Can General Electric ease the pain of BBBs?

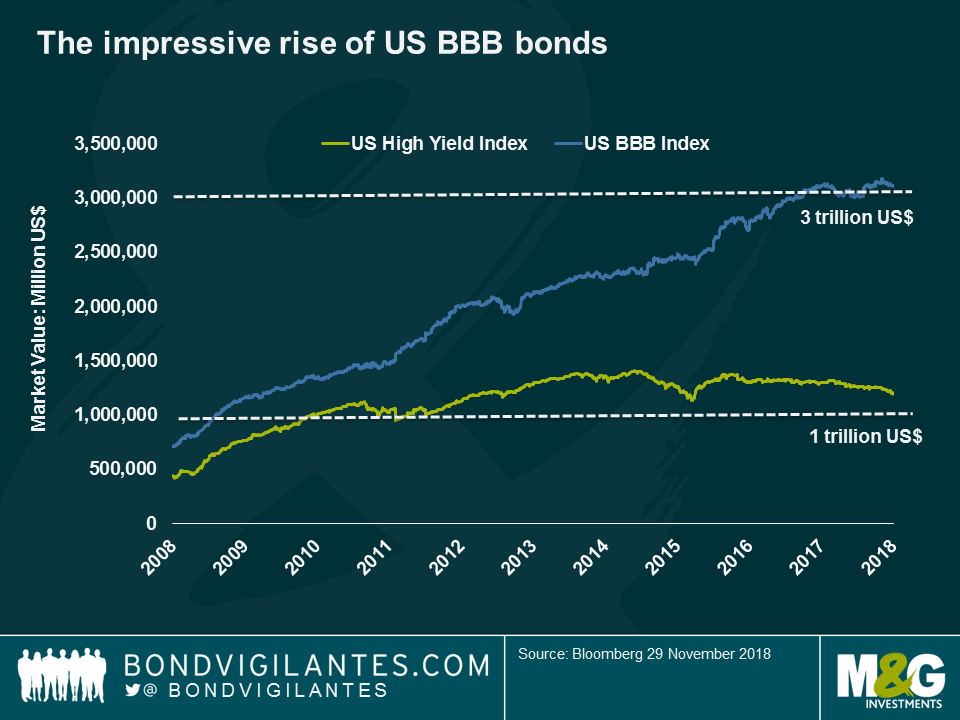

The positive and negative effects of central bank intervention after the 2007-08 financial crisis have been widely debated and are still – ten years on – not fully understood. For example, keeping borrowing costs artificially low for years has certainly helped spur economic growth (great), but by incentivising companies to take on more debt (not so great). The debt increase also makes me question if financial conditions have been kept loose for too long, as this has allowed businesses to leverage up, increasing credit risk. As seen in the chart, the lowest Investment Grade (IG) segment in the US corporate universe has grown to reach a whopping market capitalization of $3tn, almost half of the entire US IG asset class, and almost three times the size of the US High Yield market.

Whether the general sharp corporate debt increase will bring us closer to the next recession, only time will tell. But, as far as the increased concern over BBBs, how imminent is their risk? Does their recent sell-off reflect their true fundamentals?

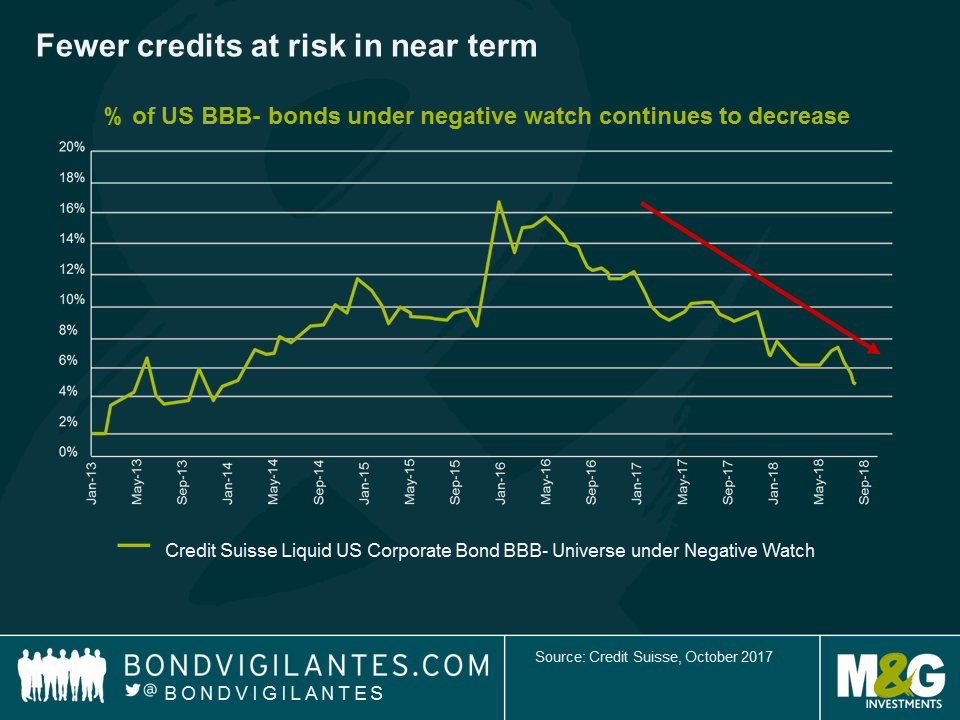

Let’s start by looking at the area most at risk, US BBB- bonds with a negative rating outlook, as those are closest to the HY frontier. As seen in the chart, this at-risk group has actually shrunk significantly over the past two years and is expected to continue doing so, according to Credit Suisse. At present the group only accounts for about 5% of the US BBB- universe, which points towards a low, near-term downgrade risk.

This reduction is mostly due to solid economic growth (world GDP is still expected to grow by 3.7% in 2019 and by 2.9% in the US according to the IMF), something which generally leads to rising corporate earnings and, ultimately, stronger balance sheets.

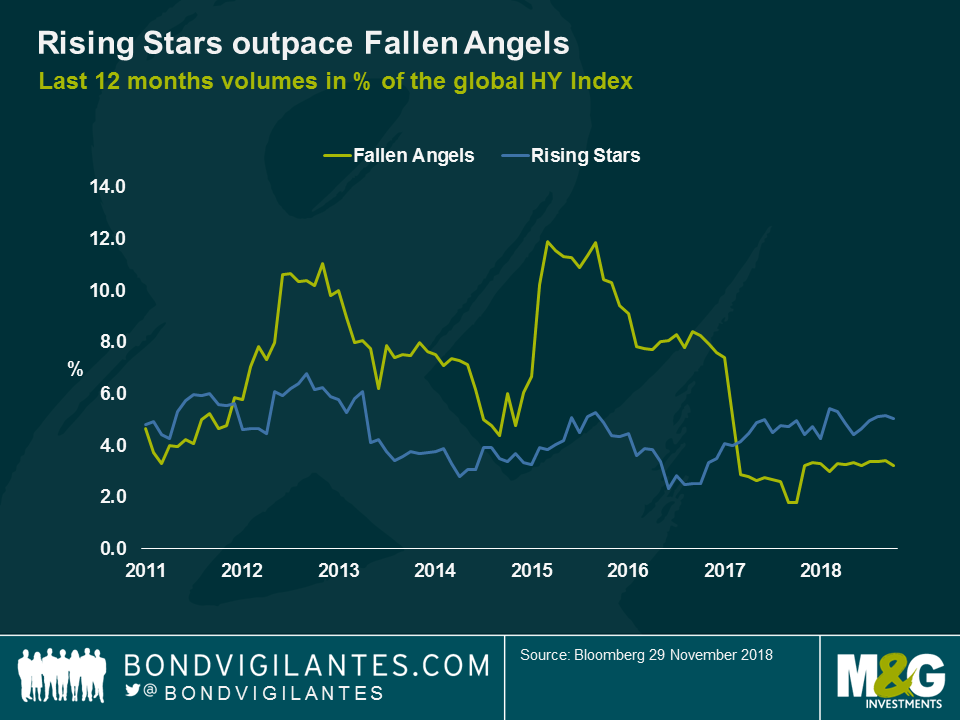

Whilst it is also true that Earnings Per Share (EPS) growth might have peaked this cycle following the US’s tax cuts, let’s not forget that year-on-year EPS growth in the third quarter for S&P 1500 companies is still tracking at a healthy pace of more than 20%. As seen in the chart, this positive backdrop has resulted in more Rising Stars (upgrades from HY into IG) than Fallen Angels (the opposite).

The Fallen Angel figure, of course, could balloon if one of these Angels happens to be a company with a large capital structure. One of the businesses that has lost its public single-A rating lately is US industrial giant General Electric – the 87th biggest company within the S&P 500 index, holding c. $50bn of notional debt – the majority of which could enter the HY market if multiple notches of downgrades occur. How immediate is this risk for investors?

GE downgrade fears are still speculative. The company is trying to shore up its cashflow and balance sheet, and may well retain its IG badge after all. Since liquidity, usually investors’ No. 1 concern, seems ample, the company is now focusing on improving its free cash flow and balance sheet structure. Companies at the lower end of the IG spectrum are indeed strongly incentivized to retain their credit ratings as a cut in long-term ratings from BBB- to BB+ materially lifts borrowing costs as some investors are prevented from holding Non-Investment Grade companies.

GE, however, still holds a BBB+ rating with stable outlooks from all three major credit rating agencies, leaving this flagship industrial group still a long way from junk. What will matter over the coming quarters is GE’s new CEO delivering on a promise of accelerated deleveraging, alongside turning around the structurally challenged power division. All of this amidst a backdrop of ongoing Department of Justice and SEC investigations, as well as some shareholder litigation.

To restore market confidence, GE needs to deliver a timely deleveraging and improve free cash flow in a sustainable manner. Concrete steps in this direction are already evident, with the dividend almost wiped out, and with an early stake sale in Baker Hughes ahead of a Healthcare exit on the cards for 2019.

Should management achieve this successfully, current valuations of this BBB+ business can actually offer an attractive buying opportunity for bond investors – and reduce some of the fears on the whole BBB spectrum.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox