This time is different: a stay at home Flash Crash t-shaped recession

Whenever there is the threat or the reality of recession, it usually follows a typical pattern. It is engendered by tight financial conditions, a real or market bubble bursting, a dramatic rise in the price of oil, or a combination of the above. This time it is different: a stay at home recession.

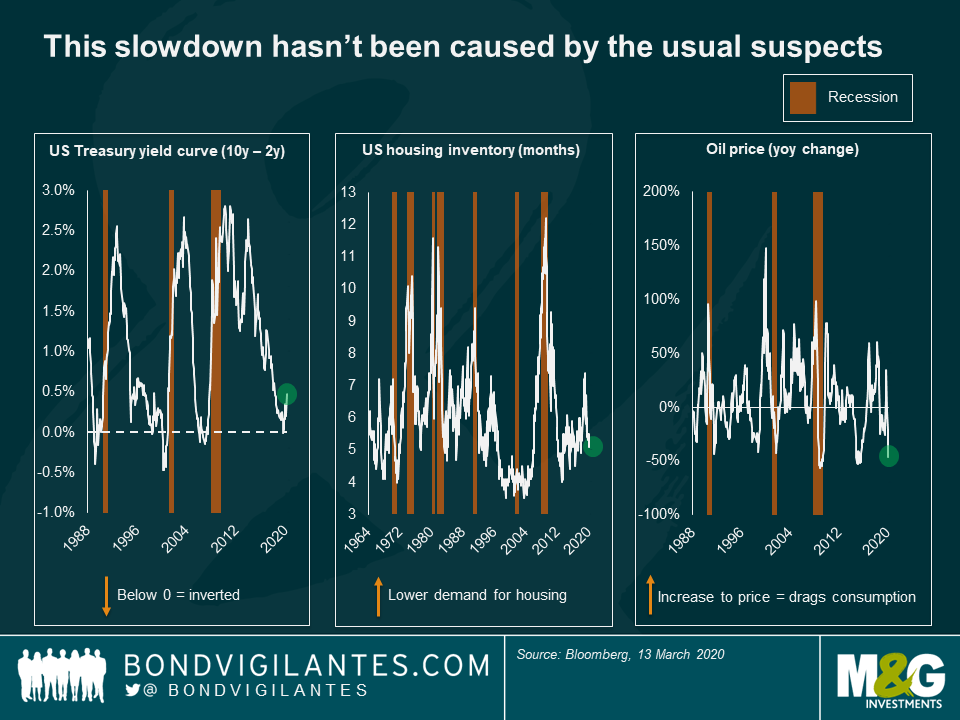

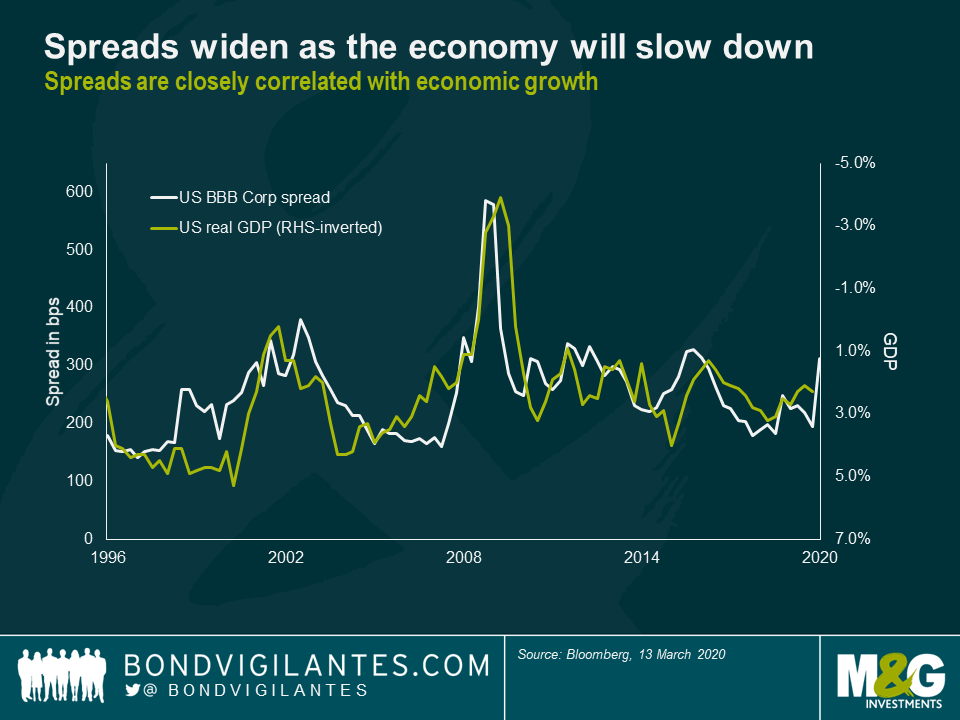

The 2020 economic slowdown isn’t due to any of the usual suspects, namely the US Treasury curve inverting, the US housing market slowing or a high oil price. Rather, it is due to the virus outbreak leading not to a policy error, but a policy-led recession. In response to the virus outbreak, governments around the world have reacted understandably by encouraging their populations to curtail day-to-day activity. For example, I am writing this on my usual journey in and the car park and train are deserted. We will all have our own anecdotes of this dramatic change to daily life. This will result in a collapse in GDP. Credit spreads are closely correlated with economic growth, and spreads have already reacted aggressively to lower GDP expectations.

Fortunately, we enter this recession with already very accommodative monetary policy from central banks. Monetary policy takes about two years before we can see its effect in the economy. For example, we saw a slowdown in 2018 a couple of years after the Fed hiked rates into 2016. Now the economy has a lead, the Fed having stopped hiking rates in early 2019 and then proceeded to cut. While the ECB has limited scope to react due to its already rock bottom policy rate, the Fed and BoE do.

There are three stages to a recession – how is this one going to be different?

Stage 1: into recession

This is the most certain recession we have ever seen: we can all observe the dramatic fall in daily activity around us. Discretionary spending has been curtailed, and the most expensive discretionary spend, travel and tourism, has been hit the most. This is not a slow evolution where individuals gradually discover the new economic reality, this is an in instruction to everyone to stop consuming. This instruction is worldwide and instantaneous, something that has never happened before.

Recessions are usually described as V or U shaped. The first leg of this recession will resemble the U shaped form. It will be vertical and dramatic, and the largest ever collapse in GDP on a weekly and monthly basis in many countries.

Stage 2: end of recession

Given that the recession’s speed and depth is due to the virus and resultant government action to prevent us mingling, we have an unusually strong idea of when and how the recession ends. This virus appears to exhibit seasonal patterns like influenza and, once it has made its way through the population, immunity can build up. At some point therefore, presumably within three months, government policy will be changed and we can potentially return to normal behaviour. This bounce back will be enormous as the population is no longer told to stay at home. Thus, economic data will show a rapid rebound: it will not be a V or a U, rather it will look like an l. It will be the biggest ever jump in GDP on a weekly and monthly basis in many countries.

Stage 3: post recession

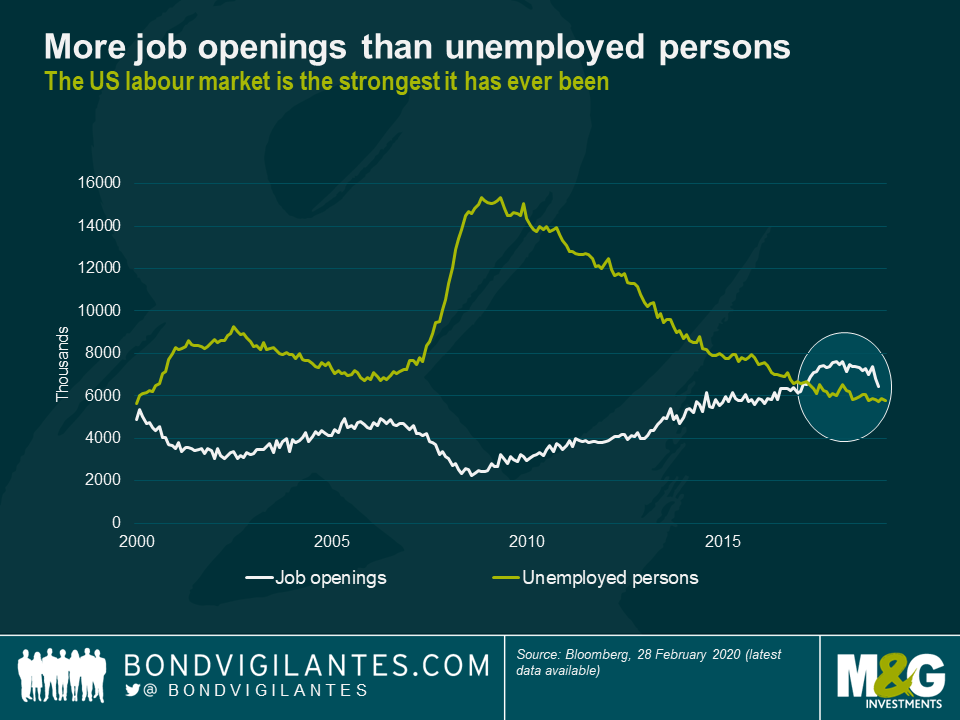

This dramatic collapse and recovery will cause some longer term damage to the economic system. Firstly, from an overall business and personal confidence level, and secondly due to the unprecedented nature of the severe short term pain of the recession. Human behaviour may change, and vulnerable companies relying on short term discretionary spending will have been weakened and potentially permanently impaired. While some consumption will just be deferred (buying a car, for example), much will be lost (going to the cinema). On the positive side, unlike most other recessions, developed economies exhibit very low unemployment and considerable numbers of the population will remain employed and many businesses can remain stable. Hopefully there will be fiscal support for those who struggle more.

Therefore, post recession growth will return to normal but initially will be unlikely to regain its previous levels. This makes this type of recession t shaped: a sharp pull down, a sharp rebound and then back to the normal economic cycle, at probably a lower level than before unless the policy response overwhelms the downdraft, in which case we return to where we were before (T not t). For the economies most affected, this t will be a larger downdraft and bounce back, though the permanent damage may be more. For credit investors during this time, it is important as always to differentiate between credit qualities. While high yield defaults can be expected to rise (previous recessions have seen up to 30% of high yield companies defaulting over five years), investment grade companies are so-called because they should survive (with closer to 2% of companies defaulting over five years in times of stress).

This recession is different. We know why it is happening, have a far clearer idea than usual of its length and can strongly postulate how it comes to an end. Different governments and central banks are therefore working on measures to get us through the short term GDP flash crash. This has allowed the authorities to act in a bold and aggressive manner that is in itself different. This unprecedented stimulation is likely to stay in place post the shock, to ensure that the economy has a chance to get to an economic level as near as possible to its previous level.

The value of investments will fluctuate, which will cause prices to fall as well as rise and you may not get back the original amount you invested. Past performance is not a guide to future performance.

19 years of comment

Discover historical blogs from our extensive archive with our Blast from the past feature. View the most popular blogs posted this month - 5, 10 or 15 years ago!

Bond Vigilantes

Get Bond Vigilantes updates straight to your inbox