.6%, a level well below its present 7.75% rate, giving the central bank ample room for cuts. Elsewhere, though, the story is different: in Brazil, markets are discounting a 6.5% rate hike from present levels, mostly as a weak currency makes imports more expensive and as domestic electricity prices continue to rise. As investors and economists around the world sit and ponder how long the present expansionary cycle will last, some, including M&G fund manager Ben Lord, question whether poorly-timed rate rises may accelerate its end. Earlier this week, the Organization for Economic Cooperation and Development (OECD) cut its global growth outlook by 0.1% in 2018 and 0.2% in 2019, both to 3.7%, and said that world growth had hit a plateau. Click here to watch M&G fund manager Jim Leaviss’ summary of a recent IMF conference on government debt.

Brazil – the real deal: As the general election first round on Oct. 7 looms, markets are expecting a second round between far-right contender Bolsonaro, recovering from a backstabbing attack, and Haddad, the Workers Party candidate after a court banned the now imprisoned and former president Lula to run. This scenario, feared by many only a few weeks ago, seems to have earned investors’ blessings now: the real has strengthened 4% against the US dollar over the past 2 weeks on hopes that neither candidate poses big risks: Bolsonaro’s main economic adviser, the Chicago-educated Paulo Guedes, is seen as market friendly, while his left-wing contender has praised fiscal discipline. For more detail, read M&G portfolio manager Claudia Calich’s blog: Brazil’s election: What’s at stake?

Heading down:

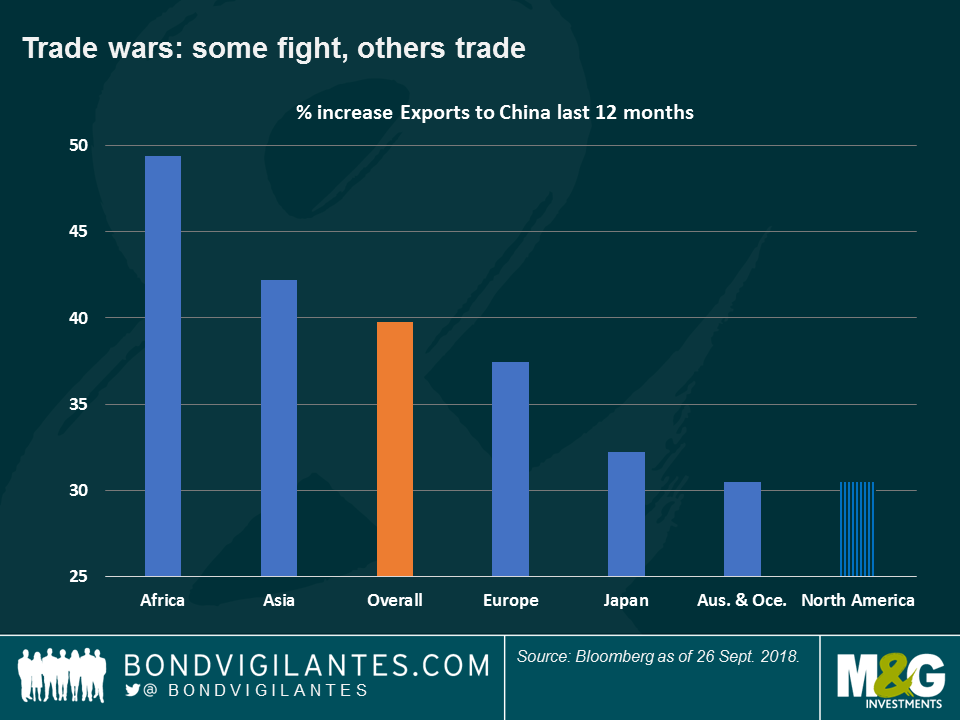

US exports to China – look over your shoulder: As the world’s two largest economies dig in their trade war trenches, other countries are rapidly aiming to fill the gap, increasing their exports to both. For instance, Brazil is selling more soybeans to China, at the same time that US grain exports to the Asian country have decreased. Asian countries are also selling more to their local leader, who is also keen to build a strong network with its neighbours, part of its “One road, one network” plan to bring the centuries-old Silk Route to the 21st century. In percentage terms, and as seen on the chart, African nations have increased exports to China the most, especially Libya and Congo. Libya’s top exports are oil, gold and gas. Other Middle Eastern or Eastern European nations, such as Slovakia, Kuwait, Uzbekistan and Qatar, have also more than doubled their exports to China over the past 12 months, a move in line with China’s efforts to sign oil contracts in renminbi as the country tries to internationalise its currency. On the other hand, US and UK exports to China grew below the average over the past 1-year period, although they were still ahead of Argentina’s, which is bottom of the list. For the effects of trade wars on EMs, don’t miss Claudia Calich’s “How vulnerable are EMs to Trade Wars?”

UK – Salzburg opera: Although not exactly written by Mozart, the Austrian hills offered plenty of political drama last week at the EU’s latest summit. As EU-UK negotiations over Brexit seem more distant than before, UK bookmakers are putting the chance of a no-deal Brexit at more than 50%. The uncertainty may keep a lid on UK gilt yields, which have sharply risen over the past month, with the 10-year yield trading at 1.59%, up from 1.27% barely one month ago. According to author Adam Tooze, Brexit is another example of the political backlash seen after the Global Financial Crisis – click here to watch a video interview.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox