Despite Brexit, Sterling credit holds up with a surprise front runner

With Brexit in every headline, it’s hard not to form an opinion on the possible outcome for the UK. Investors are getting increasingly edgy about the impact on certain asset classes, and I have read many articles predicting which sectors will do well in various exit scenarios. Sterling credit has remained healthy since the referendum, led by robust fundamentals and not by politics as the pound has been.

The sterling credit universe (as defined by the iBoxx £ Corporate Bond Index) is largely an internationally influenced index, much more correlated with what is going on in Europe and the US than in the UK domestically. Of the top ten issuers, only two have their full working operations within the UK (namely Heathrow Airport and Thames Water), while the top issuer by index weight (3.3%) is French utility company, EDF. Which just goes to show the international nature of the index – and indeed perhaps some of the reason it has proven to be robust, with only 49.8% of the index British.

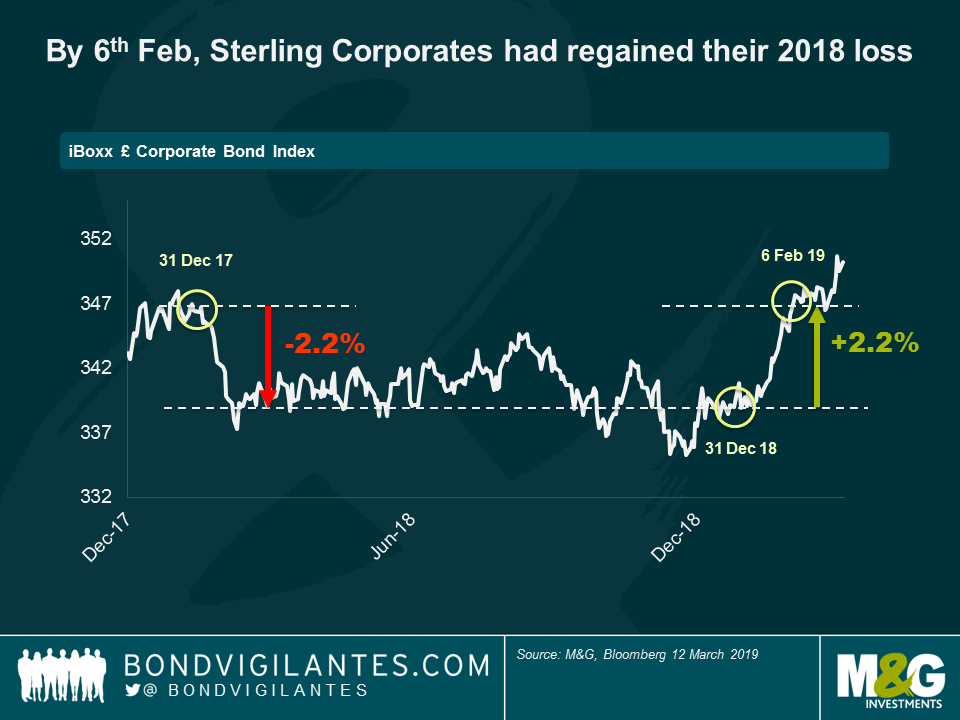

Since the beginning of the year the index has returned 3.3% (at 12 March 2019), while 2018 saw negative returns of –2.2%. By 6th February, the sterling corporate index had regained all of its 2018 loss. The credit wobbles of Q4 18 offered good value and some better entry points to investors, particularly in the financials sector. The sterling financials index returned 3.3% year to date (12 March 2019) – clearly the market has been somewhat assisted by recent headlines of potentially softer Brexit scenarios. We have seen heavily oversubscribed books for recent sterling deals, highlighting the difficulty in buying inventory with dealer positions low.

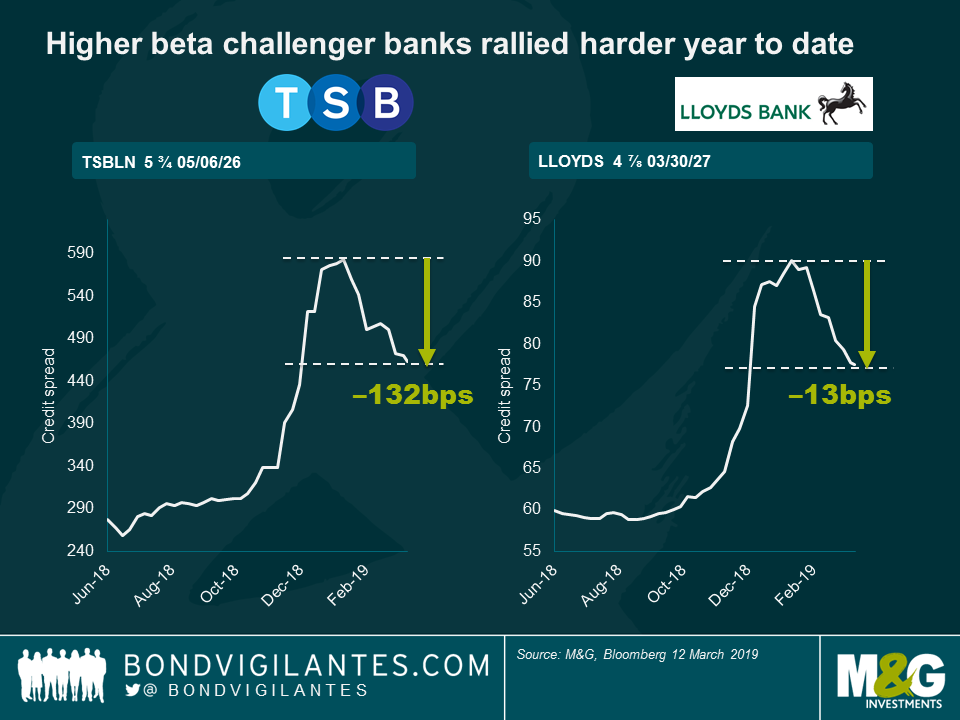

Looking more closely at the companies which have performed best year to date, we observe that it’s the challenger banks which have rallied most. Challenger banks are smaller, recently created banks which distinguish themselves from more established banks by modernising technology which aims to avoid the cost and complexities of traditional banking. Some such names are spins offs from larger institutions following divestment or wind-downs of larger, mainstream banks.

In the current environment dealers are looking for higher beta opportunities and, having underperformed in 2018, challenger banks offered some attractive yields. Take TSB for example (a divestment of Lloyds, sold to Spanish bank Banco Sabadell in July 2015). Year to date, the spread compression is much more significant than in the case of Lloyds, an established name in the UK banking sector. Does TSB pose more risk? Yes, of course, but with its low credit risk business model (they are mostly exposed to prime UK residential mortgage loans, which historically have borne very low loss rates through the cycle), one could make the case that investors are being well-compensated for this in the spread.

Investors have come to expect a surge in issuance from mainstream banks in the first quarter but dealers are still awaiting significant action in the primary markets so far this year. In the meantime, investors need to park their cash somewhere. While they are naturally higher beta credits, perhaps this is one reason that challenger banks continue to rally harder than their mainstream counterparts (Lloyds 4.875 27’s now offer 1.8% versus a high of 2.1% in January – compare TSB 5.75 26’s at 5.3% versus 6.6% in January).

In a risk on environment, and with issuance less than expected, the Lloyds bond returned 1.16% year to date on a price return basis versus TSB’s 2.55%. Not necessarily a return profile you’d expect from a sector worried about the implications of Brexit.

Over the coming weeks we will find out what Brexit looks like but one thing is for sure: sterling credit – and particularly financials – remains constructive and risk on. With a surprisingly robust UK economy, sterling credit dominated by so many global businesses, and expected issuance not materialising, there are perhaps good reasons to put cash to work in sterling credit and in higher beta financials. It might be the right time to invest in credit that has previously had a “no deal” premium built into spreads which is looking decreasingly likely to materialise.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox